Inflation/Deflation

Powell’s final Jackson Hole speech signaled a dovish tilt, opening the door to a September cut. The Fed is under pressure to balance unemployment and inflation risks, with the FOMC split between “proactive” doves and “reactive” hawks. Recent data have not…

Indonesia’s surprise rate cut signals a dovish turn that will weigh on the rupiah. Bank Indonesia cut its policy rate by 25 bps to 5%, with low inflation and weak activity pointing to more easing ahead. Our Emerging Markets team’s proprietary super core…

The Philly Fed’s August dip confirms persistent US manufacturing weakness and sends a disinflationary impulse. The index fell to -0.3 from 15.9 in July, with shipments, employment, and new orders all declining, the latter slipping into contraction.…

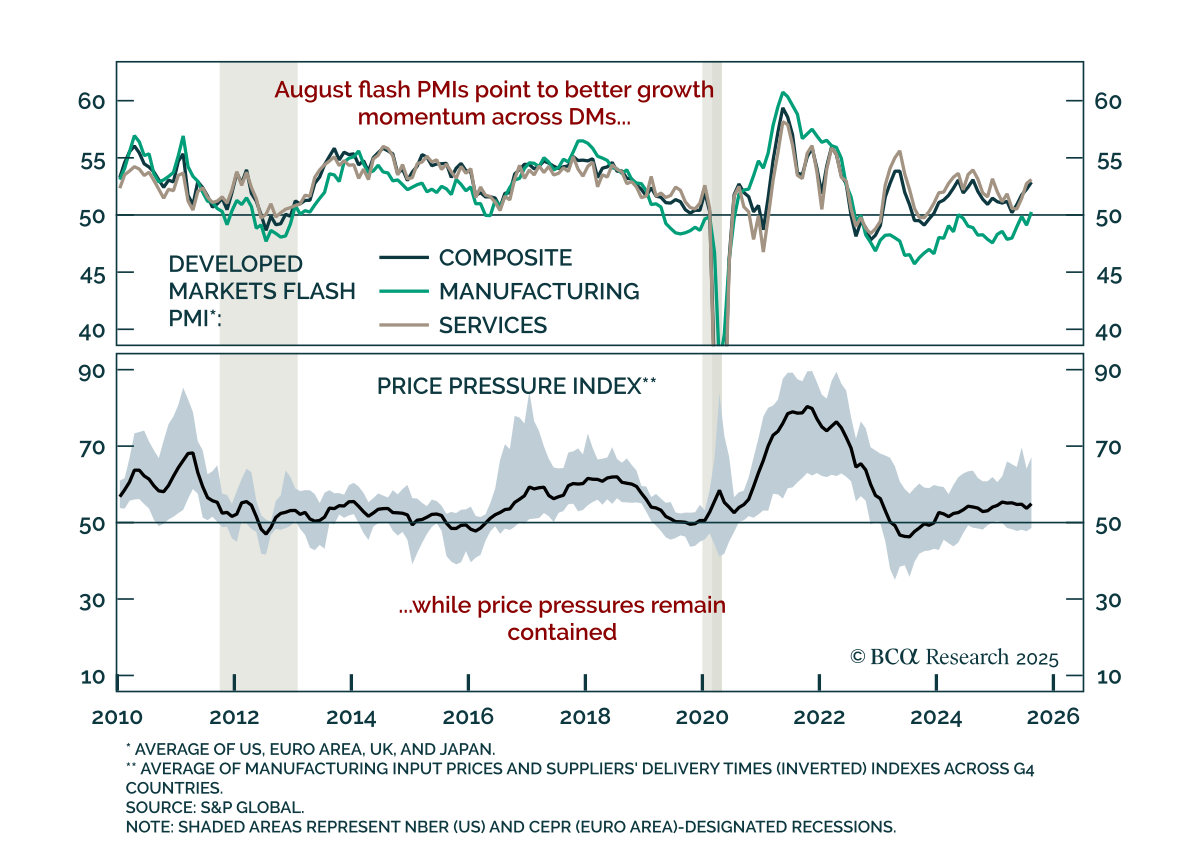

Flash August PMIs show tentative global momentum yet growth remains weak. The composite PMI improved in both the US (55.4 vs. 55.1) and euro area (51.1 vs. 50.9), with manufacturing moving into expansion for the first time in 18 months. US manufacturing…

