Iran

Since our last missive on June 15, three trading days have passed. The S&P 500 is up 0.2%, the US 10-year Treasuries yield has declined by 3 basis points, Brent crude is up 2.7%, gold is down by 2%, the JPY is down 0.7%, and DXY is up 0.7%. Our message prior to the start of these three trading days was that there was some more upside to oil prices in the very near term. However, that this upside would not be that impressive. Second, that the S&P 500 should not be shorted. And that the USD and US Treasuries would not be a great hedge, but that gold and JPY would be.

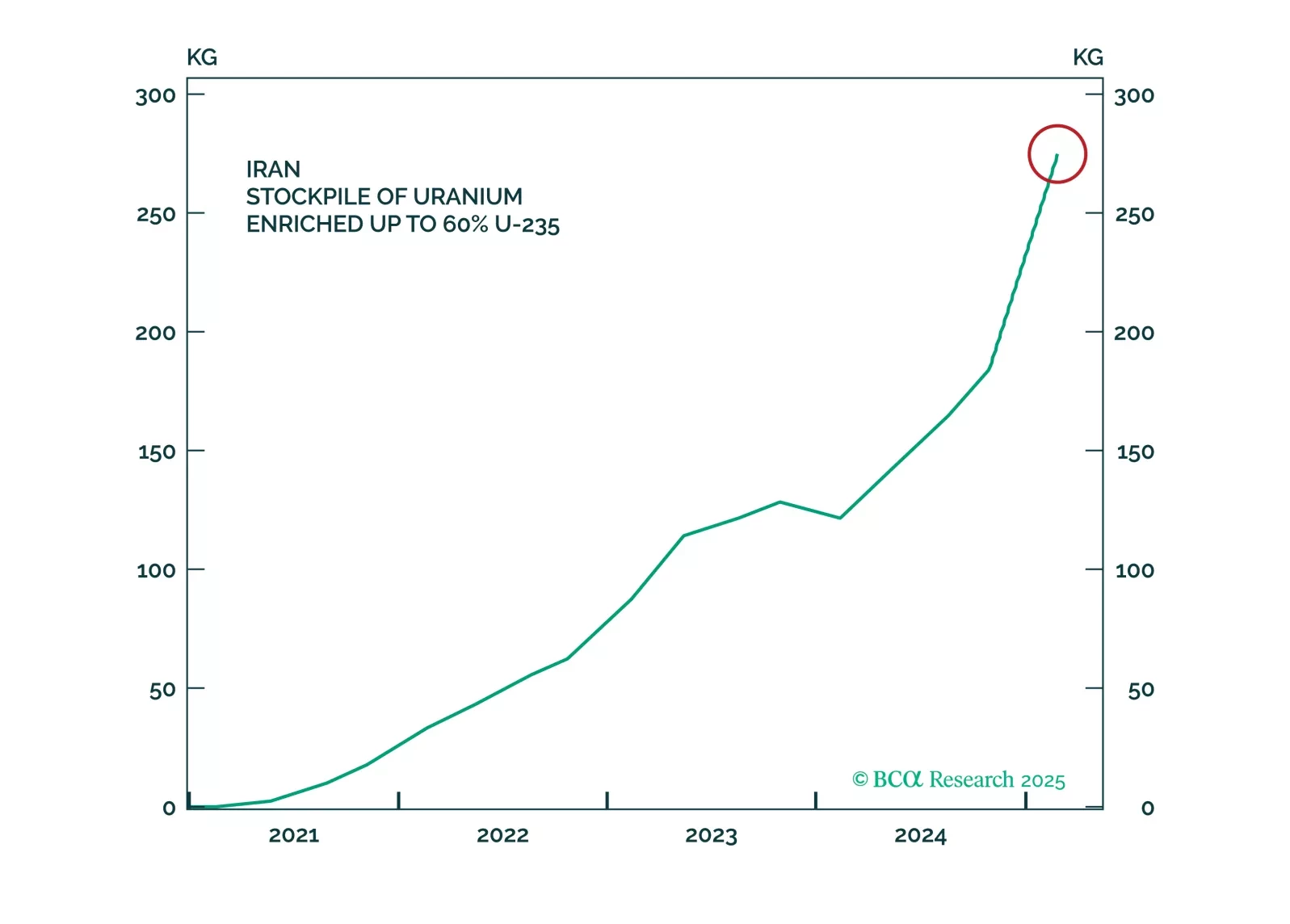

Even if Iran tries to revive talks, the US has an irresistible opportunity to dismantle its nuclear program. Tactically, investors should favor Treasuries over the S&P, defensive sectors over cyclicals, energy stocks over cyclicals, and US stocks over European stocks in the near term.

