Inflation

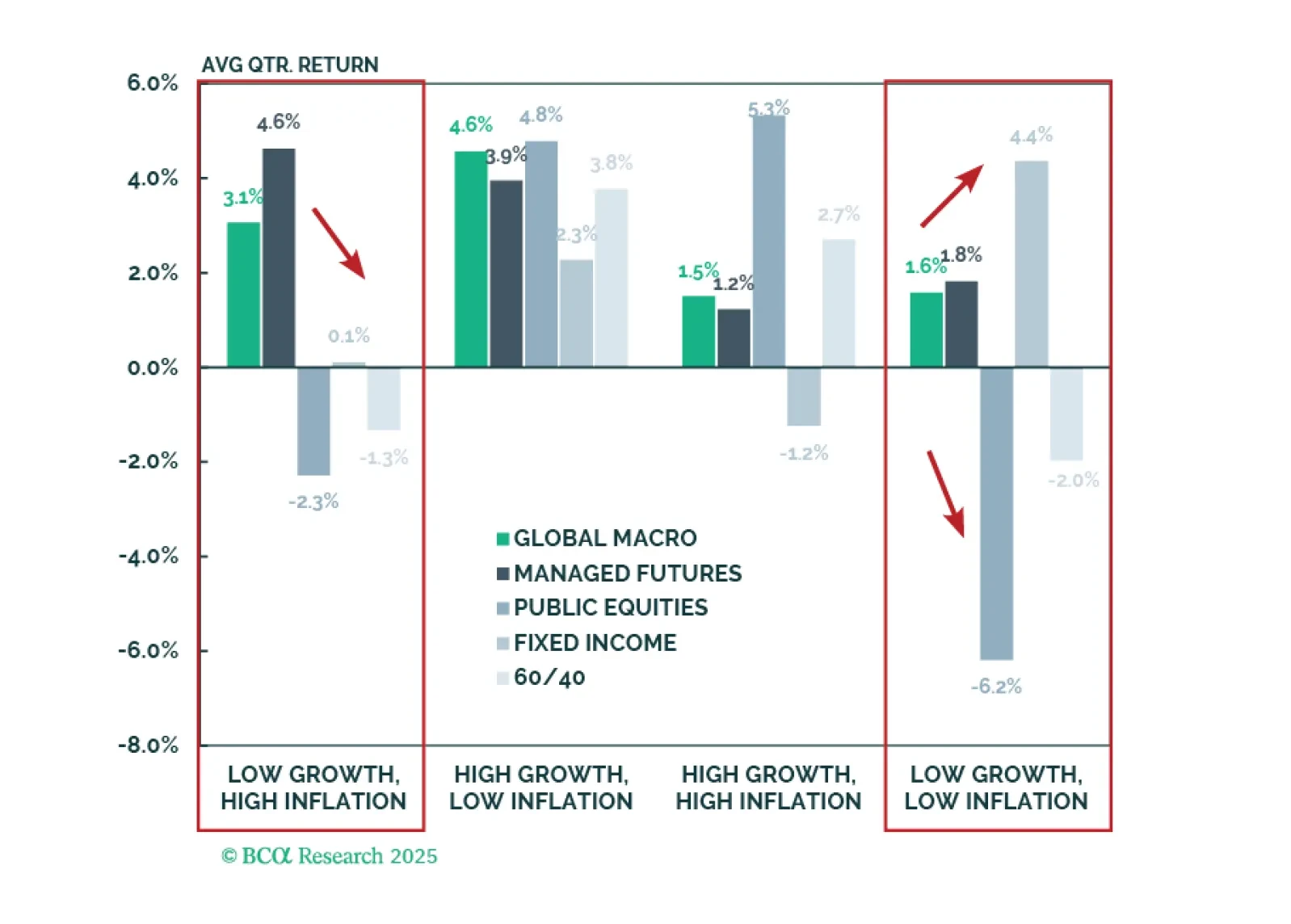

Understanding asset performance across Growth and Inflation regimes helps investors construct and manage balanced portfolios. Our first G&I Catalog report examines Hedge Fund strategies. Global Macro and Managed Futures offer the strongest protection in Stagflation-like periods, when traditional assets typically struggle. Since 1998, these regimes have occurred less than 10% of the time—but that may not hold true going forward.

