Inflation/Deflation

The Federal Reserve’s Beige Book shows a modestly growing economy imbued with post-election optimism, while highlighting some caution about employment. The latest Beige Book is in line with other sentiment indicators showing modest growth but increased…

The November Caixin services PMI ticked down to 51.5, which along with a rising manufacturing PMI pushed the composite up to 52.3 from 51.9. Components such as new orders and employment also ticked down, and output prices fell to 49.6. Services also weakened…

Our European Investment Strategy and GeoMacro Strategy teams published a joint report, digging into the structural challenges behind Europe’s economic underperformance, while pointing out to potential turnaround opportunities. Europe’s prolonged…

The November ISM Services PMI missed expectations, declining to 52.1 from 56 in October. All subcomponents declined, with new orders falling from 57.4 to 53.7. Employment also weakened but remains in expansion, while price pressures were roughly unchanged. …

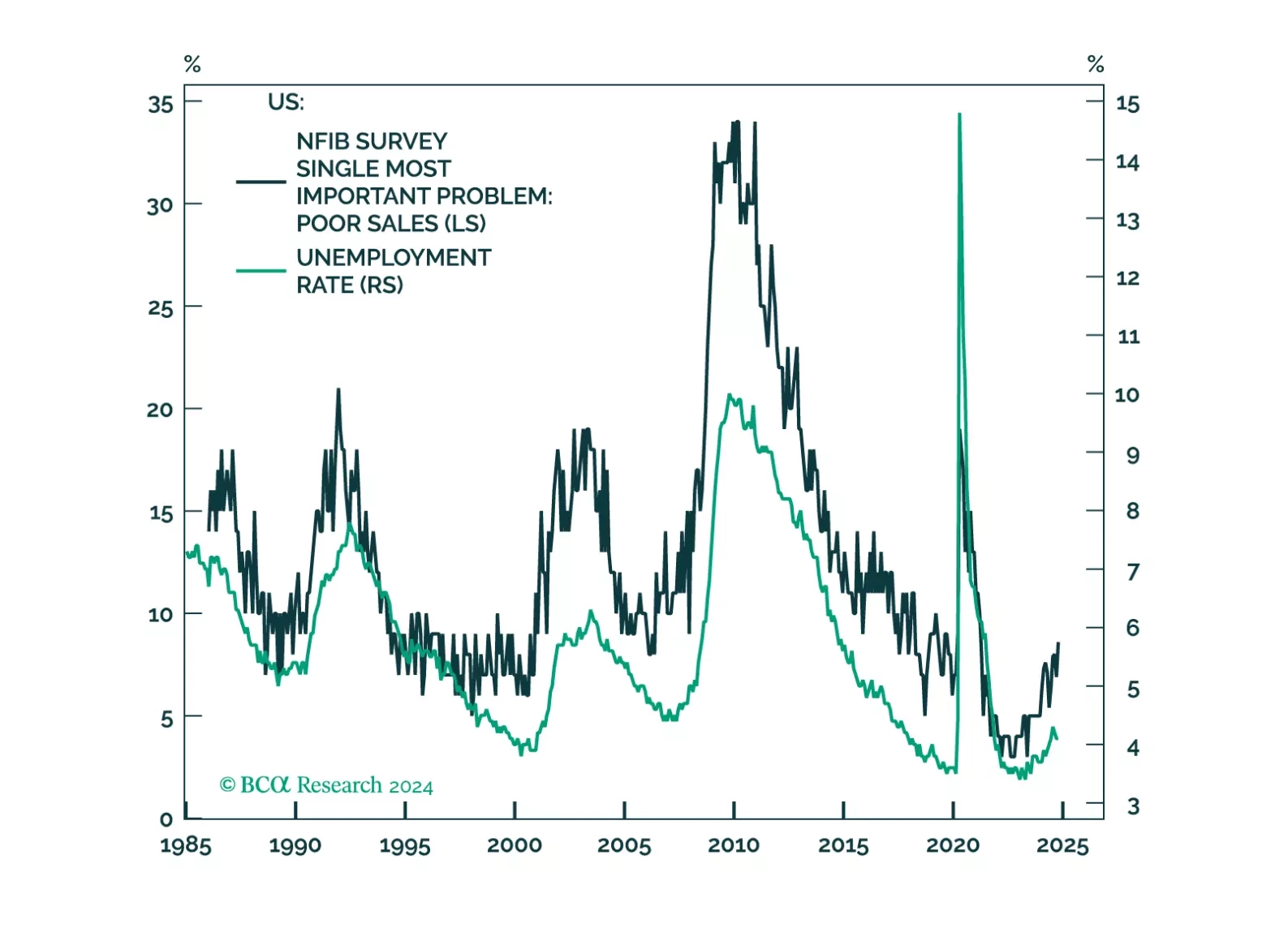

Job openings beat expectations in October, increasing to 7.74m from 7.44m in September. The details of the JOLTS report were mixed, however. Hires ticked down, driven by interest rate-sensitive sectors. Outside of hires, the rest of the report had a more…

The post-COVID recovery has been one of excesses. Government deficits have ballooned, tight labor markets have led to a windfall of consumer spending, and equity valuations have soared on the back of lofty growth expectations. But these excesses will no longer be sustainable in 2025. Our theme for next year is Thin Is Back In. Government budgets, economic growth, and equity valuations will be leaner than investors expect. We discuss this the reasoning behind this macro view and the asset allocation implications that follow from it.

The November Tokyo CPI beat expectations, with headline inflation accelerating to 2.6% y/y from 1.8%. The core (ex. fresh food) and “core core” (ex. fresh food and energy) measures also reaccelerated to 2.2% and 1.9%, respectively. The Tokyo CPI provides…

The November flash Eurozone inflation estimate met expectations, with headline HICP accelerating to 2.3% y/y from 2.0% in October, above the ECB’s target. Core inflation remained constant at 2.7%. At 3.9%, services inflation is still elevated. The outlook…

The Fed’s preferred measure of inflation, core PCE, met expectations of 0.3% m/m in October, and accelerated to 2.8% y/y from 2.7% in September. Inflation rose on the back of hot inputs from the PPI report, which is not expected to last. The market-based core…

Consumer confidence came in as expected in November, with The Conference Board’s index rising to 111.7 from 108.7 in October, a level not seen since August 2023. Both the assessment of consumers’ present and future situation drove the increase. The…