Inflation Protected

Our Portfolio Allocation Summary for April 2025.

Our Portfolio Allocation Summary for March 2025.

Our Portfolio Allocation Summary for January 2025.

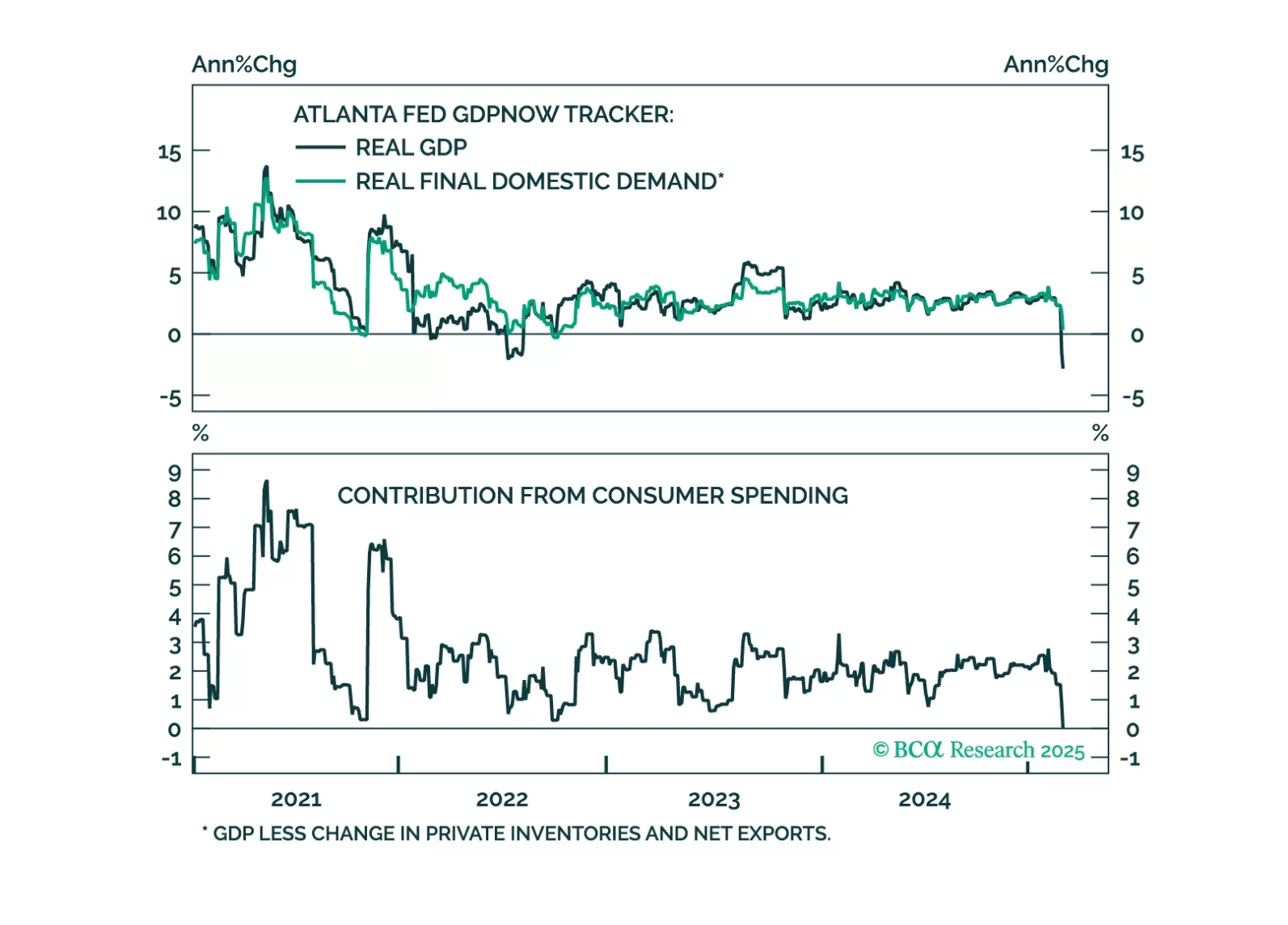

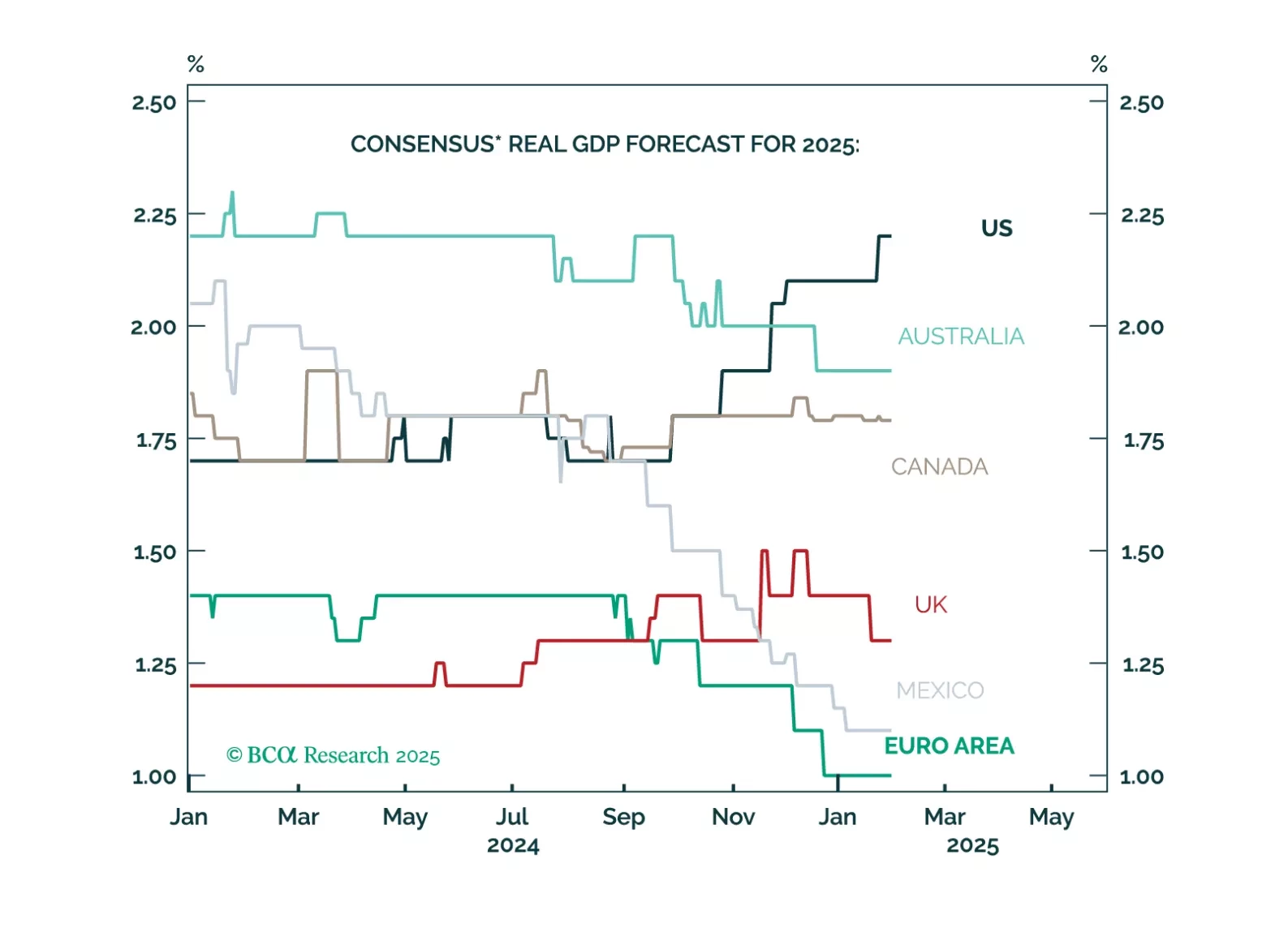

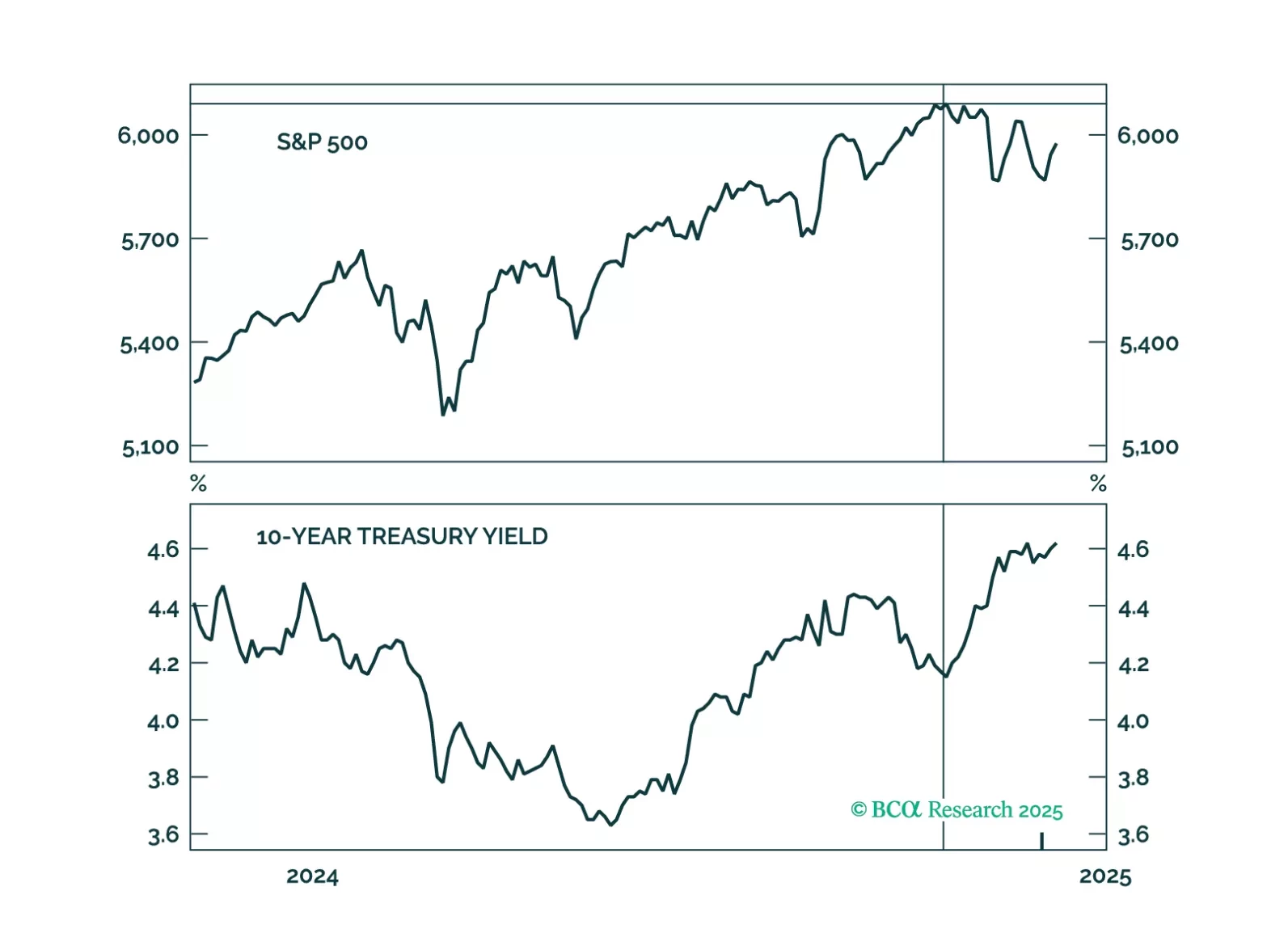

Markets and forecasters anticipate a “Golden Age” for Trump’s America, with US growth expectations soaring while the rest of the world lags. However, this extreme optimism means that there is a lot of room for disappointment. Cooling income growth, weak housing and less deficit spending than expected will result in US growth underperforming expectations. Maintain a modest underweight to equities and modest overweight to fixed income. US markets have become more expensive relative to the rest of the world even as quality differentials have stabilized. Prepare to downgrade US equities to underweight and to upgrade Euro Area and China to overweight. We will wait to pull the trigger until we have more clarity on trade policy and when the dollar's momentum turns negative.