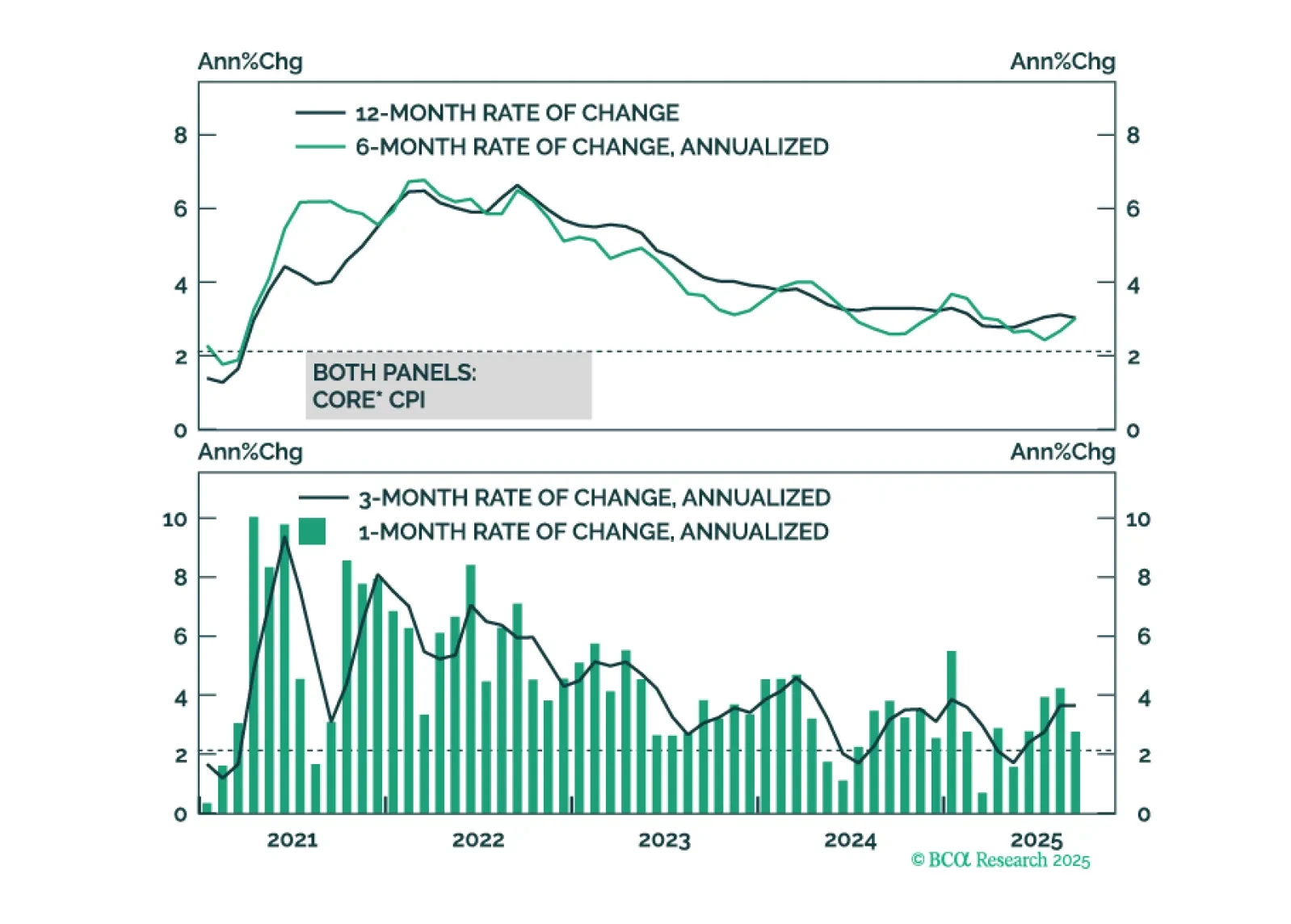

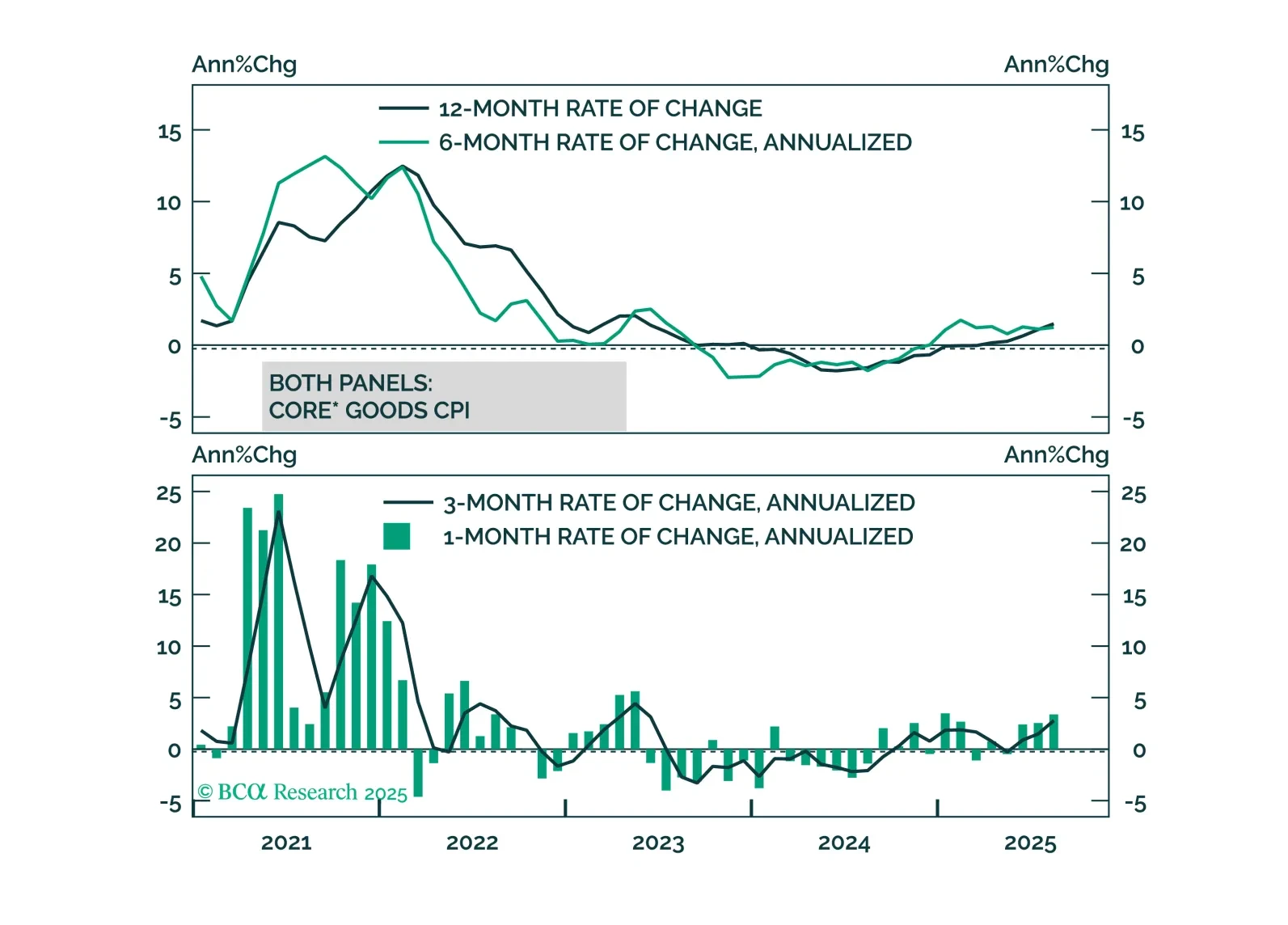

US inflation data continue to show no signs of price pressures beyond a near-term tariff effect.

