Iran

Domestic politics suggest that President Trump needs to retreat from the war in Iran, but strategic factors suggest not. Stay defensive for now.

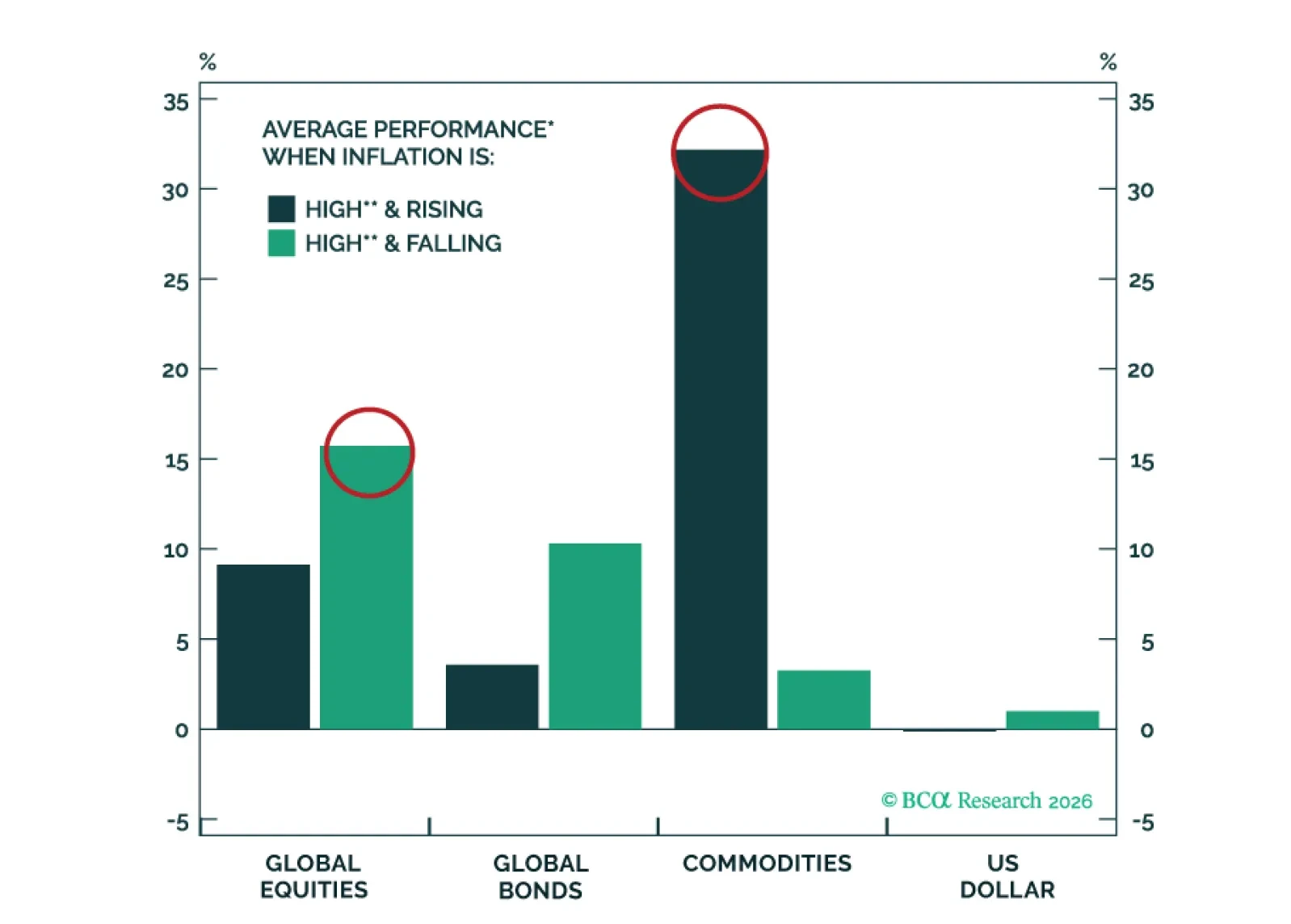

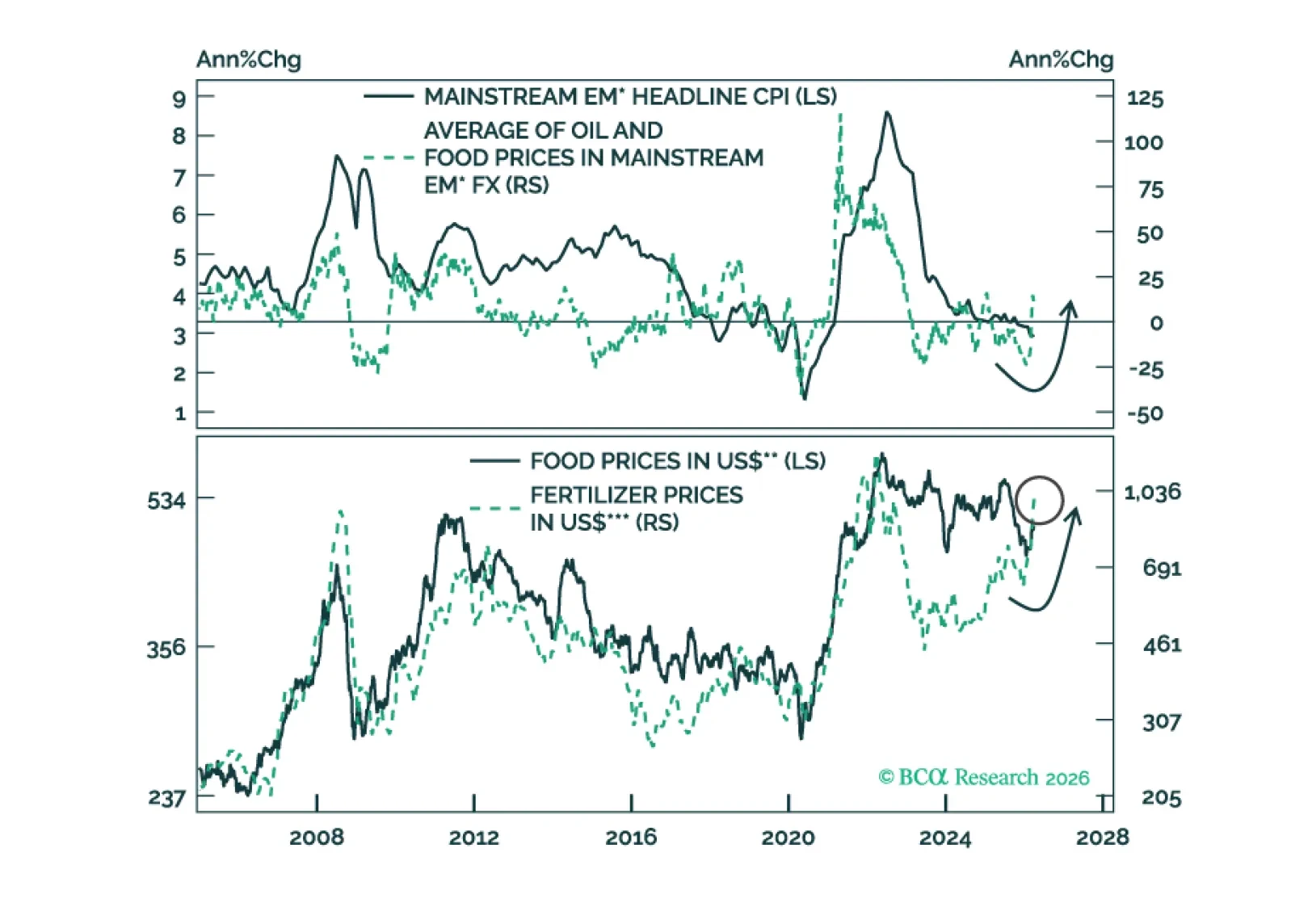

The Iran war provides a timely motivation for examining how the main financial asset classes and commodity sectors perform across different inflation regimes and during periods of elevated geopolitical risk.

Our "miniature stagflation" episode is coming together on the back of the Iran shock, China slowdown, and American political division.

The global risk-off phase will persist. It is too early to buy local-currency bonds in Mainstream EM, but it is not too late to sell EM sovereign and corporate credit (USD bonds).