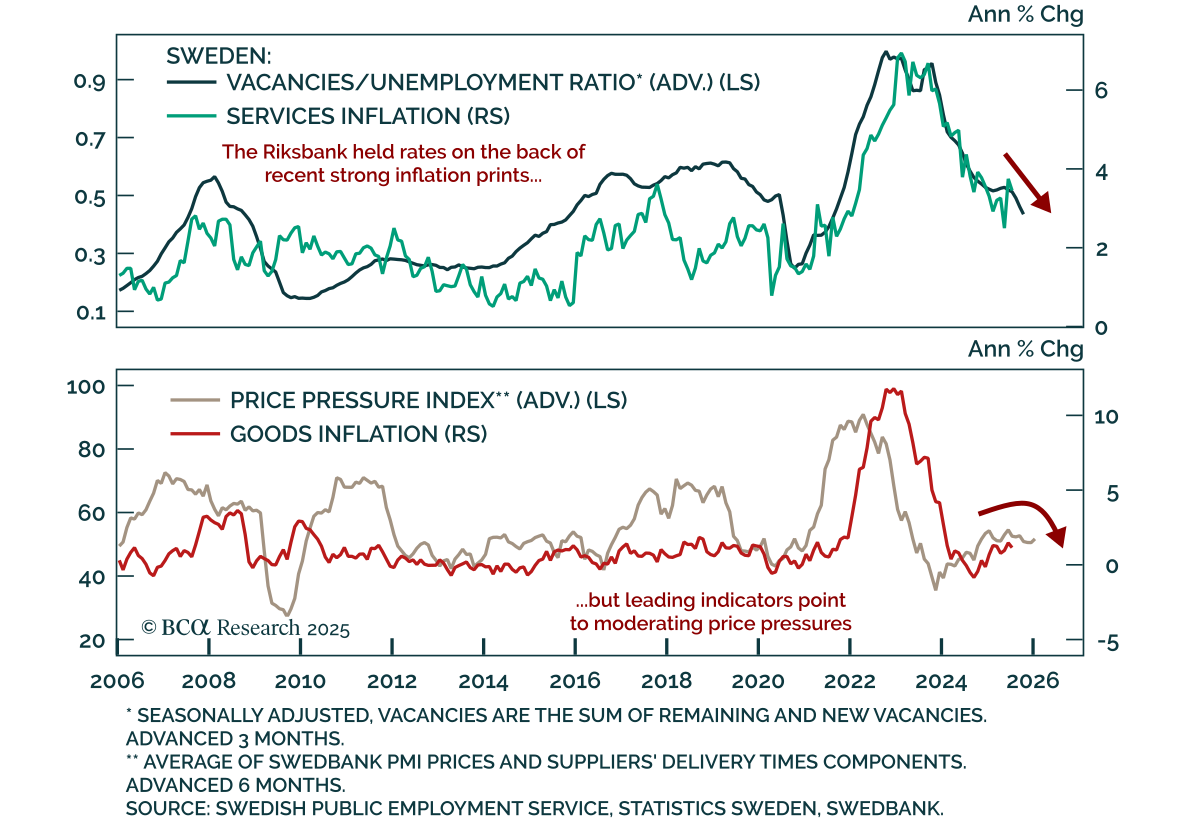

The Riksbank held at 2.0% as core inflation remains above target, though easing pressures are building. July headline inflation had slightly cooled, but core remains above both the bank’s forecast and the 1-3% target band. Inflation drivers point to…