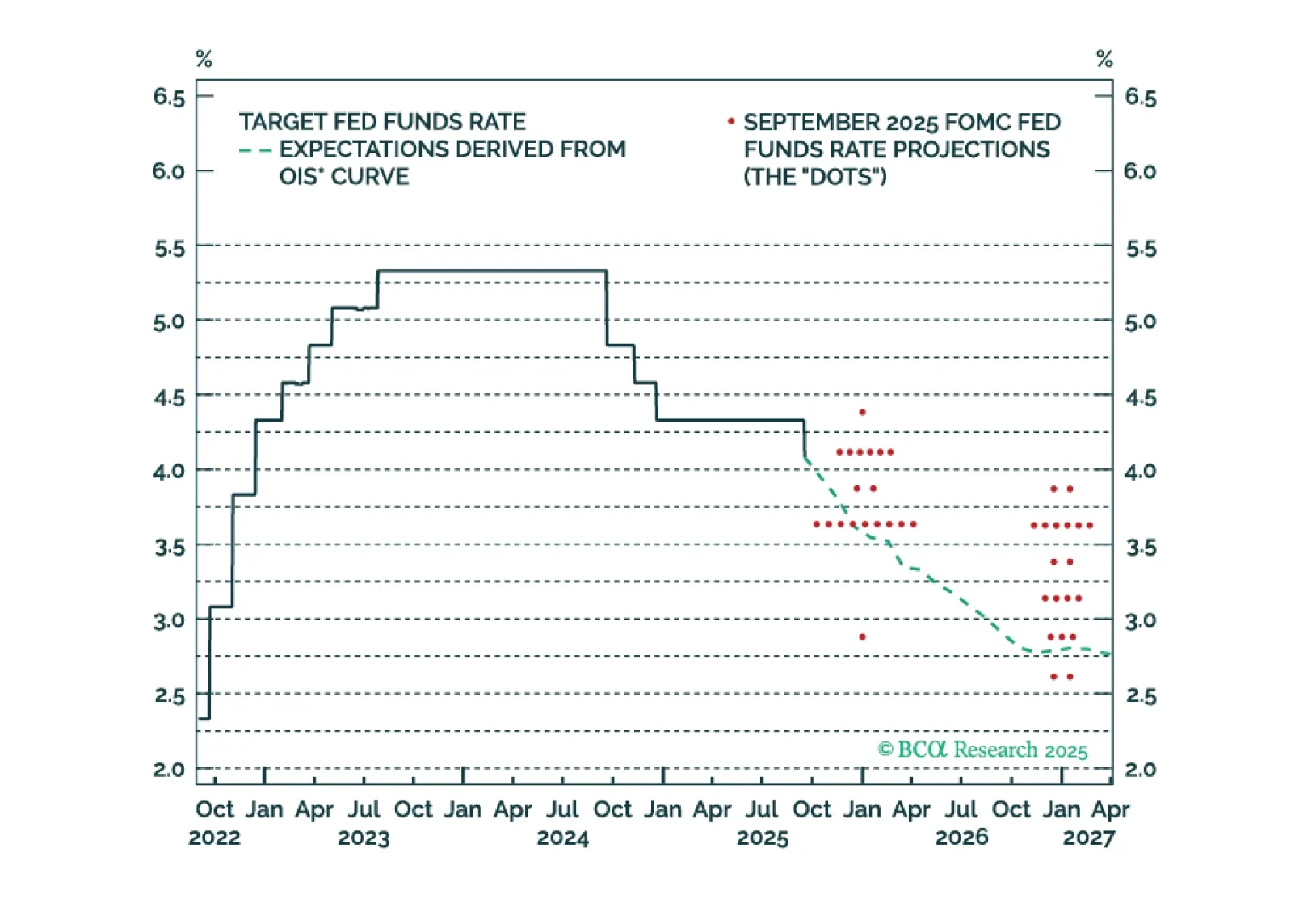

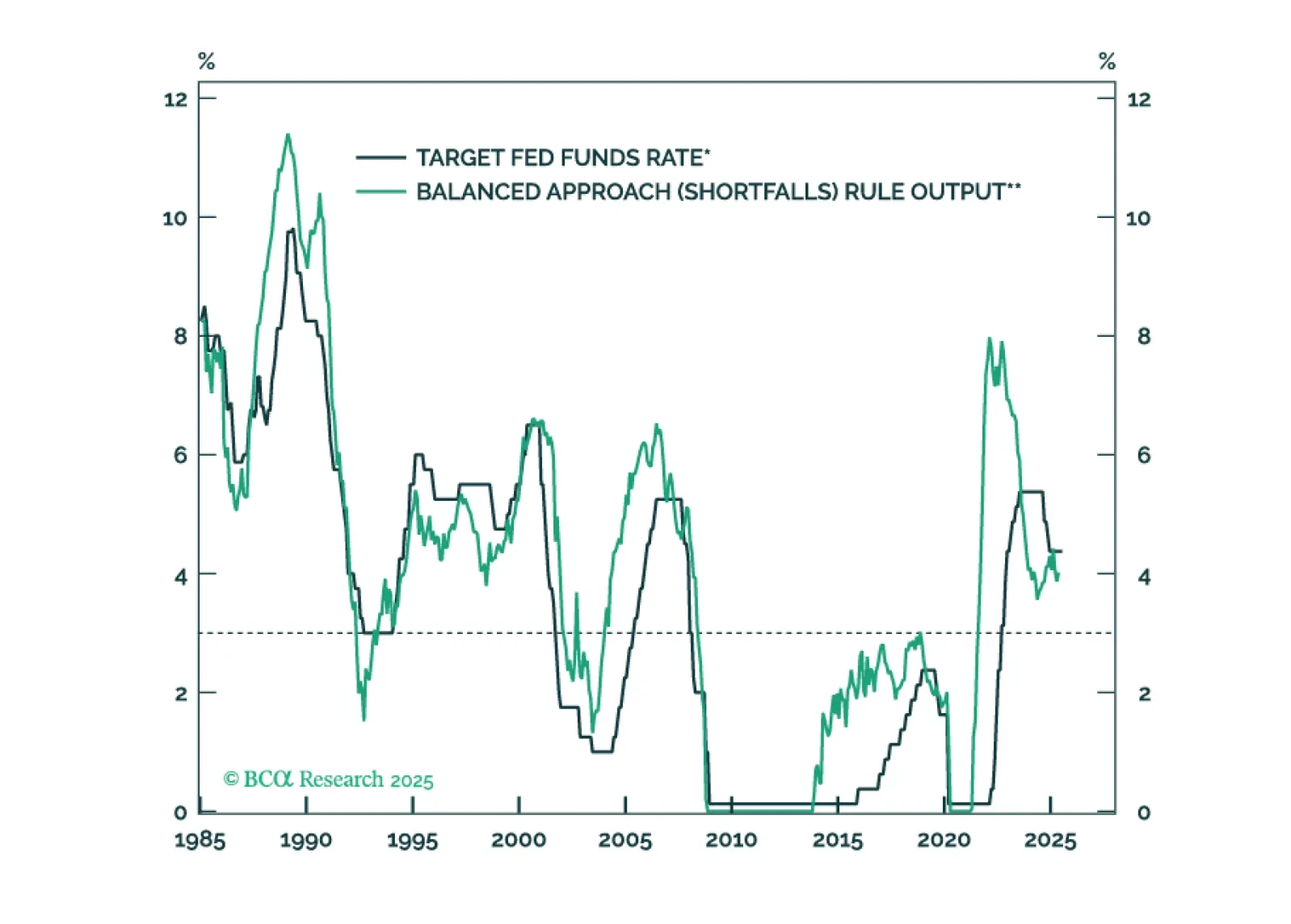

The Fed’s actions tell us that it has chosen to avoid a recession at the cost of moving its inflation goalposts to 3 percent. Thus begins the slippery slope to price instability. Long-term investors should underweight the dollar, own some gold, but better than gold is bitcoin. Plus, a new tactical trade is short GOOGL vs. SPY.

Median Fed unemployment rate projections are overly optimistic. The Fed will end up cutting more in 2026 than it currently anticipates.

