Inflation/Deflation

Copper benefited from the recent improvement in global risk sentiment, participating in the broad-based rally in November. To the extent that the red metal has vast applications across many economic sectors, it is considered a reliable gauge of global…

The BoC kept its policy rate steady at 5% for the fourth consecutive meeting on Wednesday, in line with expectations. In its press release, the BoC maintained that it is ready to keep hiking if deemed necessary. That said, the BoC noted that inflationary…

The number of US job openings fell sharply in October according to the JOLTS survey, from 9.4 million to 8.7 million. At 8.7 million, job openings are still above the 7.1 million average seen in the two years prior to the pandemic. Viewed in isolation, this…

The November services PMIs sent a slightly positive signal on Tuesday. The global measure ticked up from 50.4 to 50.6, pointing to a marginal pickup in the pace of expansion. Importantly, this slight improvement was broad-based across the major global…

The Reserve Bank of Australia (RBA) kept the cash rate unchanged at 4.35% on Tuesday, in line with expectations. In her post-meeting statement, Governor Michele Bullock revealed that economic developments since the RBA’s November rate increase have been in…

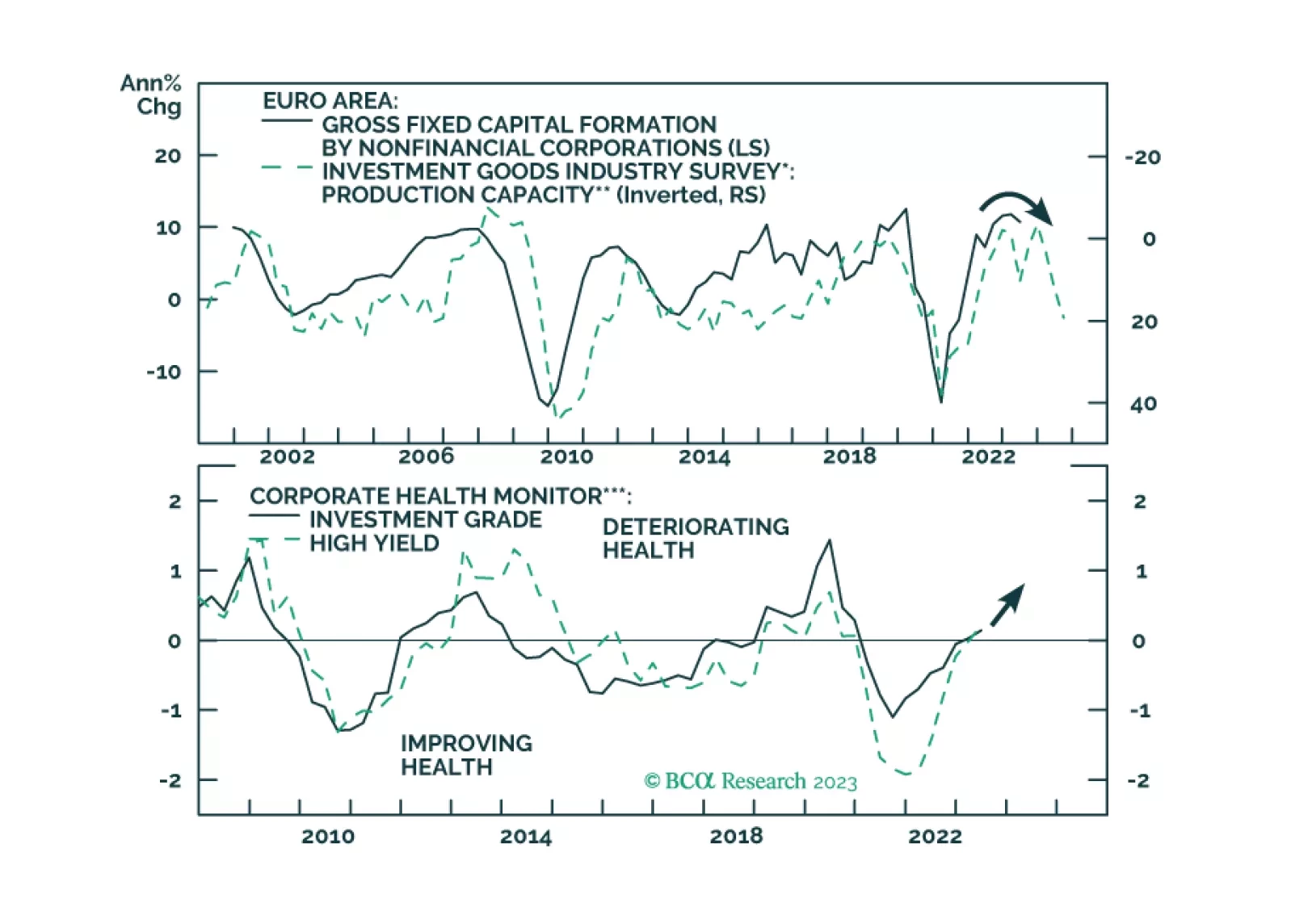

According to BCA Research’s European Investment Strategy service, European corporate spreads will widen over the coming six months before an attractive buying opportunity emerges in the second half of 2024. 2024 will likely be characterized by three credit…

In the monthly Daily Insights Survey we conducted over the past week, we asked about our readers’ outlook for the timing of the next US recession, the Fed, and concerns for the global economy in 2024. On the US economic outlook, nearly all respondents…

The recent uptick in European economic data will not last beyond the next six months. How will European corporate credit perform in this context?

We enter 2024 as we were across the last four months of 2023, tactically equal weight across the board until the S&P 500 rally is complete and we gain a better entry point for underweighting equities and overweighting fixed income.

Treasury yields will sketch out a range between now and Q1 2024, with the upside determined by inflation and the downside determined by labor markets.