Inflation

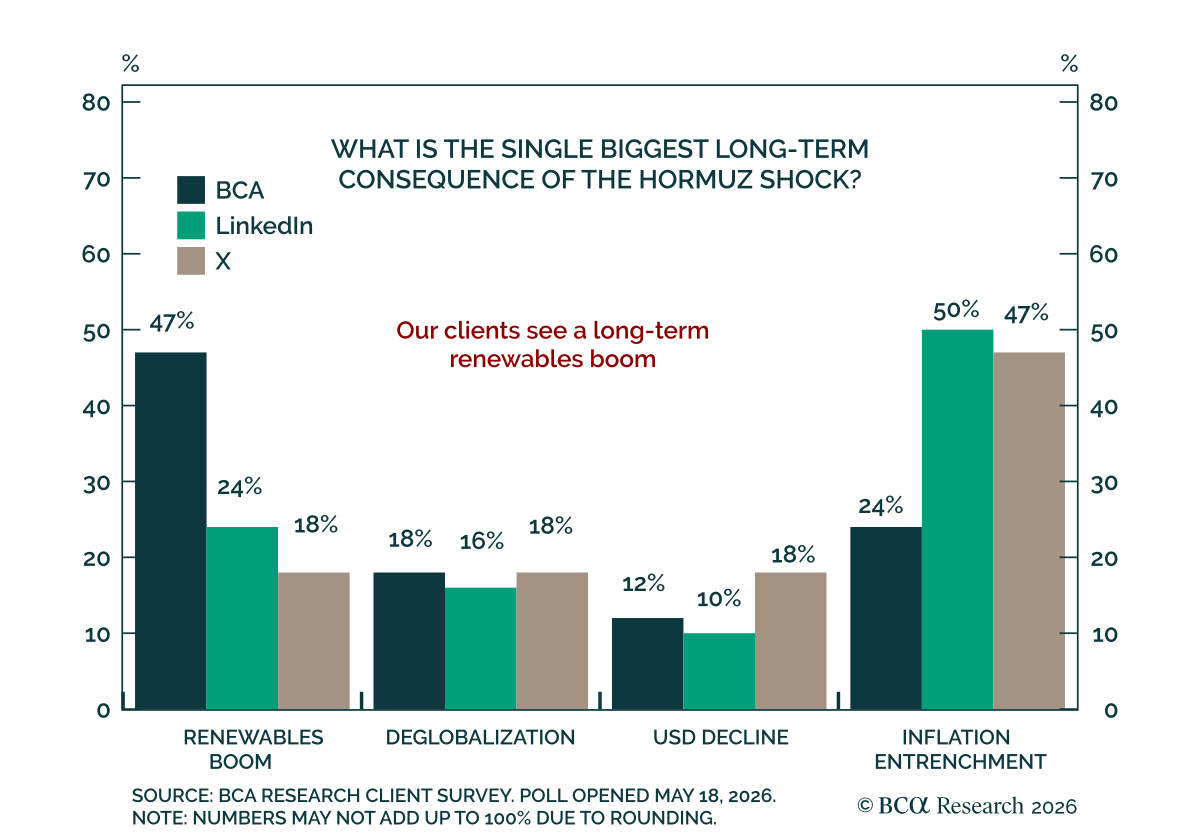

Our clients are split on the Hormuz shock’s long-term consequences. In last week’s poll, we asked what the single biggest long-term consequence would be. BCA clients leaned toward a renewables boom, chosen by 47%, while 24% pointed to inflation entrenchment.…