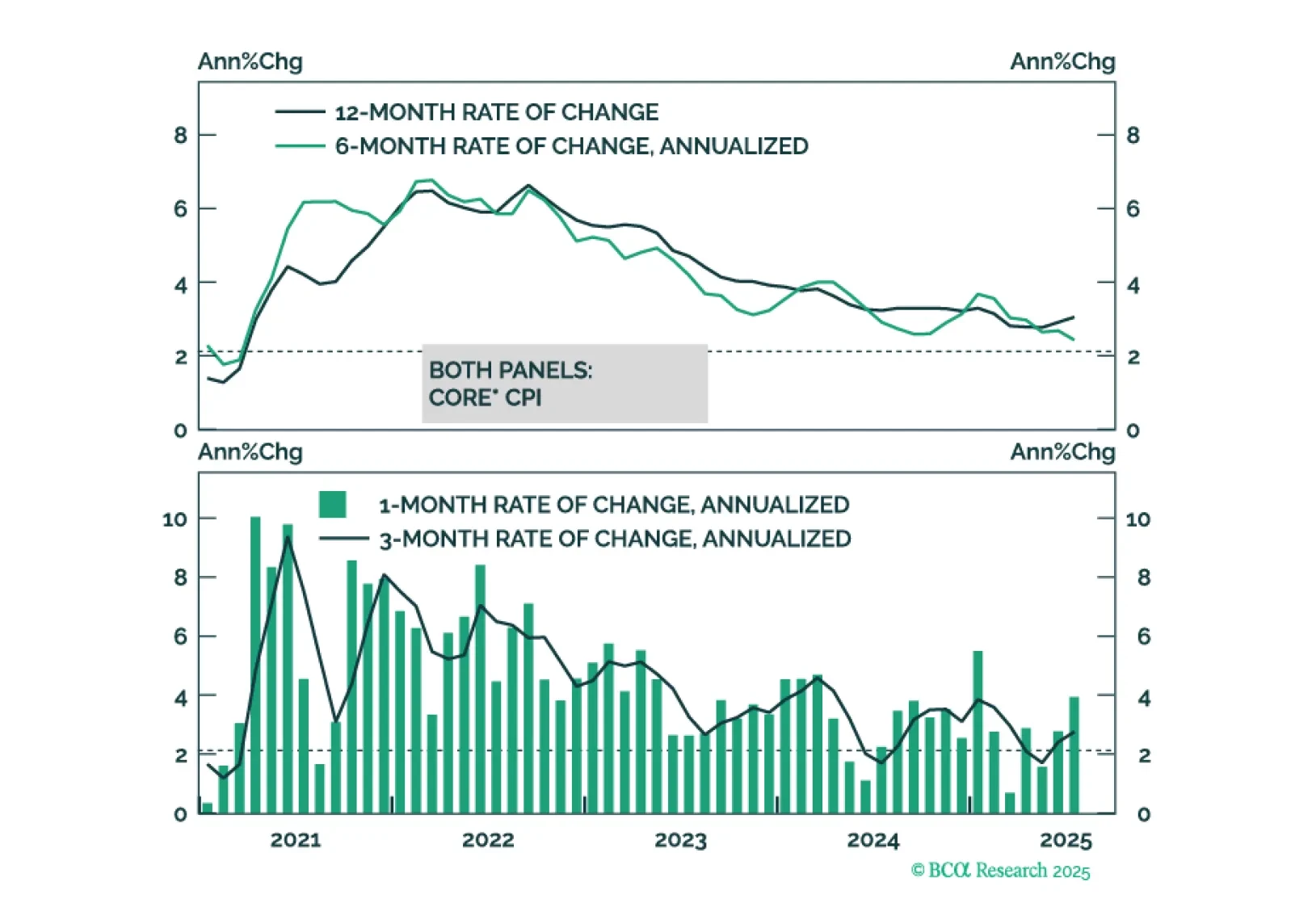

High US inflation is being driven by tariffs, not domestic inflationary pressure. This argues for Fed easing and a bull-steepening of the Treasury curve.

