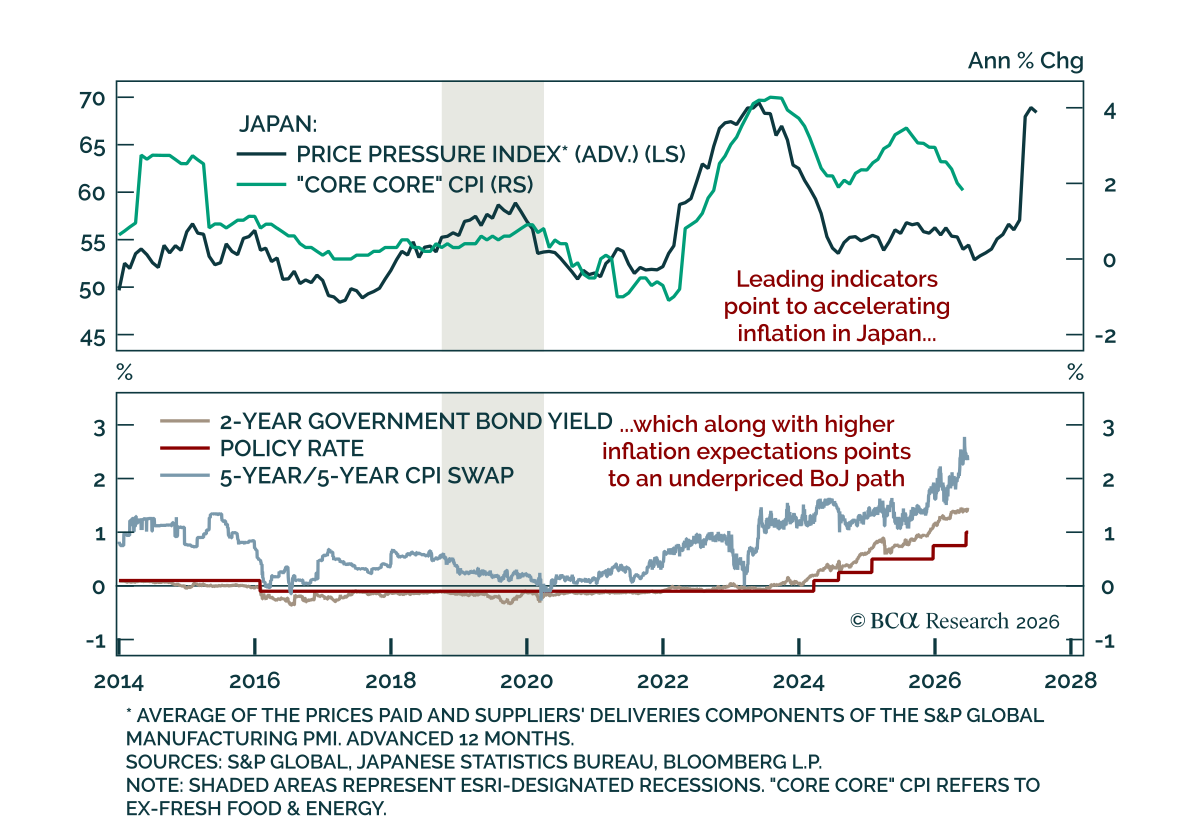

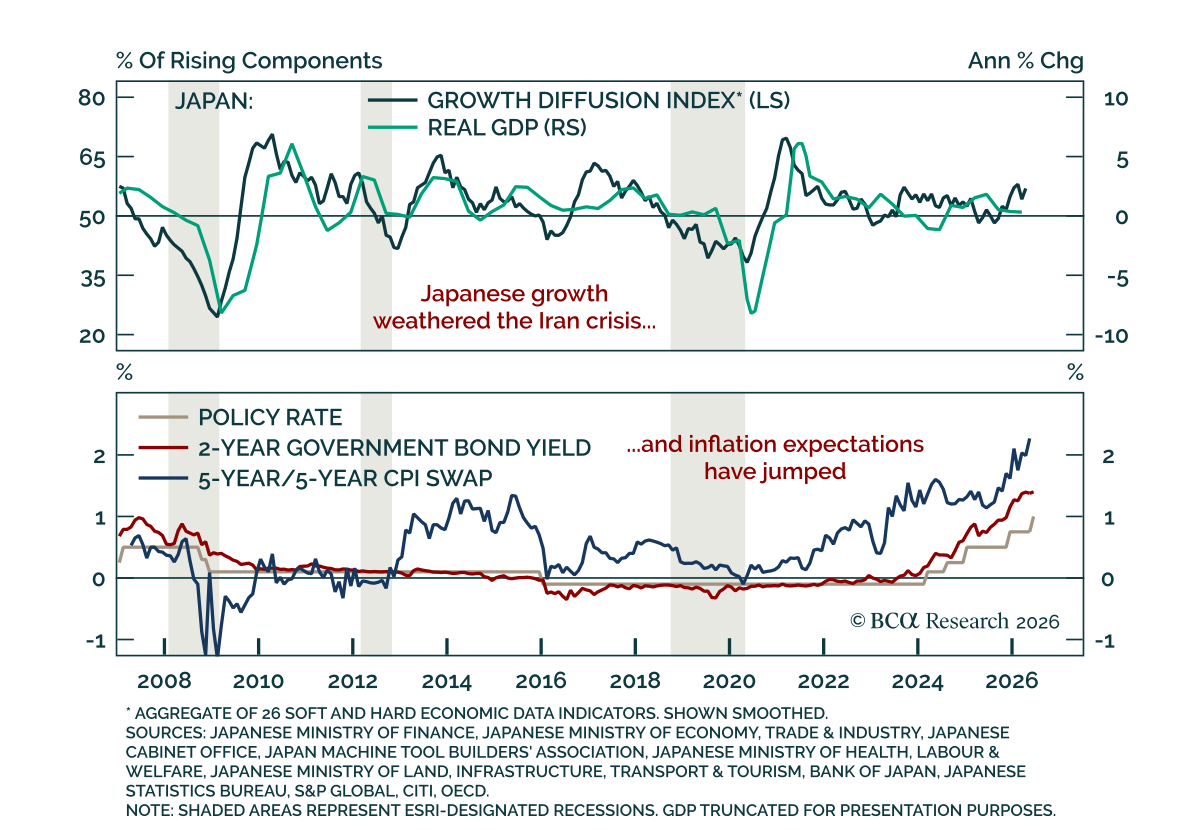