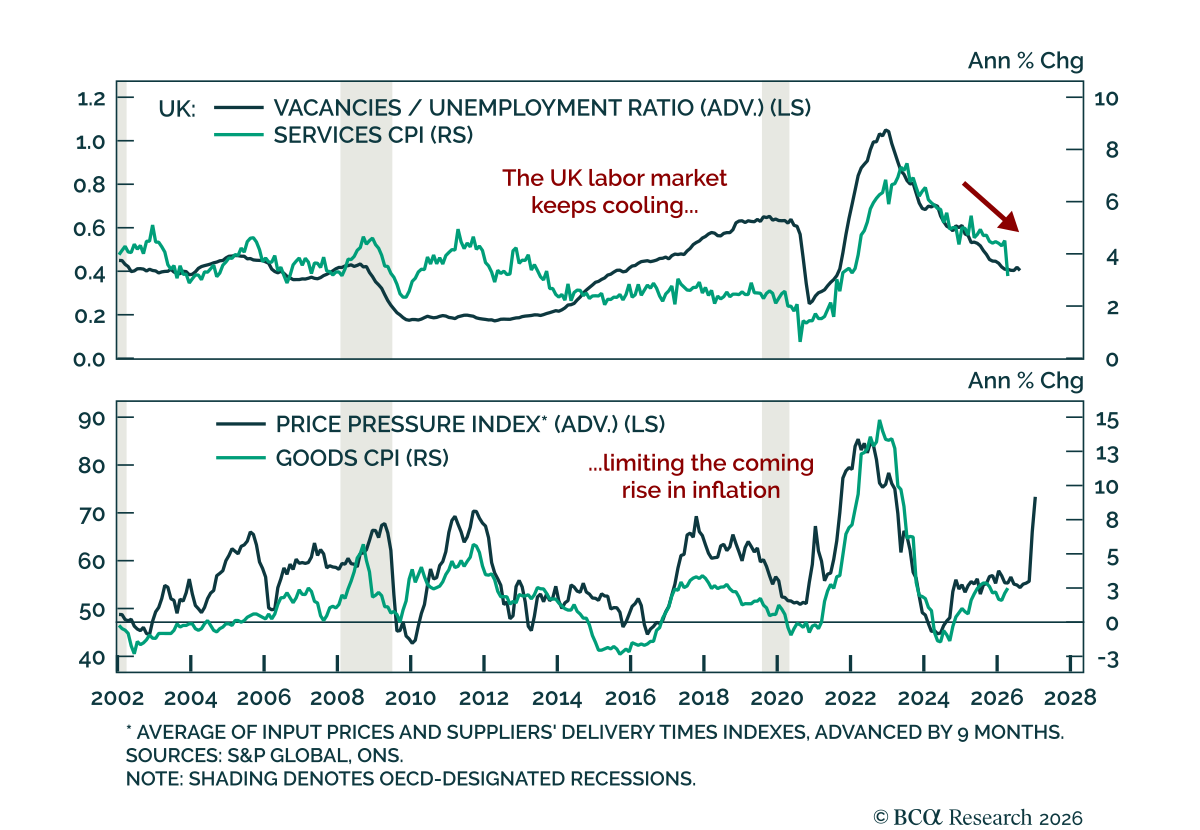

The latest UK employment and inflation data came in cooler than expected, reinforcing the case for weaker growth ahead. Payrolls fell by 100k in April after a 28k decline in March. The unemployment rate also rose 0.1pp to 5.0%. Average weekly earnings ticked…

