Inflation/Deflation

The Fed left the policy rate unchanged following its May FOMC meeting. It also announced it would slow the pace of quantitative tightening starting on June 1, from the current $60 billion per month to $25 billion per month for Treasuries redemptions, while…

Updated views on US Treasury yields and the dollar following today’s FOMC meeting.

Central banks are in a dilemma whether to prioritize supporting growth or bringing inflation back to target. This is unlikely to end well. Investors should be defensively positioned.

The Q1 US Employment Cost Index (ECI) accelerated at a faster-than-expected 1.2% q/q rate, from 0.9% q/q in Q4. On a year-on-year basis, it rose by 4.2% in Q1 and follows a similar annual increase in the previous quarter. The Fed is not expected to cut…

Euro area inflation and GDP numbers were released on Tuesday. The preliminary harmonized core consumer price index came in at 0.7% on a month-on-month basis, a decrease from 1.1% in March. The preliminary year-on-year core CPI also decreased, clocking in at…

In its latest report, BCA Research’s Global Fixed Income Strategy service introduces the latest addition in its framework for investing in global inflation-linked bonds (ILB). To apply the Euro Inflation-Linked Golden Rule, investors should follow these…

Chinese industrial profit growth slowed in the first three months of the year to 4.3% YTD y/y, from 10.2% y/y in January and February. The March slowdown is meaningful since industrial profits outright contracted by 3.5% relative to March 2023. Weak…

A few preliminary measures of German inflation for April were released on Monday. The month-on-month headline inflation measure came in at 0.5% an increase from last month’s reading of 0.4% but below expectations of 0.6%. Meanwhile the year-on-year version…