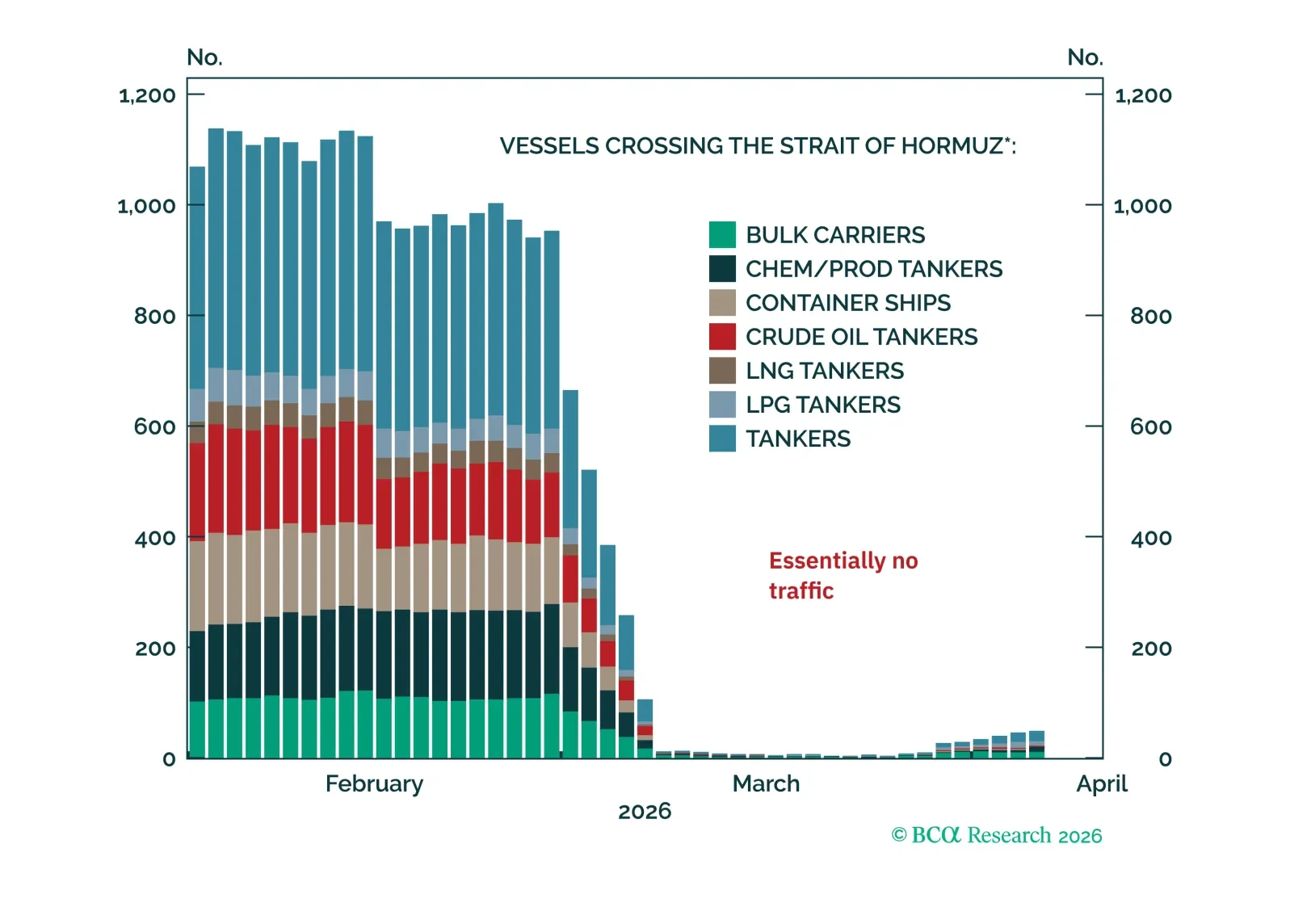

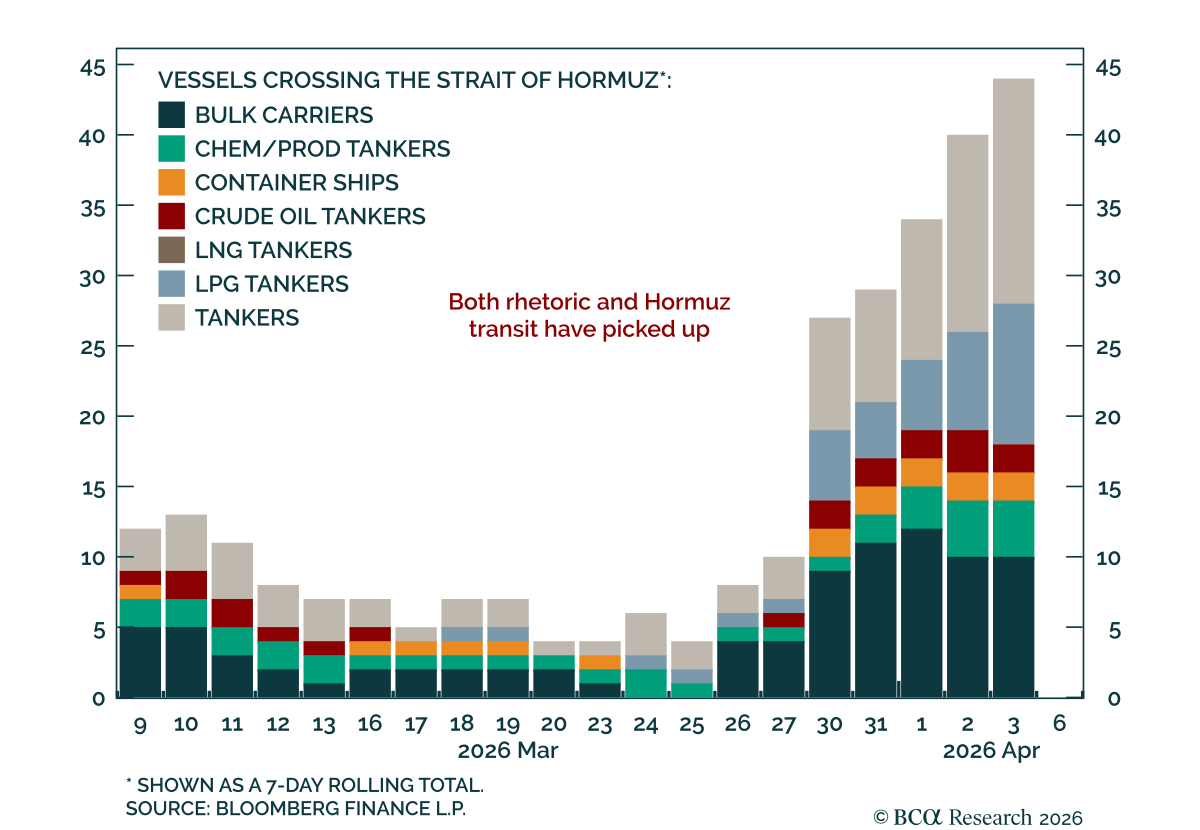

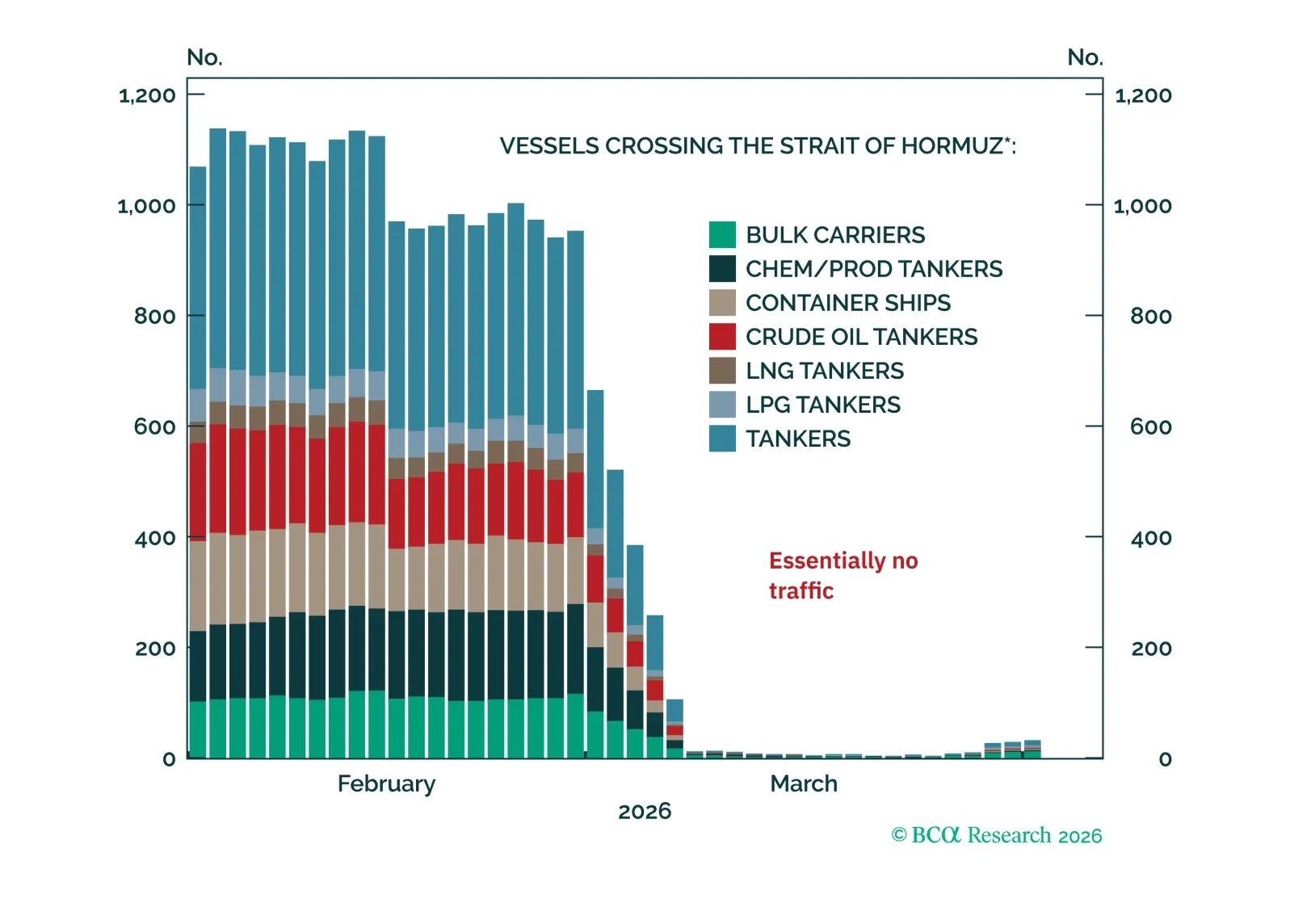

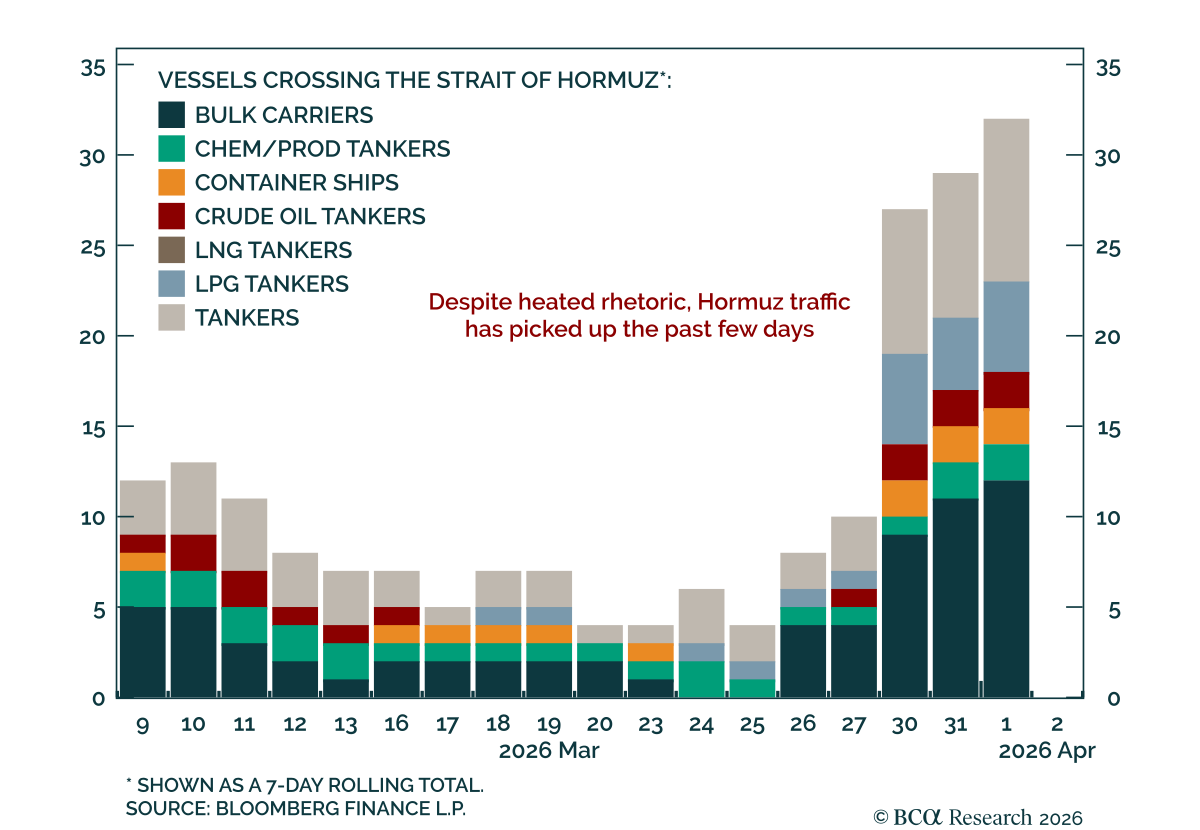