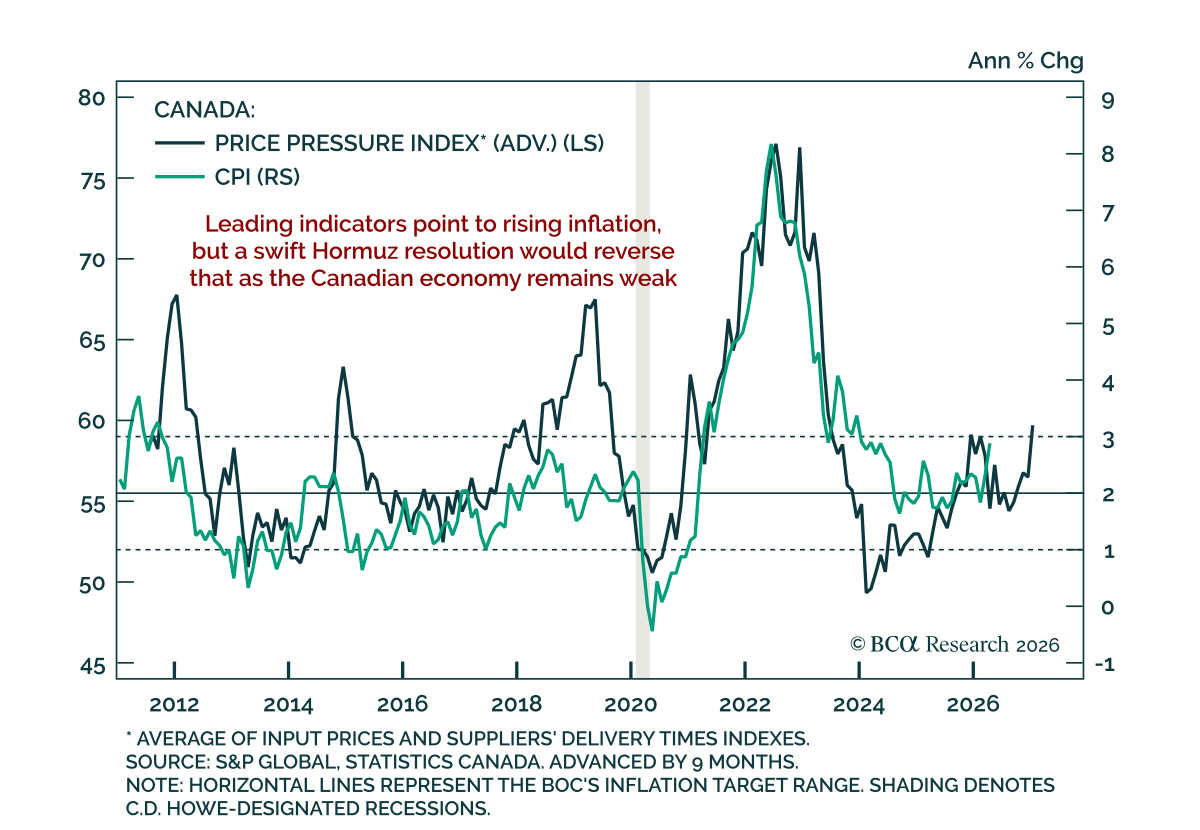

Canadian April inflation came in cooler than estimates, giving the Bank of Canada some reassurance even as headline CPI accelerated. Headline inflation rose to 2.8% y/y from 2.4%, but came in below the 3.1% consensus. Both of the Bank of Canada’s preferred…

