Inflation/Deflation

In this insight, we update our thinking on the recent BoJ move in terms of positioning for the yen and JGB yields.

The new national unity government in South Africa creates a geopolitical opportunity that investors should not bet against in the short term. A broad-based rally is likely to unfold relative to other emerging markets. However, structural problems and distrust within the new coalition hold out significant risks over the long run.

The BoE had to deal with a stagflationary headache in the second half of 2023. Inflation was stickier and growth was weaker in the UK than in many of its DM peers. This trend turned around earlier this year with a late-cycle growth reacceleration. The UK…

In a largely expected move, the Bank of Japan kept its policy rate unchanged at 0-0.1% in June. It maintained the pace of bond buying at JPY 6tr per month but signaled it would lay out a plan to reduce its balance sheet next month, without offering any…

Goods prices have been normalizing following the pandemic binge on goods spending. The May CPI release indicated that durable goods and nondurable goods prices both continued to contract. Investors and policymakers have thus turned their attention to other…

According to BCA Research’s Counterpoint service, job losers not on temporary layoff (‘bad’ unemployment) will need to rise further for the Fed to reach its 2 percent inflation target. Although prime-age participation has surged, the participation of older…

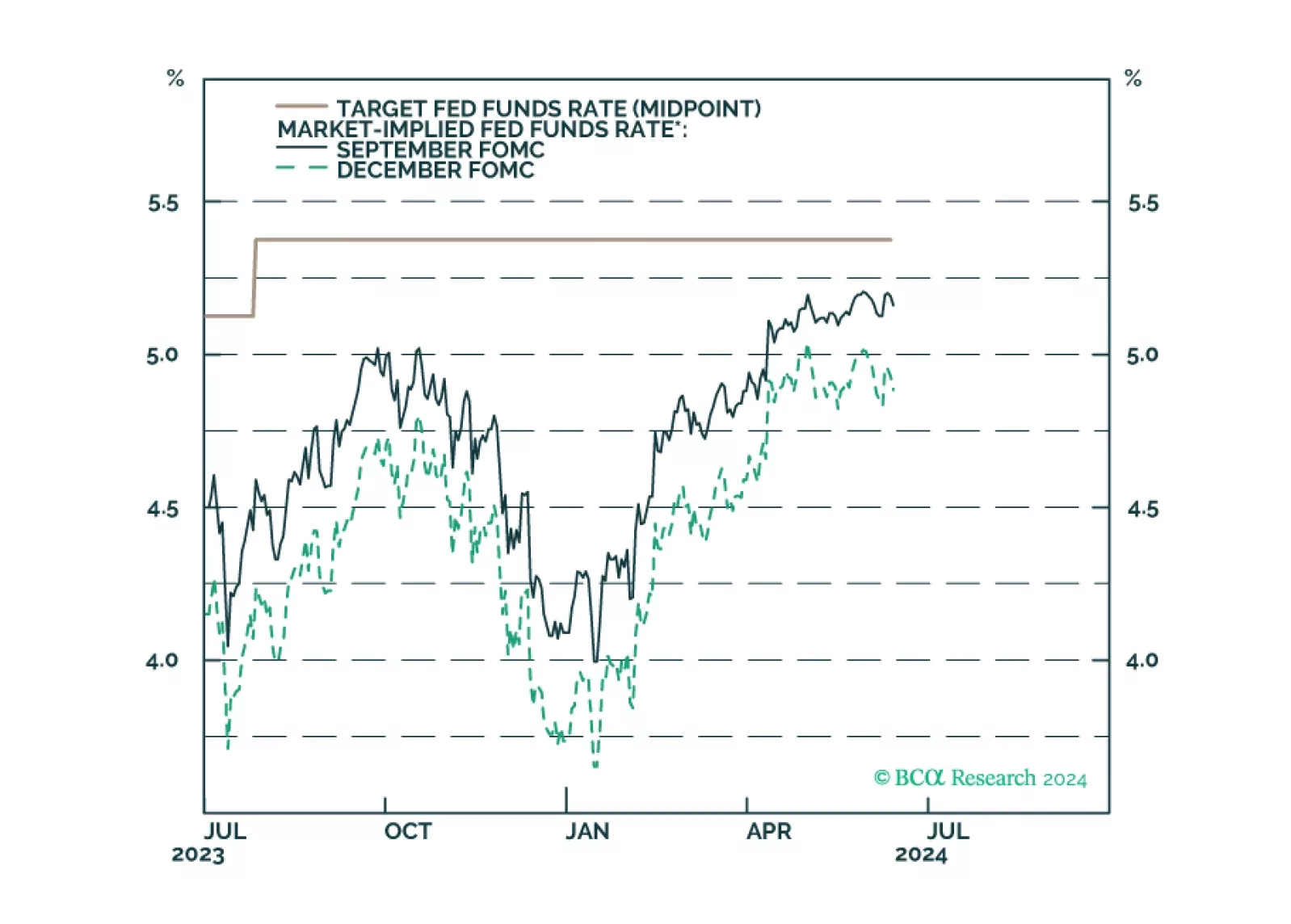

Our reaction to this morning’s CPI report and this afternoon’s FOMC meeting.

In a widely expected move, the Fed kept its policy rate unchanged within a 5.25%-5.5% range following its June 11-12 meeting. However, the median dots have moved higher for both 2024 and 2025. The median FOMC member now expects to cut only once this year…

US CPI inflation continued to ease in May. Headline CPI stagnated on a month-on-month basis (3.3% y/y) in May, down from April’s 0.3% m/m (3.4% y/y), and below expectations of a more muted rate of growth. Core CPI also slowed more than expected, rising…

The Bank of Japan exited negative interest rate policy in March, but subsequent softer-than-expected CPI inflation prints have complicated its path towards tightening. The central bank is widely expected to stay put when it meets this week. Governor Kazuo…