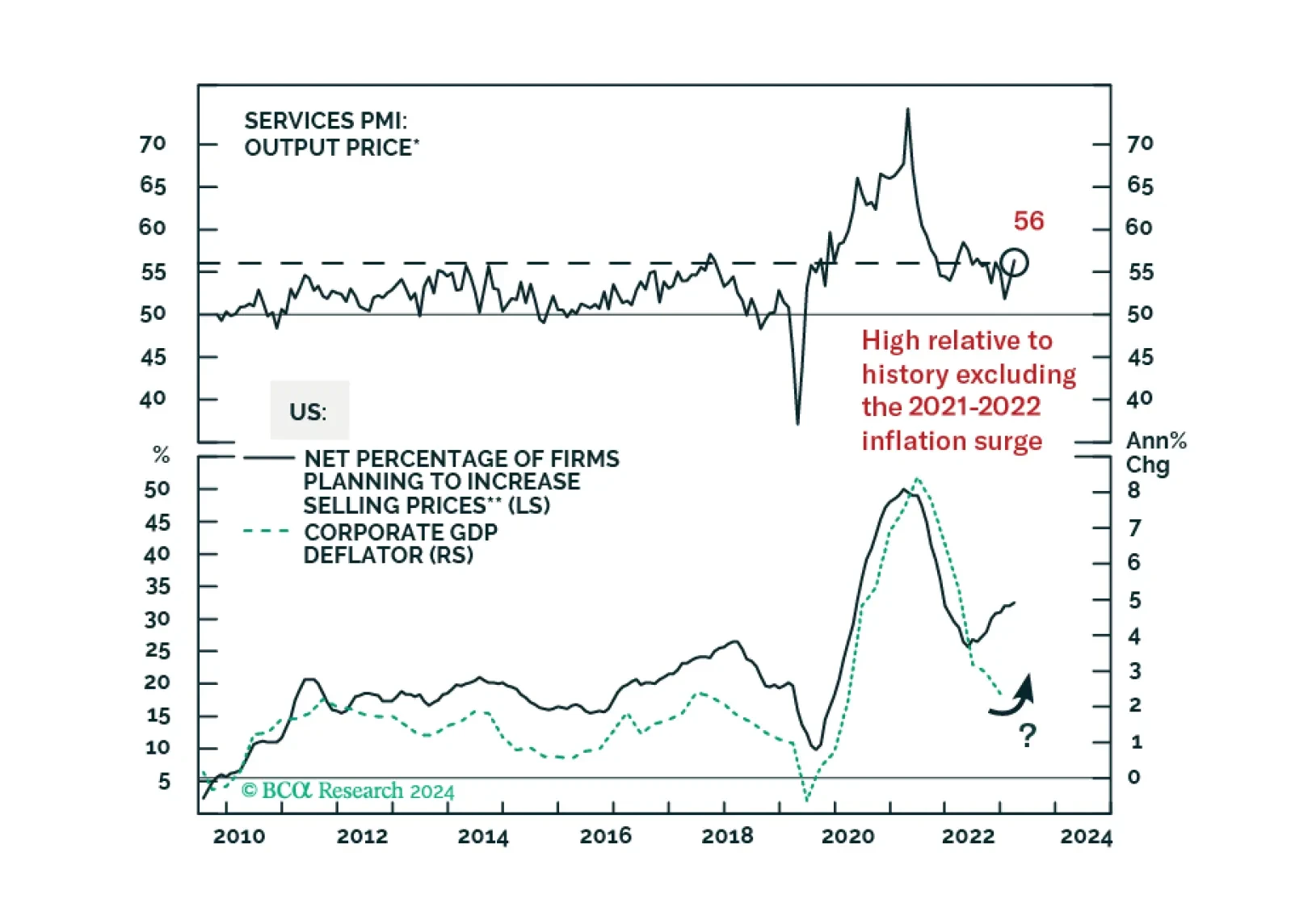

Inflation

Investors should prepare for economic data to weaken even as policy uncertainty and geopolitical risk skyrocket ahead of the US election.