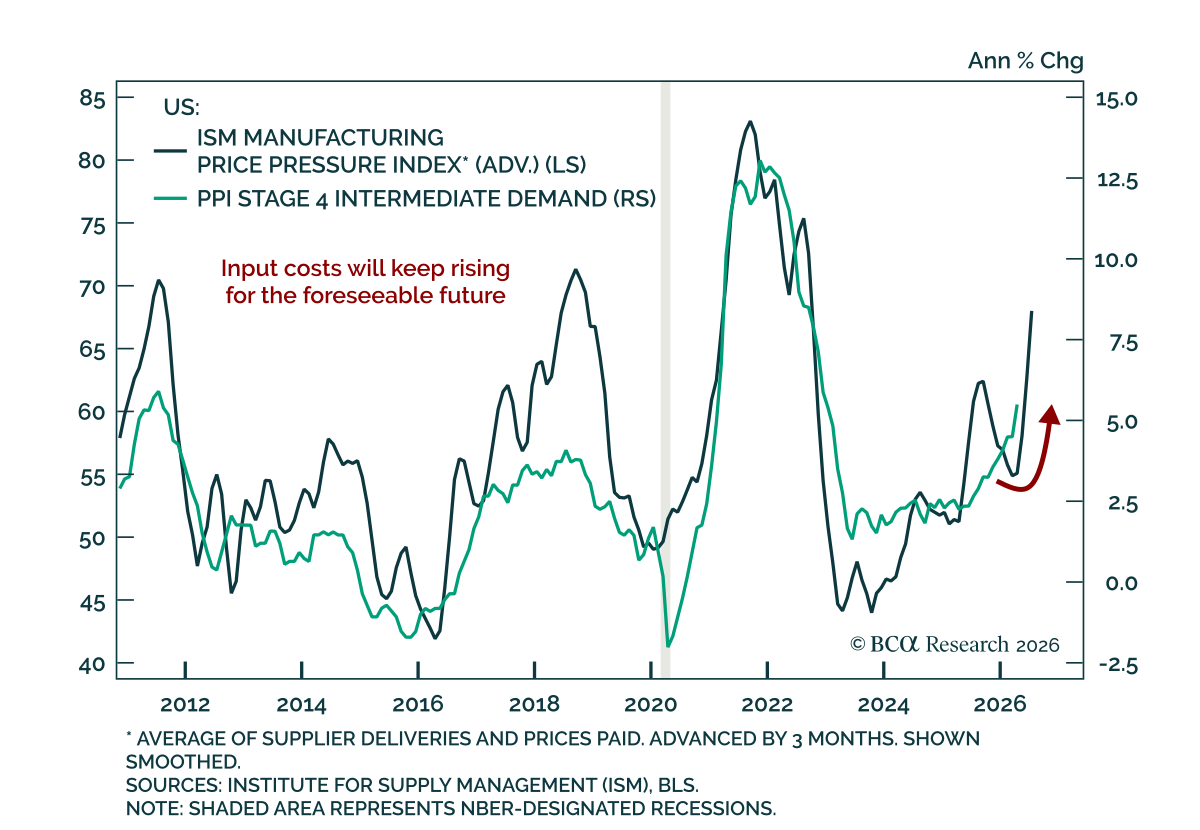

April PPI was hotter than expected, reinforcing the inflation message from CPI rather than changing it. Headline PPI for final demand rose 1.4% m/m, up from an upwardly revised 0.7% in March. The core measure, which excludes food, energy, and trade, rose 0.6%…

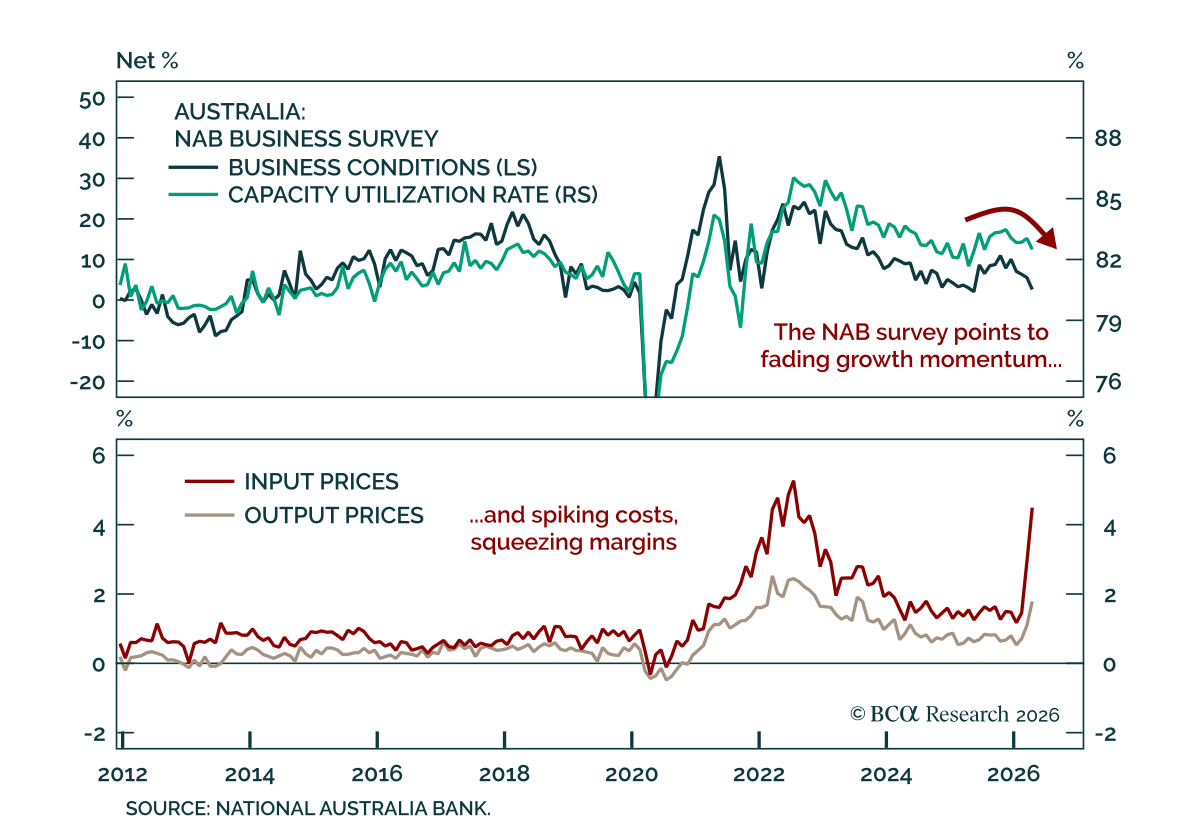

The April NAB survey points to a worsening growth-inflation mix in Australia. Business conditions moderated to +3 from +6, a fourth consecutive decline that left the index firmly below its long-term average. Business confidence, the more forward-looking…