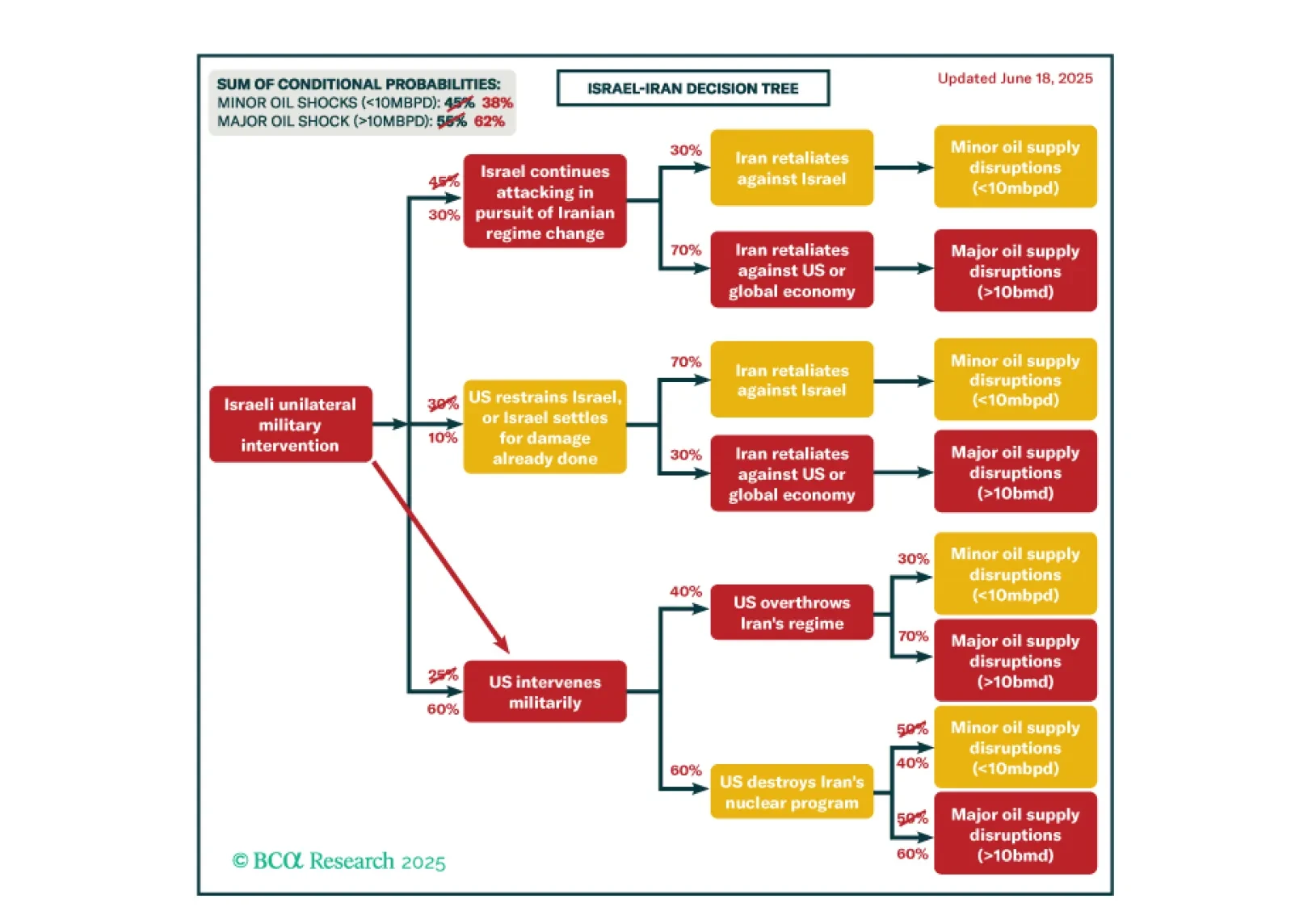

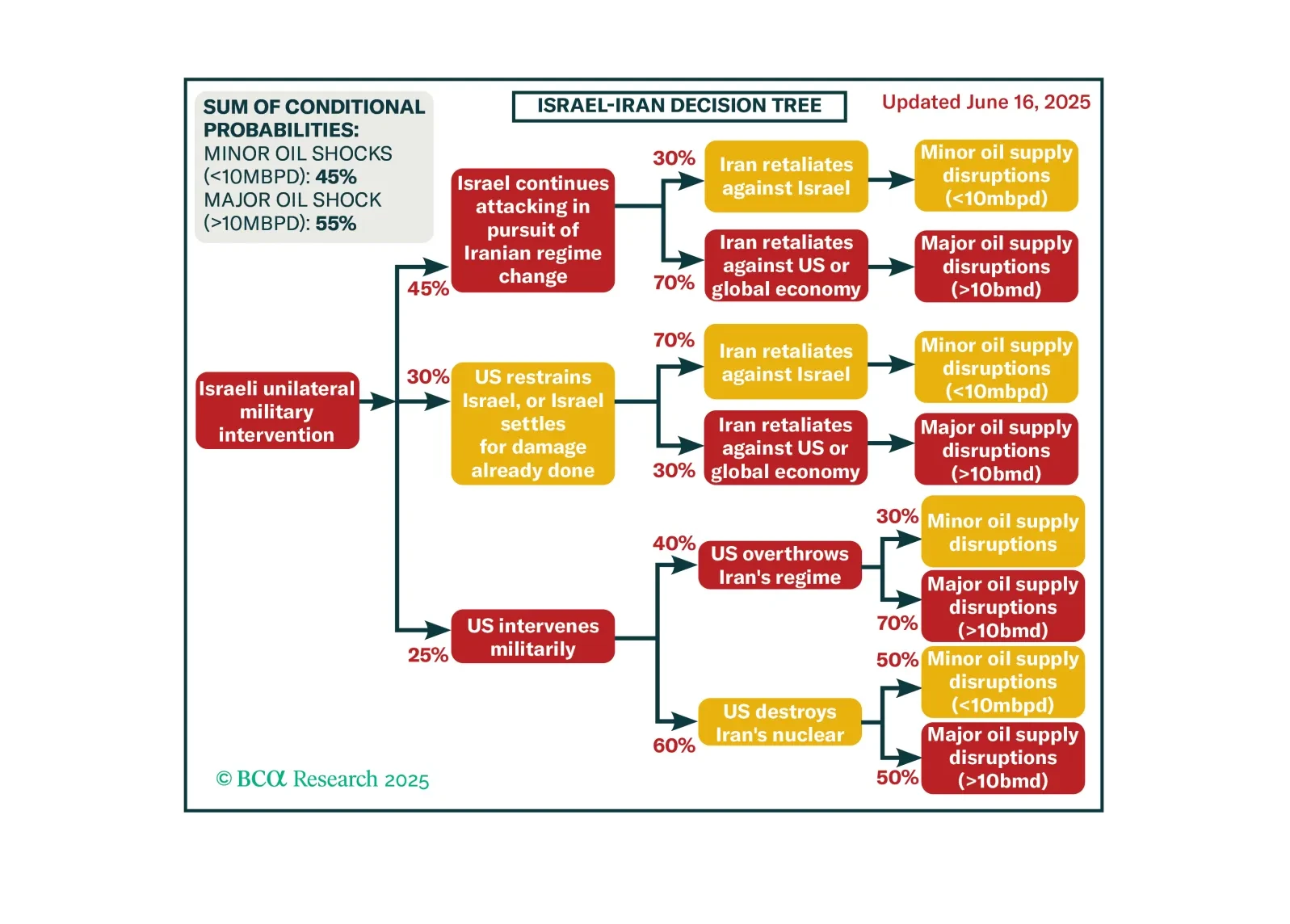

Israel’s attacks on Iran will continue until Iran is forced to strike regional oil supply to get the US to restrain Israel. That may not work. Investors should prepare for a broader economic impact of the conflict.

It has been three days since Israel started its air campaign against Iran. We now have greater visibility into Israel’s targeting, as well as Iran’s retaliation. Israel’s air force has struck almost every single Iranian nuclear program facility, government buildings, research centers, and – most importantly – energy facilities. Most of these targets are expected, but the attacks against Iran’s energy facilities are concerning as they suggest that Tehran may have casus belli to strike back at the energy facilities strewn around the Persian Gulf.

Investors should hold gold, build up some cash, tactically overweight US equities relative to global, and prepare for at least minor oil supply shocks – possibly major shocks – as the Israel-Iran war escalates.

Israel has taken unilateral action against Iran on June 12. According to the media reports, the following are the key developments:

- Israel has attacked multiple targets across Iran, including in the capital Tehran.

- Israeli Prime Minister Benjamin Netanyahu has stated that the Operation Rising Lion would “continue for as many days as it takes to remove” the alleged Iranian nuclear threat.

- The US has stated that it did not participate in the attack, calling Israel’s action unilateral.

Negotiations on trade, Iran, and Ukraine will prove critical this month. Markets will remain volatile because positive data surprises enable the White House to press its hawkish tariff hikes, while negative surprises force the White House to backpedal.

Stocks will continue to struggle in the second quarter as President Trump tries to implement tariffs. Tax cuts will only temporarily dispel growth fears, if at all. Middle Eastern instability will add oil price surprises to an environment that is looking fairly stagflationary.

Trump’s foreign policy can be explained by rational US interests, but it requires settling the trade war with allies sooner rather than later. Book gains on EUR-USD for now.

The tariffs on Canada and Mexico will come into effect as scheduled while the tariffs on China will be doubled. In the Middle East, Iranian response to any attack will threaten Middle Eastern oil supply. Meanwhile, Chinese fiscal support will surprise to the upside at the Two Sessions. But Trump's China policy will cause volatility. Now that the stock market is cracking, reinitiate defensive trades, such as long treasuries versus US stocks and long global defensives versus cyclicals.