Iran

In our last update on the Iran-US conflict, we noted that both sides in the conflict (all three, if we include Israel) were “coloring inside the lines.” By that we meant that they were abiding by the “red lines” of kinetic activity established in the heat of the first iteration of the Iran conflict. Specifically, we noted that investors should watch carefully for any sign that attacks were spreading beyond military facilities.

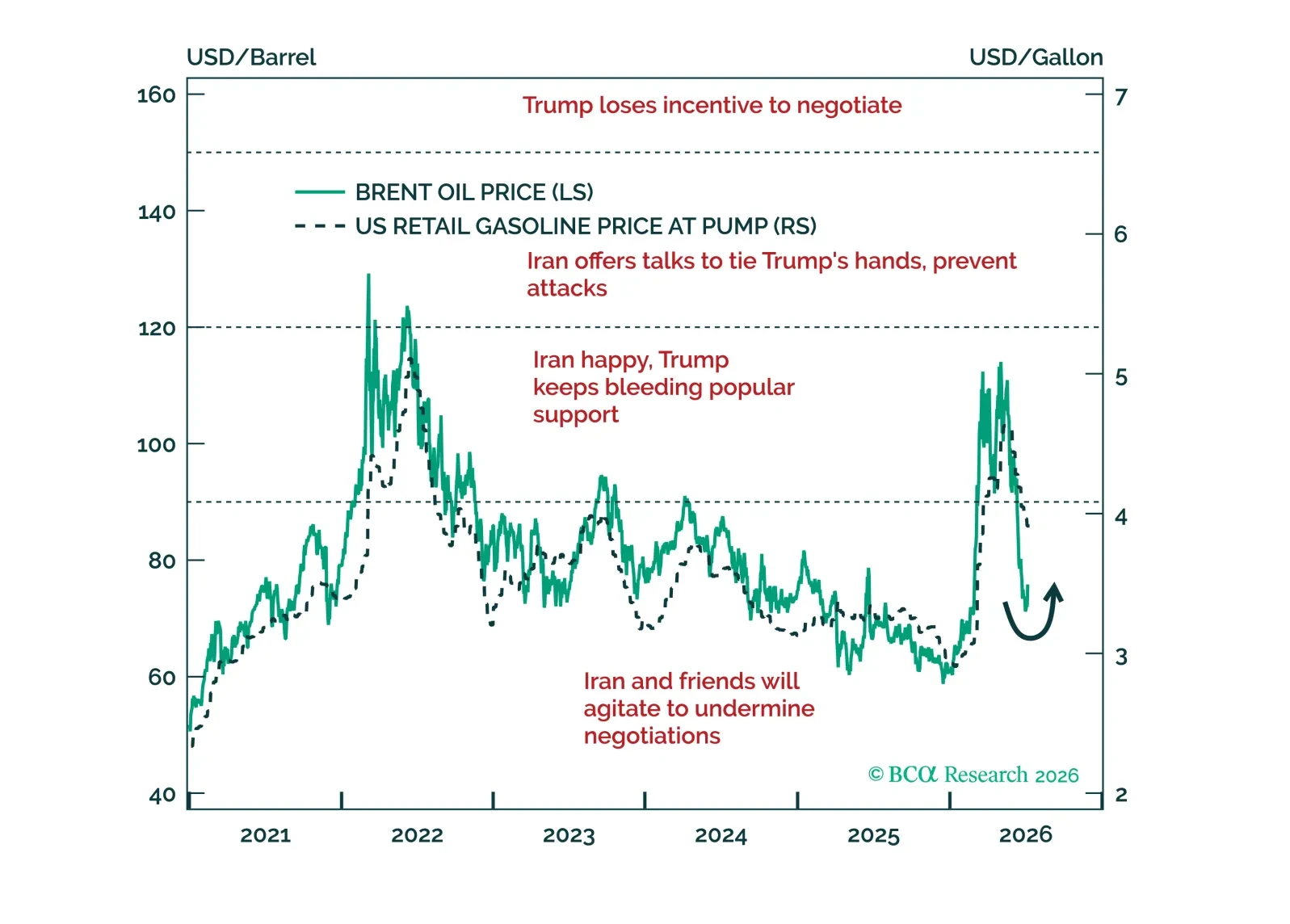

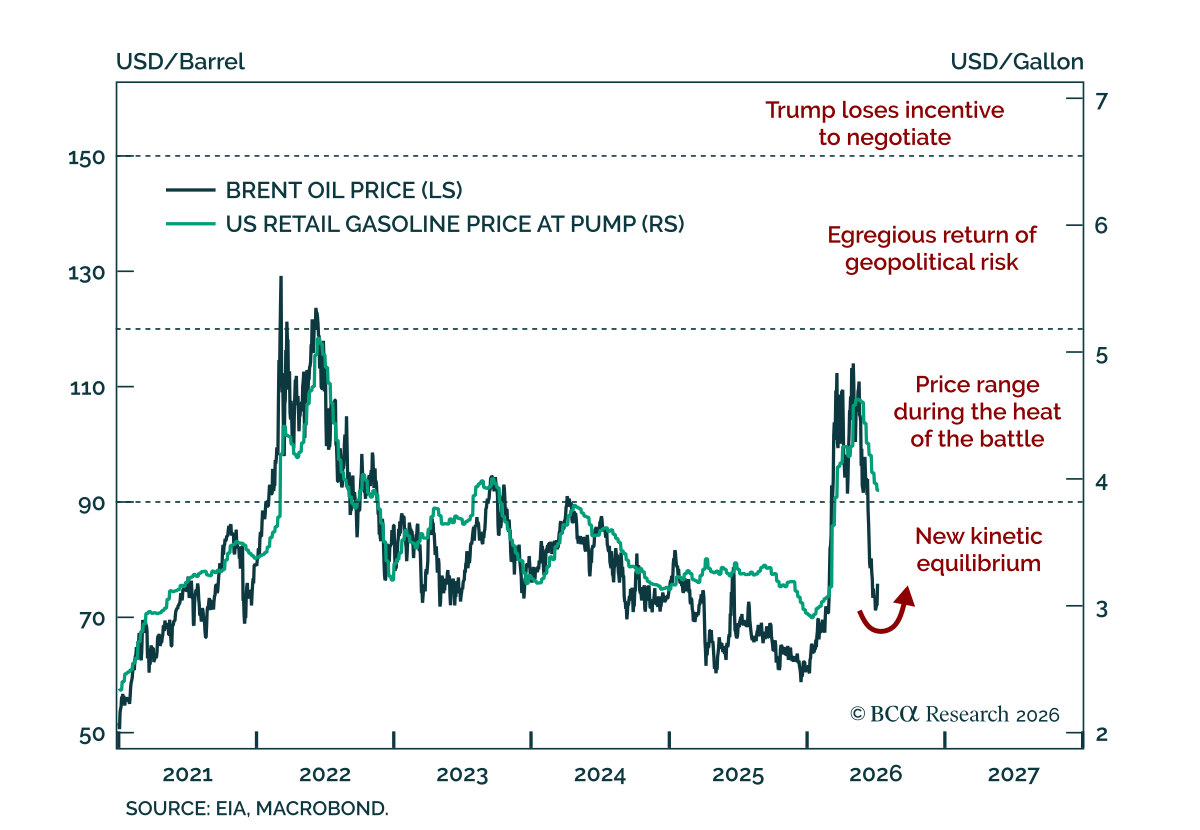

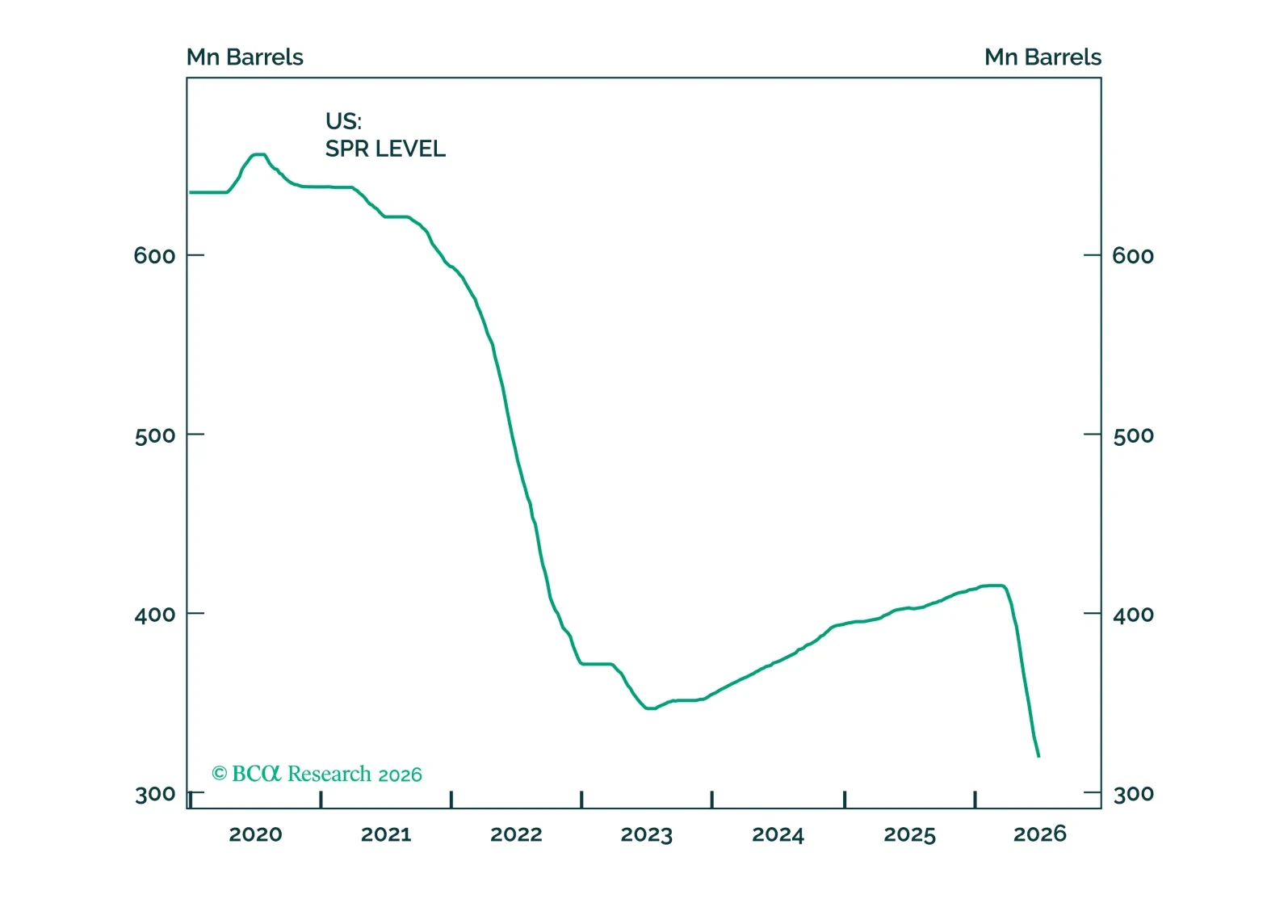

We stick to the view that geopolitical risk has peaked. The US and Iran tensions will increase oil prices, but below a level that will matter for the market. With global liquidity ample, private sector leverage low, and inflation peaking, bears are holding onto an epic collapse of the AI capex to short stocks. Eventually, the capex cycle will end in tears. That much history teaches us. But not yet.