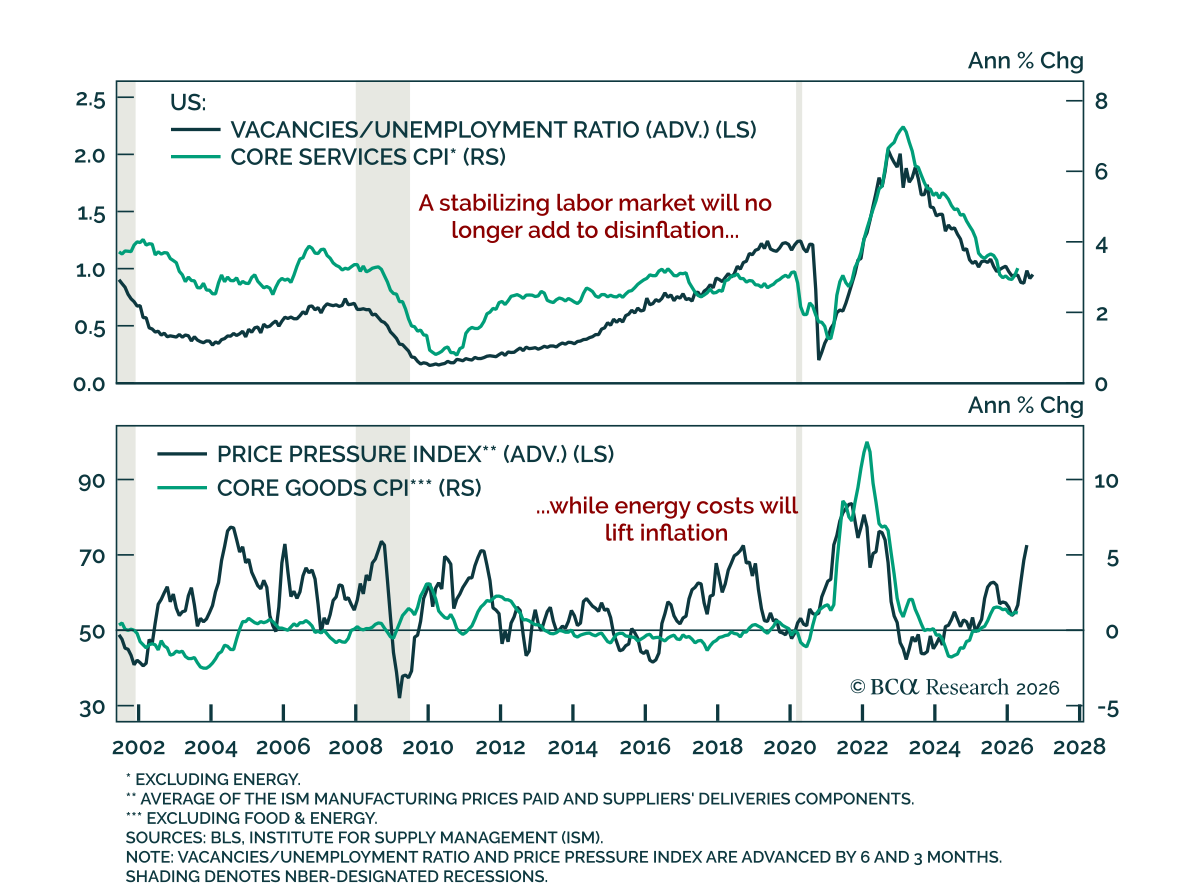

US April CPI was hotter than expected, keeping the Fed on hold as inflation risks remain tilted higher. Headline CPI rose 0.6% m/m and core 0.4%. While headline monthly inflation was below the prior month’s 0.9%, it remains too high to be consistent with the…

