Inflation/Deflation

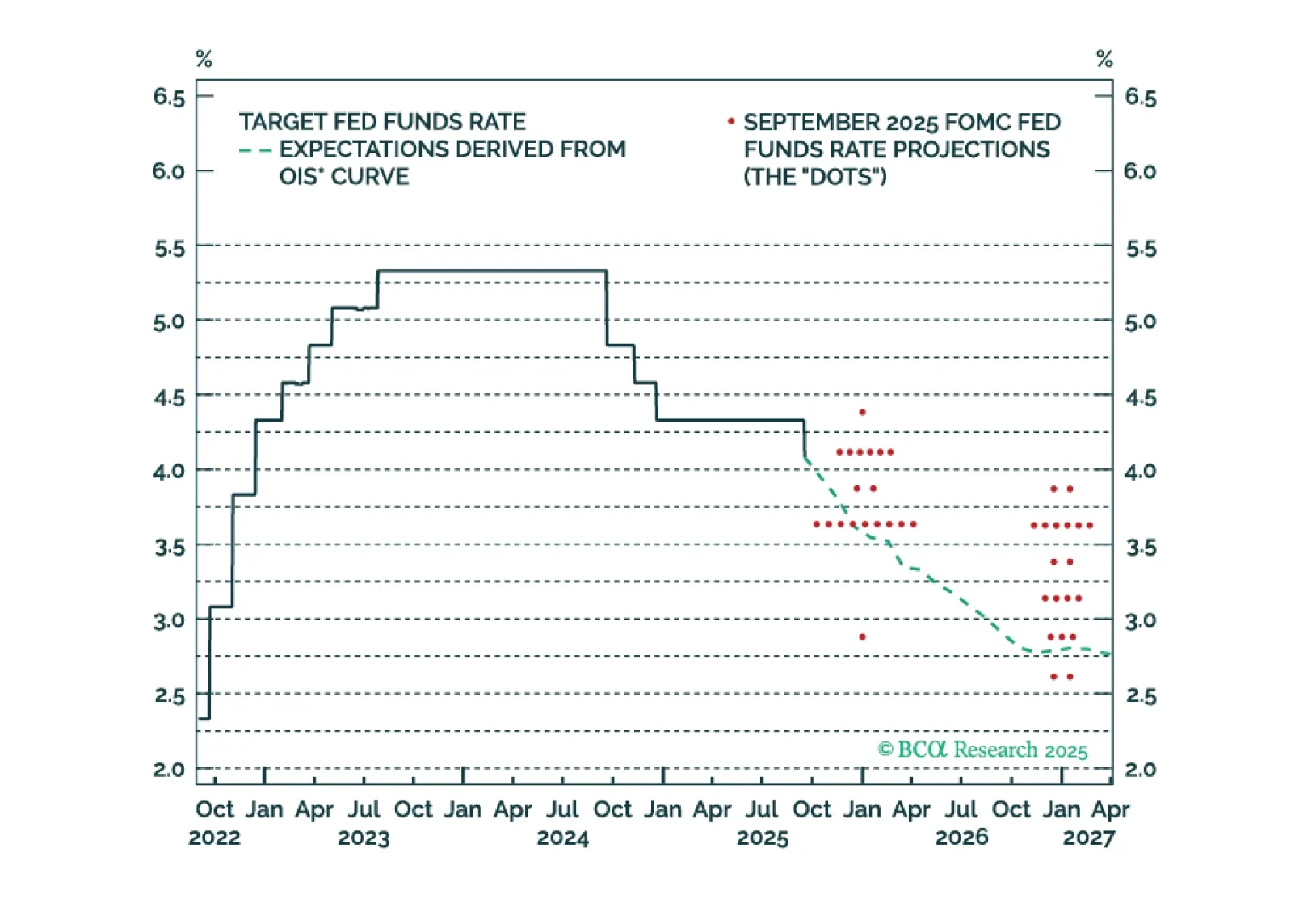

Median Fed unemployment rate projections are overly optimistic. The Fed will end up cutting more in 2026 than it currently anticipates.

