Inflation/Deflation

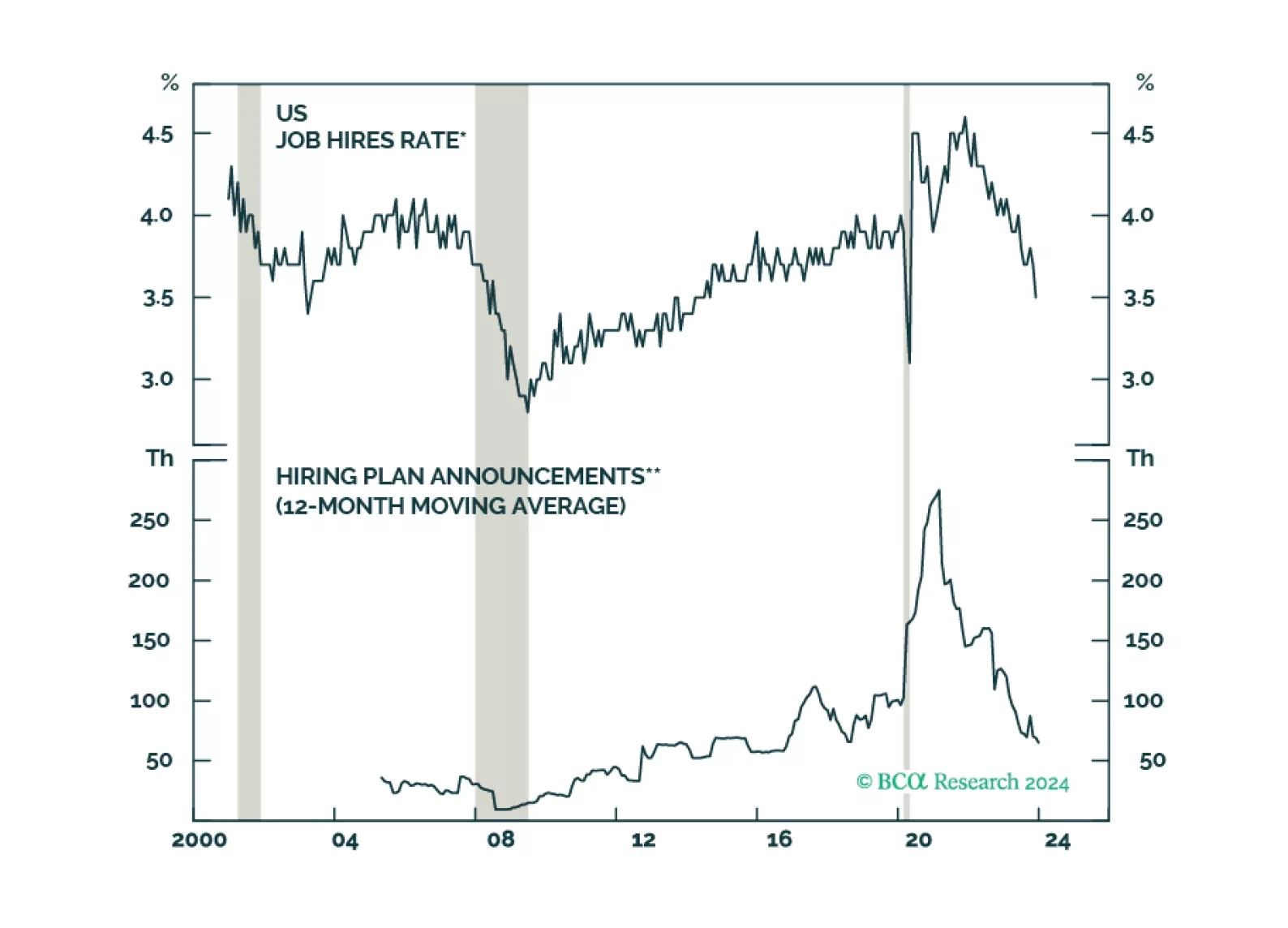

Investors have taken comfort in the fact that unemployment has remained low in the major economies. But underneath the surface, there are clear signs that labor demand is weakening. The clock keeps ticking towards our H2 2024 recession call. After being bullish on risk assets last year, we are slowly turning more defensive.

The Central Bank of Brazil (BCB) has cut the Selic rate by 50 basis points in each of the past four meetings and has alluded to maintaining this size of cuts for the coming meetings. Governor Roberto Campos Neto stated last month that he aims to bring…

An update to our outlooks for the Fed’s interest rate and balance sheet policies following this week’s remarks from Fed Governor Waller.

The British pound was the best performing G10 currency on Wednesday as UK gilts sold off meaningfully with the 10-year yield ending the day nearly 19 basis points higher. An unexpected acceleration in CPI inflation in December prompted the move. Notably,…

The US retail sales release delivered a positive signal about the US economy in December. The 0.6% m/m increase in overall retail sales beat expectations of a more muted acceleration from 0.3% m/m to 0.4% m/m. Importantly, the improvement was broad-based with…

Chinese data continues to send a pessimistic signal for domestic risk assets and China plays. Although at 5.2% in Q4, GDP growth stands above the official target, it underwhelmed anticipations of 5.3%. Moreover, other data releases reveal that the economy…

Results of the ZEW survey sent a slightly positive signal on German investor sentiment. The economic expectations indicator rose to an 11-month high in January – beating consensus estimates of a decline. This increased optimism about the outlook reflects an…

Canadian government bond yields jumped on Tuesday, with the 10-year yield rising by nearly 14 basis points. While most other major DM government bonds also sold off, the move in Canadian yields was relatively more pronounced. Both global and domestic forces…

Canada’s Business Outlook Survey (BOS) indicator increased slightly in Q4, suggesting that sentiment stabilized at the end of 2023. In particular, easing inflationary pressures amid weaker demand and greater competition drove the 0.3-point uptick. Notably,…

The soft-landing narrative has won, but is too much of a good thing now expected by investors?