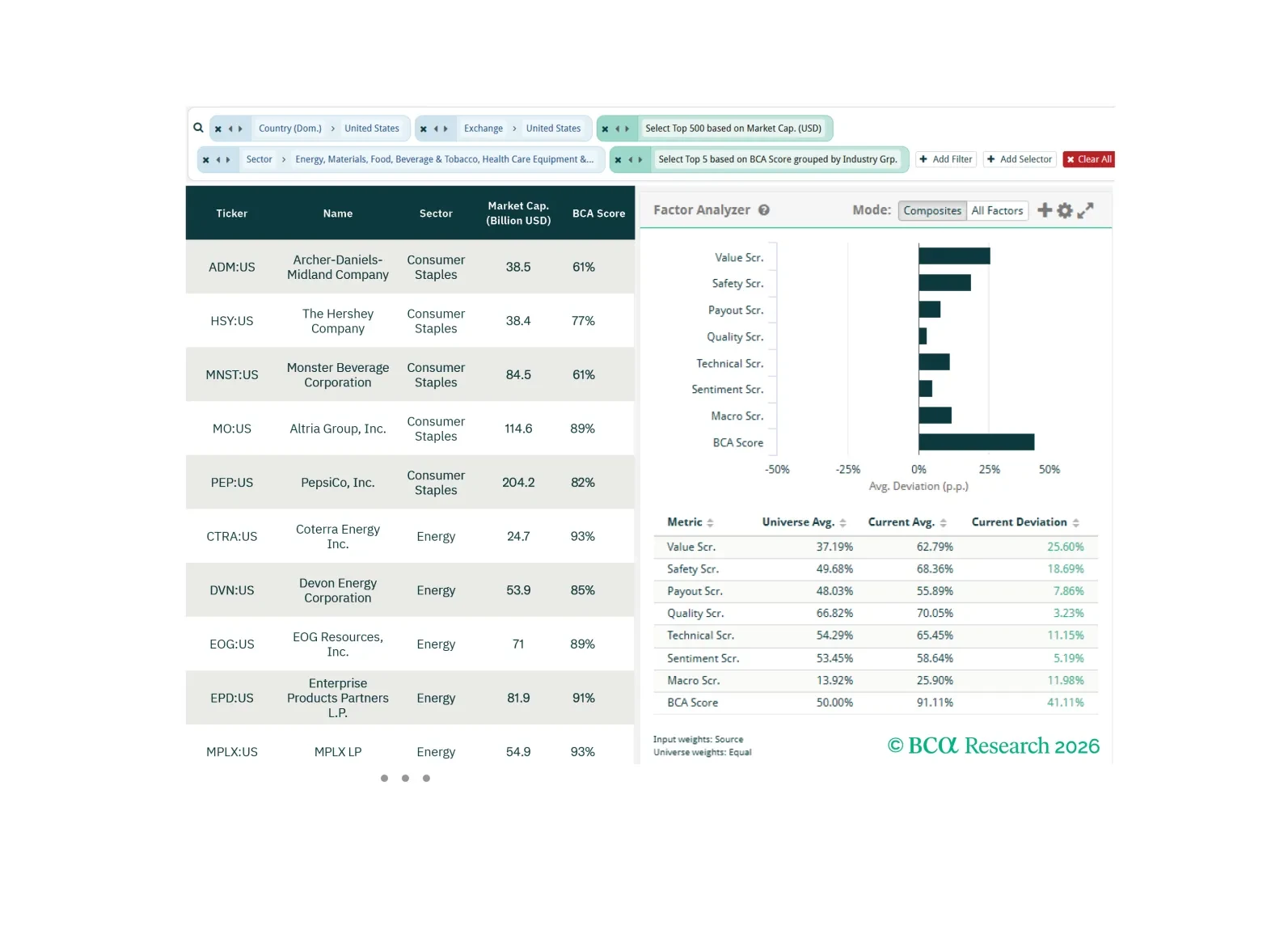

In this screener report, we explore opportunities in Inflation risk, supply-constrained Information Technology stocks, and old-economy cyclicals.