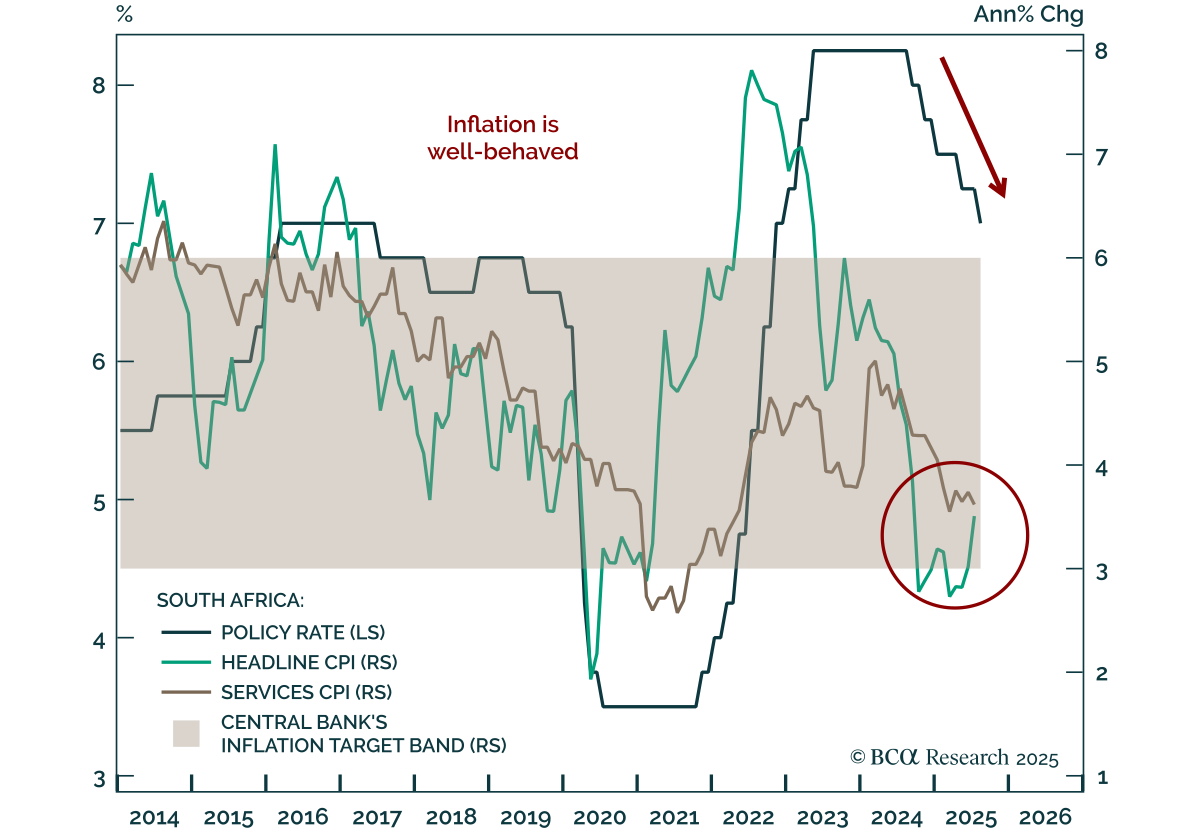

South African inflation will remain at the bottom of the SARB target range, allowing further easing. July CPI came in line with expectations at 3.5% y/y, with core at 3.0%. Our Emerging Markets strategists expect the central bank to keep cutting in…

