Inflation/Deflation

The Bank of Canada (BoC) reduced its policy rate by 25bps for the second meeting in a row on Wednesday. We highlighted in a recent Insight that the soft June inflation print and weakening labor market increased the odds of more aggressive BoC easing. …

UK’s CPI growth stands right on the Bank of England’s (BoE) 2% target. However, services inflation remains sticky, growing at a constant 5.7% y/y in June. Moreover, the deceleration in wage growth remains insufficient to temper inflationary pressures in the…

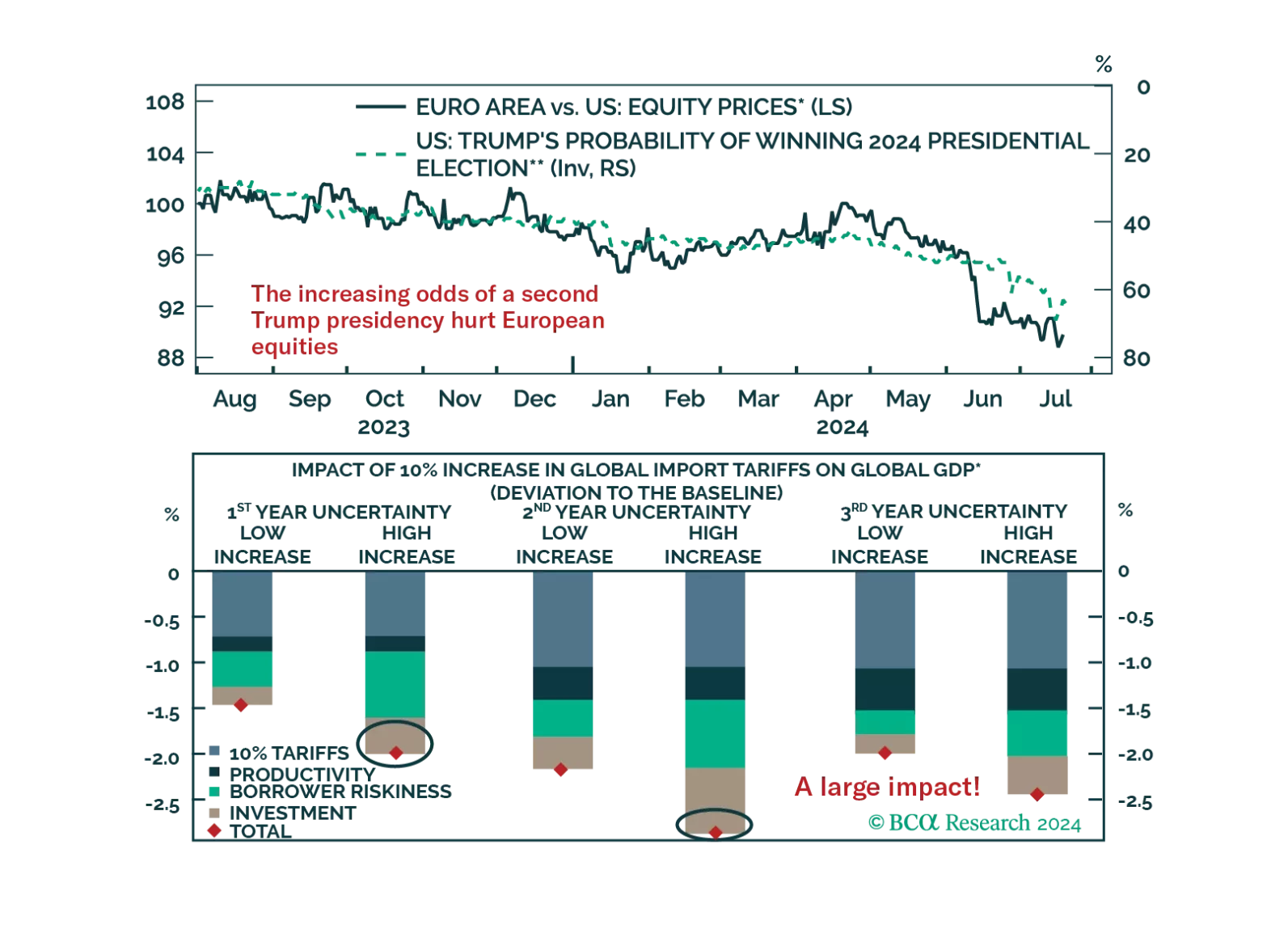

As Trump’s victory odds rise, the underperformance of European equities deepens. How negative would a global trade war be for European assets?

The four ASEAN stock markets (Indonesia, Malaysia, Thailand, and the Philippines) have fallen in absolute terms over the past year despite the powerful rally in the developed markets. They have also underperformed their EM benchmark. Our Emerging Markets…

The Conference Board Leading Economic Index (LEI) for the U.S. declined by 0.2% in June from May, marking the smallest decrease in the past three months. Year-over-year, the US LEI remained negative but less so compared to prior months, prompting The…

Don't buy the dip. The equity bull market is over. The US will enter a recession in late 2024 or in early 2025.