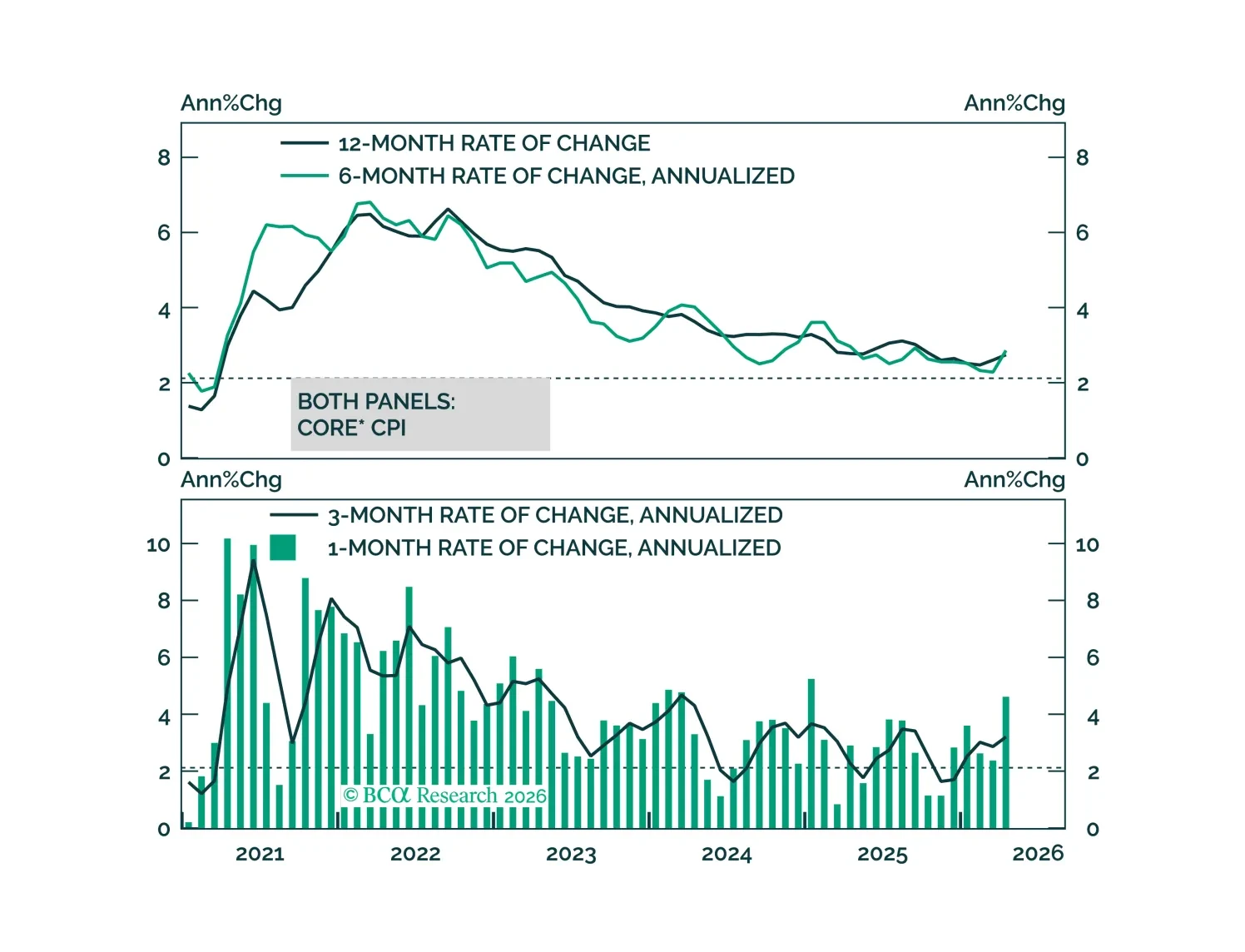

The April CPI report showed clear evidence of the direct effect of higher oil prices on inflation but, so far, limited evidence of passthrough to core.

