Inflation/Deflation

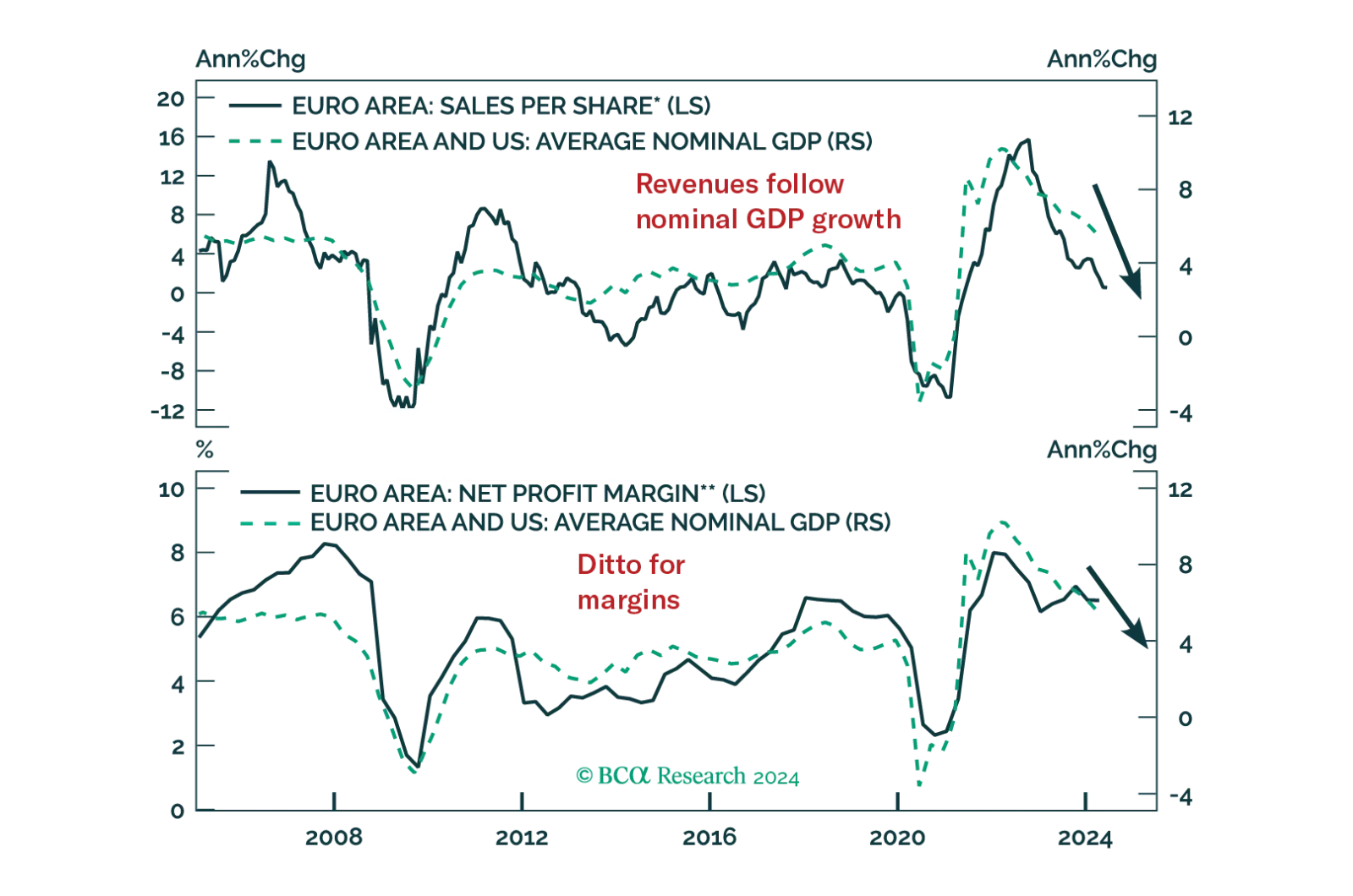

The real threat to European equities is growth, not political risk. How low will Eurozone earnings fall during the coming recession and how much will equities decline in response?