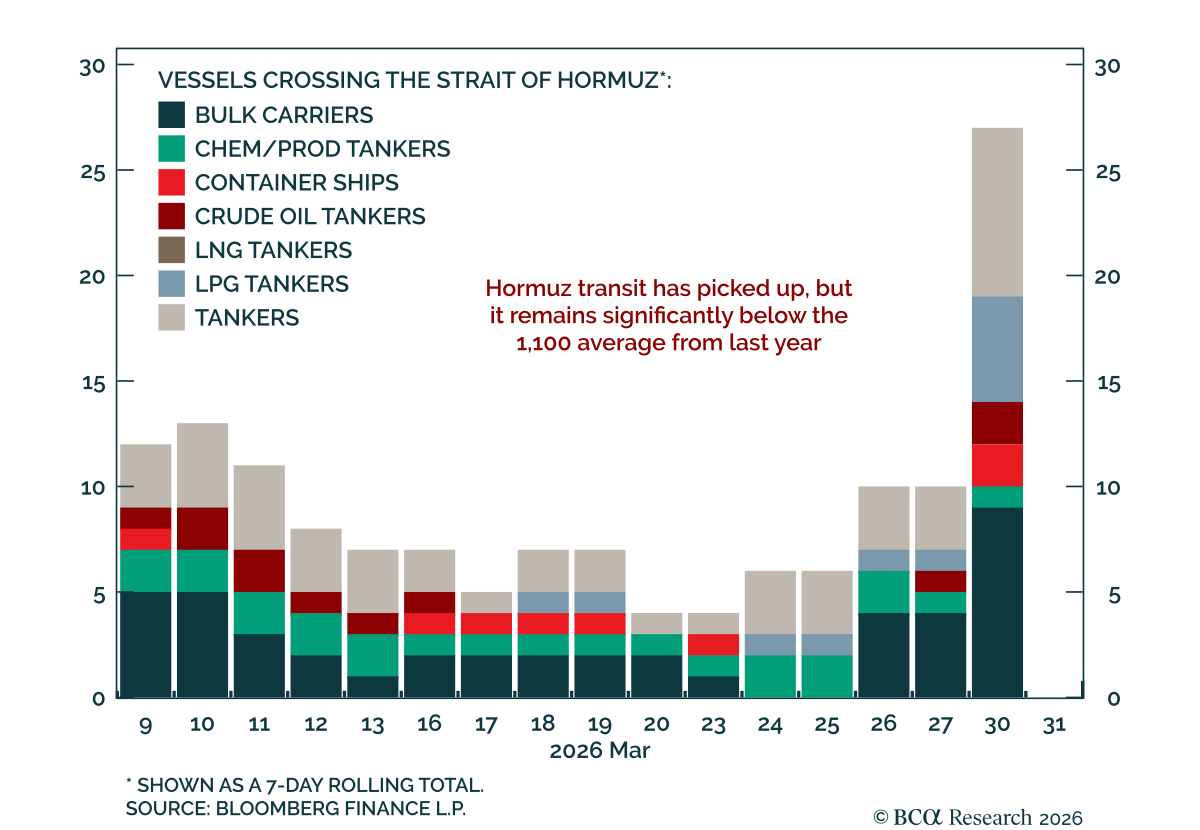

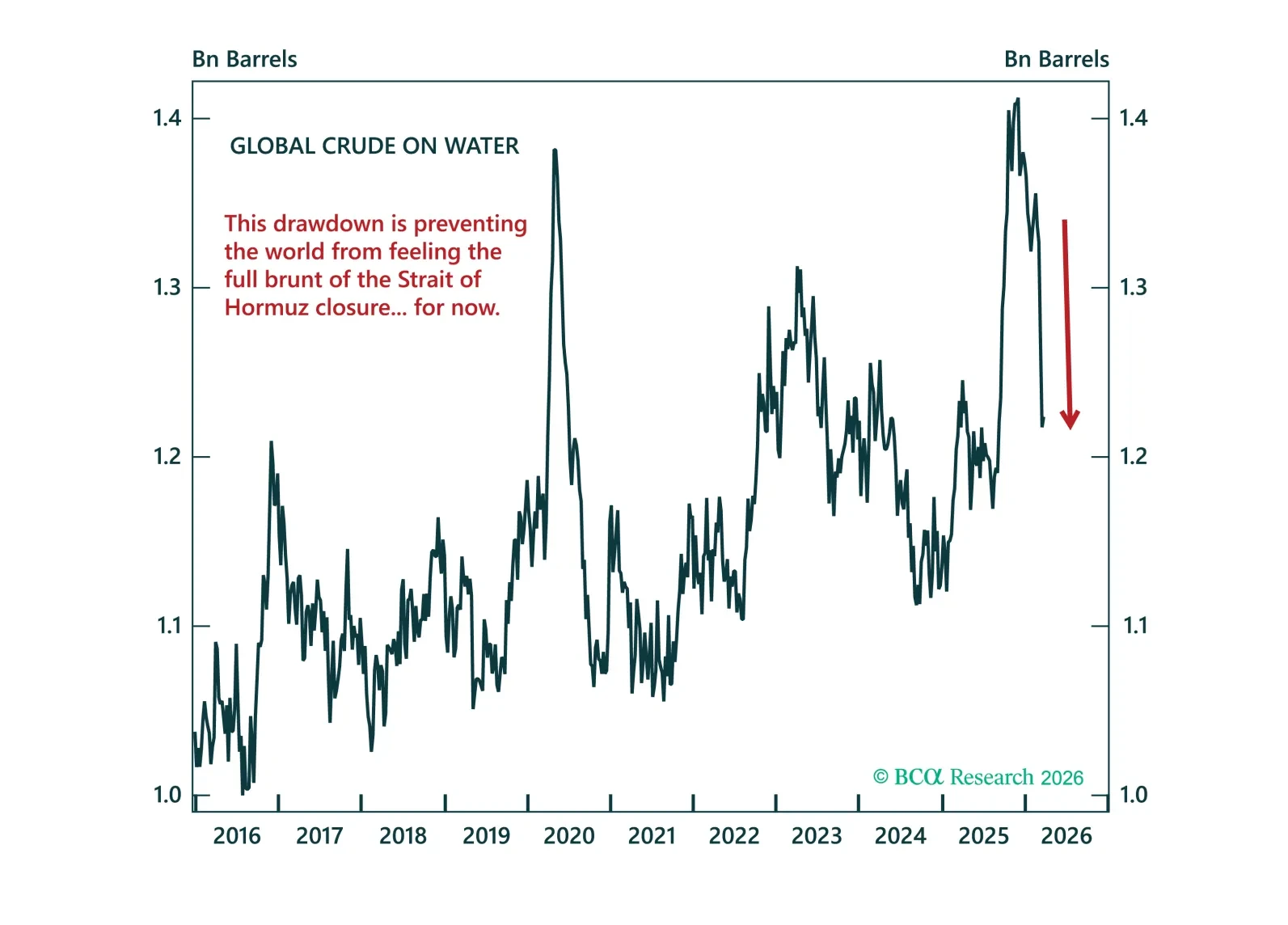

Over the past 48 hours, there has been a cacophony of statements back and forth between Tehran and Washington, DC, some suggesting that the probability of de-escalation is rising. At the same time, kinetic action has continued unabated. A Kuwaiti tanker was targeted by Iran off the coast of the UAE, followed by a Qatari tanker off Doha, and the US ramped up its attacks on Iranian industrial capacity. The world now awaits with great anticipation President Trump’s remarks to the nation on April 1.

