Inflation/Deflation

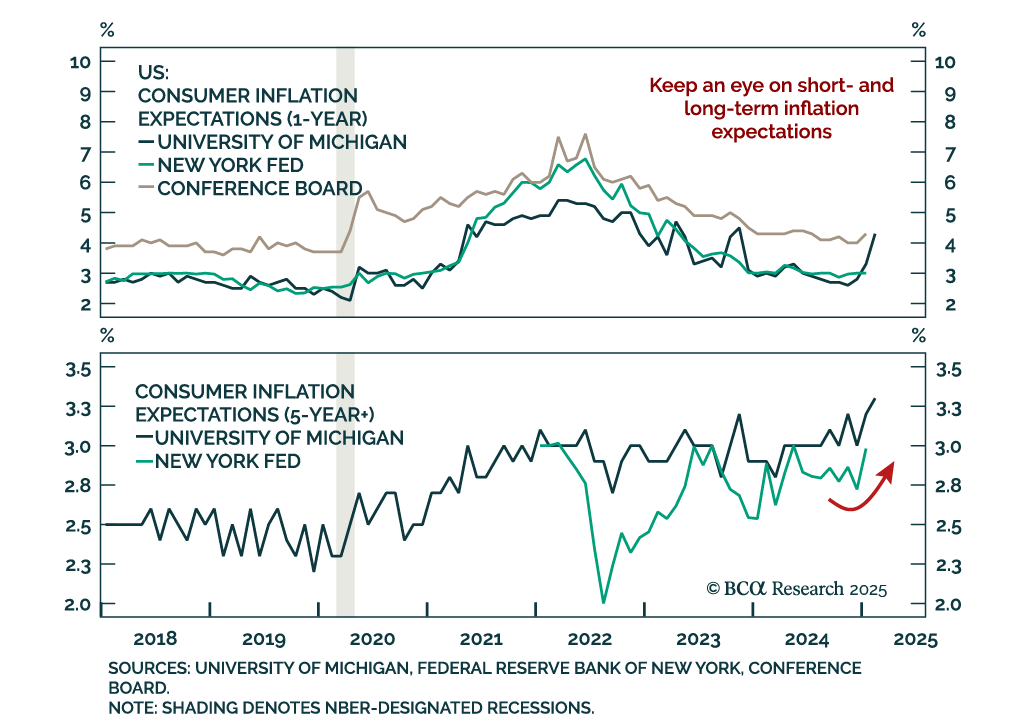

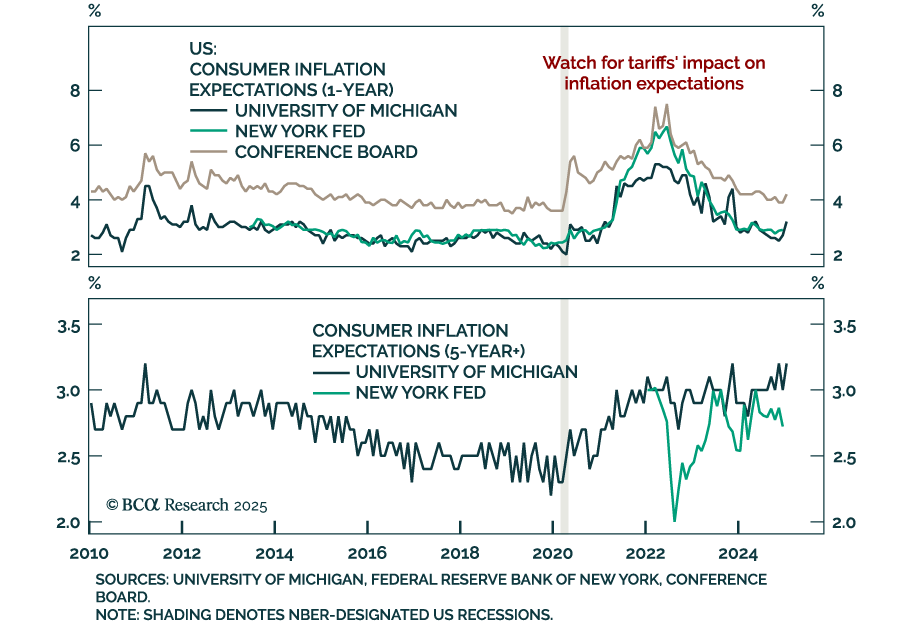

The New York Fed’s Survey of Consumer Expectations’ 1-year and 3-year inflation expectations were unchanged in January. Five-year ahead expectations however increased, as did expectations for staples inflation, while spending expectations…