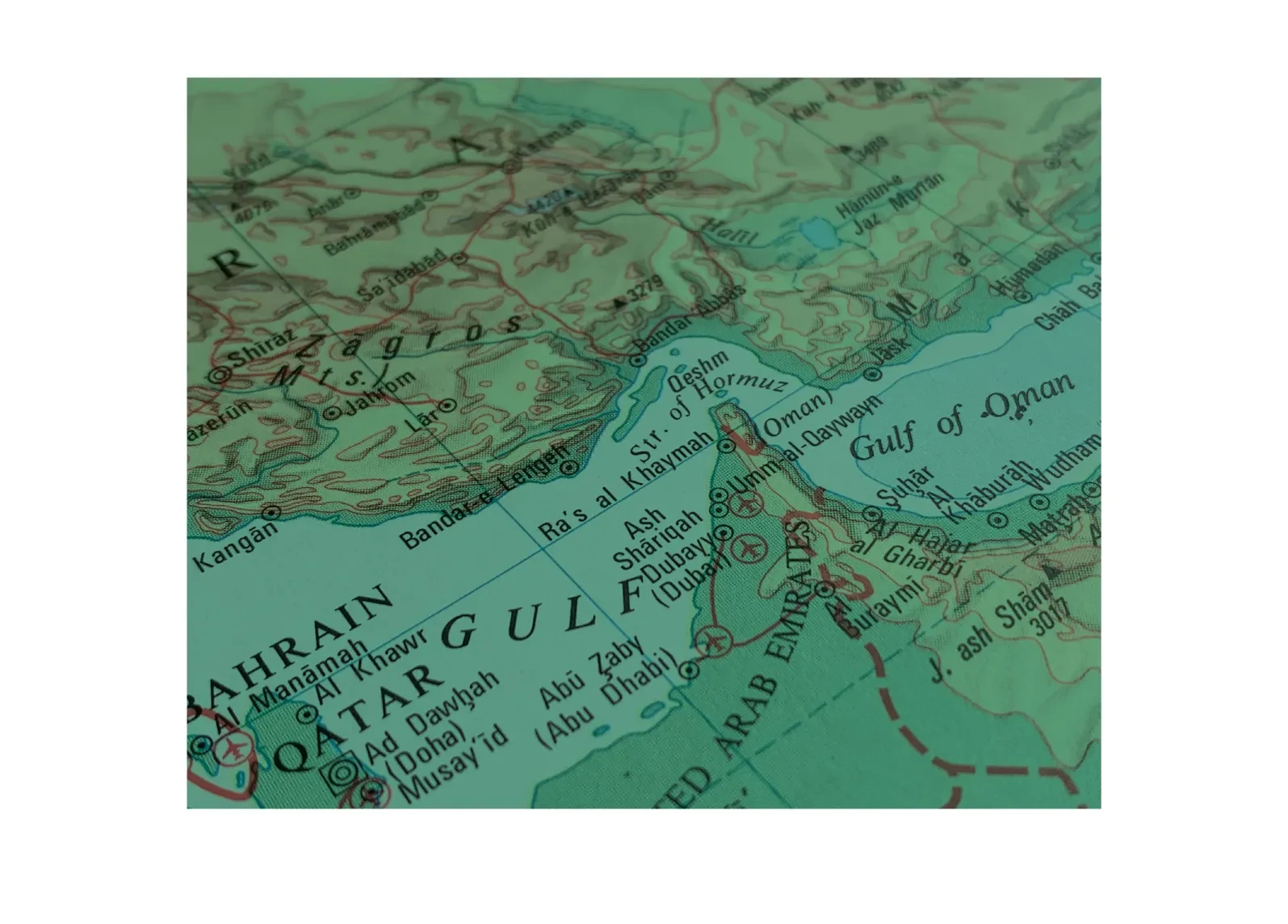

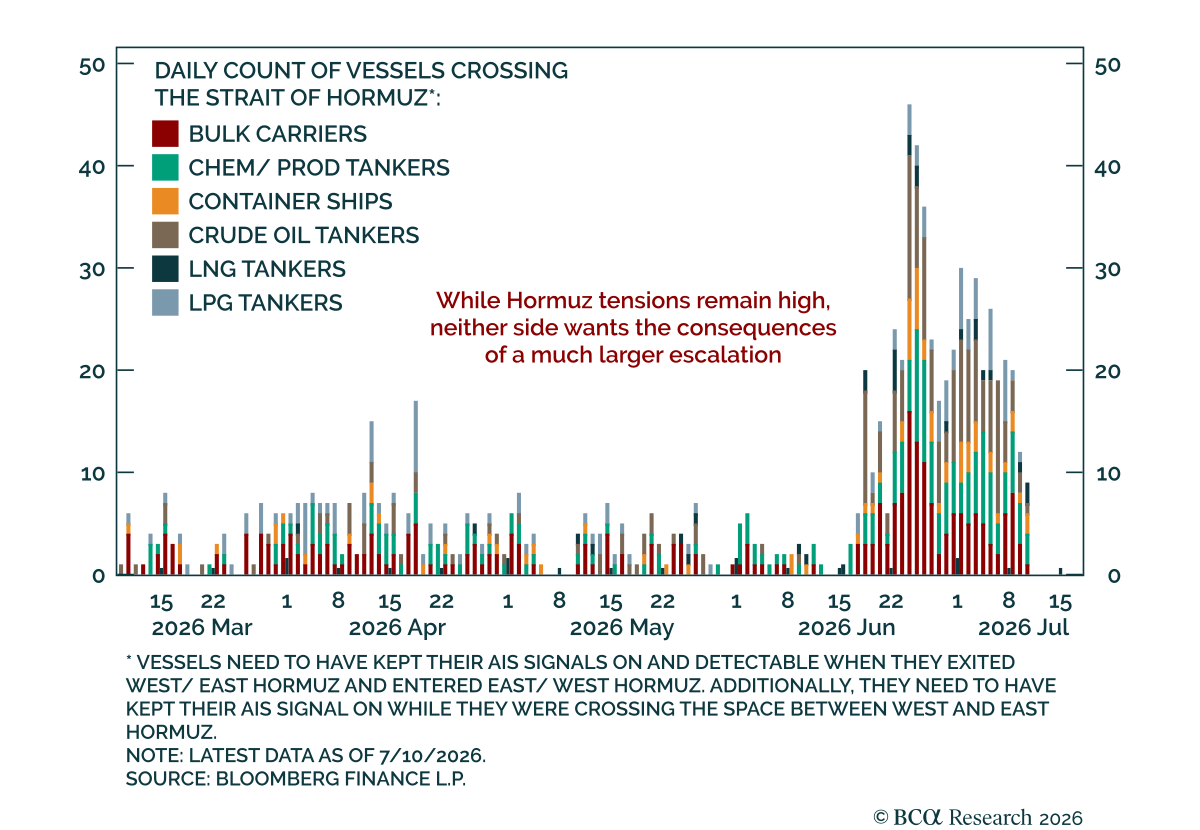

The US and Iran have engaged in a dramatic increase in kinetic activity over the past several days. It all appears to have started on July 6-7, when Iran allegedly attacked several ships in the Strait of Hormuz, vessels that were using the US-recommended route closer to Oman. Following US strikes against Iran in retaliation for that incident – with the US military claiming to have struck 140 sites – Iran has retaliated against US military facilities across the Gulf region. According to media reporting and Iranian government sources themselves, Iran attacked Bahrain, Kuwait, Jordan, Qatar and Oman on July 11-12.

Dear Friends,

As part of our new and improved GeoMacro service, please find attached our Global Risk Outlook, a quarterly digest of scenario probabilities and estimated market impacts for all the major geopolitical topics in the world today.

Our strong record of forecasting geopolitical events with numerical probabilities — including the Russian invasion of Ukraine in 2022, Liberation Day tariffs in 2025, Iran oil shock this year, and last few US elections, among others — is reflected in the constraints-based, Bayesian, and empirical method that we use to produce this report.

The Global Risk Outlook minimizes text and narrative, instead focusing attention on our risk matrixes, with bullet points to explain each scenario. It compiles our global coverage into a single document organized by Red Alerts, Gray Rhinos, Black Swans, and Red Herrings. The forecasting horizon is 12 months, while the financial assets covered are treasuries, the dollar, US and global equities, oil, and gold. Asset allocators and risk managers around the world have found these tables useful as inputs into their investment process, including portfolio stress tests.

On the first page you will find our subjective global geopolitical risk score on a scale of one to ten. Right now the score stands at eight, pending a downgrade whenever durable ceasefires in Iran and Ukraine are settled without spreading to larger conflicts between the great powers — a positive outcome that we ultimately expect, albeit not within the next three months.

Markets have grown accustomed to a high level of geopolitical risk in recent years and are mostly trading on macro and tech themes, but they will respond to significant changes up or down from that level. In the third quarter, we expect the shaky Iran ceasefire to hold together and we give fair odds of a Ukraine ceasefire, which is neutral-to-positive for global risky assets. But we expect Russian provocations to precede a ceasefire, and Iran threats — as well as US-China trade tensions — to escalate again after the US midterm elections, preventing us from being purely optimistic in the third quarter.