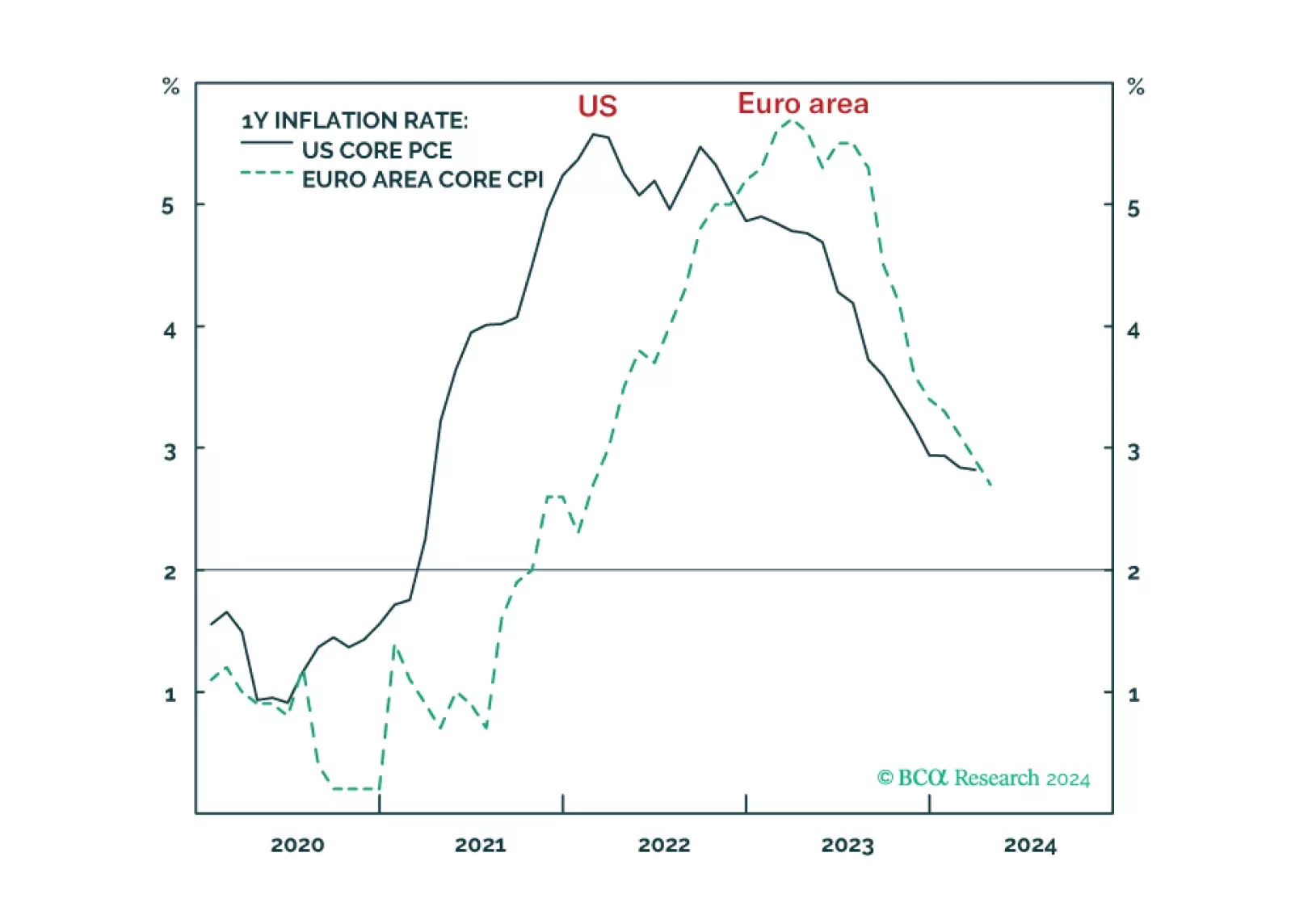

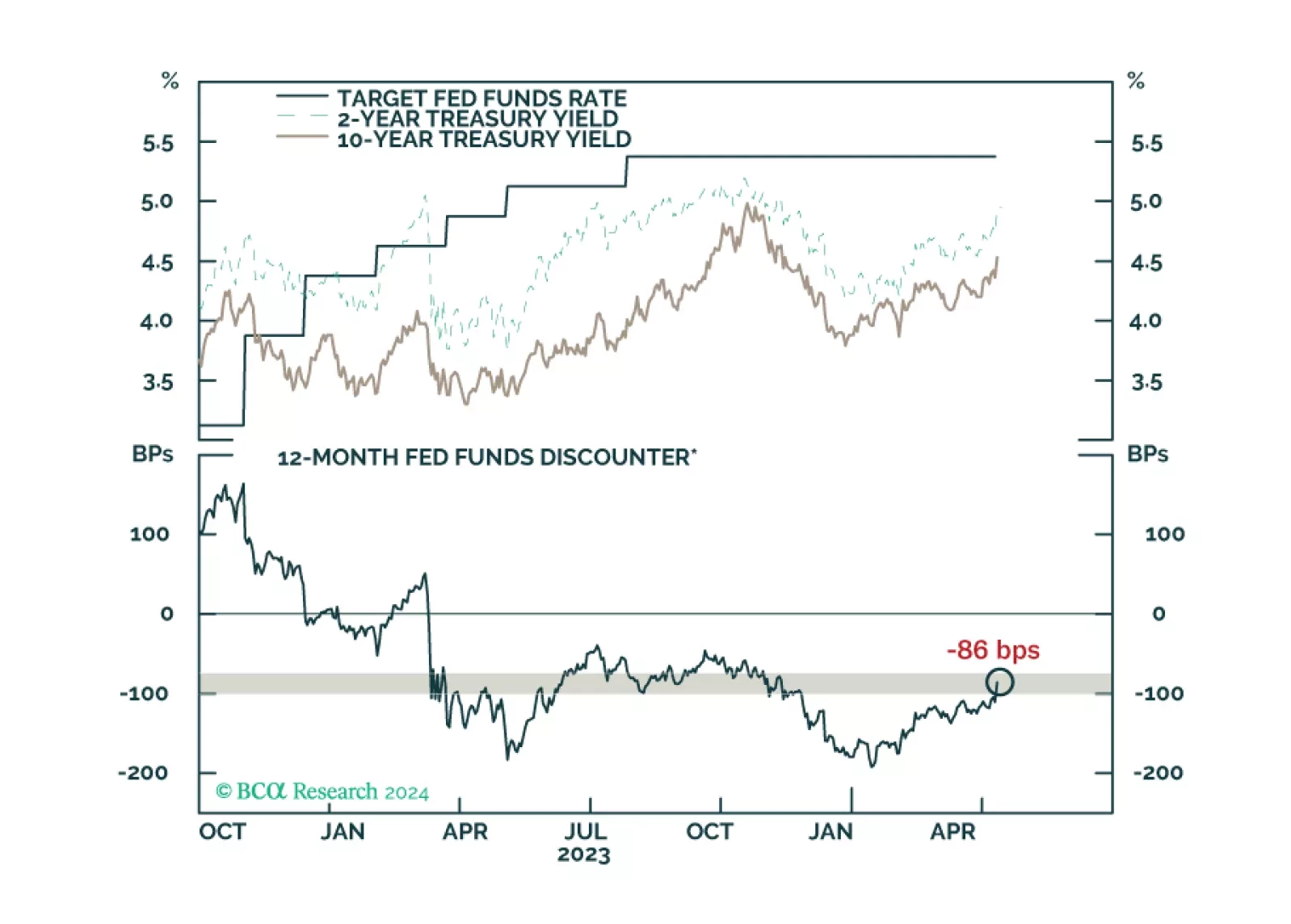

Wild hopes for US rate cuts got shattered, exactly as we predicted. But given the different incentives that the Fed and ECB now face, the relative pricing between the Fed and the ECB could widen further in the coming months. We discuss the implications for rates, the dollar, and the relative positioning in US versus European equities.

