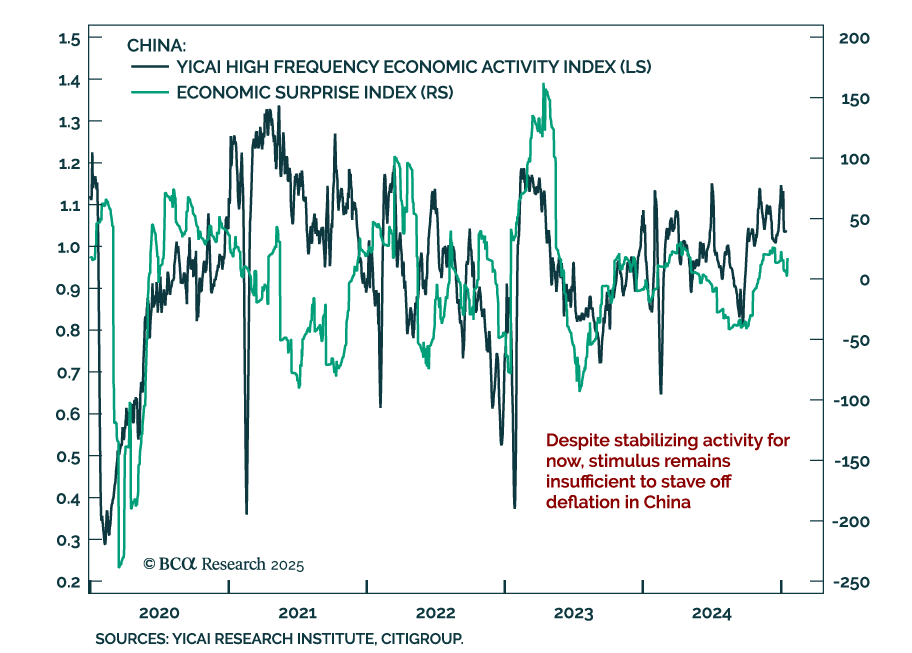

Inflation/Deflation

Global risk assets are engulfed in a wave of euphoria, which is pulling Europe higher along the way. However, risks still abound. How should investors adjust their allocation to Europe under these highly uncertain conditions?

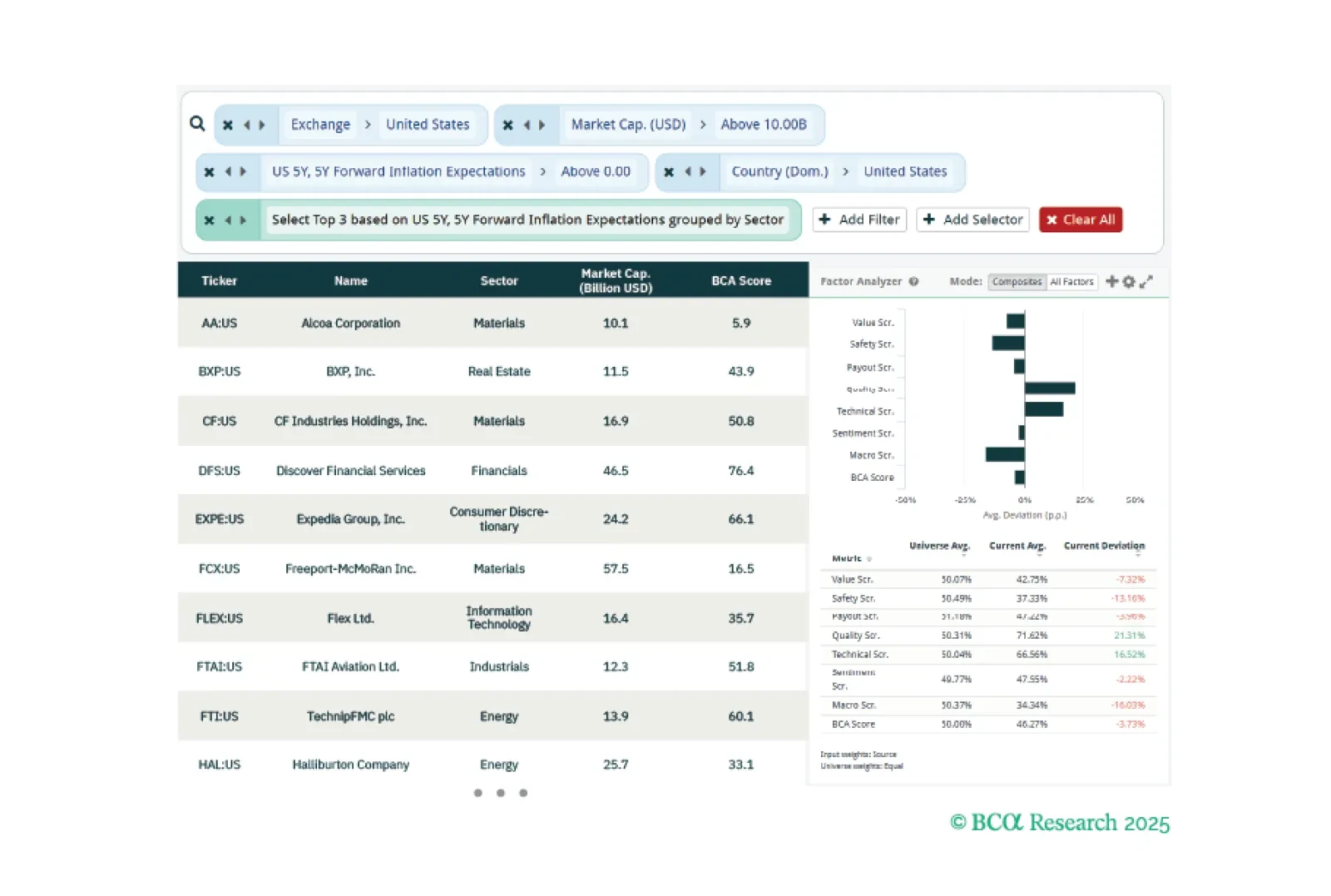

This week, our screeners cover views on Trump 2.0, defensive US equity sectors, and a pullback in Singapore equities. Our first screener aims to hedge longer term inflation risks that Trump 2.0 will likely generate, targeting US equities that are highly correlated with future inflation expectations. Our second screener identifies several defensive sectors that are worth consideration, in case of a tactical pullback in US equities. Lastly, we pick out Singapore stocks that are cheap and high safety, should a pullback occur in the local bourse given weakening macro and technical conditions.