Inflation/Deflation

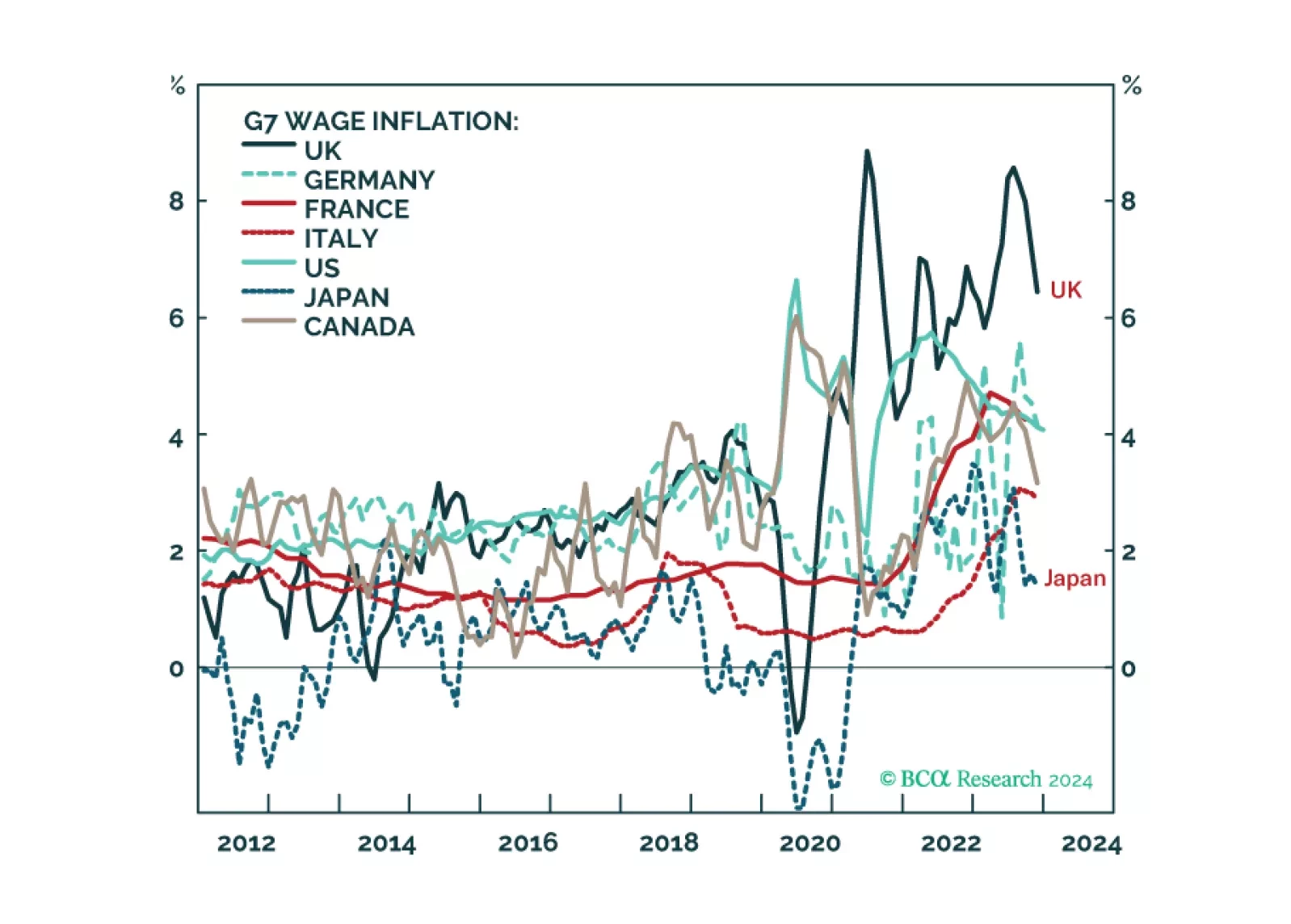

Given the huge disparities in wage inflation between the US, euro area and UK, it is remarkable that the markets are pricing near-identical rate cuts from the Fed, ECB, and BoE of around 150 bps through 2024. Assuming central banks don’t behave recklessly –…

As expected, the Bank of England voted to keep its bank rate unchanged at 5.25% on Thursday – maintaining policy on hold for the fourth consecutive meeting. Two of the nine MPC members voted in favor of a 25bps rise (one less than in December) while one…

In this Insight, we share our thoughts on yesterday’s FOMC meeting and the Fed’s likely next moves, with implications for US bond strategy.

When will the US also buckle under high rates? We expect a US recession to begin around mid-year. Stay defensive.

