Inflation/Deflation

Preliminary estimates suggest that Eurozone headline and core CPI inflation decelerated from 2.2% to 1.8% y/y and from 2.8% to 2.7%, respectively, in September. The inflation data from individual Euro Area countries earlier last week had already prompted…

The ISM manufacturing PMI remained constant in September at 47.2, against expectations of a slower pace of decline and extending a six-month contraction streak. Measures of production and domestic demand decelerated at a notably slower pace while foreign…

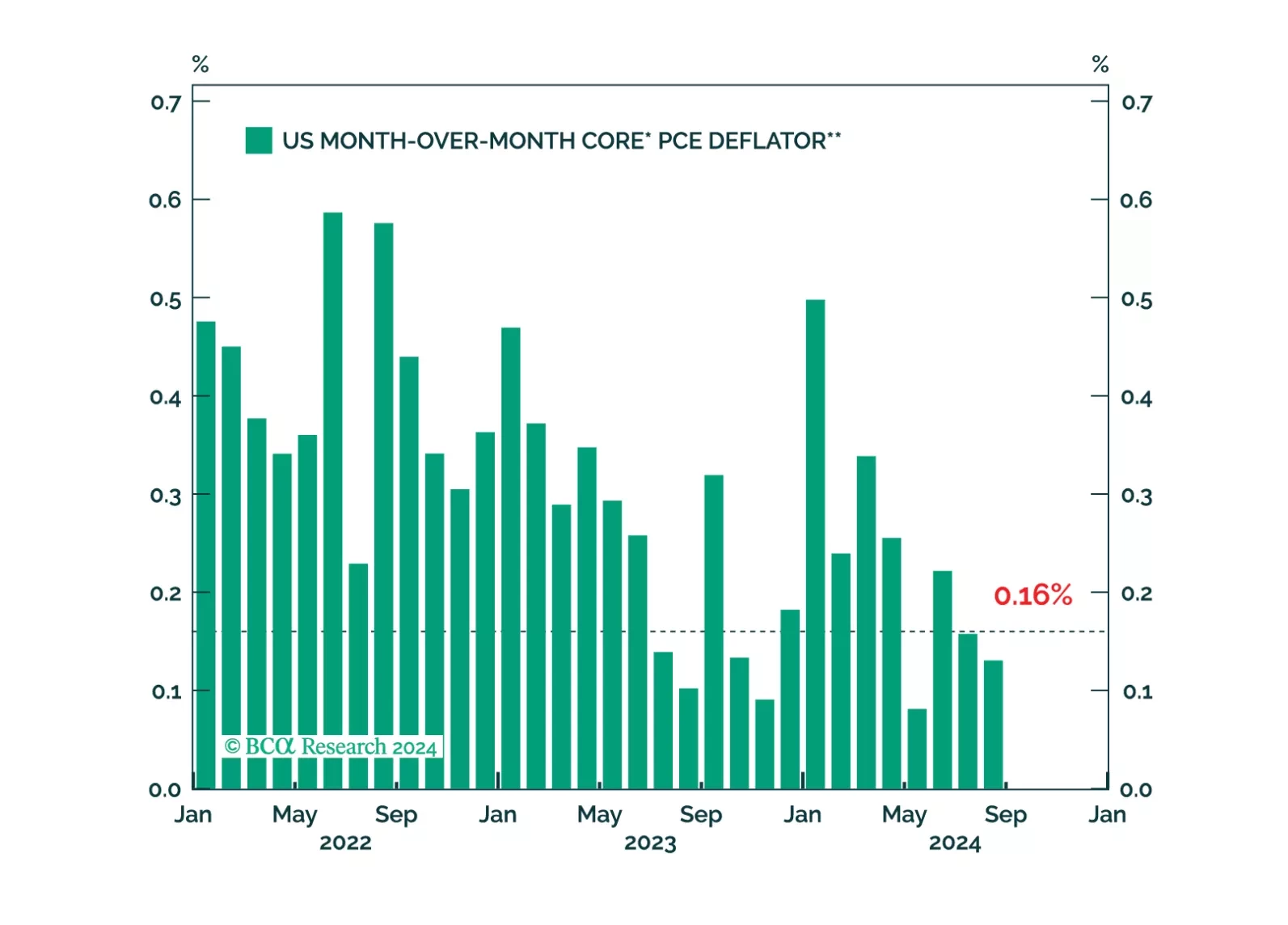

US nominal personal income growth decelerated to a 0.2% pace in August, from 0.3% in July, missing expectations that it would accelerate. Nominal personal spending also disappointed, growing at a slower 0.2% pace from 0.5%. In real terms, spending barely…

France’s and Spain’s preliminary September CPI readings declined on a month-on-month basis, clocking in at 1.5% and 1.7% y/y respectively, and undershooting consensus expectations. Germany’s and Italy’s updates are due on Monday and the Eurozone CPI will be…

We consider the possibility that lower interest rates could lead to an increase in household borrowing, prolonging the economic recovery.

This week has not been short of developments on Chinese policy. After unleashing a monetary policy blitz, the authorities held an unscheduled Politburo meeting resulting in a pledge to take actions towards stabilizing the housing market and to support fiscal…

In a widely expected move, the Swiss National Bank (SNB) cut its policy rate for a third consecutive meeting on Thursday, from 1.25% to 1.00%. The move marked President Thomas Jordan’s final policy decision and his incoming successor Martin Schlegel…

The conventional 30-year mortgage rate eased further to 6.2% from above 7% back in the spring, spurring a 20.3% surge in refinancing activity last week. Mortgage applications rose 11.0%, marking a fifth consecutive week of increase and the Conference Board…

In a widely expected move, the Riksbank lowered its policy rate from 3.5% to 3.25% in September, marking its third cut this year. It embarked on its easing cycle in May, leading many other DM central banks, and has been sending increasingly dovish messages…

A US recession remains our base case over a cyclical investment horizon. We expect the ongoing labor market deterioration to eventually tip the economy into a recession. We therefore continue to expect the disinflationary forces to dominate the US economy…