Inflation/Deflation

The messaging from the minutes of the ECB’s January meeting was similar to the Fed. Although Governing Council members noted that “for the first time in many meetings, the risks to reaching the inflation target were seen as broadly balanced or at least…

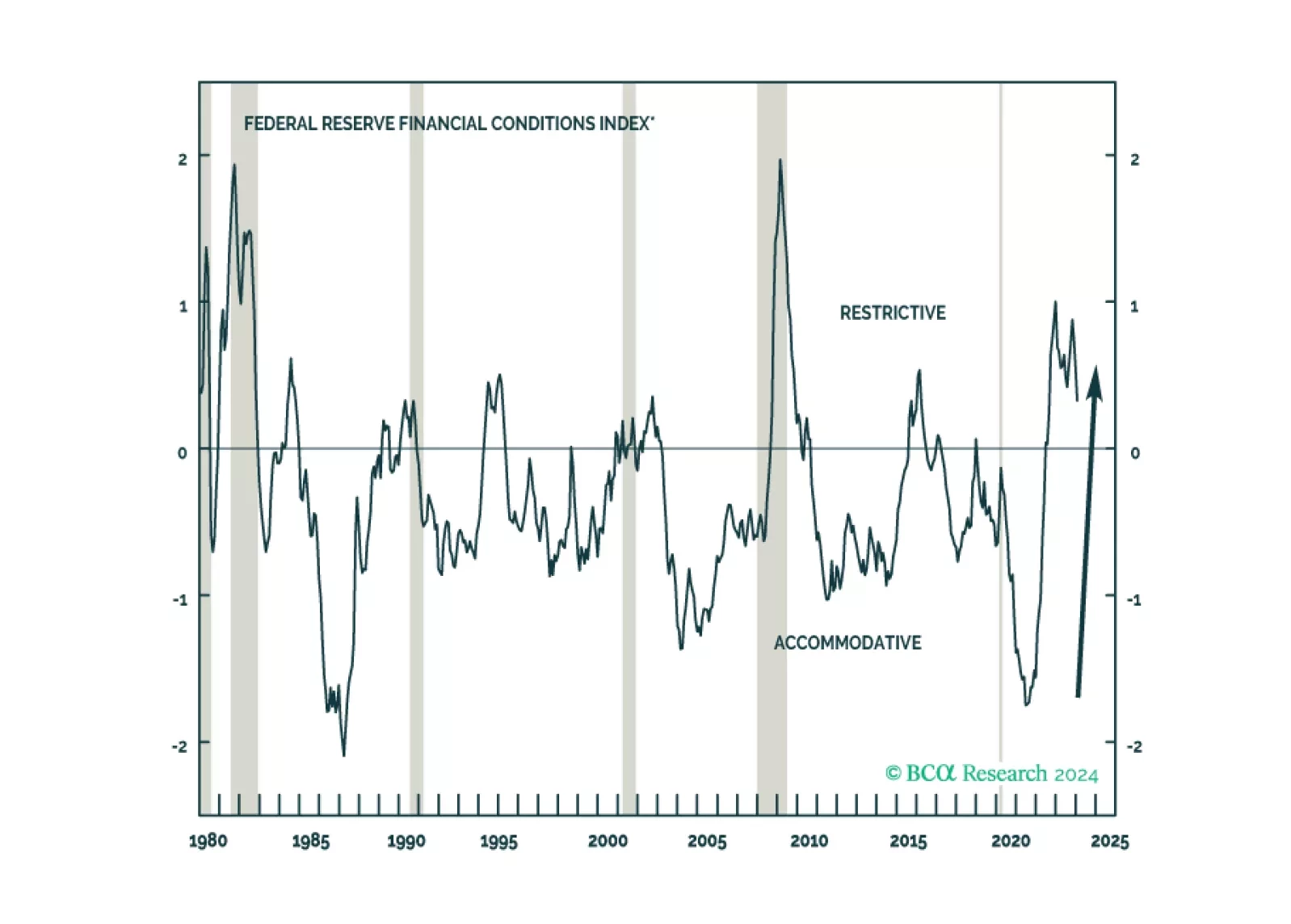

Clients have been pushing back on our recession call on the grounds that it is incompatible with the economy’s second-half acceleration and the more recent easing in financial conditions. We examine both of those points in the course of doing some pushing back of our own.

Canada’s January CPI release shows price pressures cooling last month. Headline CPI eased to 2.9%y/y from 3.4%y/y in December, below expectations of 3.3%y/y. Furthermore, month-over-month inflation fell for the first time since May 2020. Headline CPI has…

The minutes of the January FOMC meeting underscore that policymakers are adopting a cautious approach in timing the pivot to policy easing. Although Fed officials acknowledged that inflation and employment risks are “moving into better balance,” and that…

Chinese equities are extending their gains following the end of the Lunar New Year holiday. Onshore stocks have gained 9.0% since February 5, outperforming the global benchmark by 7.5 percentage points over this period. Similarly, the MSCI Investable index –…

The US Conference Board’s Leading Economic Index (LEI) fell by 0.4% m/m in January, following a 0.1% m/m drop in December – disappointing expectations of a milder decline. This marks the 23rd consecutive monthly decrease and has pushed down the index to its…

US Treasuries have been selling off over the past two months as investors downgrade the odds of an imminent start to the Fed’s easing cycle. Naturally, a question facing investors is whether current levels constitute a good opportunity to increase duration…

Democrats remain favored for reelection in 2024, which implies gridlock and policy status quo in 2025. That is not negative for stocks in the near term. However, economic, political, and geopolitical risks will escalate from here, causing volatility.

The stronger-than-anticipated acceleration in Sweden’s headline CPI inflation is unlikely to derail the Riksbank’s plan to pivot to policy easing this year. In particular, base effects from lower energy prices a year ago are behind the 1-point increase in…

The S&P 500 forged a new all-time high last Thursday and ended the week with a 4.9% year-to-date gain, extending the rally that started in late-October. Interestingly, the recent increase comes even though investors have priced out a Fed rate cut in March…