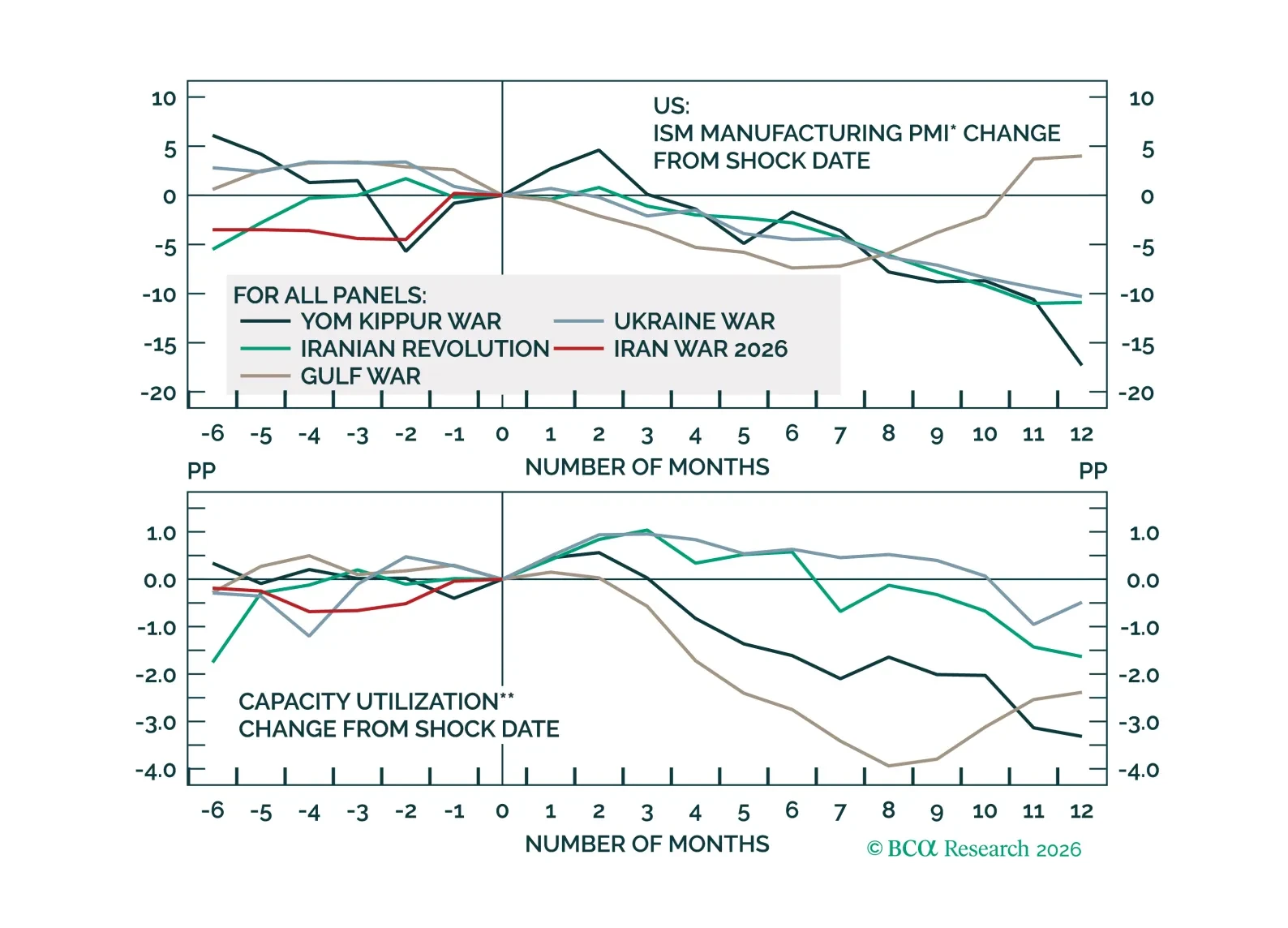

We explore how markets reacted to different oil supply shocks in the past, how conditions differ today, and provide a playbook for investors to navigate the current crisis. Remain neutral between equities, bonds, and cash. Downgrade Tail Risk Strategies from Max Overweight to Overweight.

We are pleased to introduce our new Quarterly Investment Outlook, a joint publication bringing together the European Investment Strategy (EIS), Global Fixed Income Strategy (GFIS), and Foreign Exchange Strategy teams.

The main takeaway of the current edition is that investors should not add risk. Markets are still focused on inflation, but the binding constraint is growth: if the energy shock persists into mid-April, a rapid shift toward recession pricing will follow.