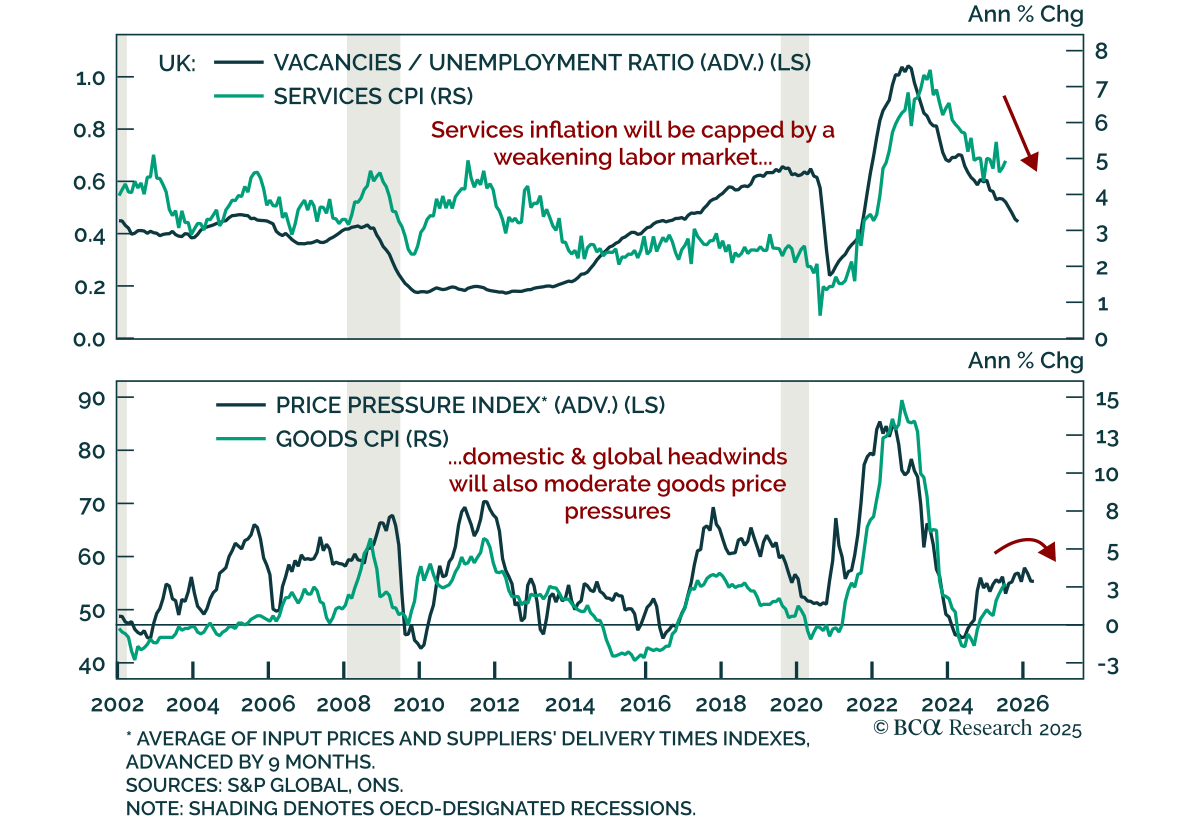

Hot July inflation does not alter the weakening UK backdrop, keeping Gilts attractive and GBP vulnerable. Headline CPI rose 0.1% m/m, lifting y/y inflation to 3.8% from 3.6%, while core ticked up to 3.8% from 3.7%. Services inflation remained sticky,…