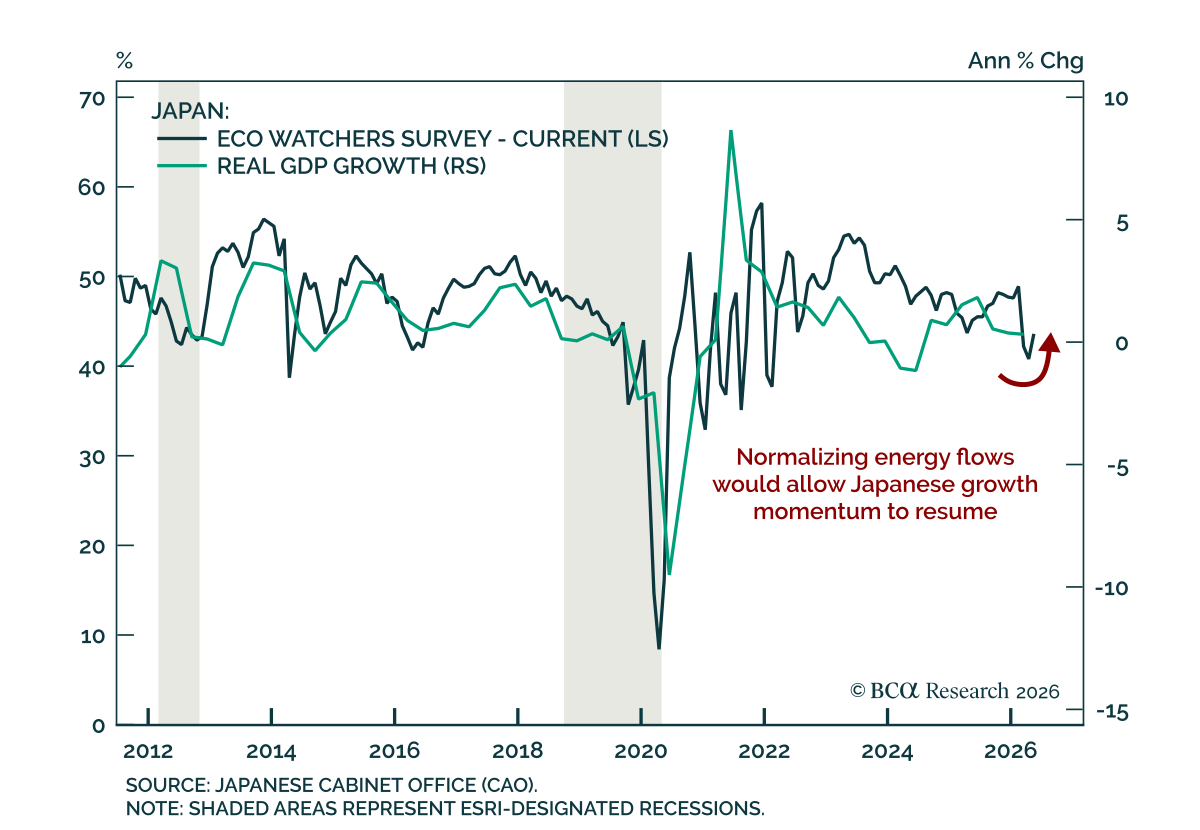

Japan

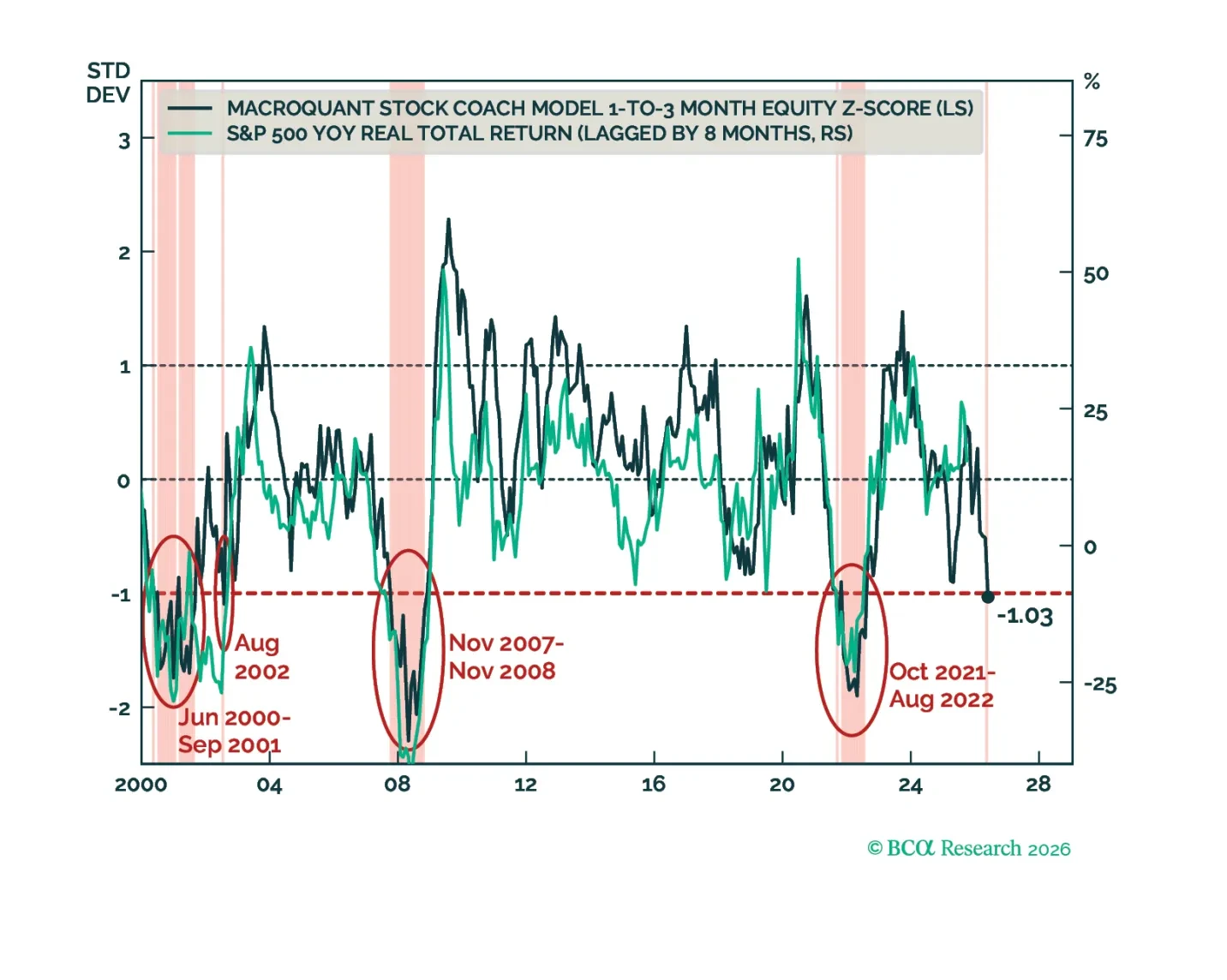

The equity bull market