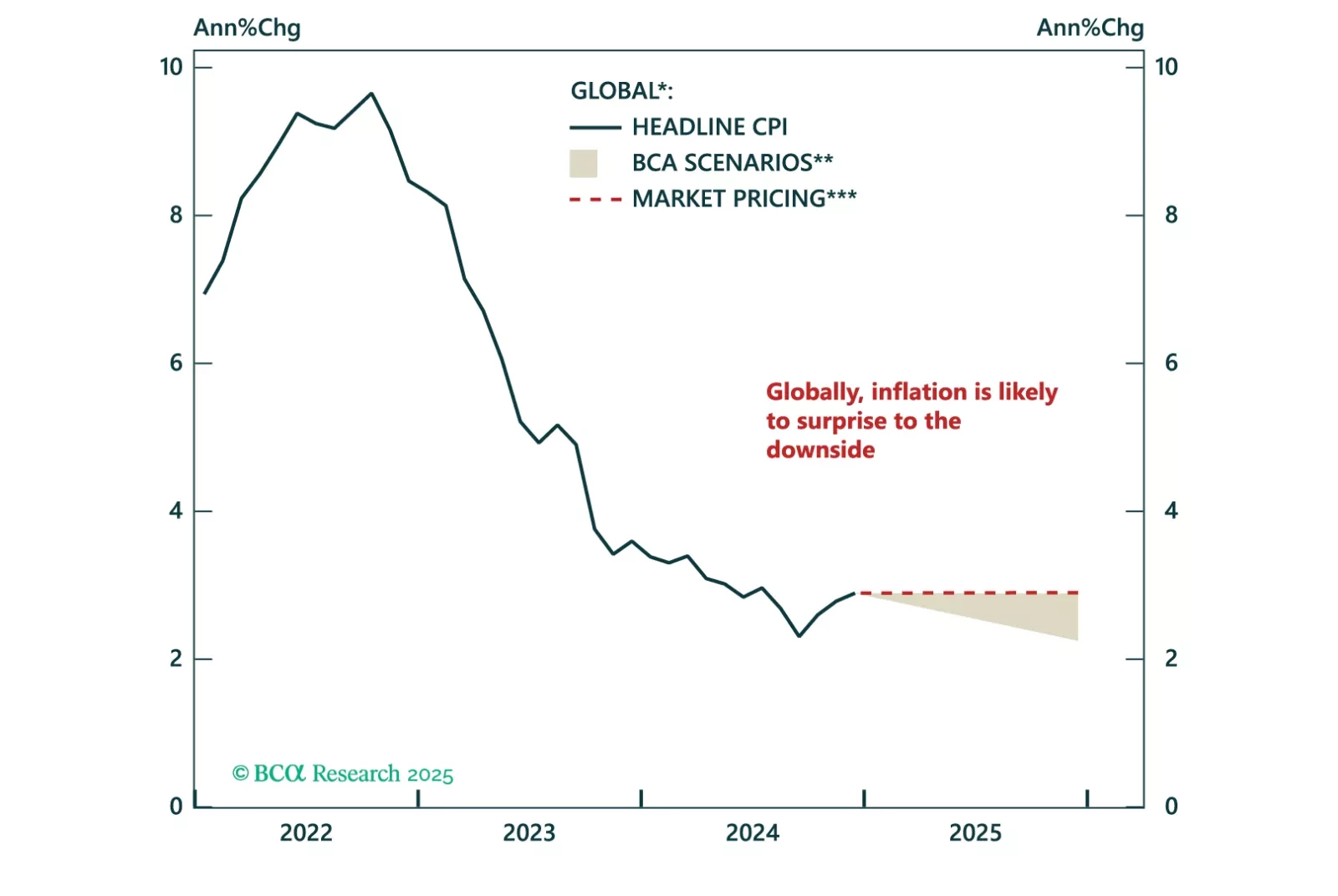

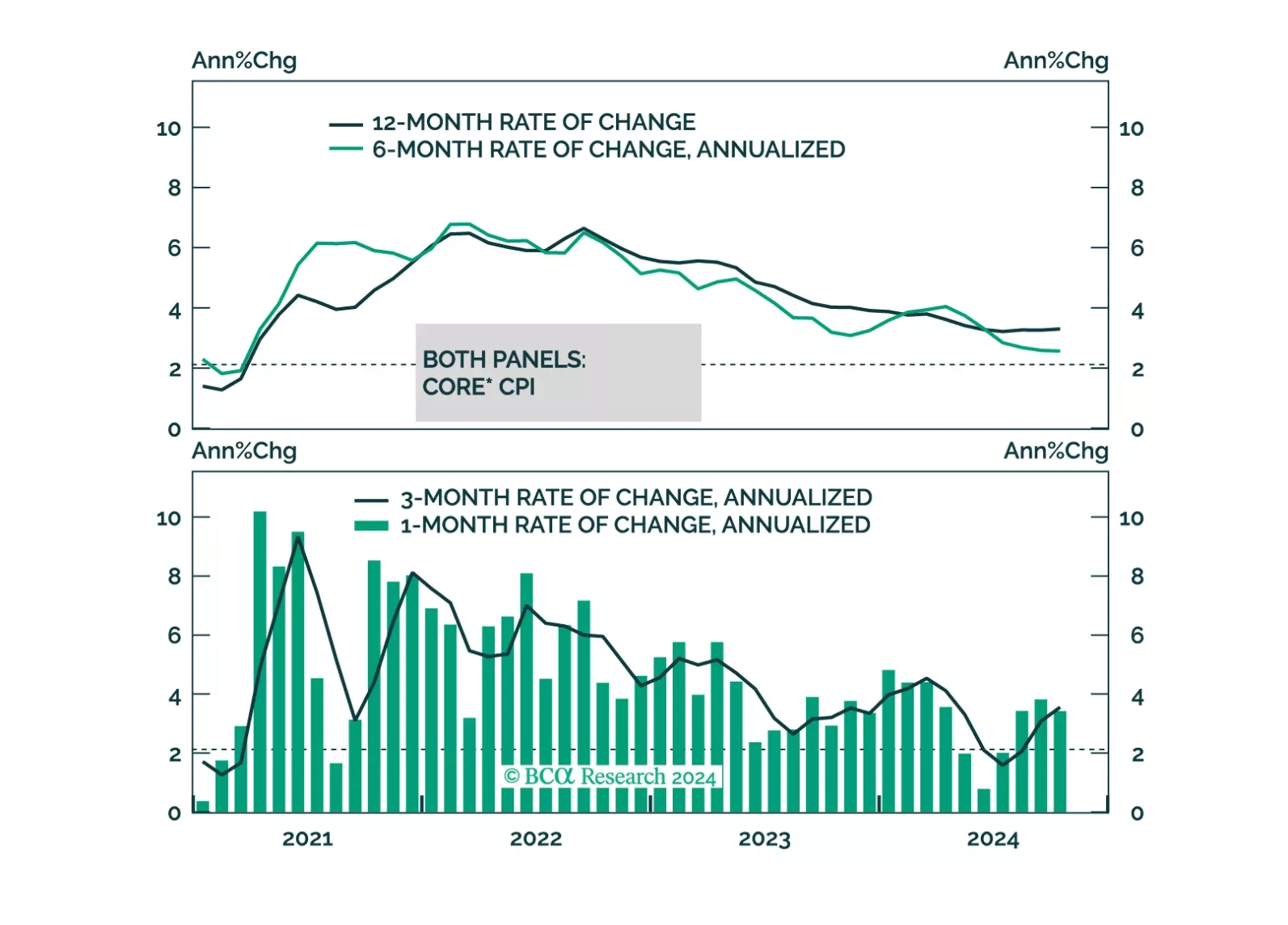

Inflation concerns are starting to ramp up again due to potentially inflationary policies from the new Trump administration. These concerns mostly affect the US inflation outlook. Evidence from forward-looking indicators shows that the global disinflationary trend remains intact. Today’s Special Report covers the global inflation outlook in 2025 and the implications for inflation-linked bonds.

Our Portfolio Allocation Summary for January 2025.