According to BCA Research’s Foreign Exchange Strategy service investors should remain long NOK/SEK. The Norges Bank kept policy on hold last week, but the bullish case for the NOK (albeit over the short term) remains in place. There were no major…

China’s official NBS PMI indicates that growth conditions remain sluggish. Although the composite index ticked up from 50.3 to 50.9, it is still barely in expansionary territory. Notably, the manufacturing PMI – which inched up by 0.2 points in January –…

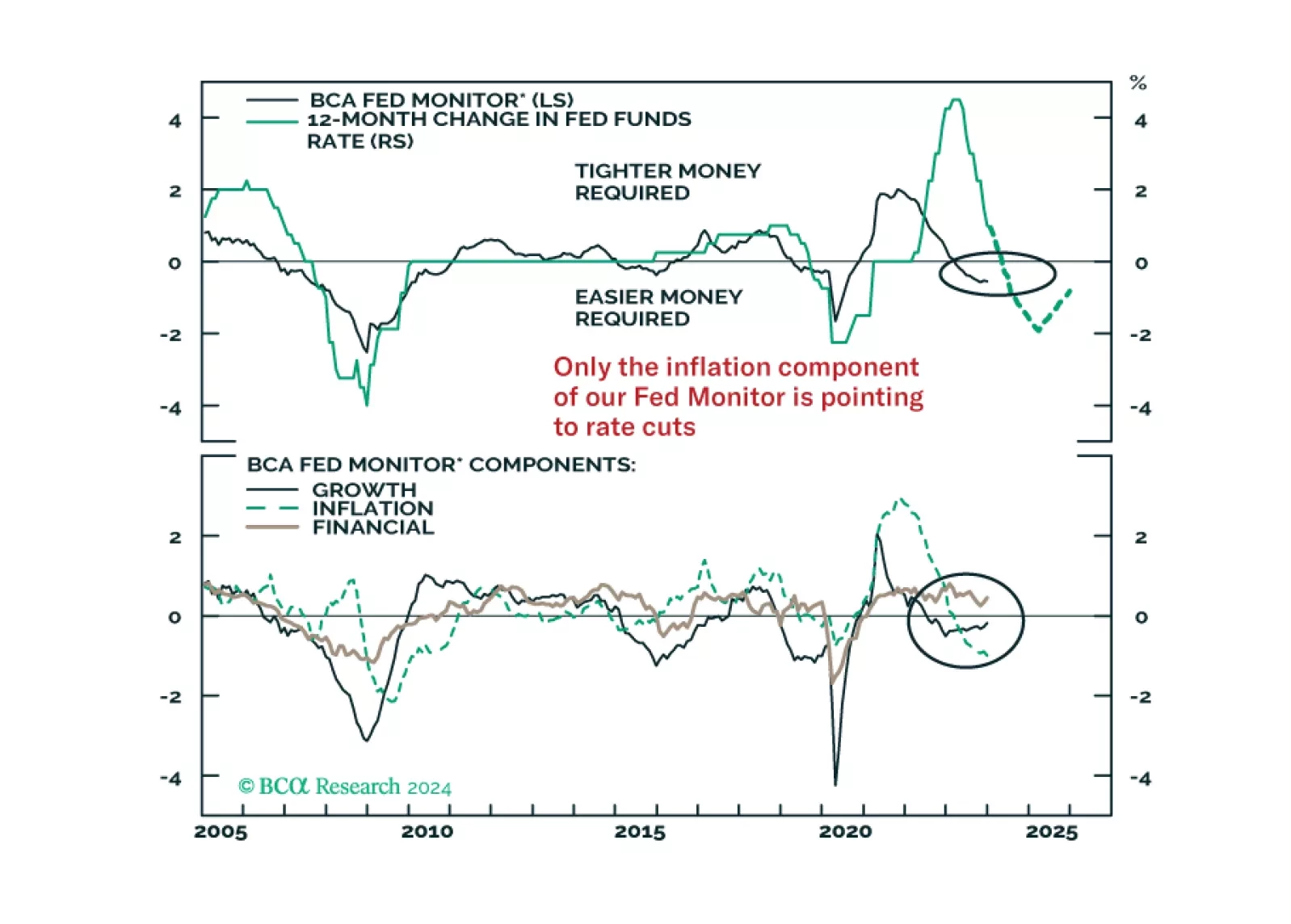

As expected, the Fed decided to keep policy unchanged at the conclusion of the FOMC meeting on Wednesday. The changes to the Fed Statement generally indicate that the central bank is preparing to move towards easing monetary policy. Specifically, the…

The US Employment Cost Index for Q4 delivered a positive signal that the disinflation process is intact. The ECI’s slowdown from 1.1% q/q to 0.9% q/q came in softer than anticipations of 1.0% q/q. This marks the slowest pace of quarterly increase since 2021Q2…

We describe and explain the wide disparity of wage inflation across G7 economies, and discuss what it means for the Fed, ECB, BoE, and BoJ policy moves in the coming year. Plus: we highlight two investments ripe for reversal, and two investments ripe for rebound.

Results of regional Fed surveys suggest that the US manufacturing sector is starting the year on a weak footing. Monday’s report from the Dallas Fed– the last to release its results for January – showed the headline manufacturing activity index collapse from…