is getting long in the tooth. Bonds should perform well once economic growth begins to slow. The dollar will strengthen over the coming months before resuming its downtrend. While crude has likely found a near-term floor, we favor metals over energy in the long run.

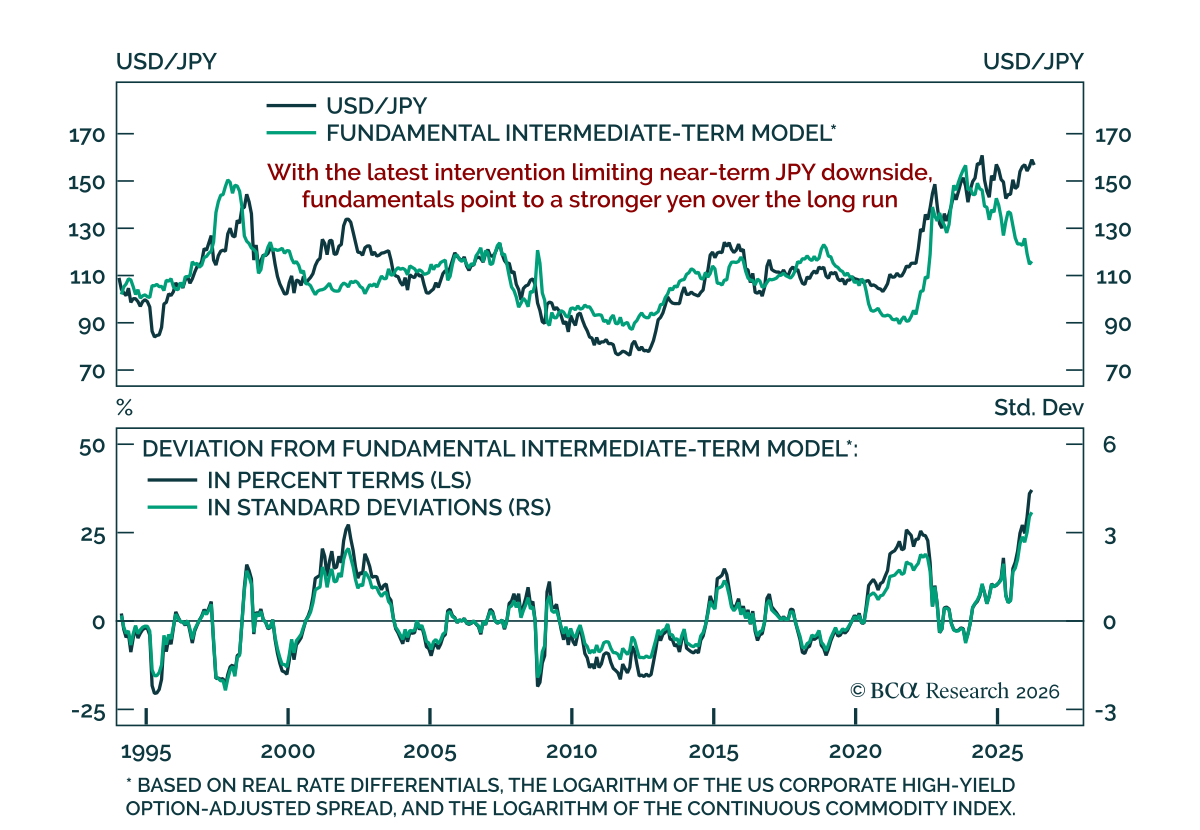