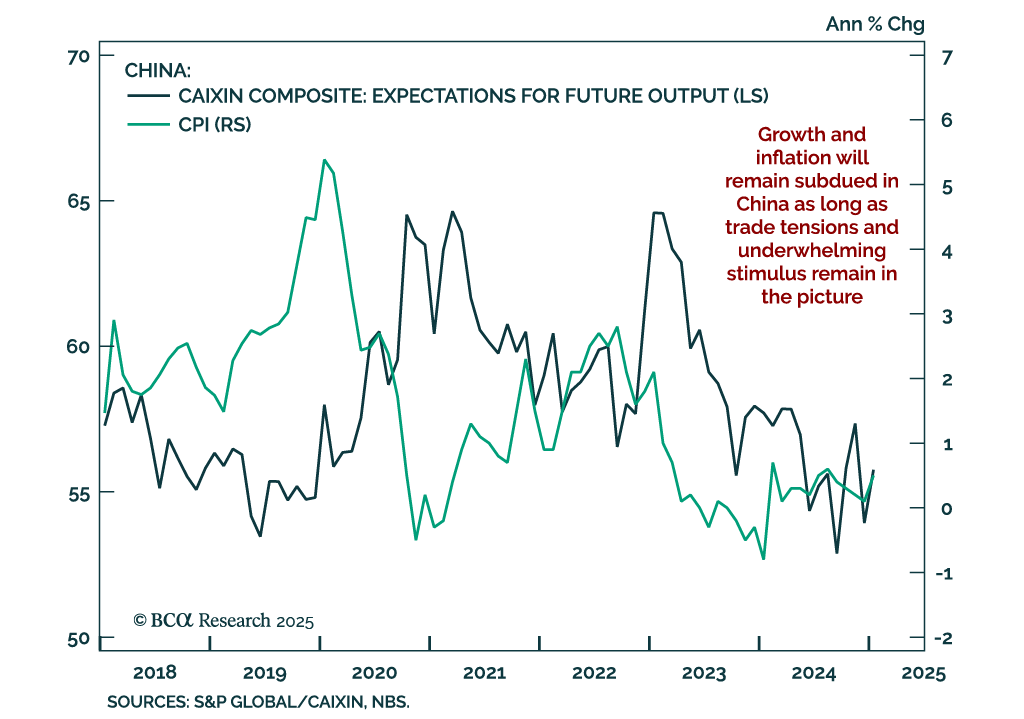

China’s January consumer prices rebounded to 0.5% y/y, and producer price deflation was unchanged at -2.3%. China’s first quarter data tends to be distorted by the Chinese New Year, as its variable dates shift consumption peaks around without a clear pattern.…

Our Emerging Market strategists published a follow-up piece to their Bessenomics note where they assess the new Treasury Secretary plan’s impact on markets. Lower interest rates are central to Bessenomics. The Trump administration is expected to pressure…

