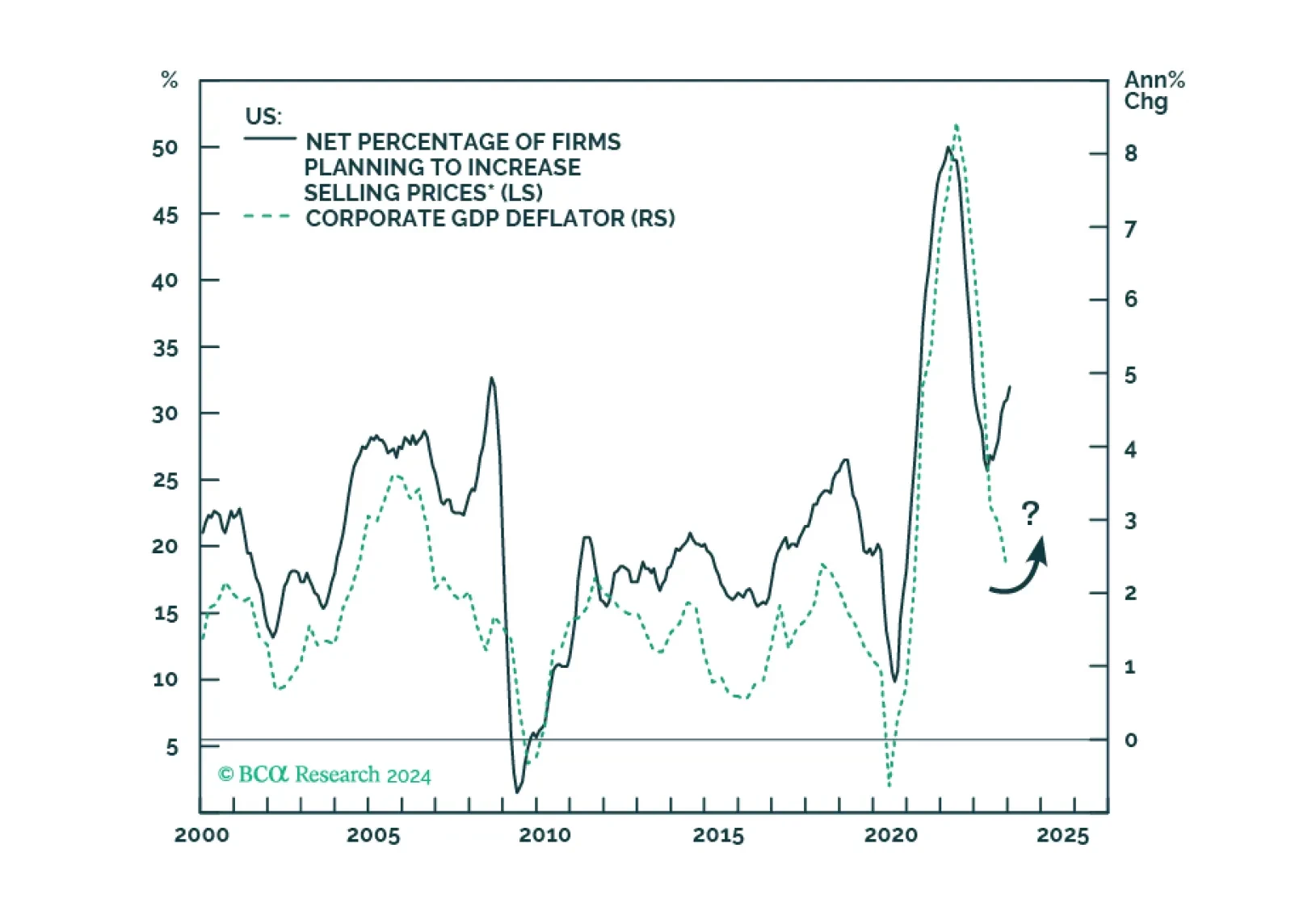

Inflation/Deflation

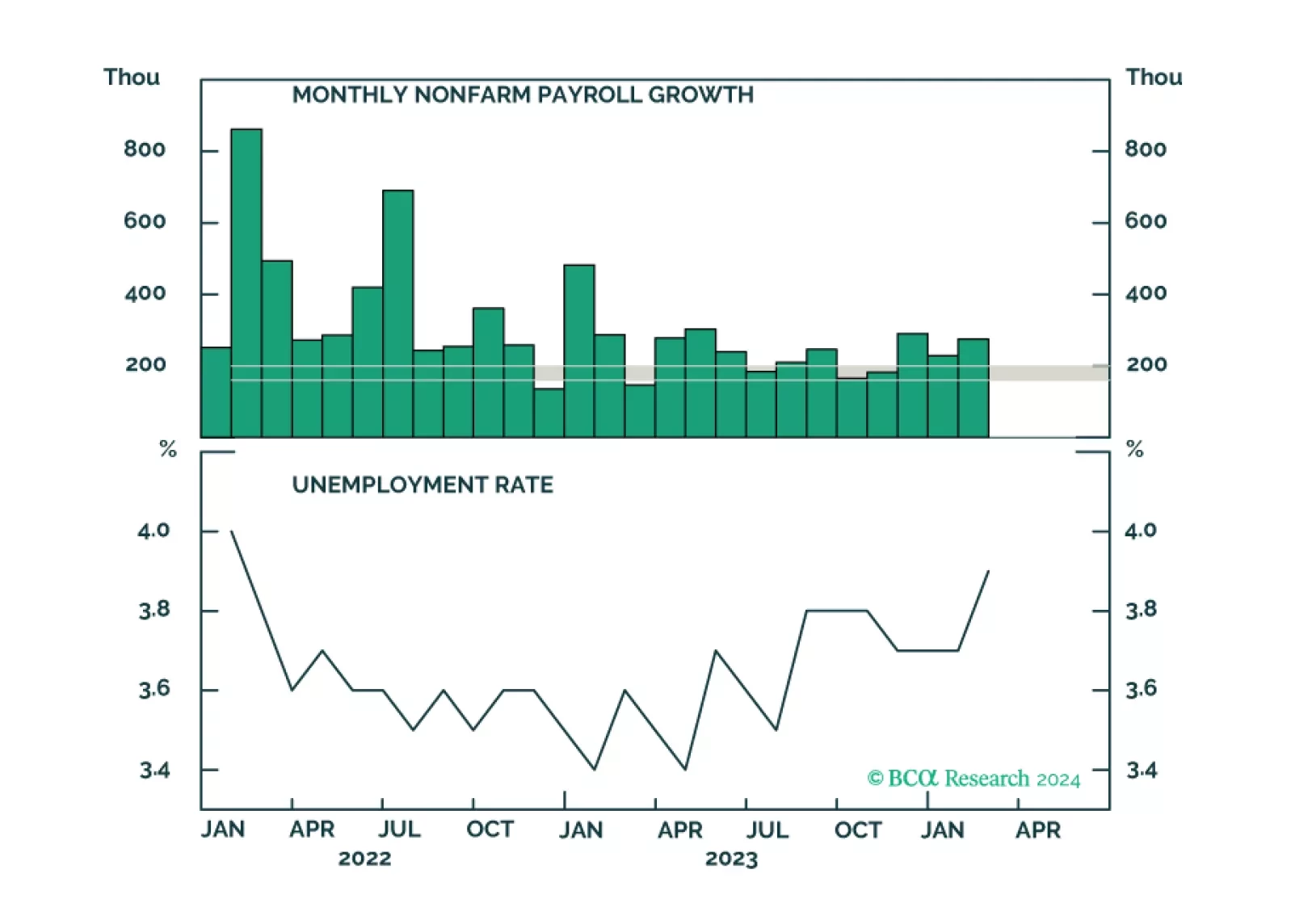

We update the indicators in our duration checklist following this morning’s employment report.

Presently, our four high-conviction themes are: (1) the US dollar will rally as US growth continues to outpace the rest of the world; (2) US equities will continue to outperform EM and European stocks until a major sell-off occurs; (3) a US profit margin squeeze is imminent; (4) EM domestic bonds and sovereign USD bonds are due for a setback.