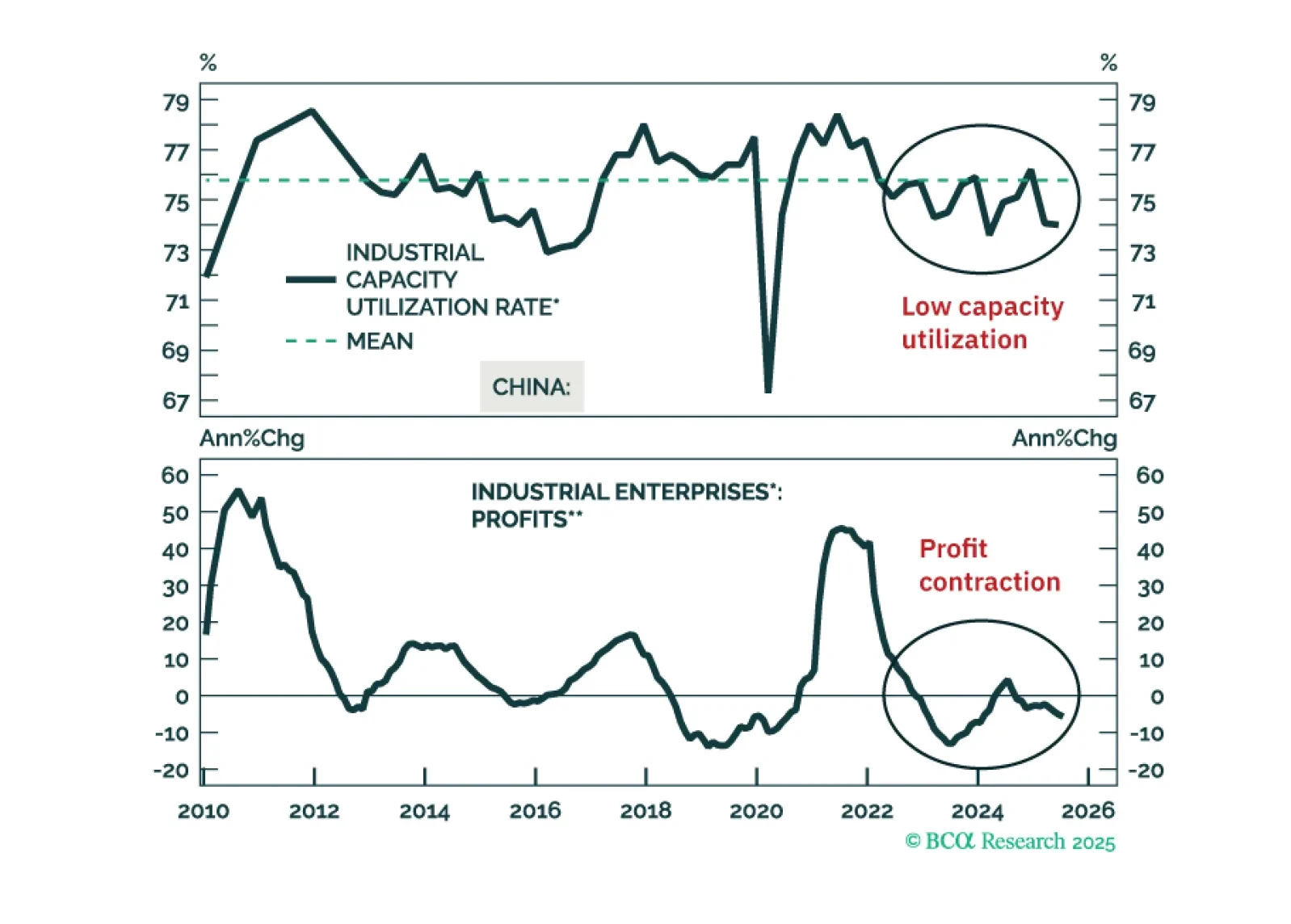

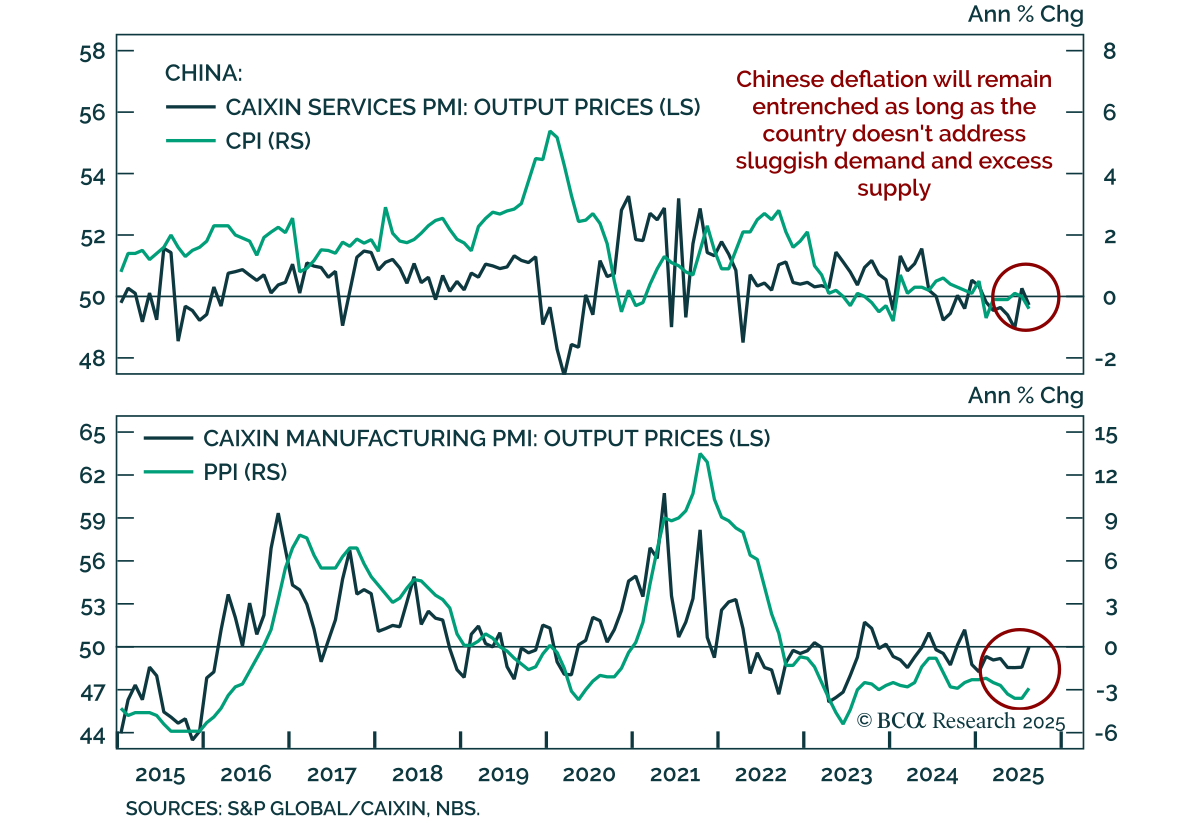

China’s policy-driven constraints prevent the “destruction” part of the creative destruction process. Instead, they entrench overcapacity, deflation, and poor profitability. We are reluctant to chase the rally in Chinese stocks in absolute terms.