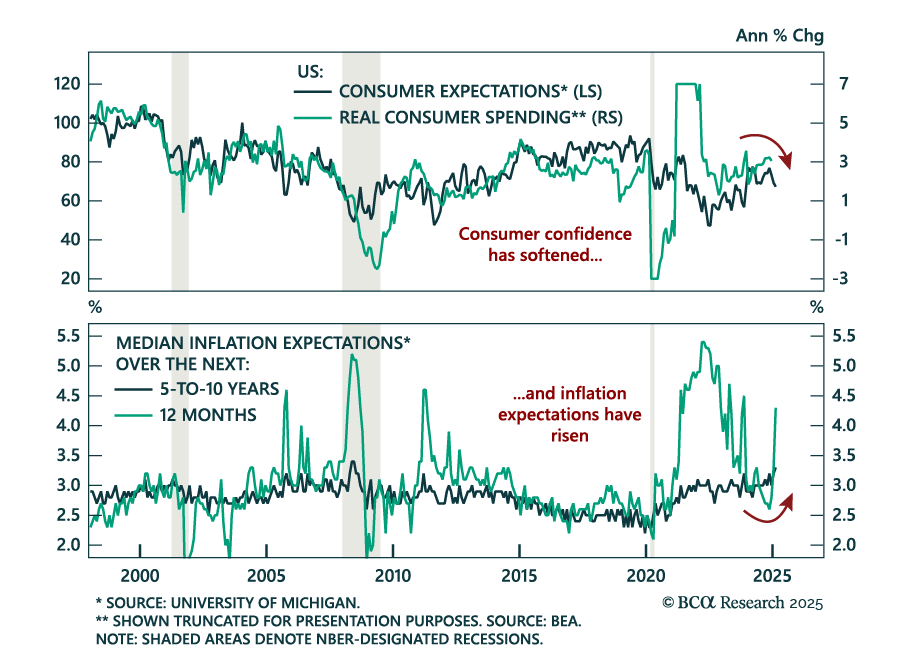

The preliminary February University of Michigan Consumer Sentiment Index missed estimates, falling to 67.8 from 71.1 in January. The decrease came from both expectations and the assessment of current conditions. Measures of 1-year and 5-10 year inflation…