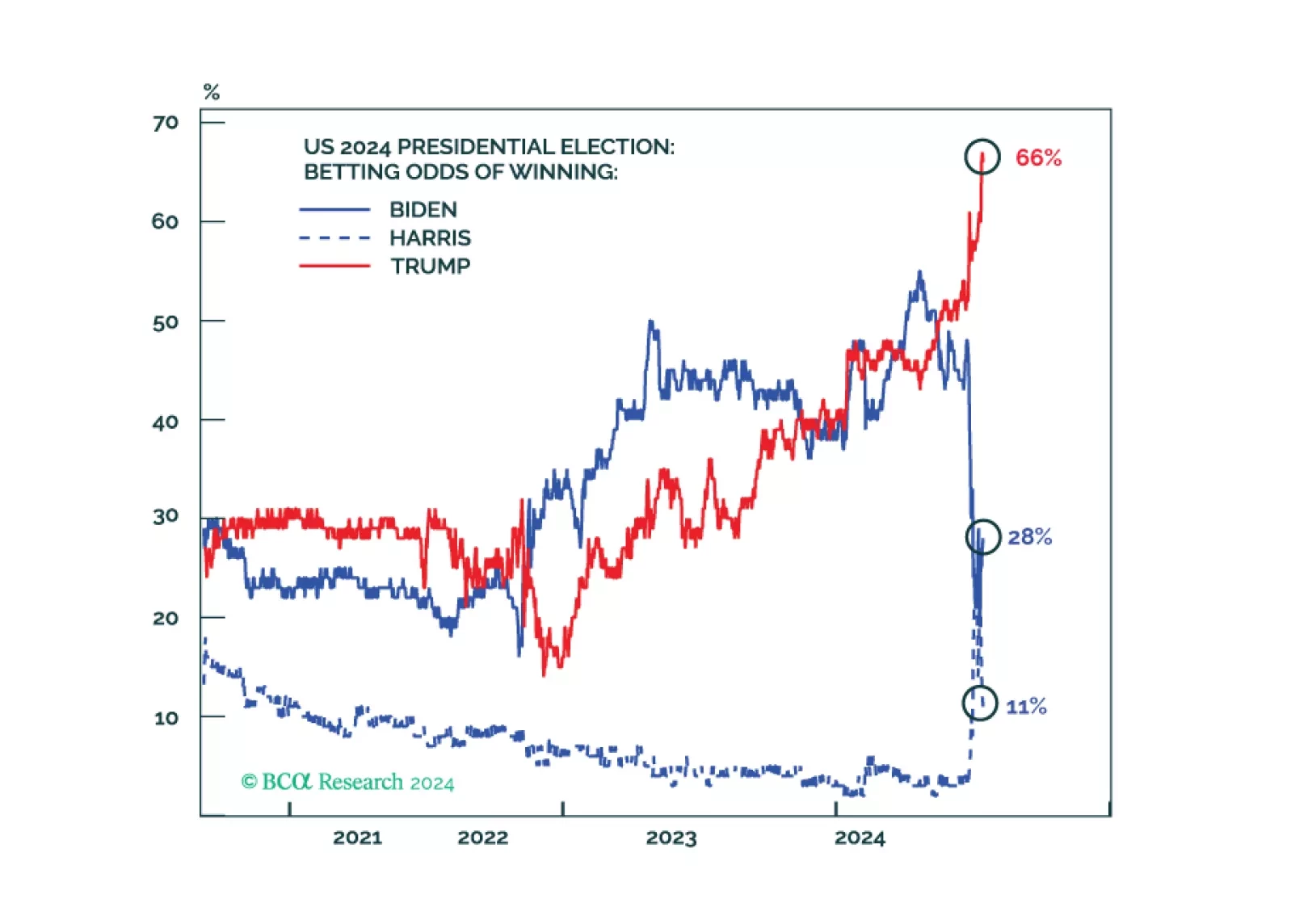

The cyclical economy is slowing today. Republicans are now more likely to win a full sweep, crack down on immigration and trade, and at least modestly stimulate the economy. Uncertainty and volatility will rise.