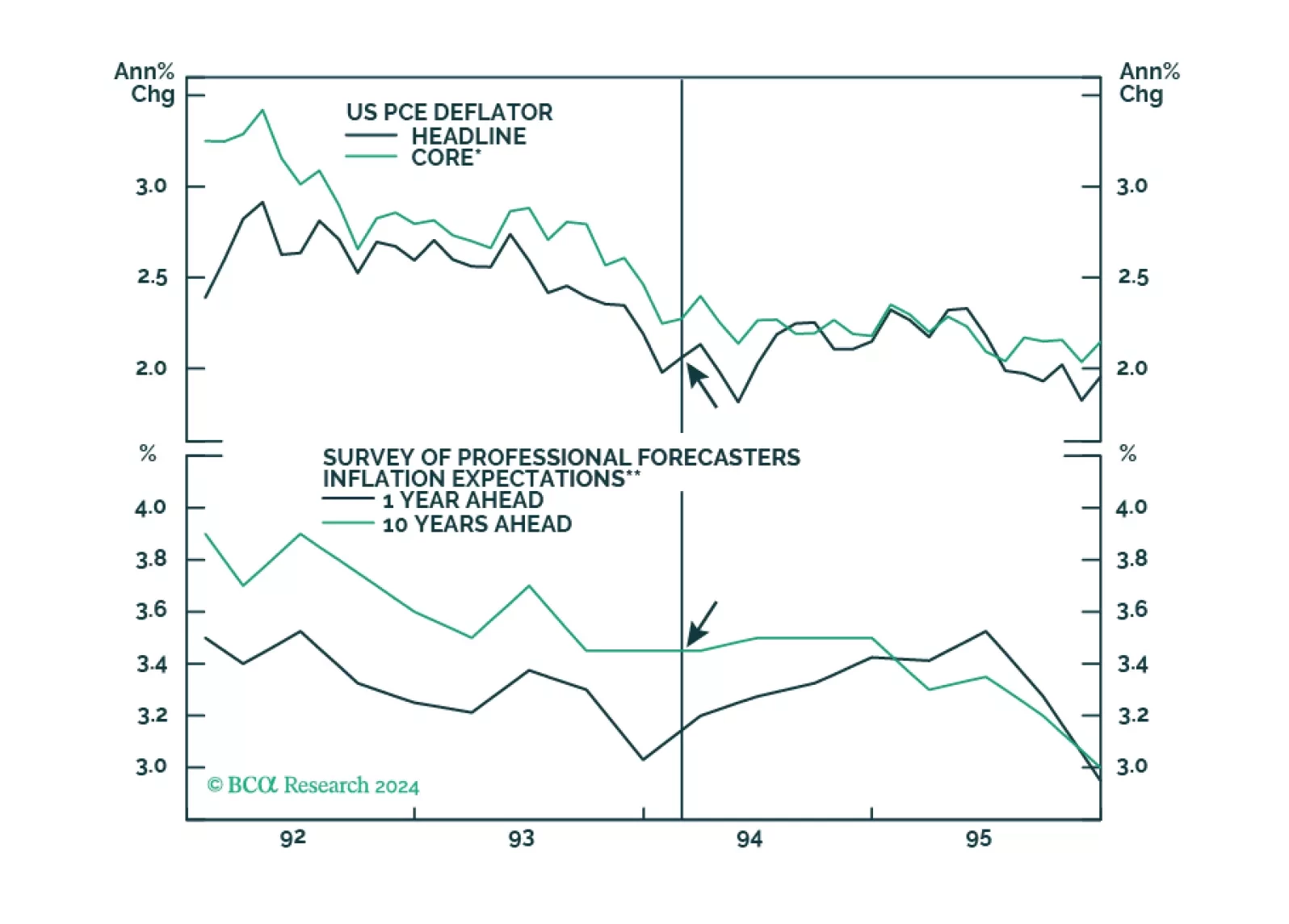

Many investors have cited the 1994 tightening cycle as an example of how the Fed managed to raise rates without triggering a recession. However, the unemployment rate was 6.5% in early 1994, which meant that inflation was less of a risk than it is today. Productivity growth also accelerated starting in the mid-1990s. While something similar may happen again thanks to AI, so far this is not visible in the aggregate productivity data.