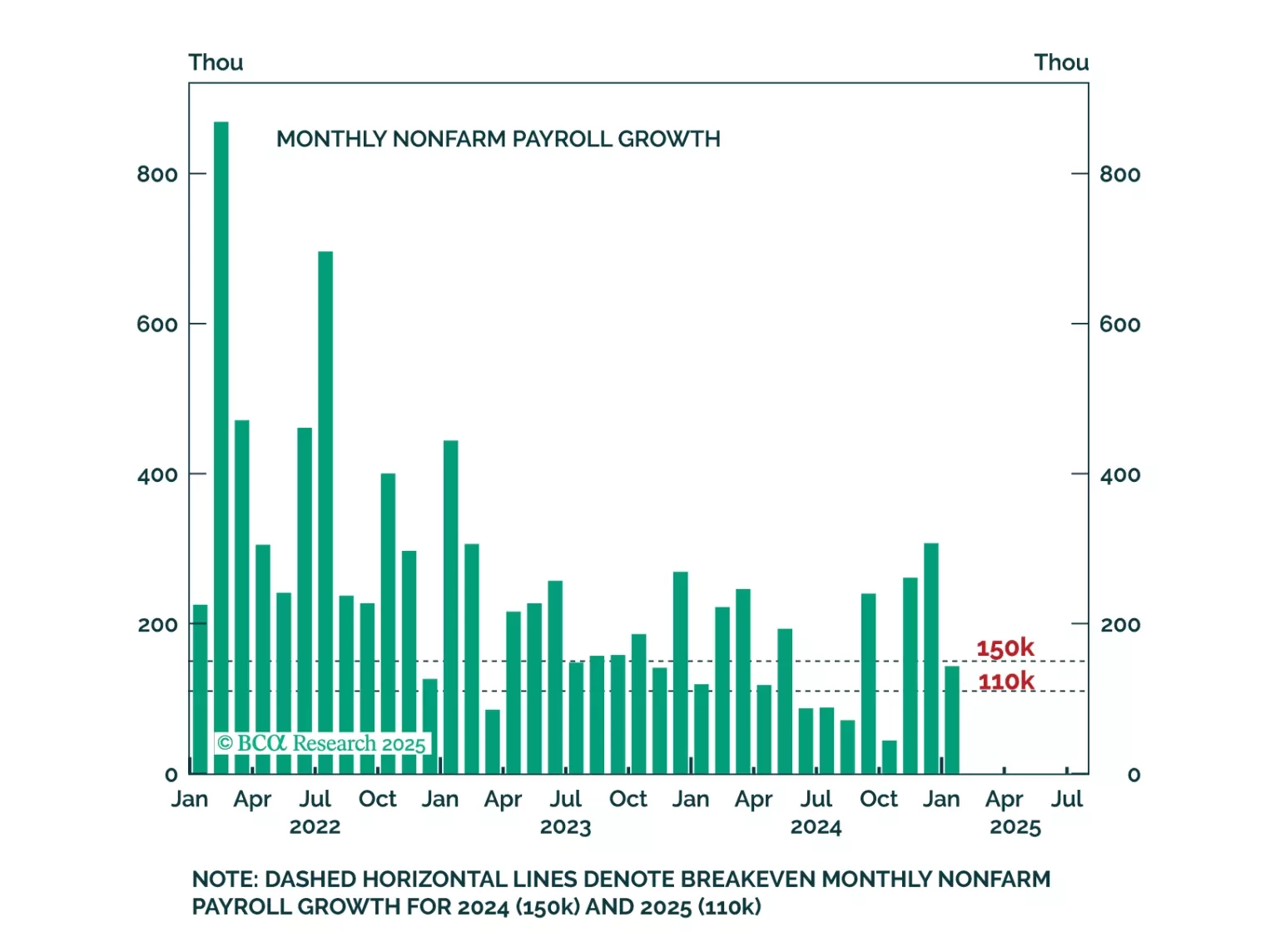

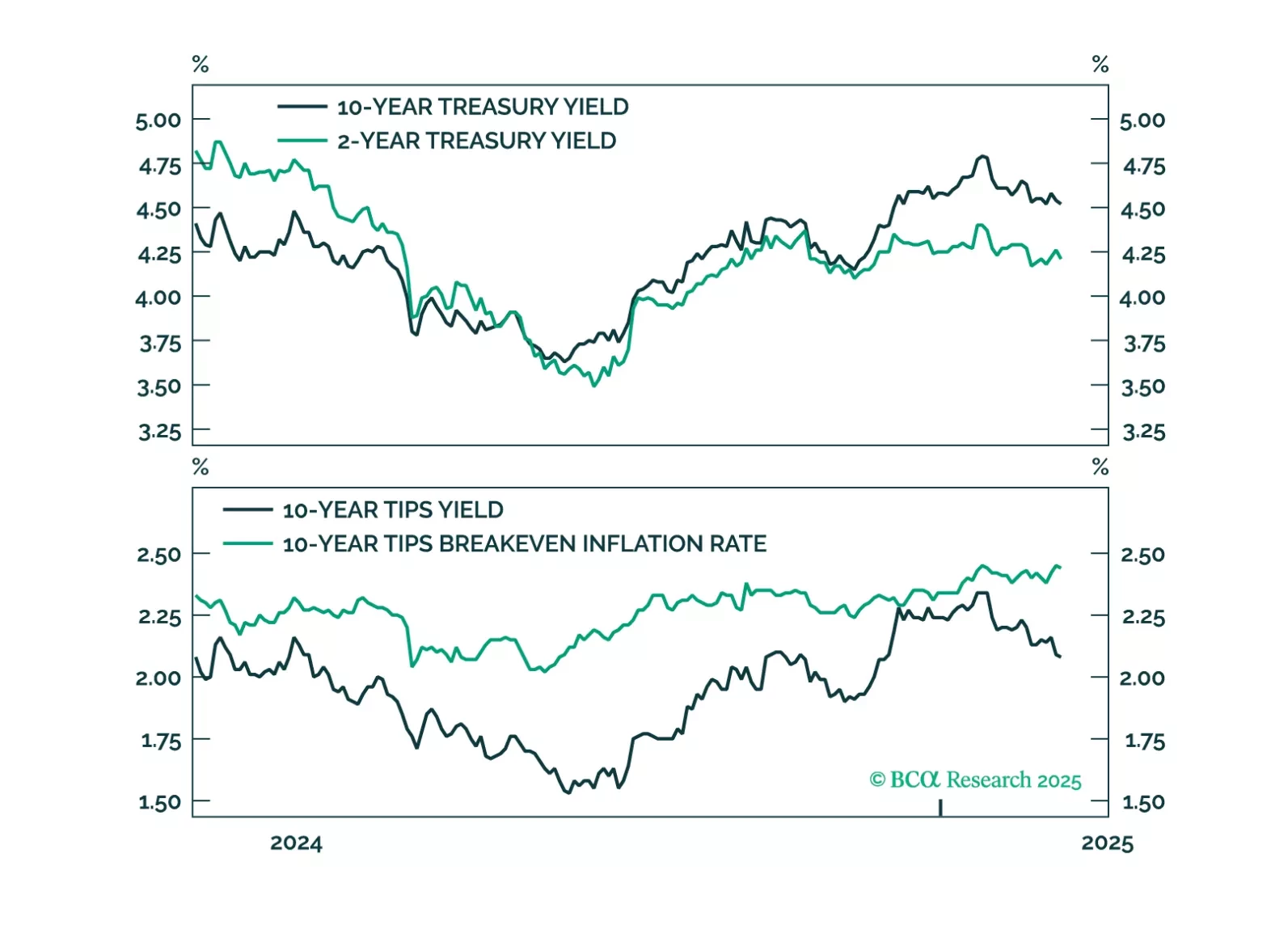

Some thoughts on this morning's employment data and Treasury Secretary Bessent's recent attempts to talk down the 10-year Treasury yield.

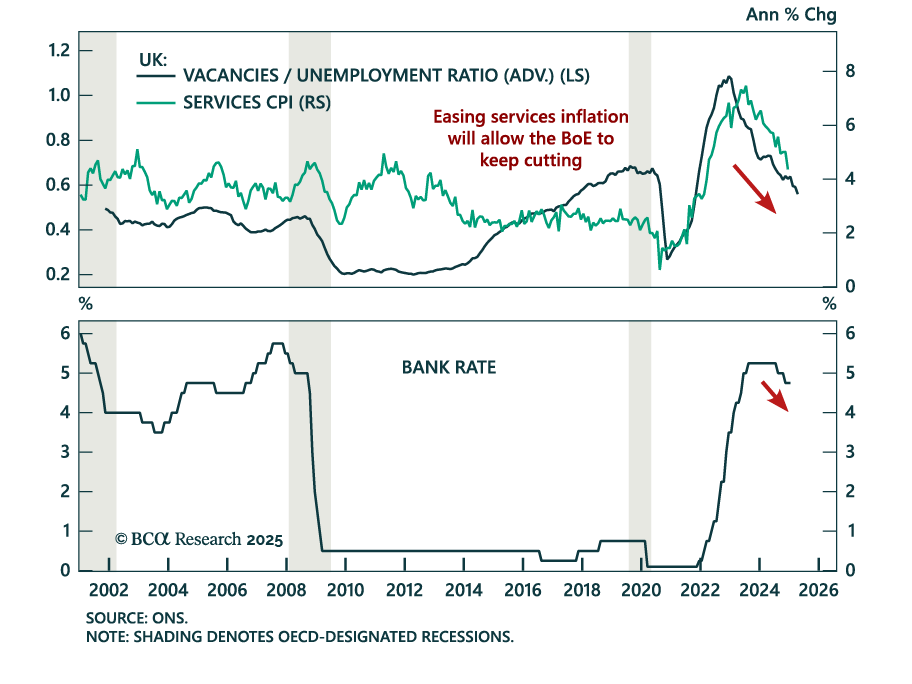

The Bank of England cut its policy rate by 25 bps to 4.5%, with two members of the MPC voting to cut 50 bps instead. The BoE acknowledged “substantial progress on disinflation”, driven by a tight policy stance and stabilized inflation expectations. The dovish…

