Inflation/Deflation

Chinese stocks are experiencing their longest rally since the country’s exit from Covid restrictions over a year ago. The MSCI Onshore and Investable indices (in USD terms) have gained 15.8% and 9.1% respectively since February 5th, with the former…

Although the Atlanta Fed GDPNow estimates for Q1 have been trending lower, the latest 2.5% print (which is down from 3.4% a month ago) still suggests that economic conditions are resilient in the US. Yet small business owners are less optimistic. The results…

Our Portfolio Allocation Summary for March 2024.

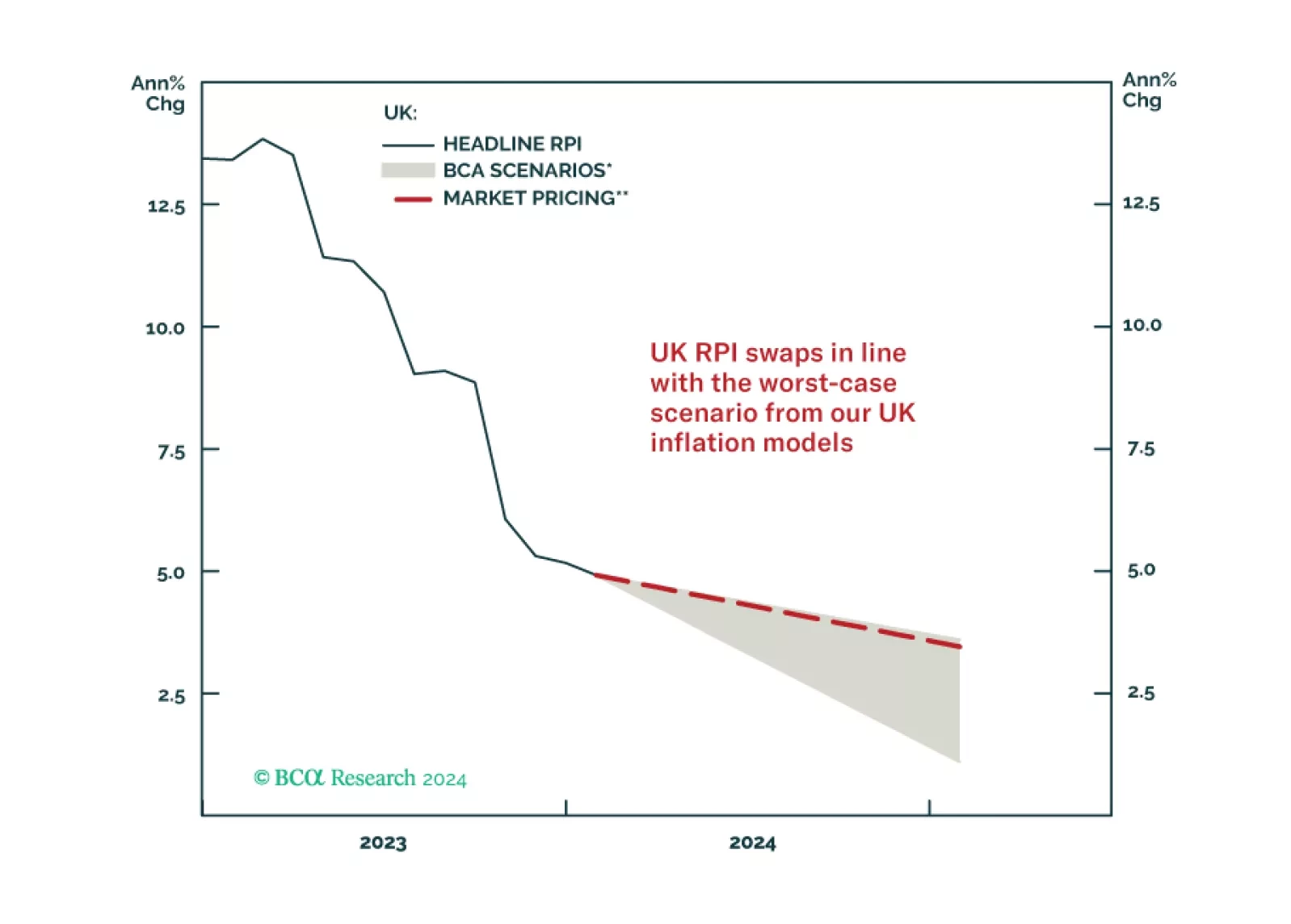

In this Special Report, we introduce our UK Linkers Golden Rule – a framework to profitably trade and invest in UK inflation-linked bonds versus nominal UK gilts. The Rule is currently signaling that nominal Gilts should outperform UK linkers over the next year as UK inflation slows.