Our detailed study of financial market history amid past geopolitical crises informs our estimates of market impacts — and we update our historical table of geopolitical events and market reactions over different time horizons in the appendix of every issue for your convenience.

As always, we welcome any feedback — and we appreciate your readership!

All very best,

Matt Gertken

Head of GeoMacro

mattg@bcaresearch.com

Access BCA's US Midterm Election Dashboard

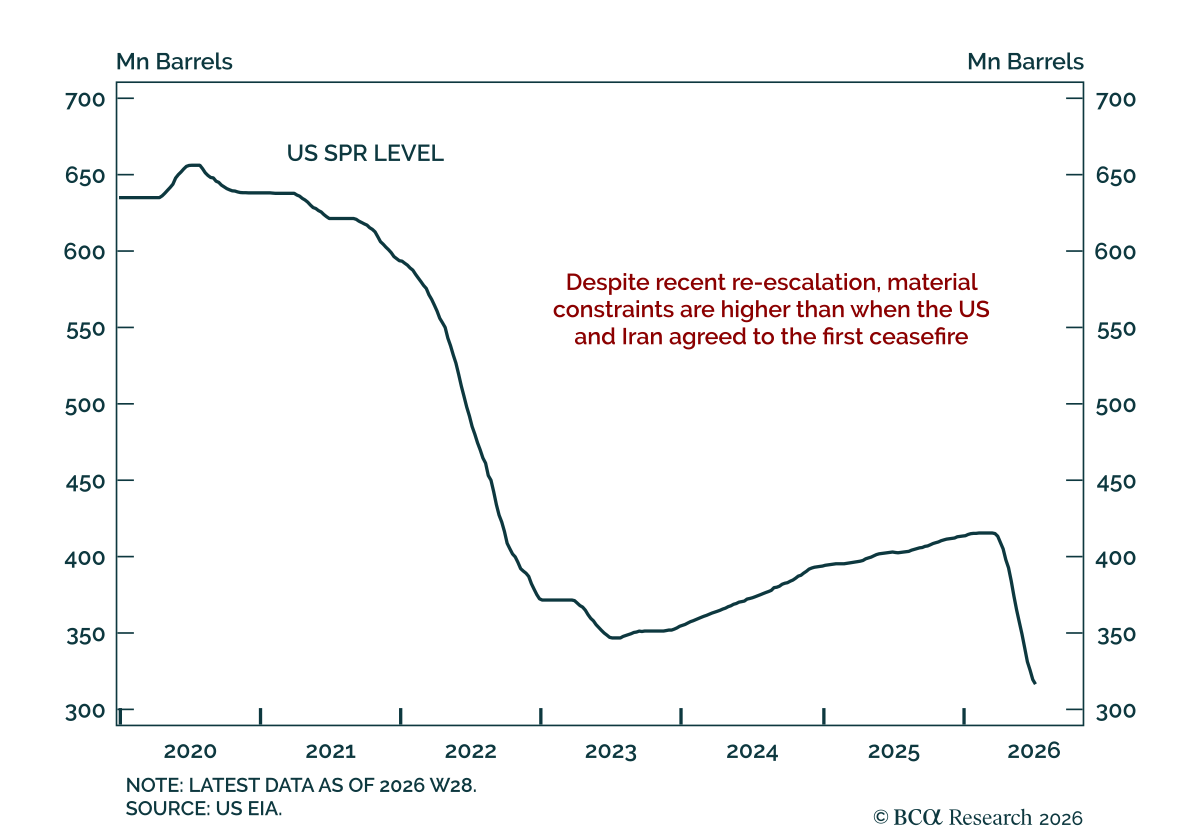

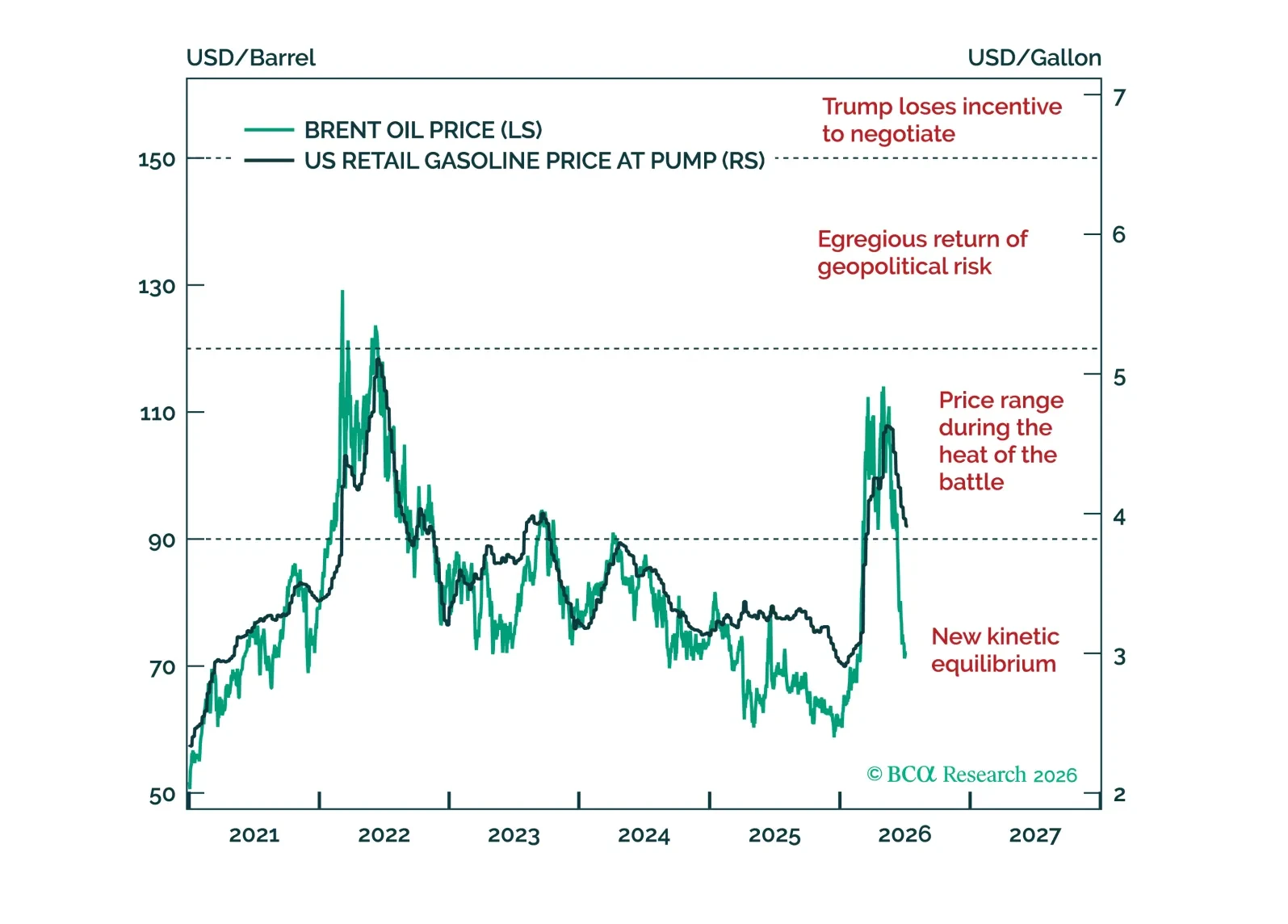

Just as we declared that geopolitical risk has peaked for the year – in yesterday’s Alpha report – President Trump has declared the ceasefire with Iran over after repeated violations via strikes against three tankers in the Strait of Hormuz. That is the life of an investment strategist. But the underlying dynamics continue to play out as we’ve described.

We remain bullish on risk assets given that the Hormuz war has resolved itself and oil prices have declined by even more than we expected. In addition, the macro fundamentals are not flashing any red signs. That said, we remain skeptical that the AI revolution will continue without any hiccups. In fact, a price war may ensue once all the players realize they’re in the commodity – not tech – space.