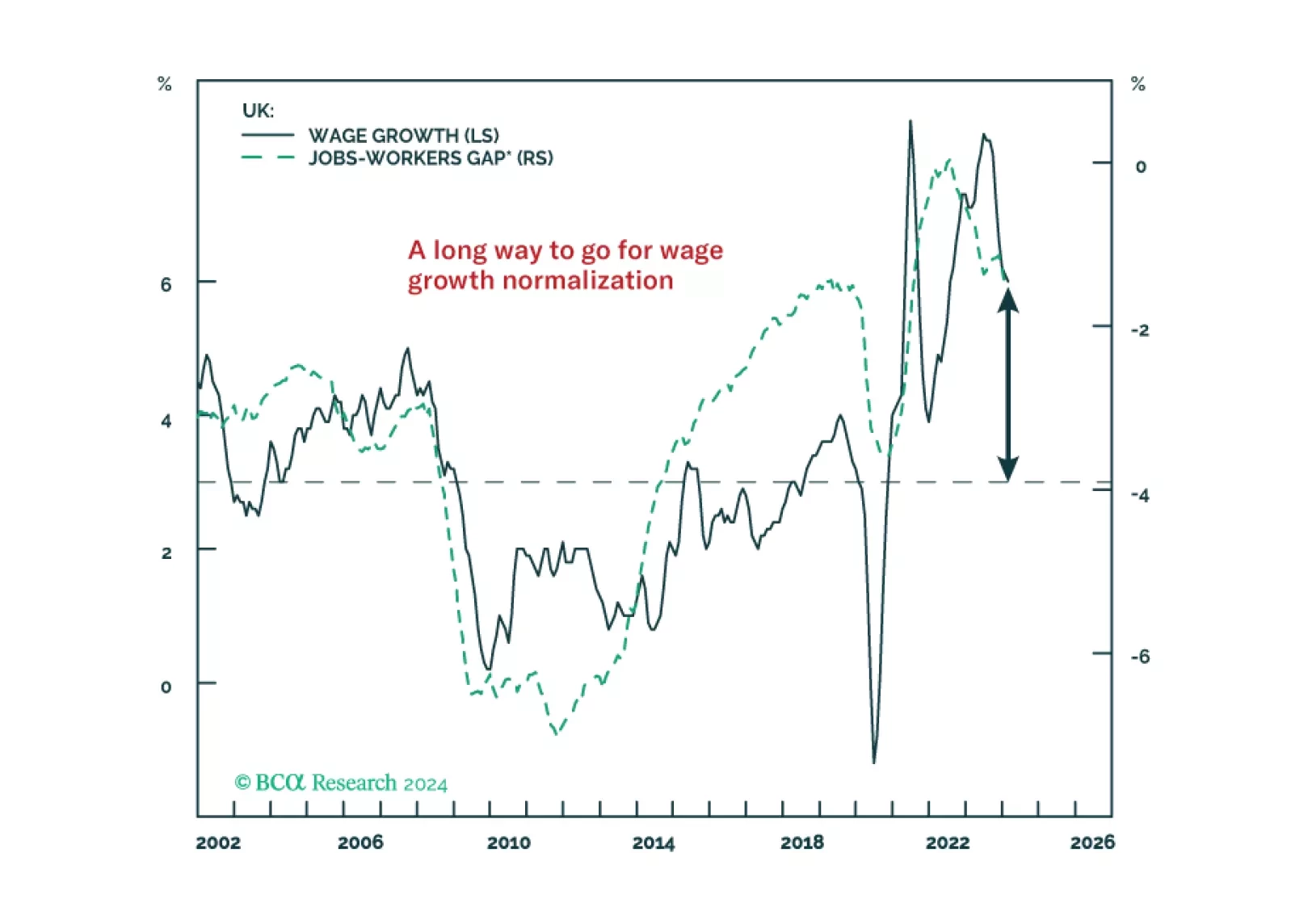

The UK labor market remains far too tight to expect wage growth to slow to levels consistent with the Bank of England inflation target. A true recession with rising unemployment is needed to finally slay the UK inflation beast. 2024 rate cuts are off the table, with the central bank having to keep monetary policy tighter for longer than markets expect and the UK economy now rebounding. We recommend downgrading UK gilts to underweight in global bond portfolios, while also looking for opportunities to buy the British pound on pullbacks versus the euro, Canadian dollar and Swedish krona.