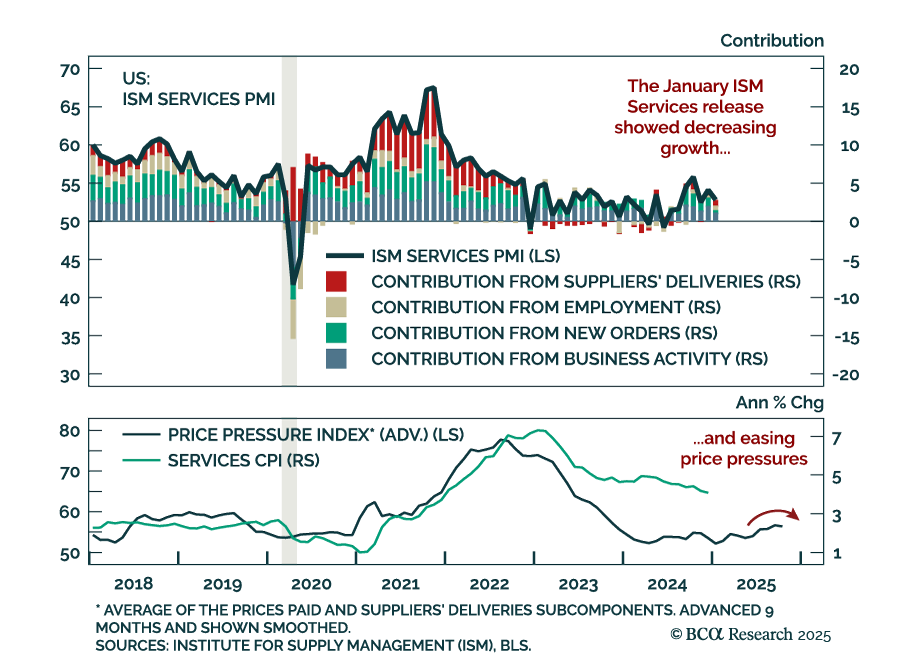

The January ISM Services missed estimates, decreasing to 52.8 from 54.0 in December. The move was driven by activity components, while employment and suppliers’ delivery times increased. Additionally, the prices paid measure decreased, reversing the…

Our Portfolio Allocation Summary for January 2025.

Trade tensions muddy the outlook for global central banks. The 2010s were an era of low growth and low inflation that called for easy monetary policy. The post-COVID era has been marked by overheating and high inflation calling for tight policy. The second…

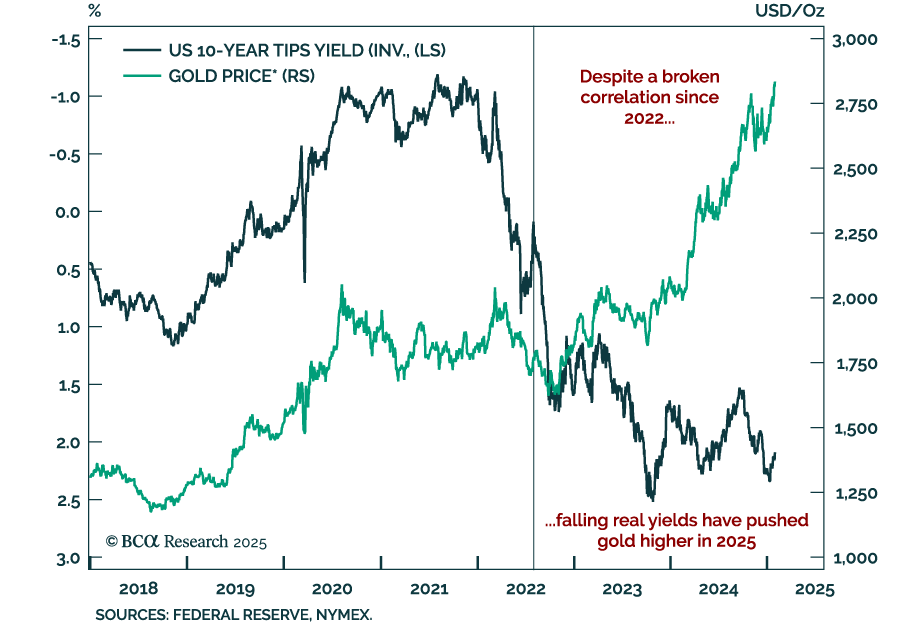

While the US dollar has outperformed every single DM currency in the past few months, the only monetary asset it did not outperform is gold. The greenback is up between 5-10% against DM currencies since September of last year, but down by more than 8% vs.…