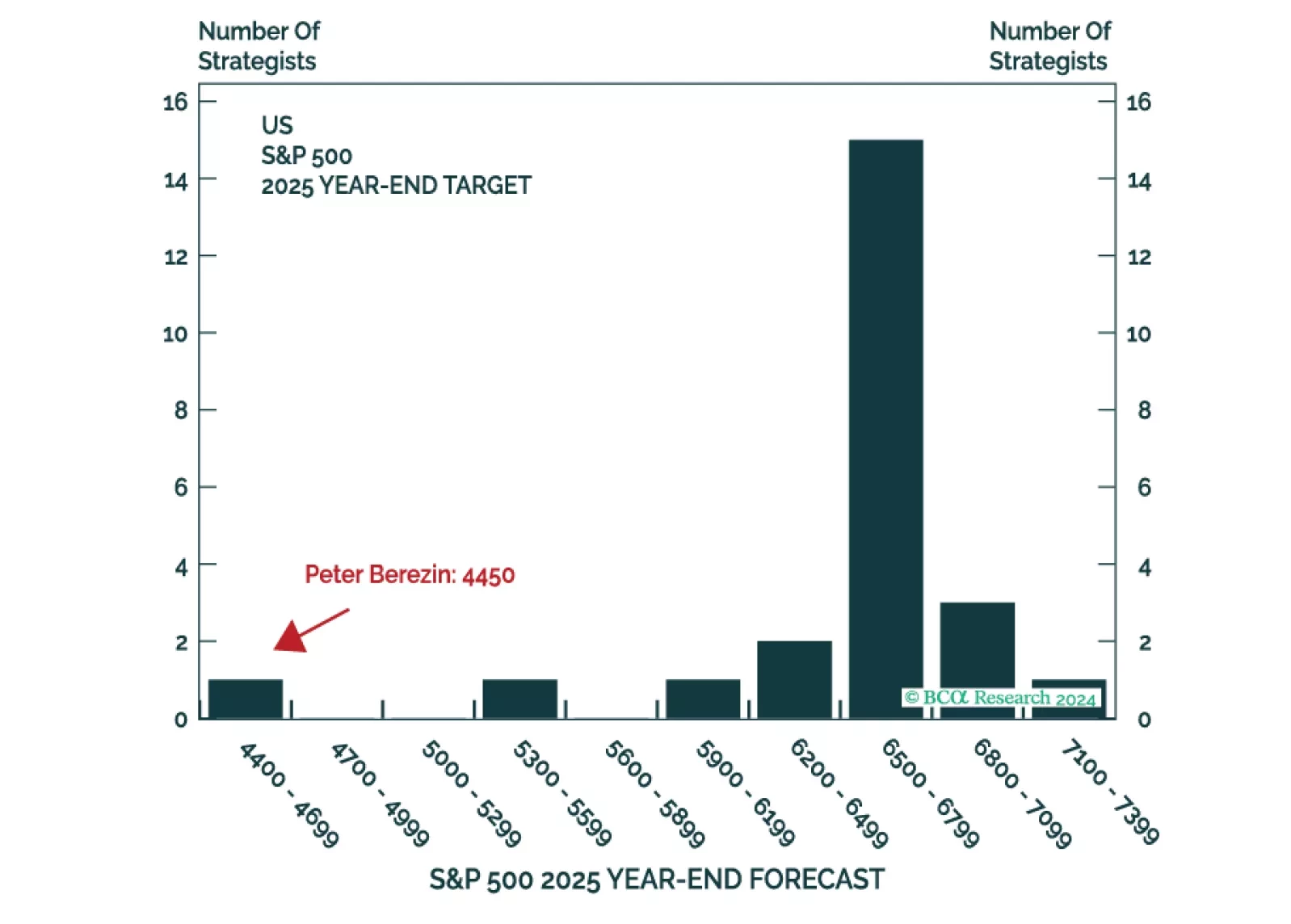

This is the time of the year when strategists are busy sending out their annual outlooks. Here on the Global Investment Strategy team, we decided to go one step further. Rather than pontificating about what could happen in 2025, we decided to harness the power of the multiverse to tell you what did happen (in at least one highly representative timeline).

Next week, please join me for a Webcast on Tuesday, December 17 at 10:30 AM EST (3:30 PM GMT, 4:30 PM CET) to discuss the economy and financial markets.

And with that, I will sign off for the year. I wish you and your loved ones a very happy and healthy 2025. We will be back in the first week of January with our MacroQuant Model Update.