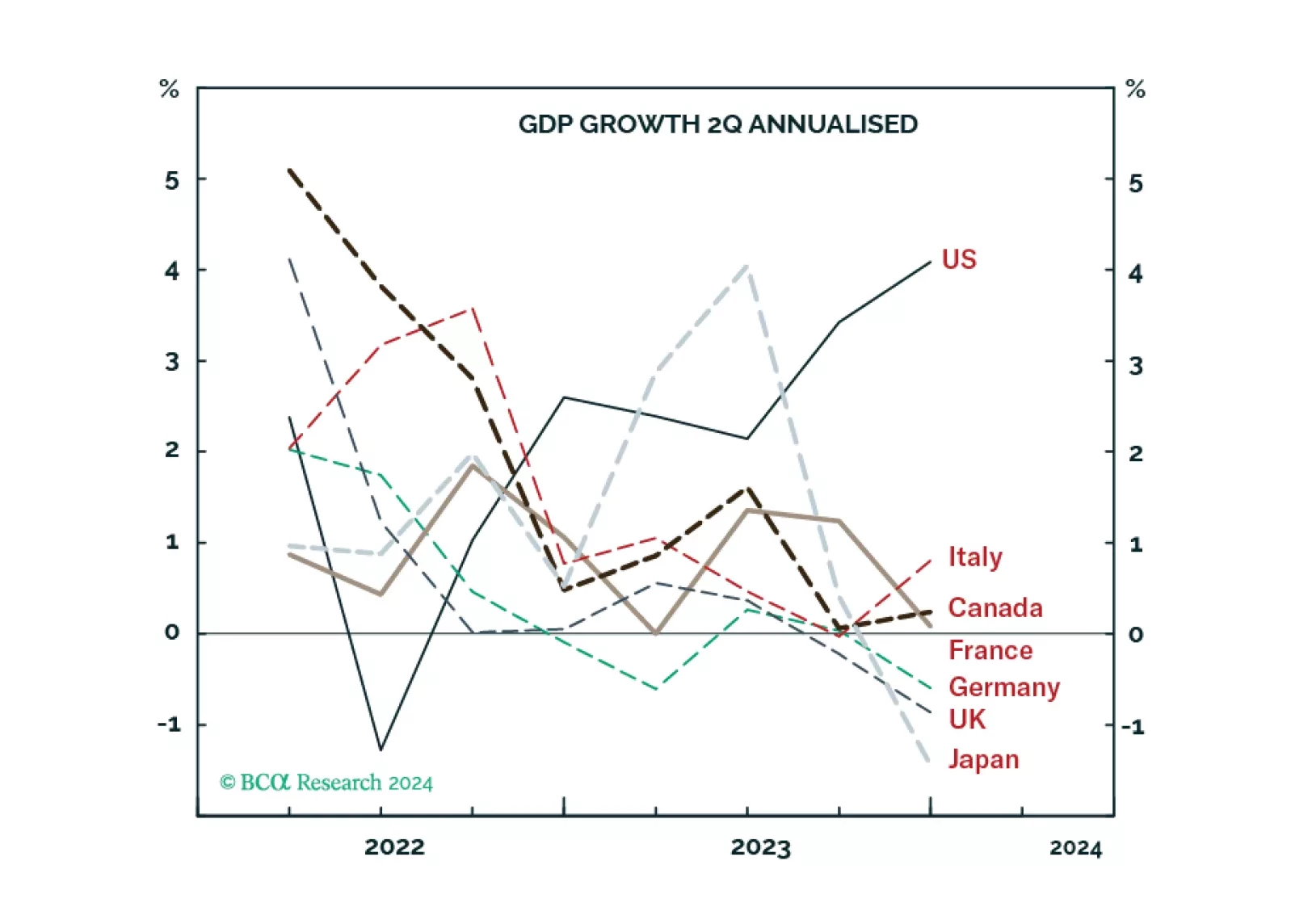

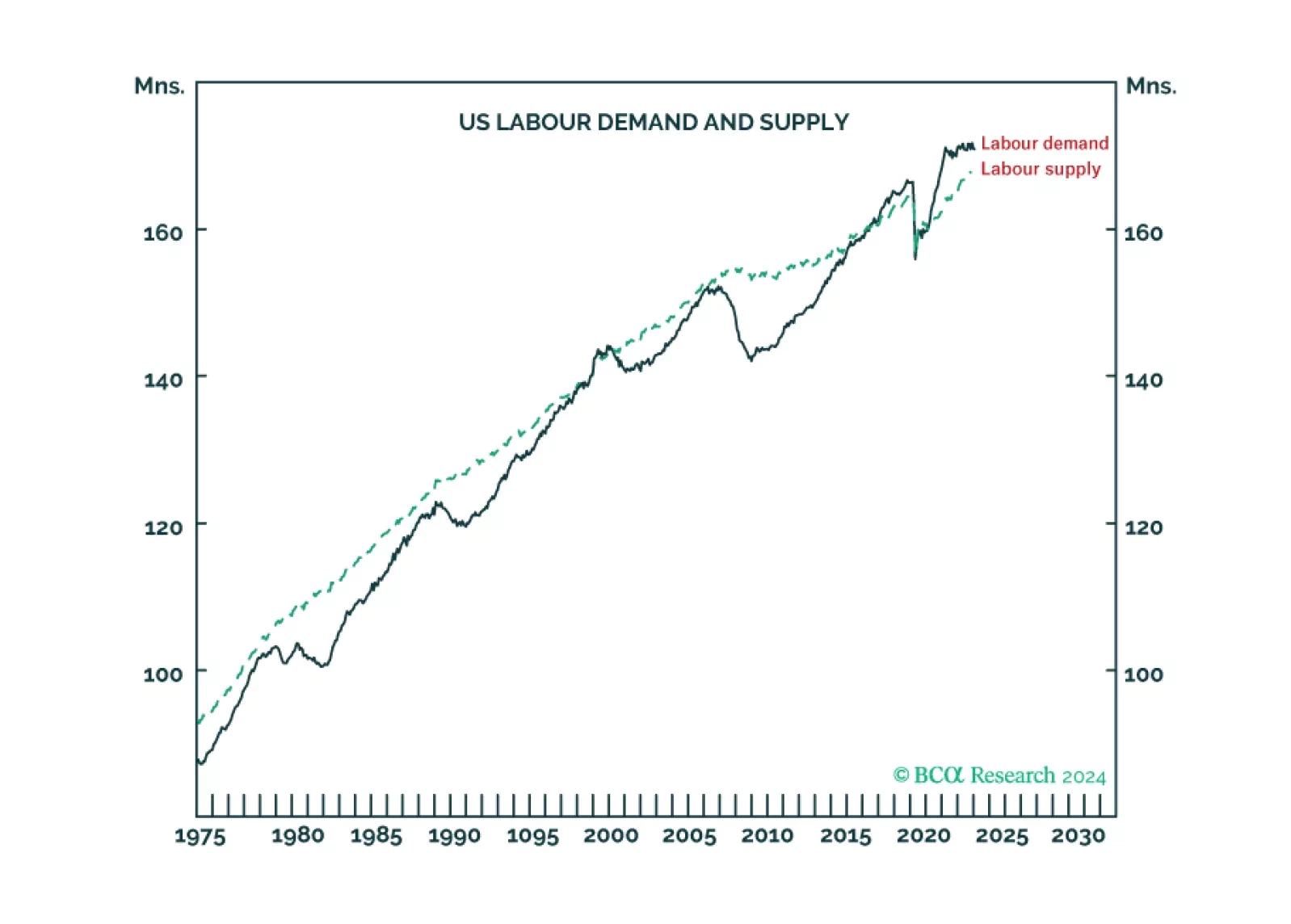

Unlike most advanced economies that are flirting with recession due to weak demand, the ‘inverted’ US economy is motoring along due to strong supply, from a combination of surging labour participation and surging immigration. We go through the implications for stocks, bonds, interest