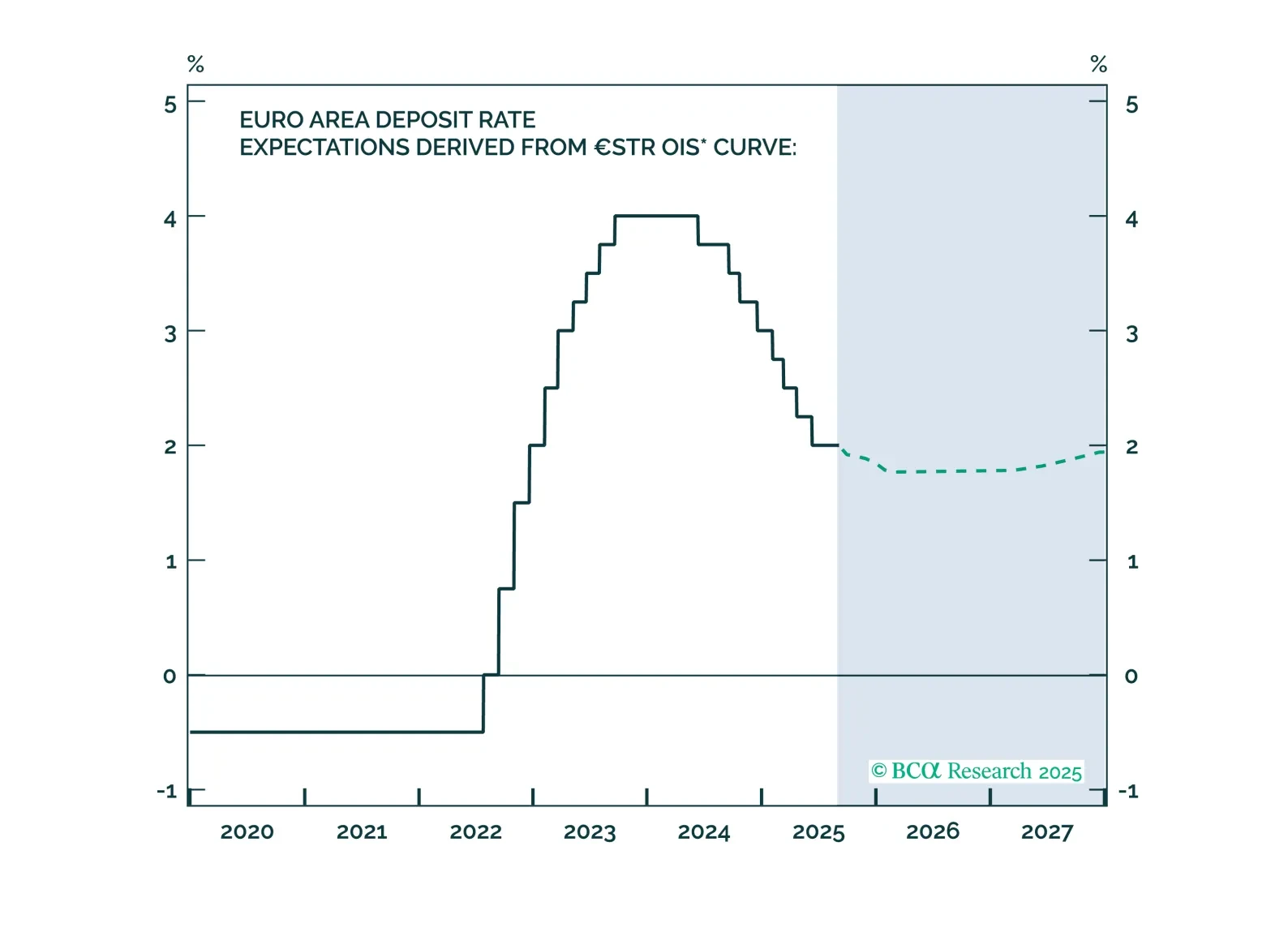

The European Central Bank has achieved a soft landing. Inflation is back to target, with well-anchored inflation expectations. The unemployment rate is historically low, and real economic growth is stable, albeit weak. Given that little to no additional easing will come from the ECB, investors should underweight government bonds relative to equities.