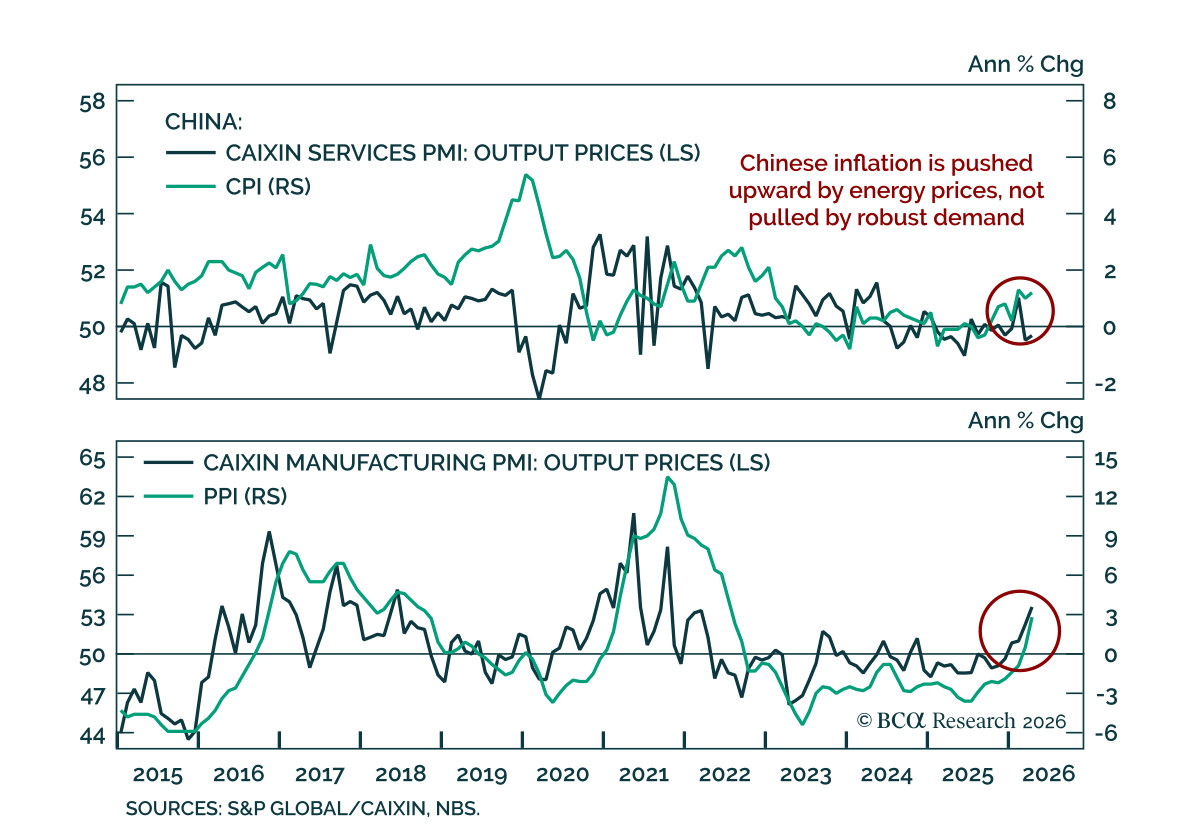

Chinese inflation surprised to the upside, but the rise reflects higher energy prices rather than stronger demand. CPI rose 1.2% y/y versus 0.9% expected, while PPI was the bigger surprise at 2.8% y/y, almost double consensus. The PPI move matters more…

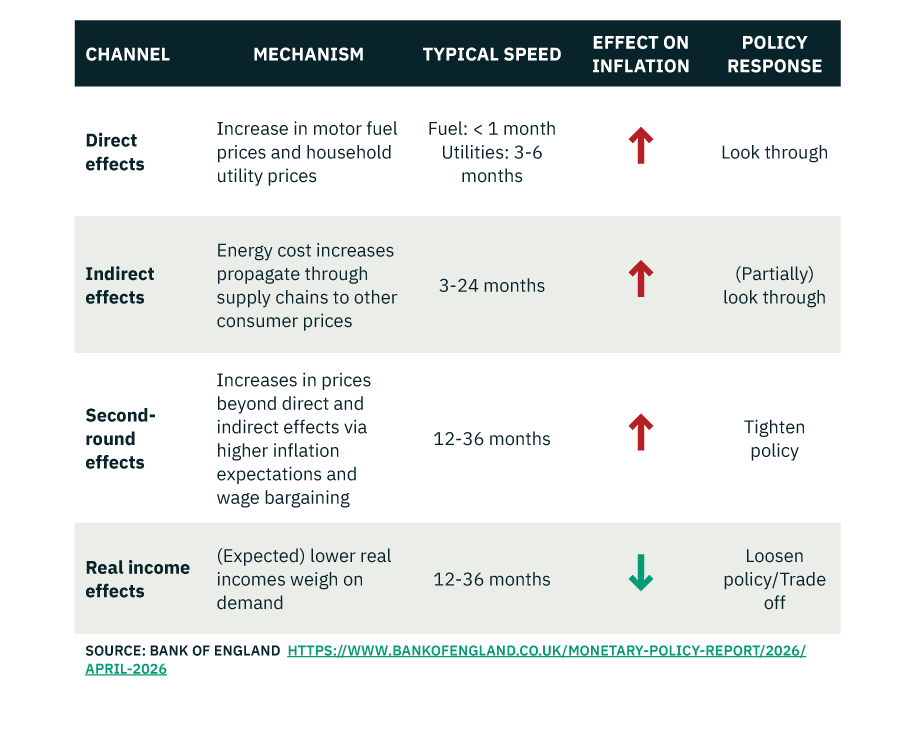

The Bank of England’s latest Monetary Policy Report offers a clean framework for thinking through an oil shock and the appropriate policy response. The first channel is the direct effect of higher energy prices on inflation such as higher gas and utilities…