rates, and the dollar. Plus: IXJ, PEP, and MCD are good tactical outperformance candidates.

In the short run, global risk assets are vulnerable due to rising oil prices and bond yields. Cyclically, a global economic downturn will weigh on global risk assets.

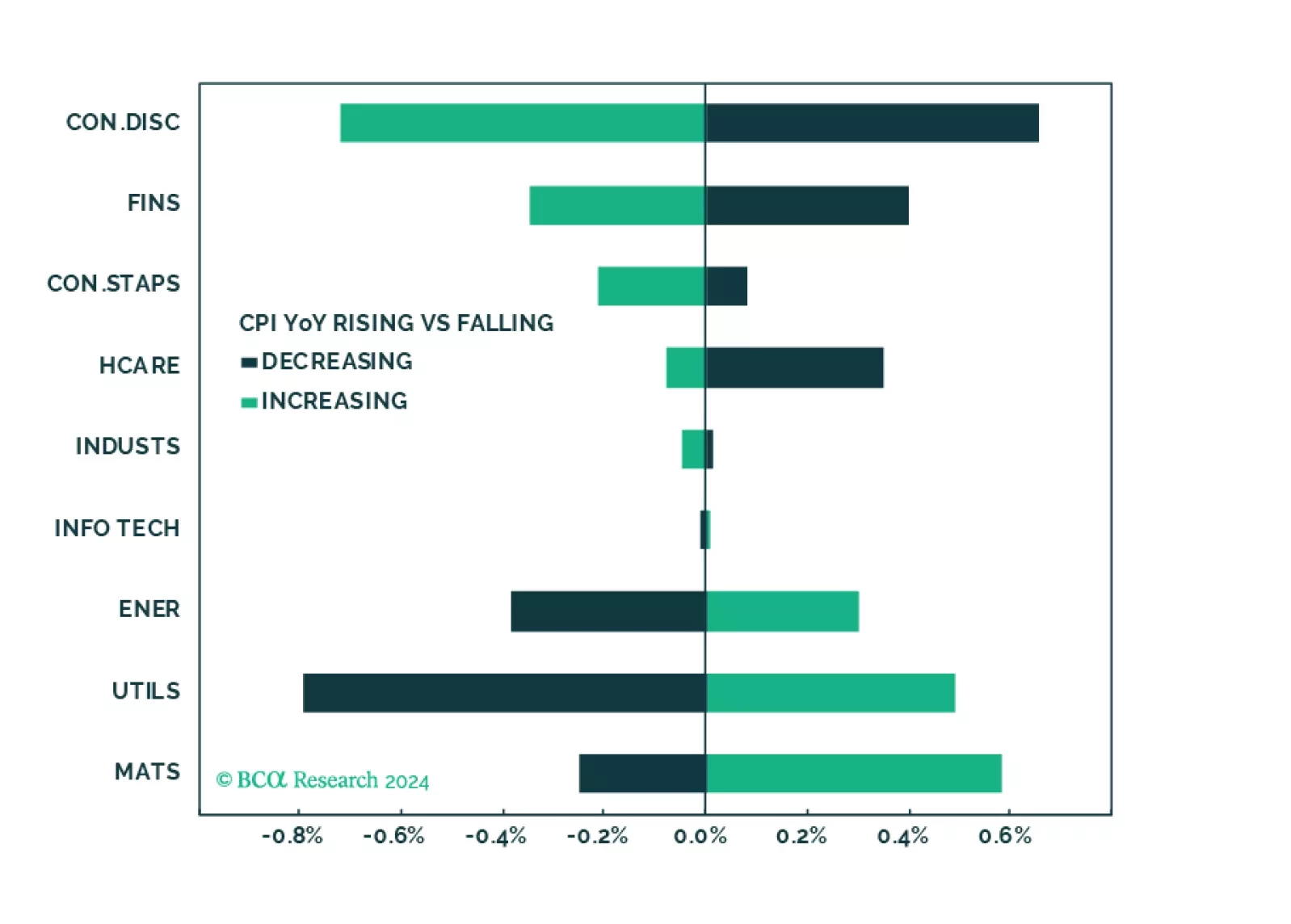

Our reaction to this morning’s CPI report and bond market moves.