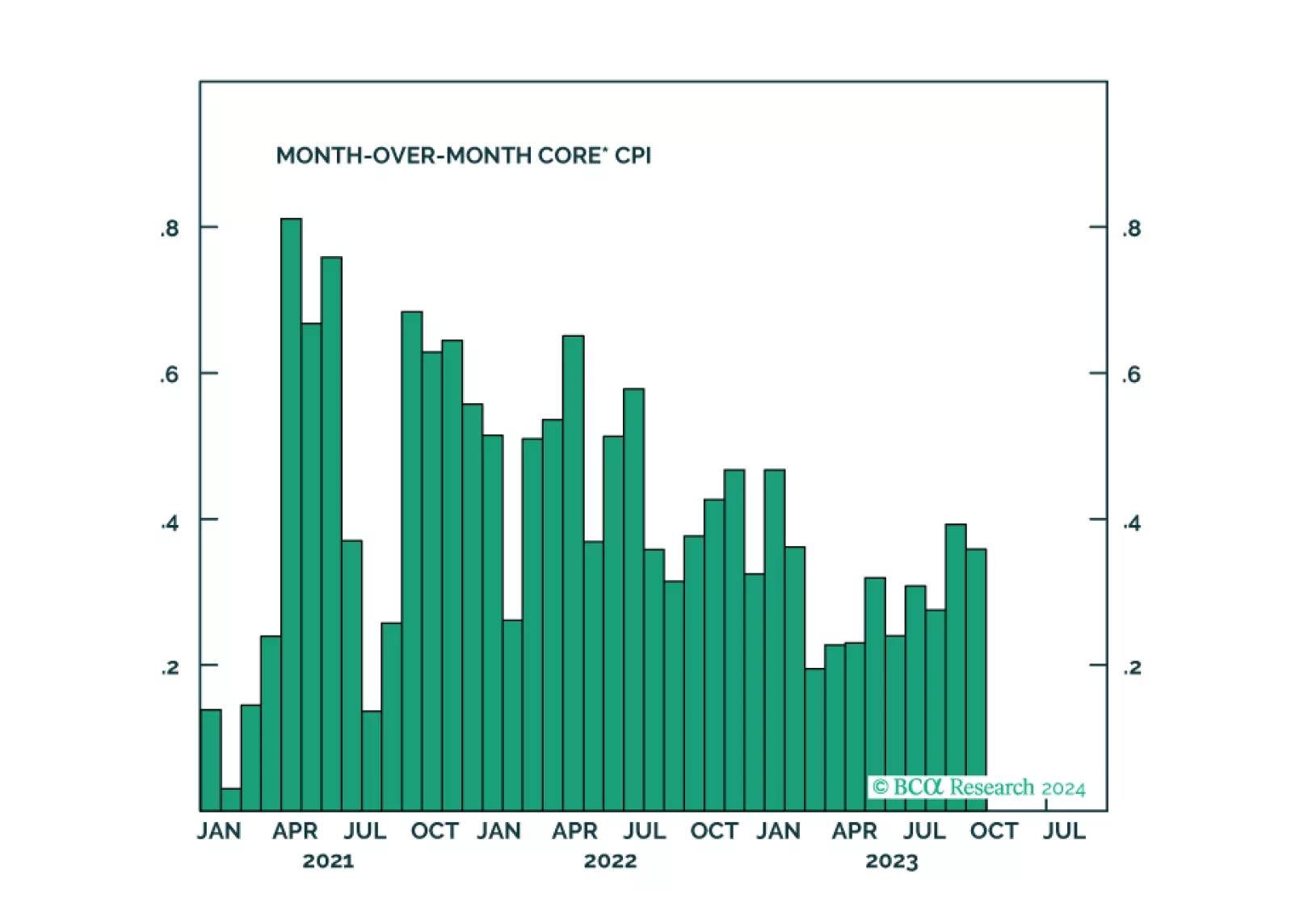

Results of the New York Fed’s Survey of Consumer Expectations showed an uptick in medium- and long-term inflation expectations in February. Specifically, the three-year ahead measure rebounded from a record low of 2.4% to 2.7% and the five-year ahead gauge…

The US employment situation report sent a mixed signal on Friday. While total nonfarm payrolls rose by 275 thousand jobs in February, exceeding the 200 thousand expected, the previous two months’ numbers were revised lower by 167 thousand jobs (see Indicator…

Japanese equities and government bonds sold off on Monday and the yen strengthened following the release of the revised Q4 GDP report showing the economy expanded by an annualized 0.4% q/q in Q4 2023 versus earlier estimates of a 0.4% contraction. A…

According to BCA Research’s European Investment Strategy service, last week’s ECB meeting confirmed their long-held view that the most likely date for the first ECB rate cut would be June. The ECB continues to acknowledge that the European economy is soft…

We are pushing back the anticipated start date for a Eurozone recession and assessing how it affects our equity stance.

As we discussed in a recent Insight, the krone is the top pick for our Foreign Exchange Strategy team. The krone upgrade is one of the most significant changes in our colleagues’ attractiveness ranking model. Norway has the perfect storm of sticky inflation,…