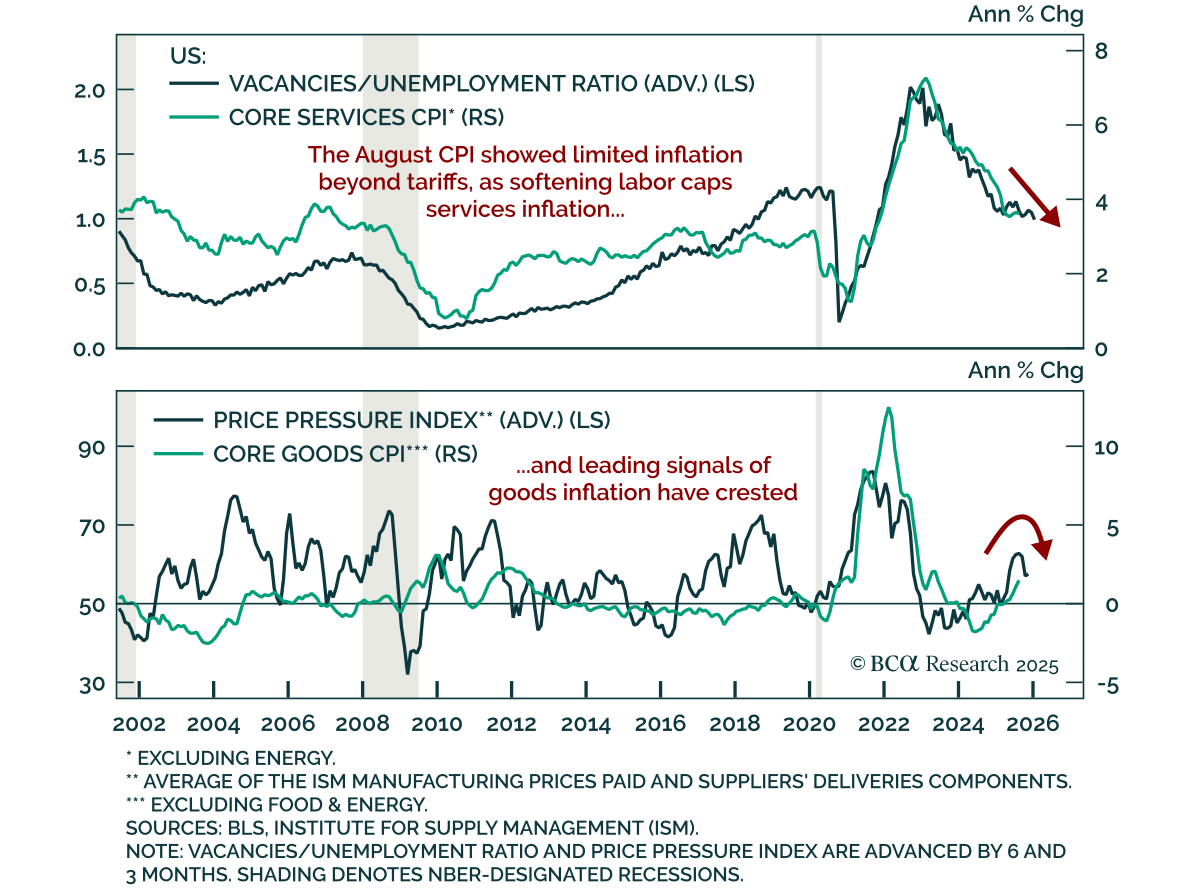

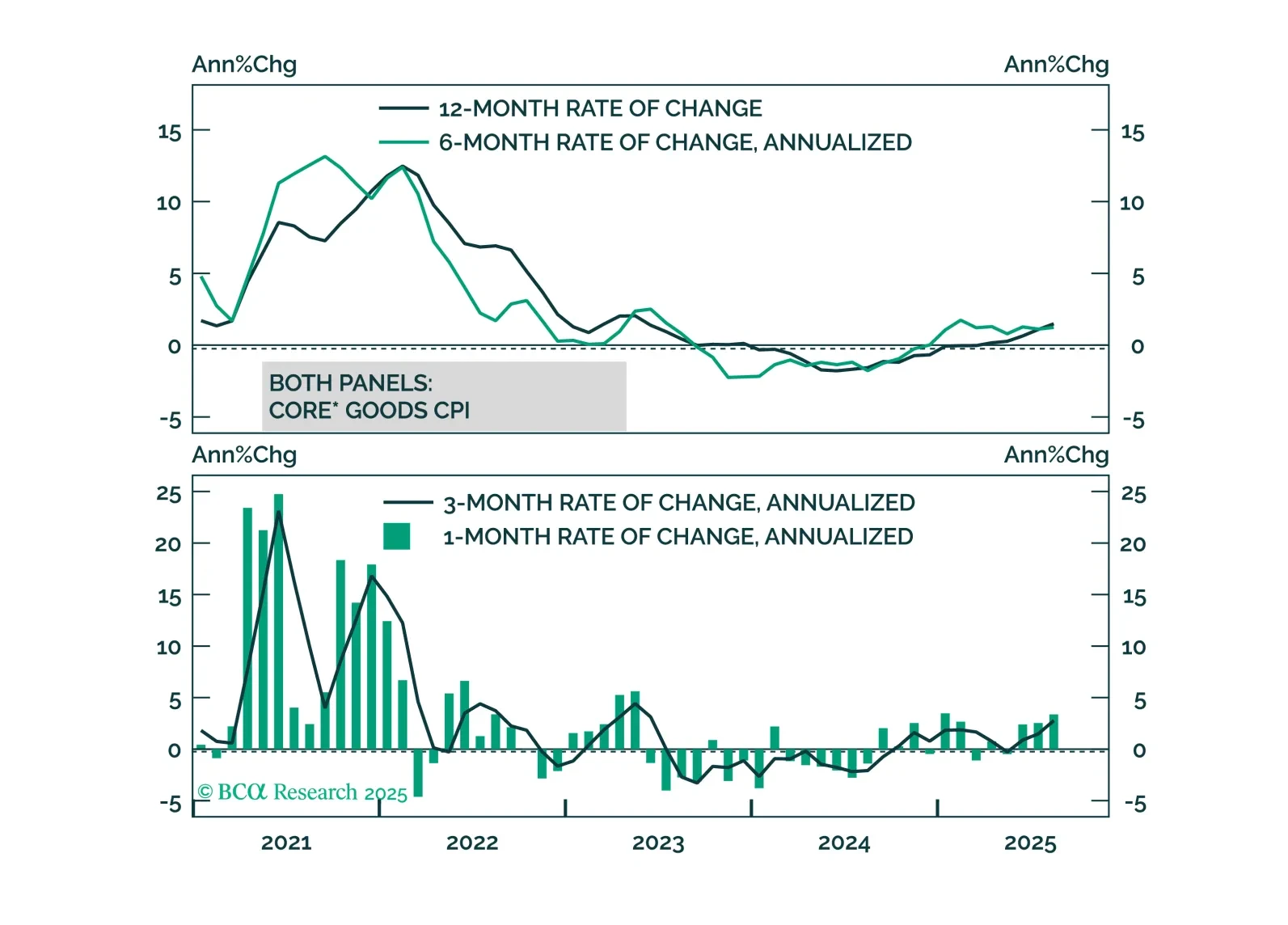

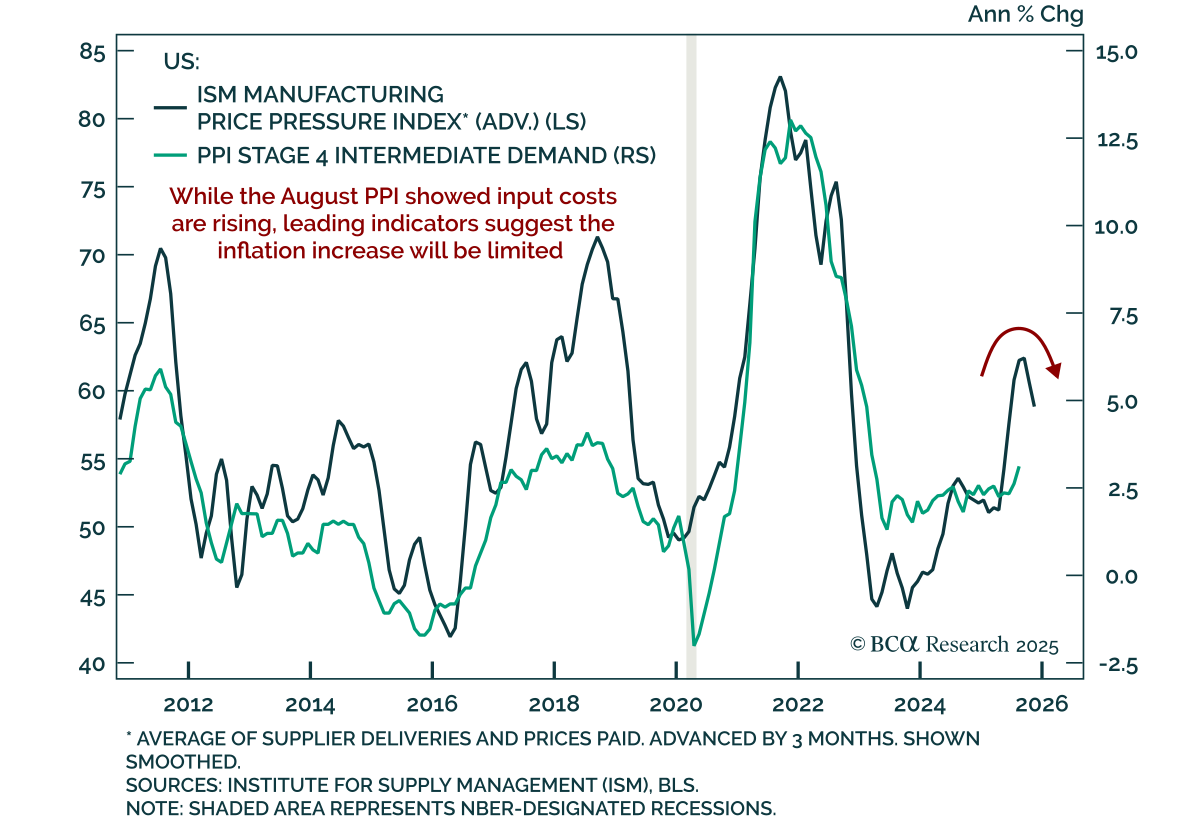

High US inflation is being driven by tariffs, not domestic inflationary pressure. This argues for Fed easing and a bull-steepening of the Treasury curve.

Core Europe’s industrial sector will relapse in the coming months due to US tariffs and a strong euro. Investors can play the imminent deflationary shock by being long Central European bonds. They should, however, hedge the currency risk vis-à-vis the euro.