Fears of a hard landing are abating as growth has been surprising to the upside. New worries are emerging, such as the trajectory of disinflation, and the pace and timing of rate cuts. In this environment, it is important to build a resilient all-weather portfolio, which protects against a correction, rising rates, or stubborn inflation but also has exposure to the AI theme.

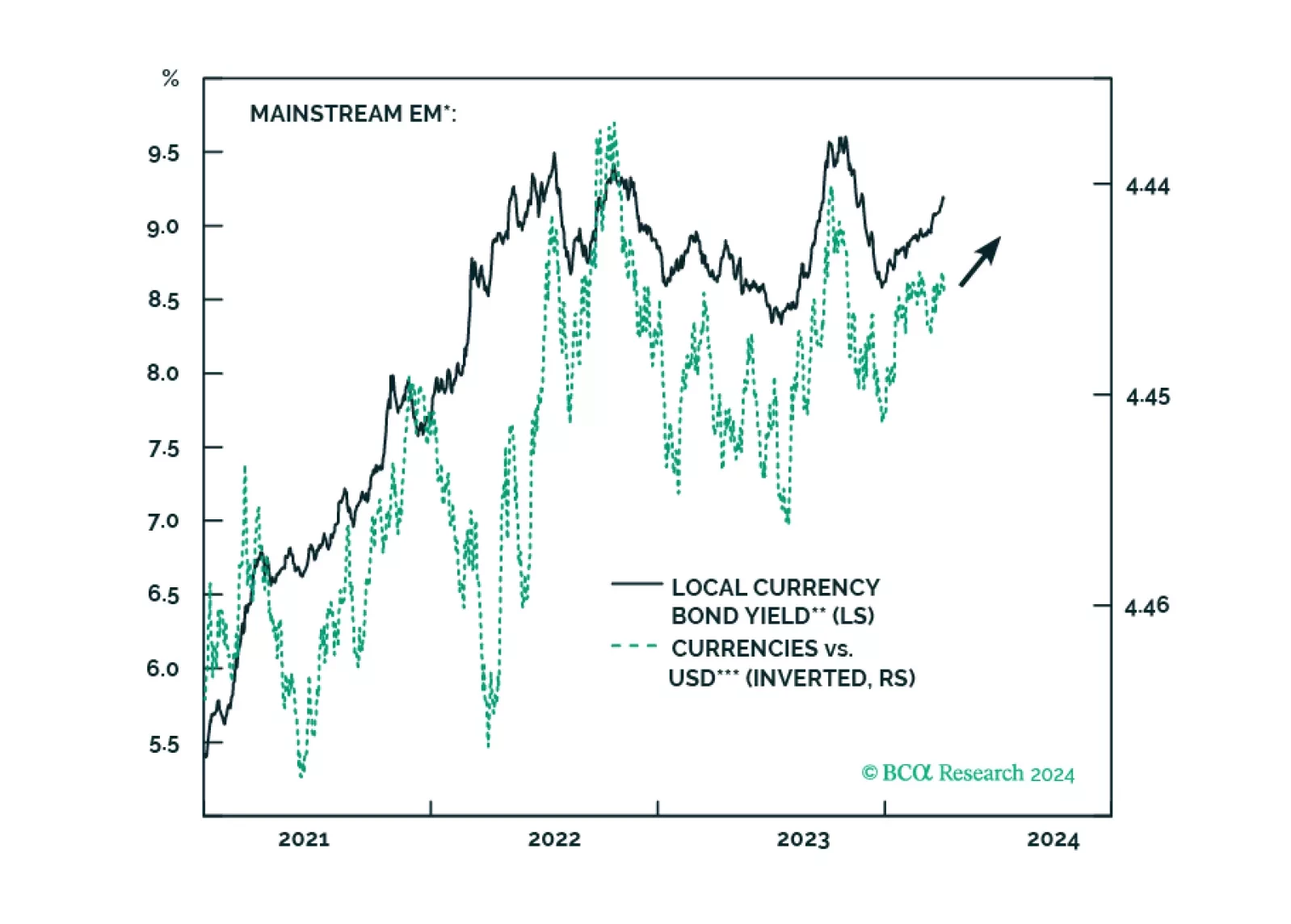

Climbing US bond yields, alongside higher oil prices, might spoil the party for global risk assets. There are budding cracks in EM domestic bonds, and even though we like this asset class in the long run, investors exposed to it should reduce their positions for now.