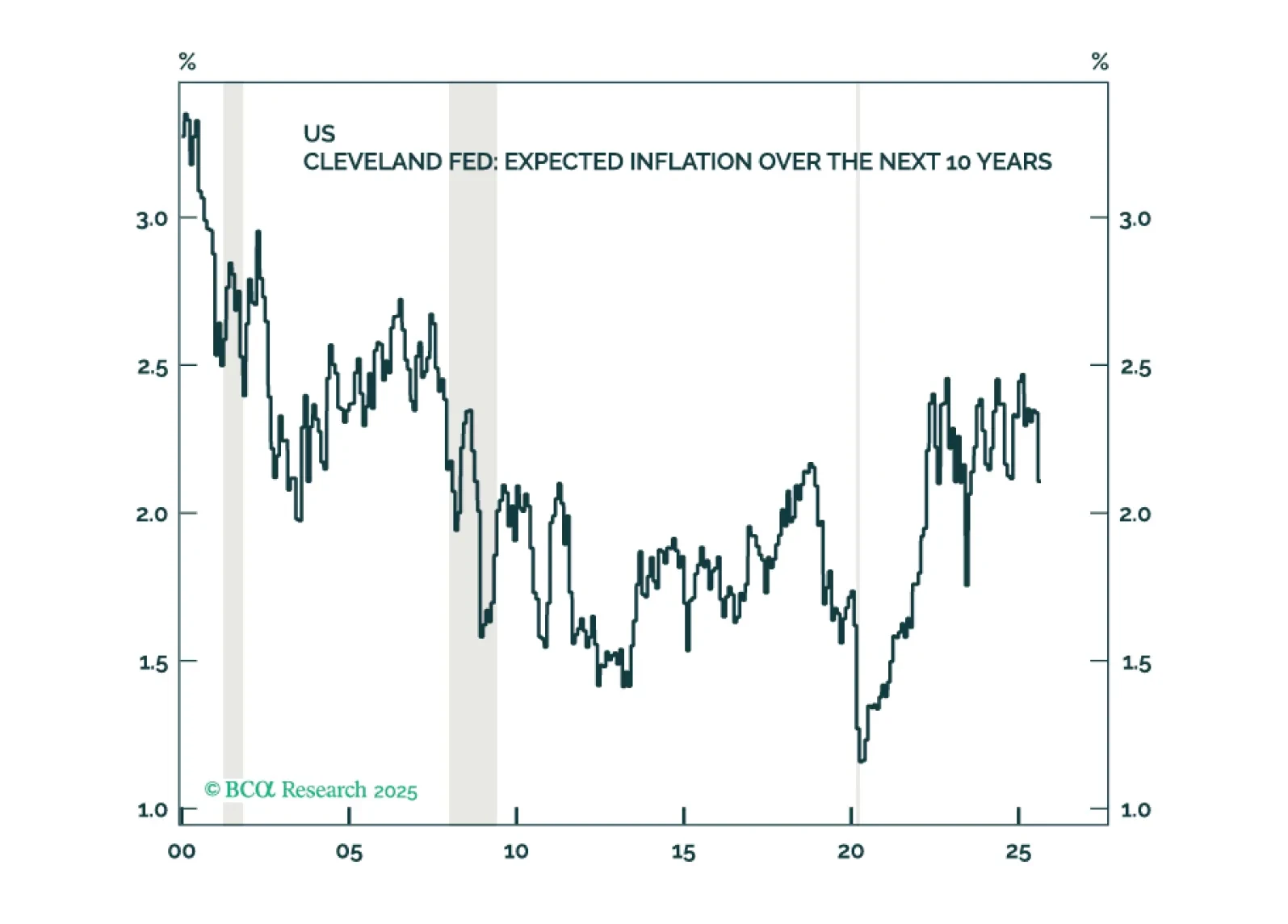

Inflation expectations in the US remain reasonably well anchored and there are few signs of a brewing wage-price spiral. Thus, the near-term risks to growth outweigh the risks of higher inflation. Looking beyond the next year or two, however, we are worried about stagflation.

We see two risks that could spoil the rally in US risk assets: (1) a tariff-driven stagflation, and (2) a US Treasury tantrum. Our negative view on EM risk assets is primarily driven by the outlook for global trade, which is set to shrink in Q4 this year.

This morning’s CPI report marginally tips the scales in favor of a September rate cut.

The Fed will keep rates on hold until the unemployment rate forces its hand.