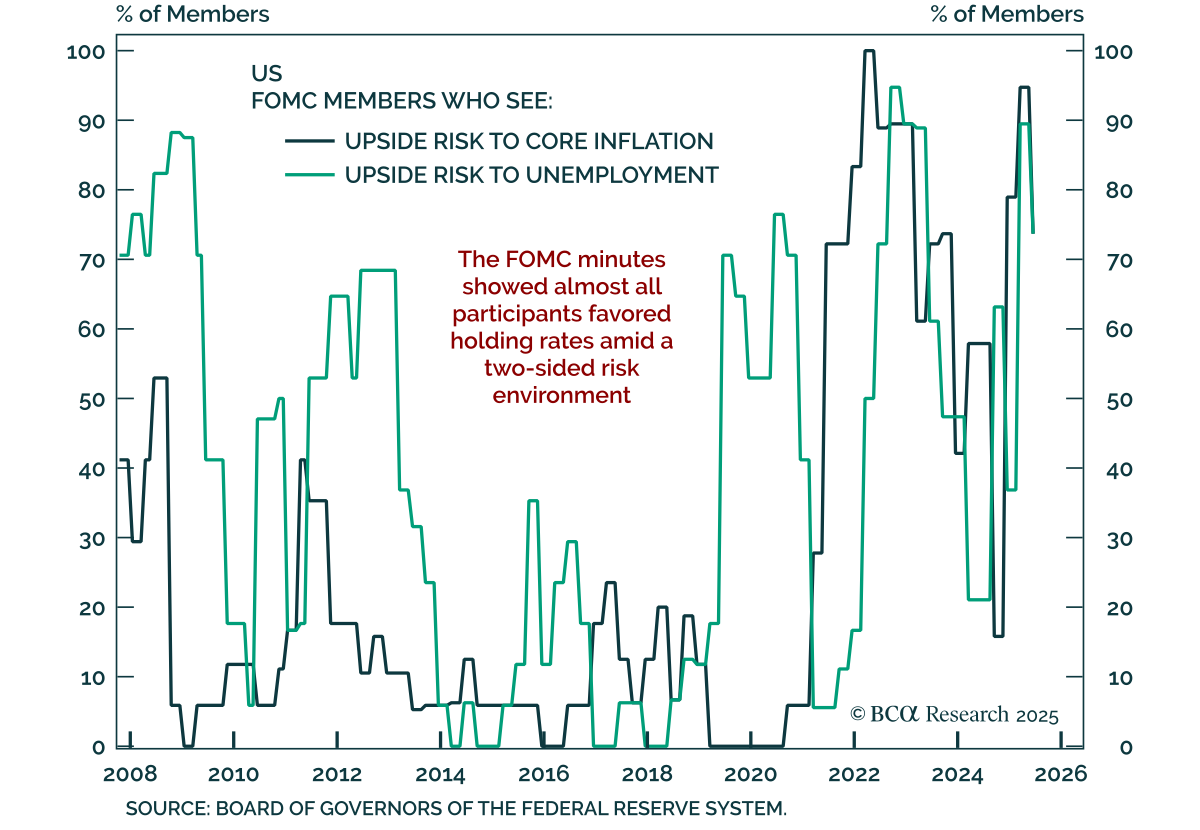

FOMC minutes showed broad support to hold in July, but the committee remains divided between proactive doves and reactive hawks. “Almost all members” favored leaving the funds rate unchanged, though two dissented for an immediate 25 bps cut. Doves want…