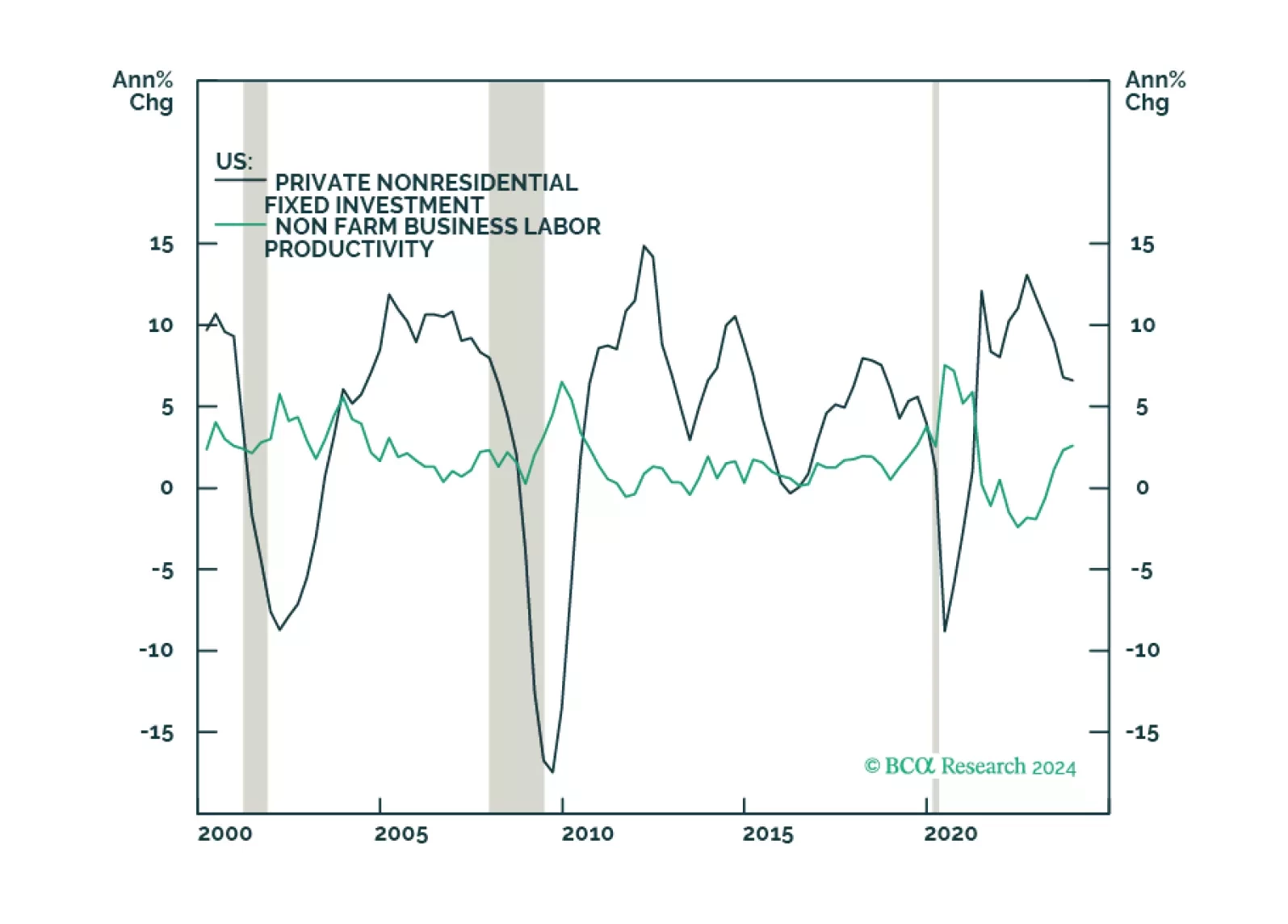

Inflationary pressures this year will remain subdued as labor-productivity growth – driven by strong capex and R+D spending – continues. This will make the Fed more confident in beginning its policy-rate-cutting cycle in June, and will keep gold well bid. We are raising our gold target to $2,300/oz. We continue to expect no recession this year.

For the first time in at least fifty years, US labour supply is running well below labour demand, meaning the US economy is ‘inverted’. We discuss how and why the economy inverted, and what it means for recession, inflation, and asset allocation. Plus: NVDA is at a consolidation point.