Two of Brazil’s ever-recurring demons have come back to haunt investors: public debt sustainability and persistent inflation. According to the latest report from our Emerging Markets Strategy (EMS) team, these troubles are set to worsen in the next six to…

US shelter inflation has been stubbornly high for the past few years, but we finally saw a notable drop in the June CPI release. Given that shelter accounts for more than 40% of the core CPI index, the outlook for shelter inflation is critical for the overall…

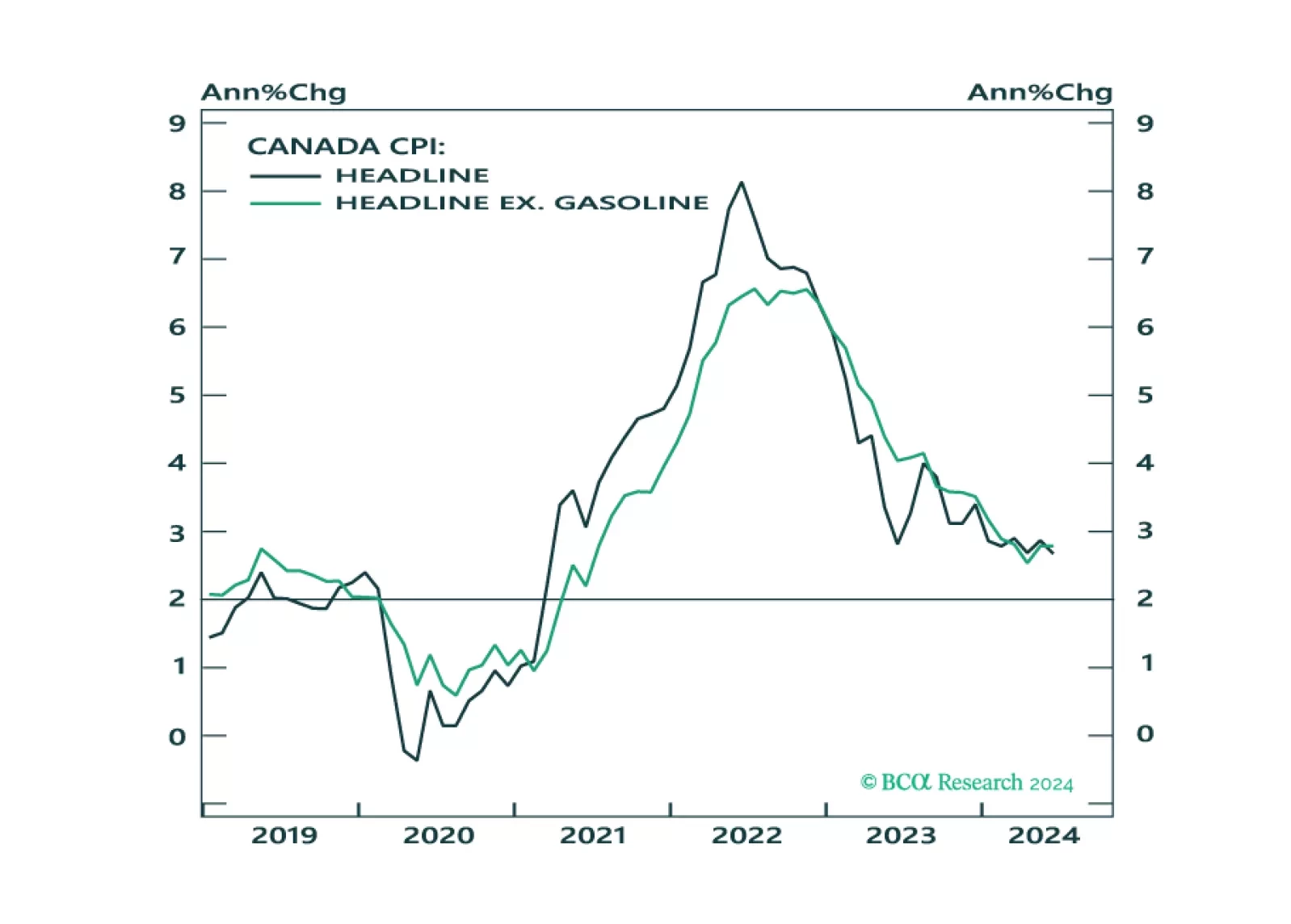

In this Insight, we look into the recent CPI release in Canada, and the possible implications for fixed-income market trades.

Markets had already been sussing out that the Bank of Canada (BoC) will cut rates for the second time when it meets next week, and this morning’s soft CPI report all but confirmed it. The last remaining obstacle in the way of another BoC rate cut was the…