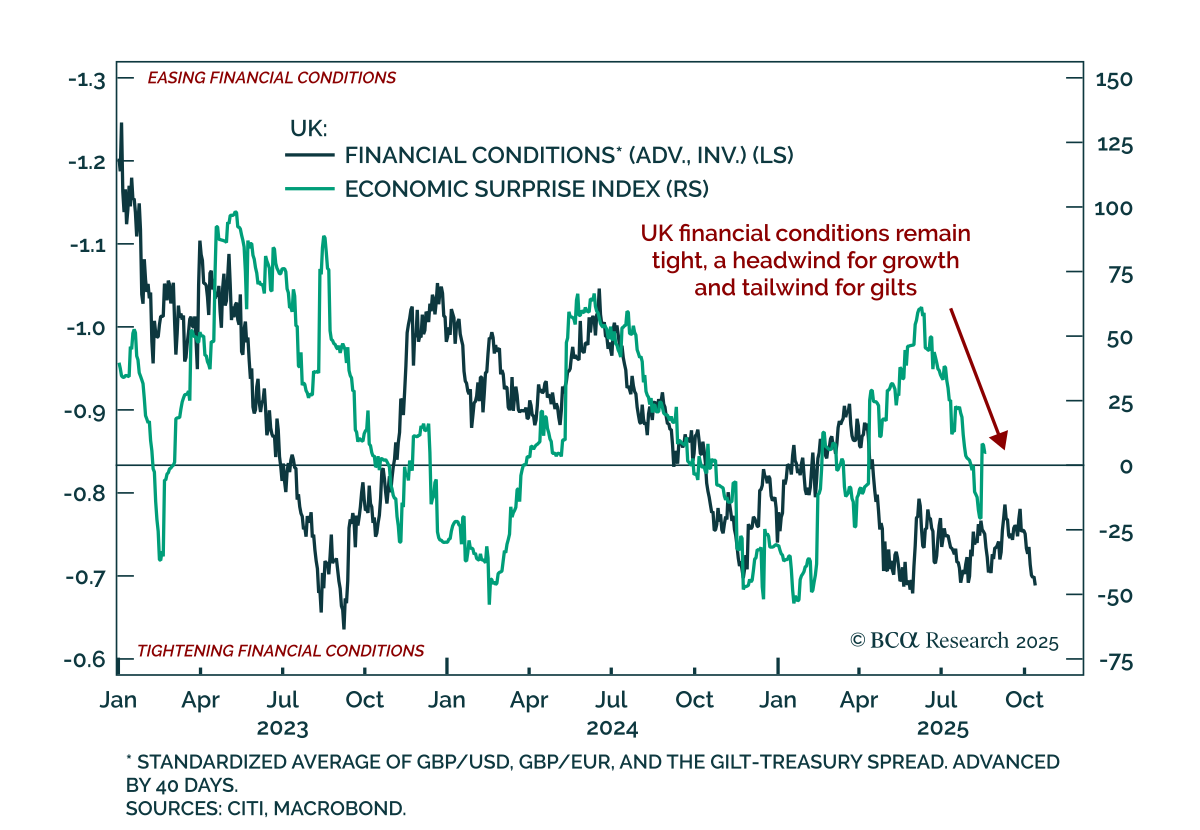

UK data momentum is fading, keeping Gilts attractive and GBP vulnerable. At 5.60%, 30-year Gilts trade at their highest yields since the late 1990s, reflecting persistent pressure on the long end across DMs. The Bank of England has lagged the ECB in its…

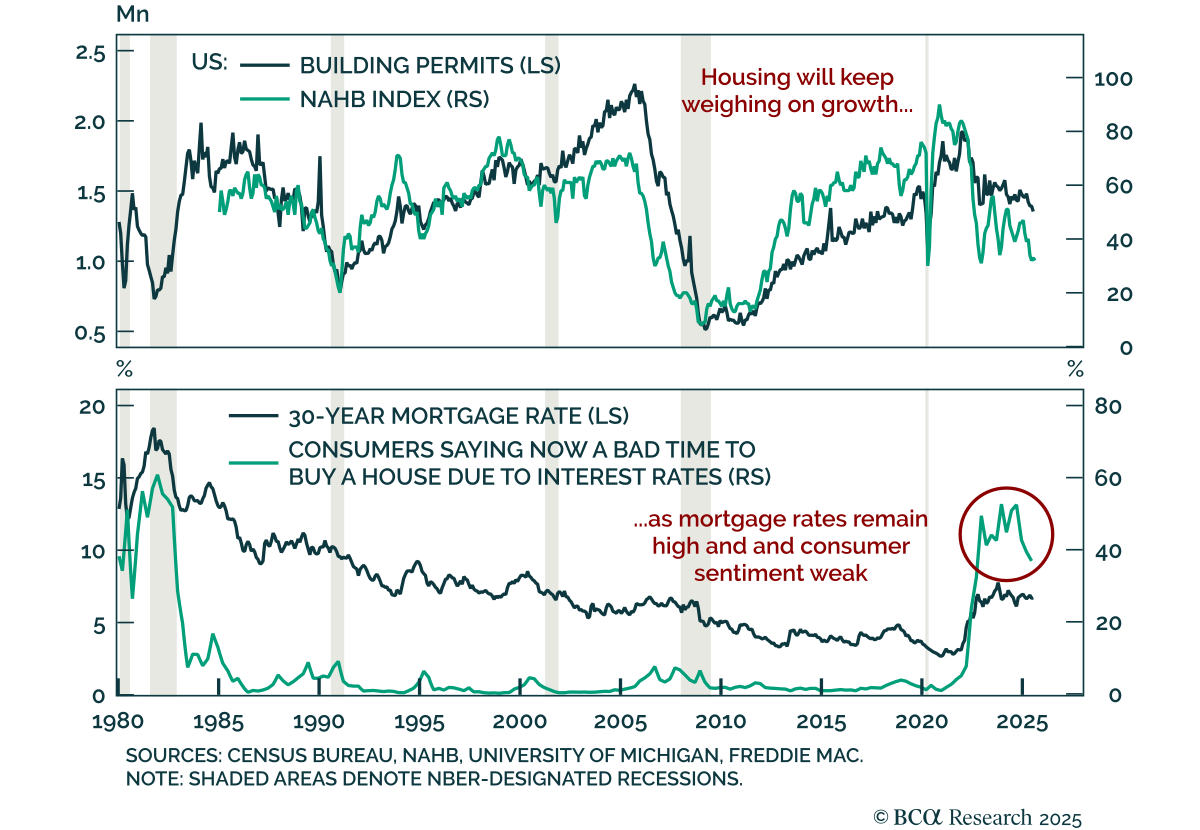

US housing data remain weak, reinforcing a fragile growth backdrop and the need for equity downside protection. July housing starts rose 5.2% m/m (annualized), but building permits fell 2.8% following a small June decline. The August NAHB Housing Market…