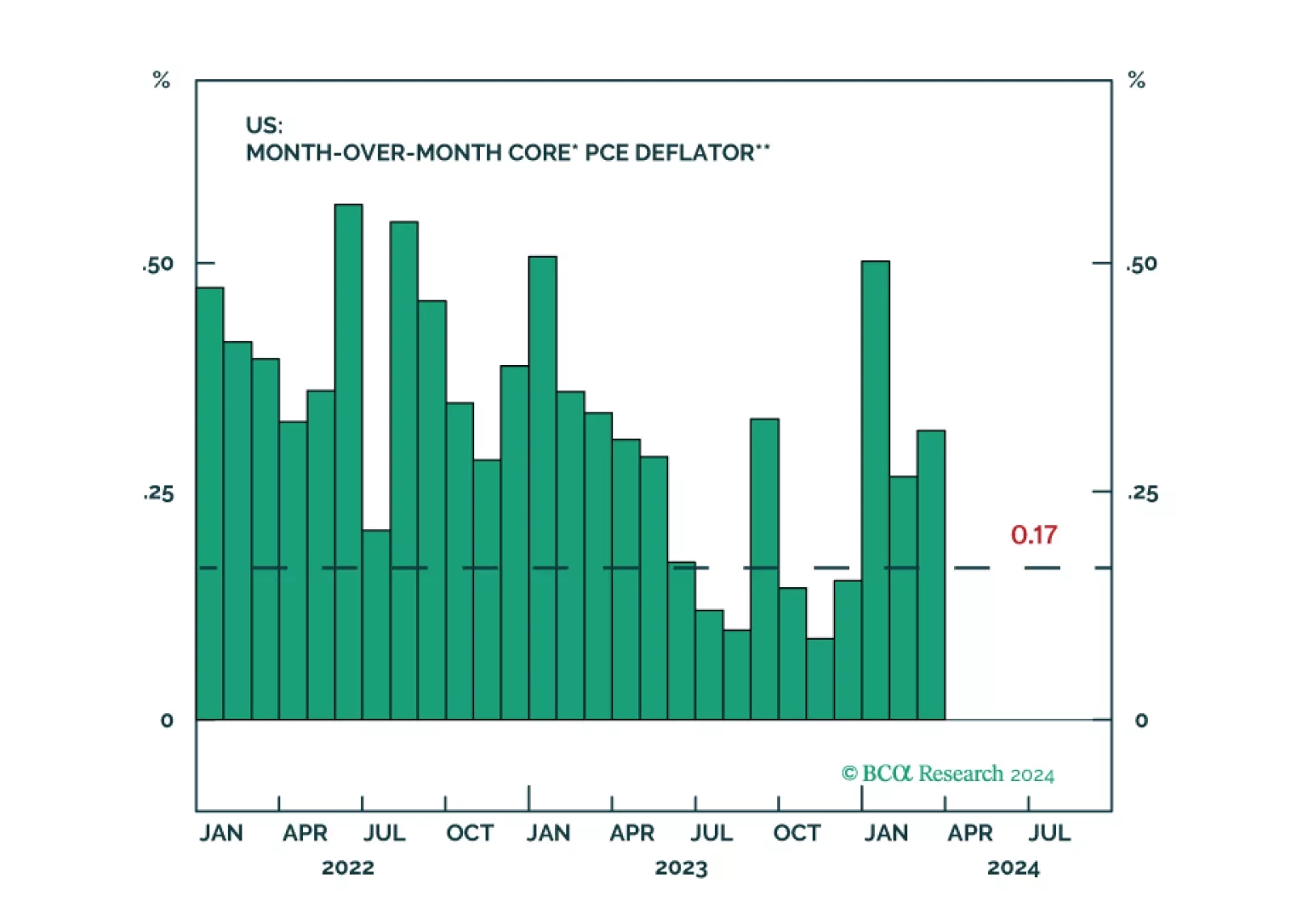

The trimmed mean PCE was released on Friday by the Dallas Fed. This measure removes the top 31% of items with the highest inflation and the bottom 25% of items with the lowest inflation within the PCE basket. Historically, it has served as an accurate gauge…

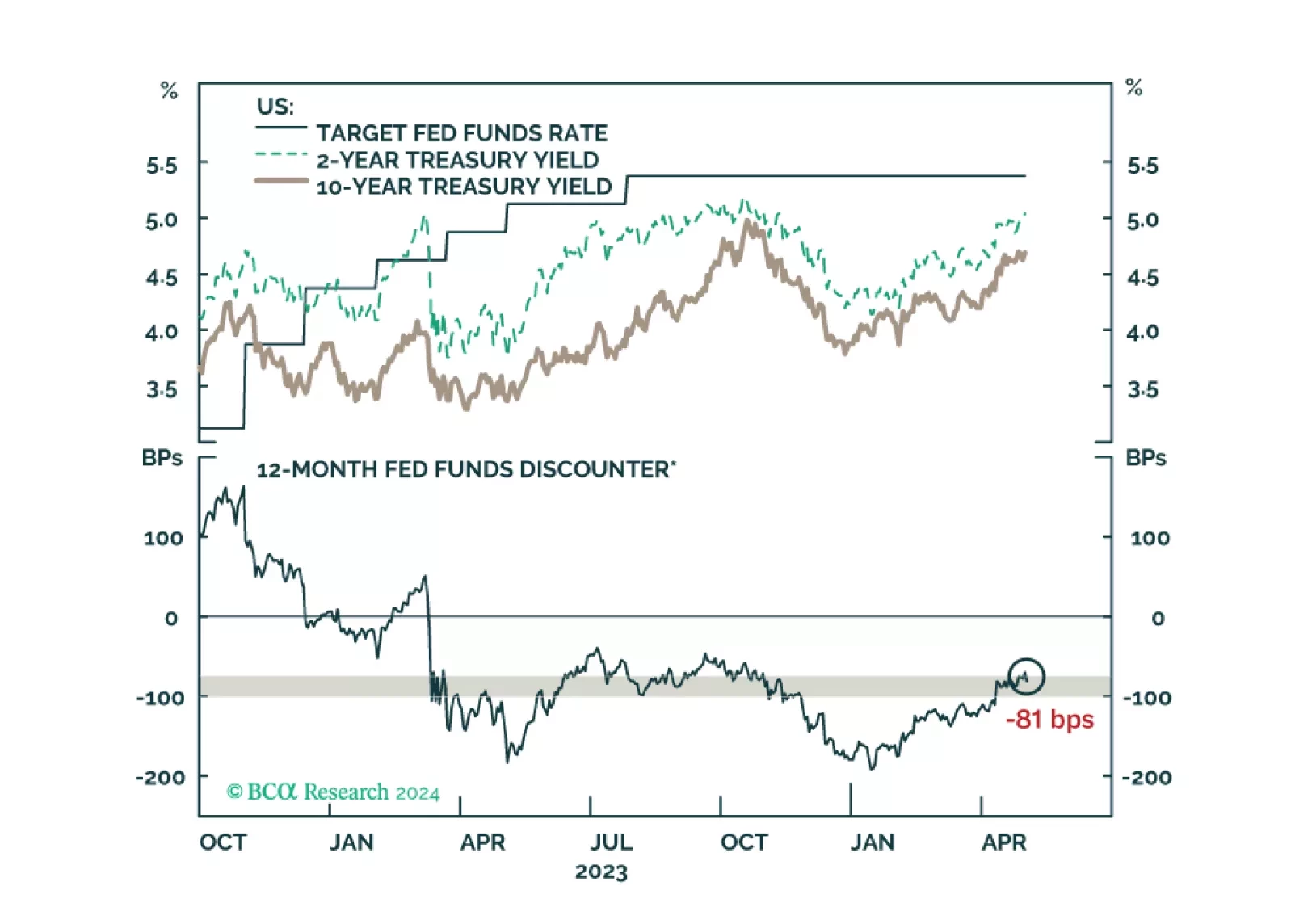

According to BCA Research’s US Bond Strategy service, the May FOMC meeting is unlikely to cause a stir in fixed income markets. The Fed will hold an FOMC meeting next week and while it will not update its economic or interest rate projections, we will be…