Inflation/Deflation

Inspired by a client’s questions, we examine the rationale behind the implementation of the trailing stop governing our near-term asset allocation recommendations.

European real GDP growth is stabilizing, so why would European equities continue to trade sideways for the remainder of the year? The answer lies with nominal growth and its impact on earnings.

Investors should think probabilistically about the economy and financial markets. In the face of non-linear effects, the range of possible outcomes can be very large. A systematic application of Bayes’ rule can help improve decision-making.

Numerous divergences have opened up between global risk assets and global business cycle variables. These gaps are unsustainable, and odds are that the recoupling will occur to the downside with risk assets selling off.

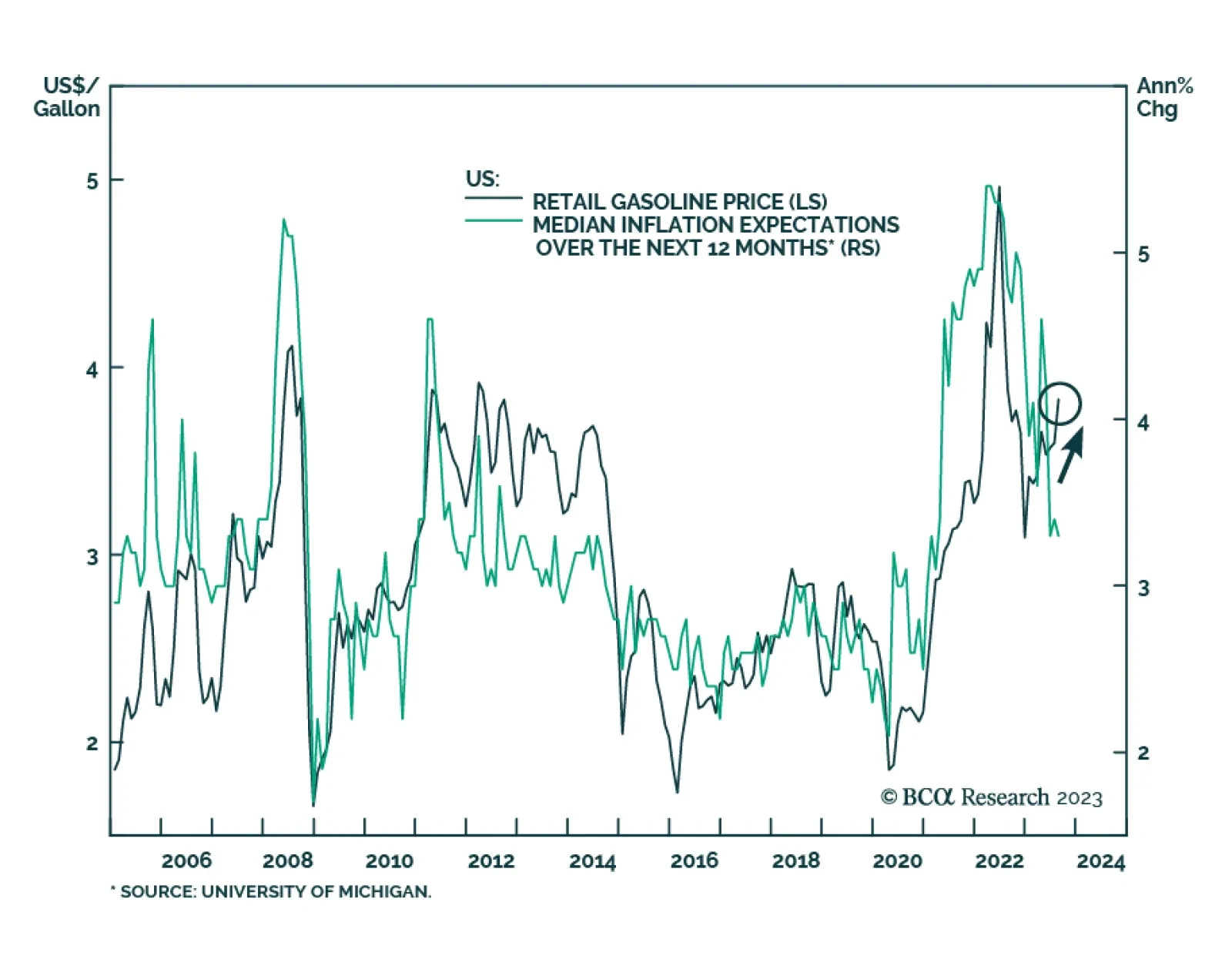

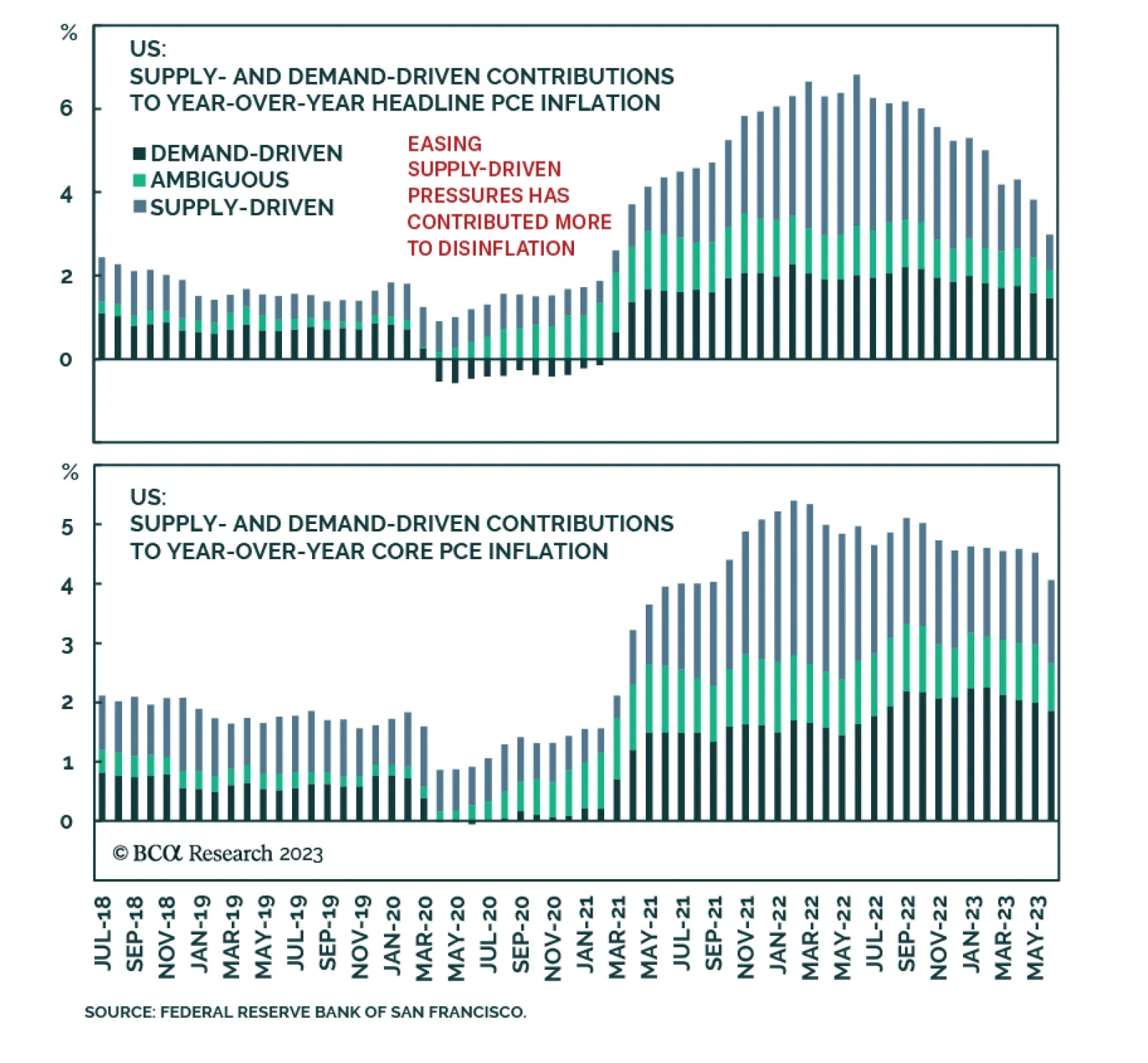

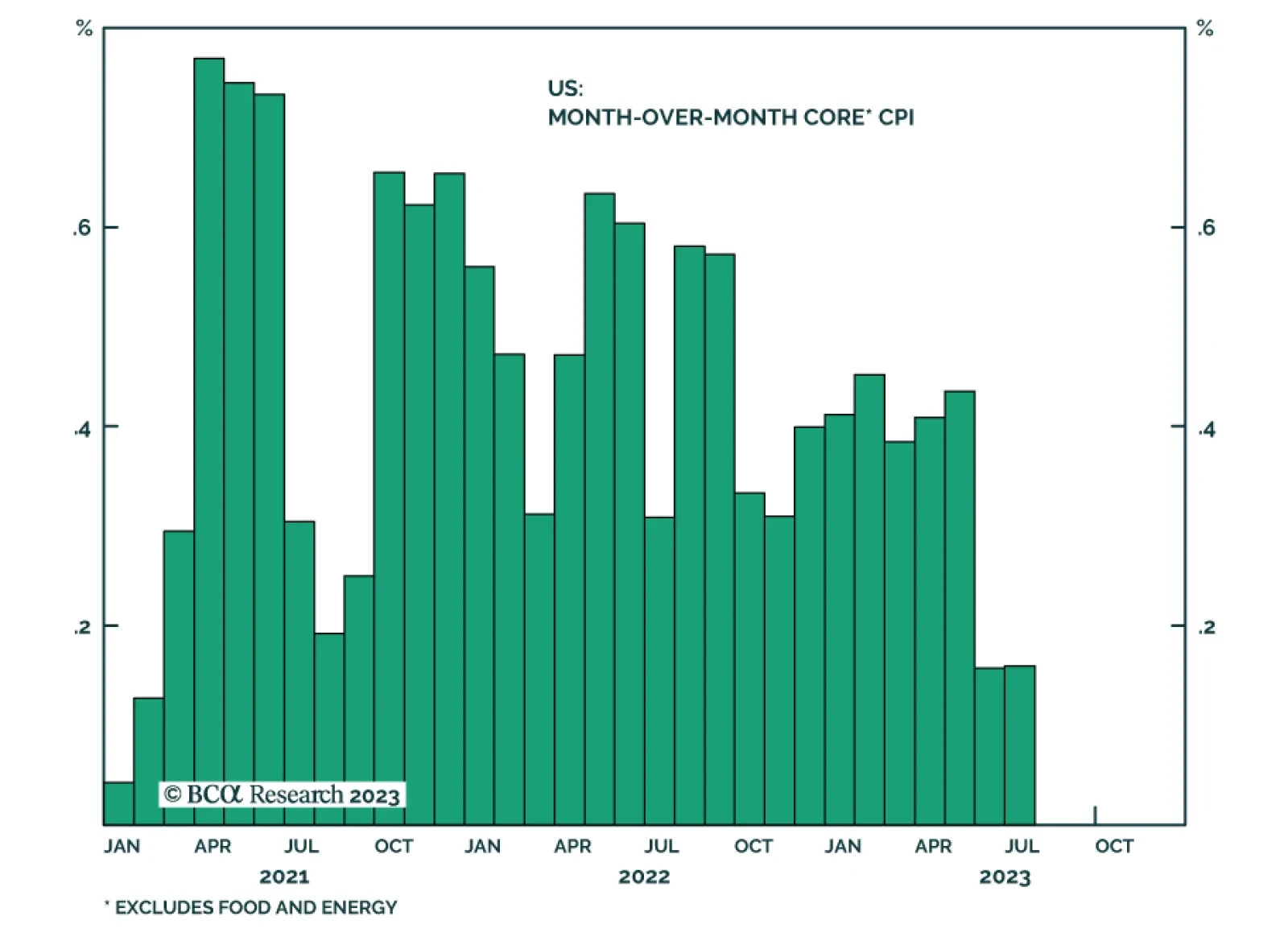

Some thoughts on this morning’s inflation number and implications for Treasury yields and TIPS.