In light of last week’s employment report and this morning’s CPI, it’s time for the Federal Reserve to cut rates.

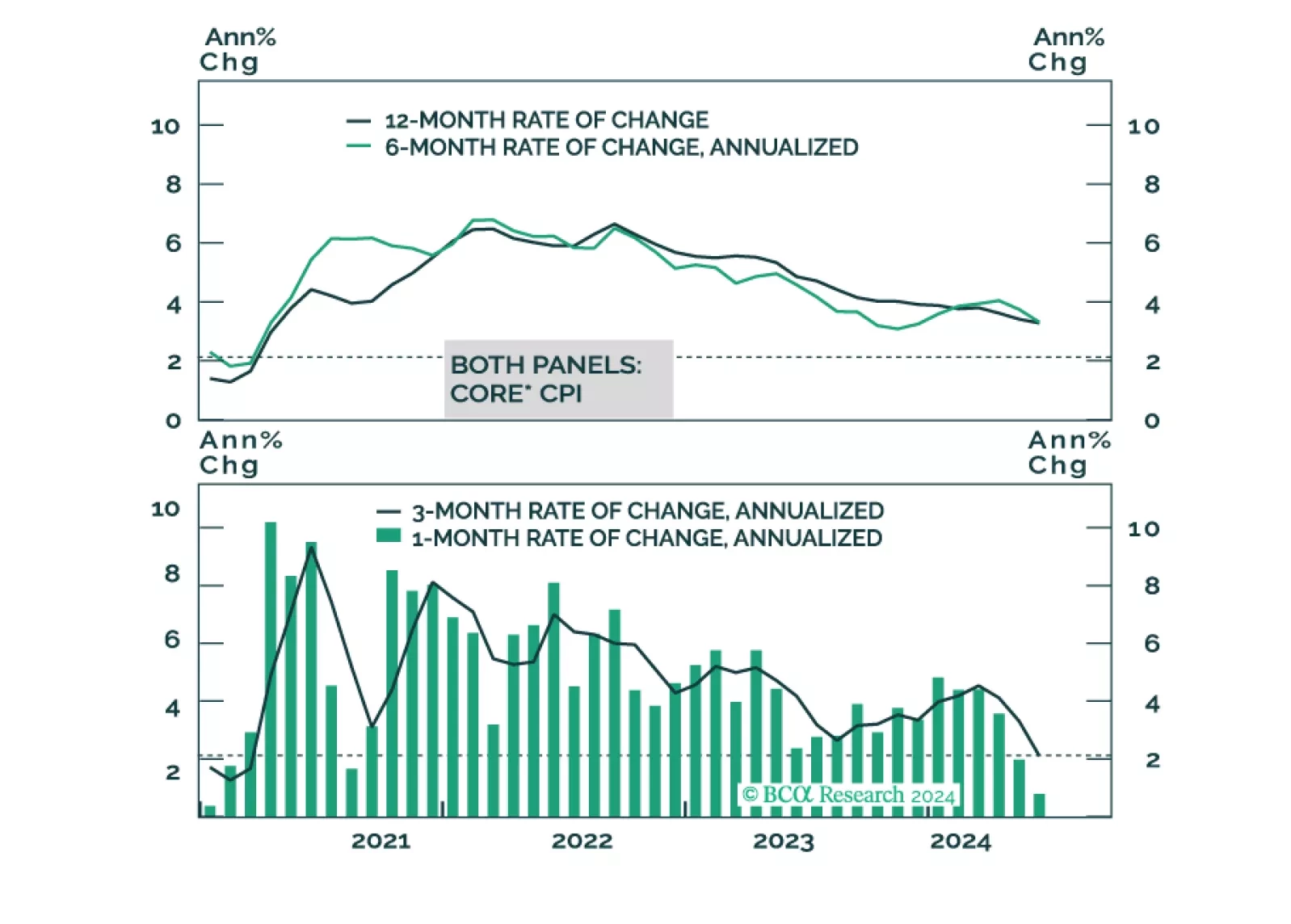

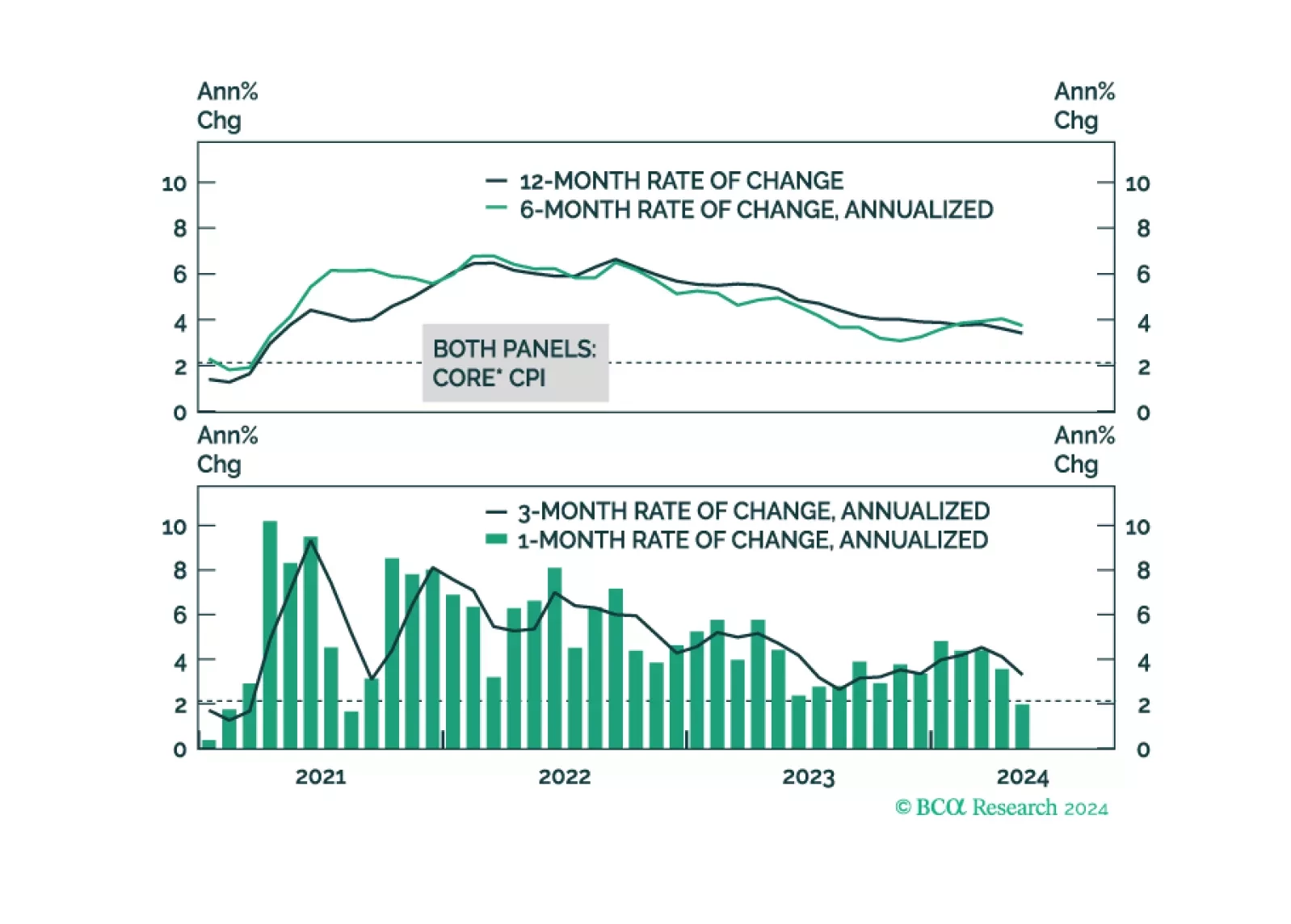

We consider the outlook for CPI inflation over the next 12 months. Our baseline forecast calls for core CPI to hit 2.40% during this timeframe and for headline CPI to fall between 1.74% and 2.49%.

At first glance, France has moved to the far left. However, this coalition is fragile, and Macron’s allies still hold the balance of power. What are the assets that will benefit from this new political setup, and those that will not?