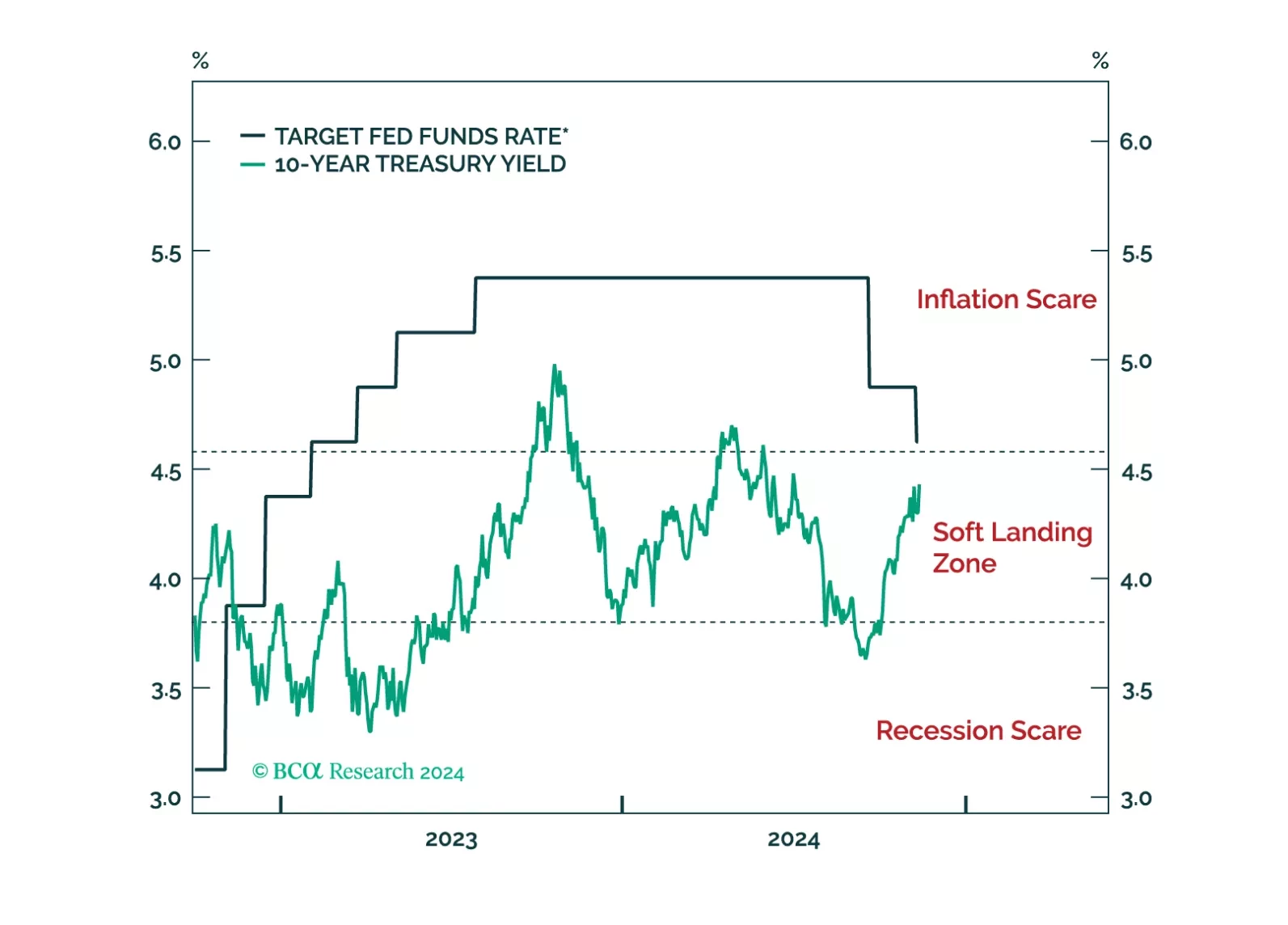

We offer 5 key investment views for US fixed income markets in 2025.

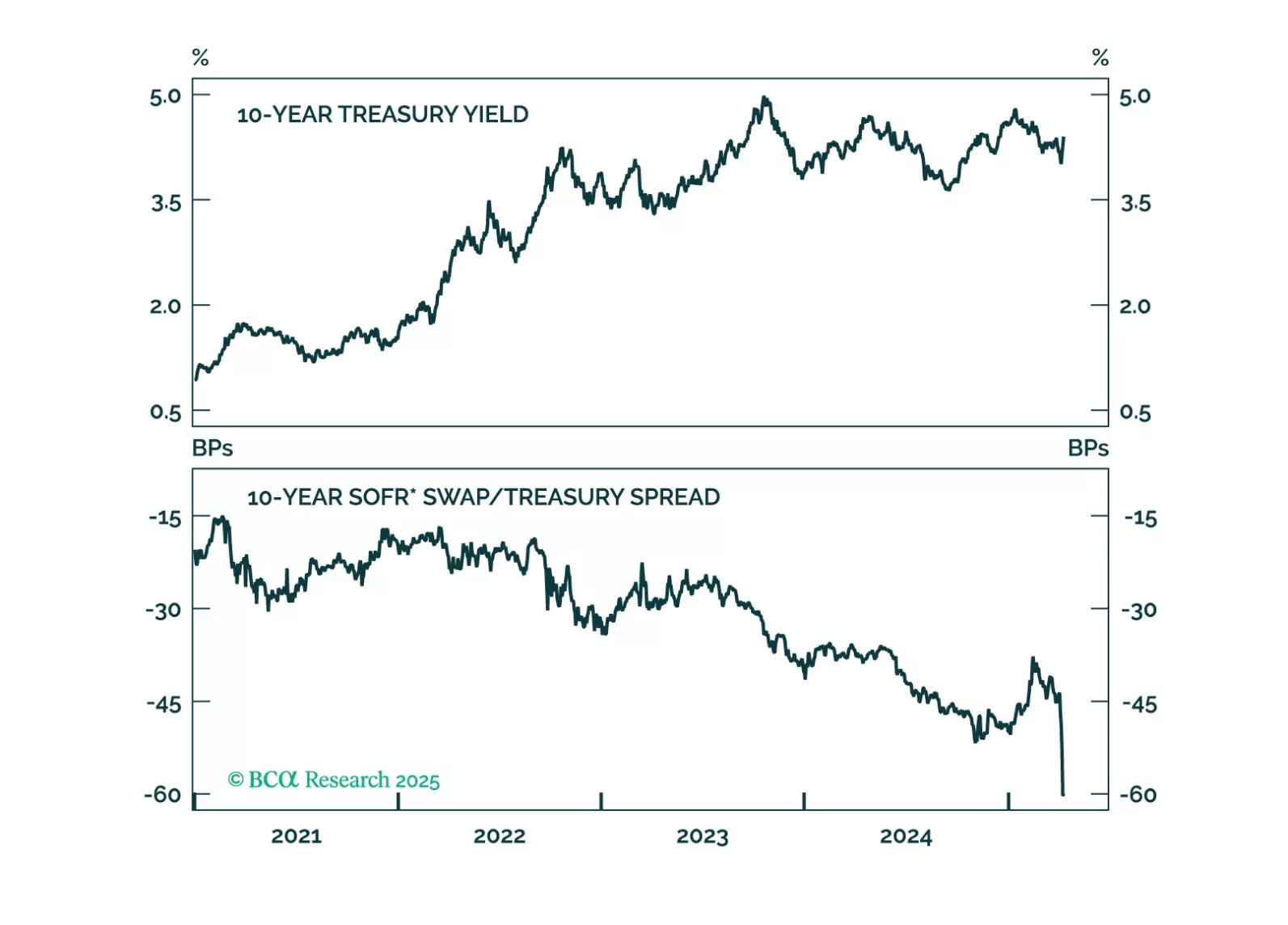

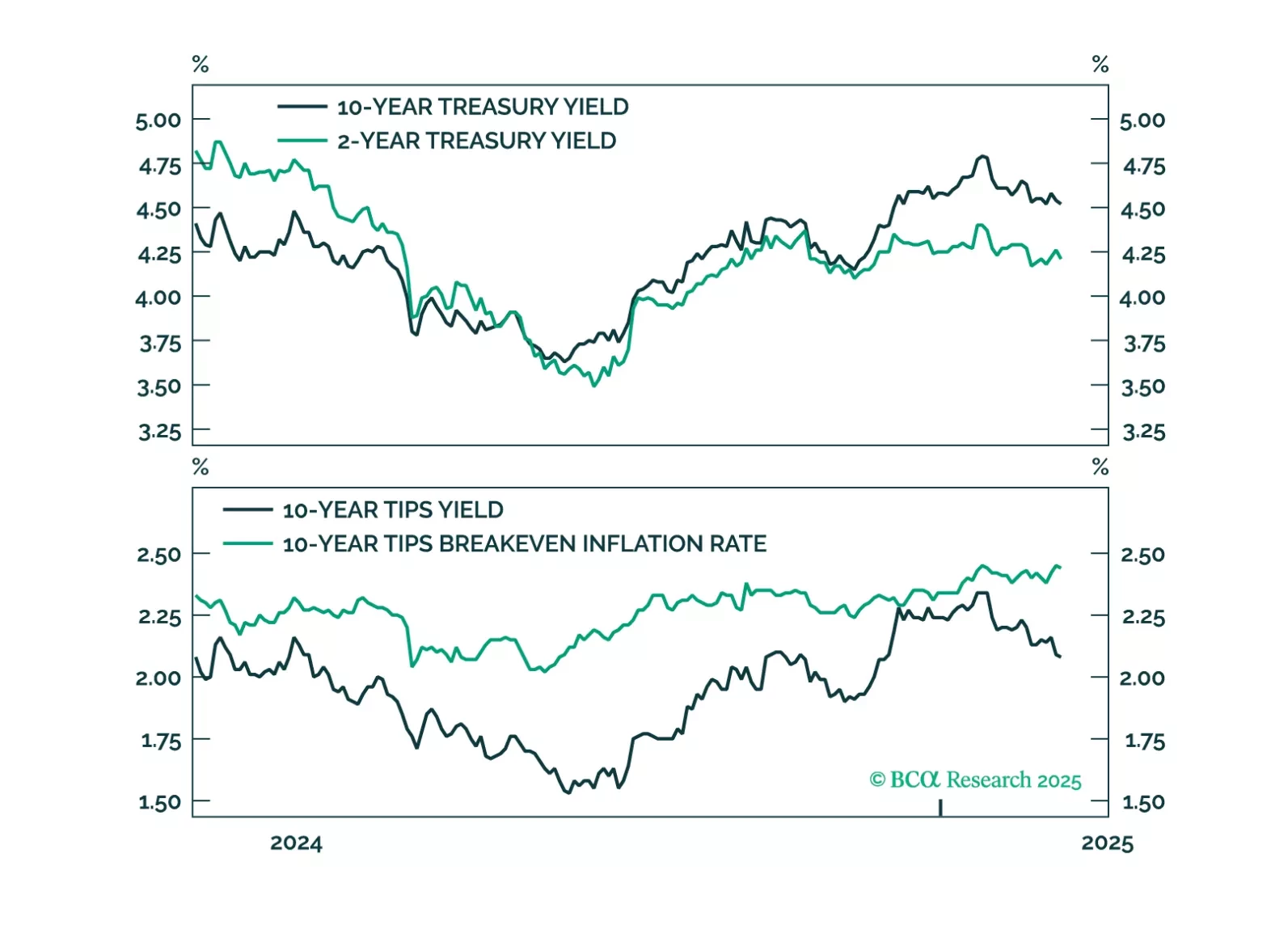

We update our inflation forecast following this morning’s CPI release, concluding that TIPS breakeven inflation rates have room to fall.

Our Portfolio Allocation Summary for November 2024.