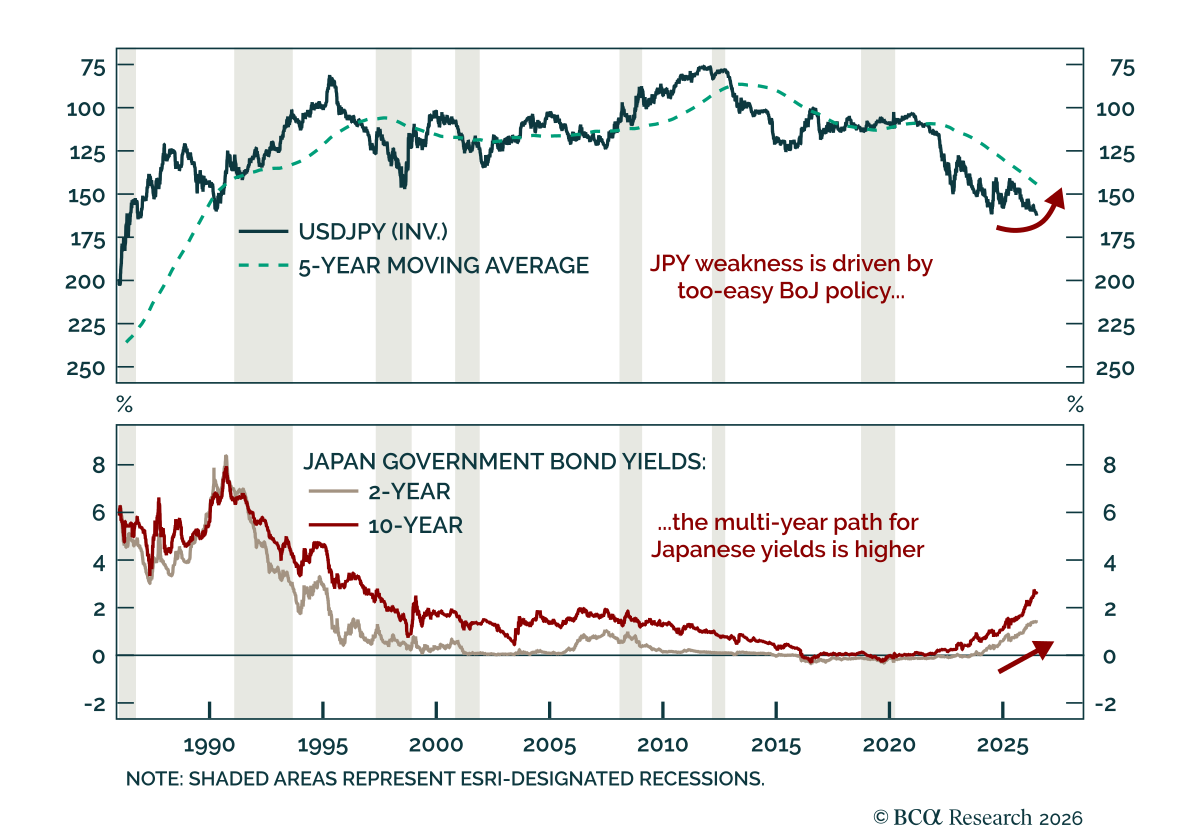

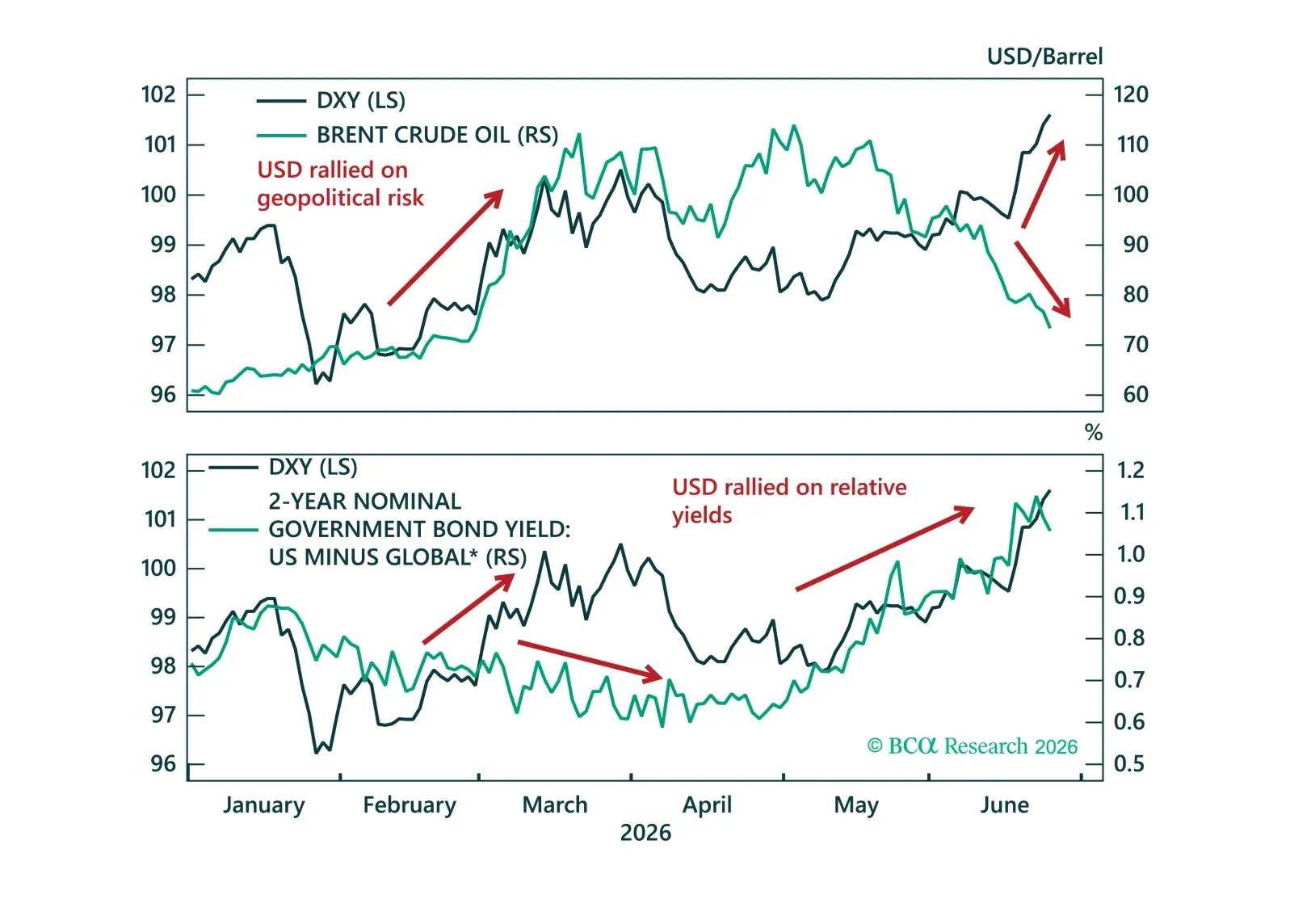

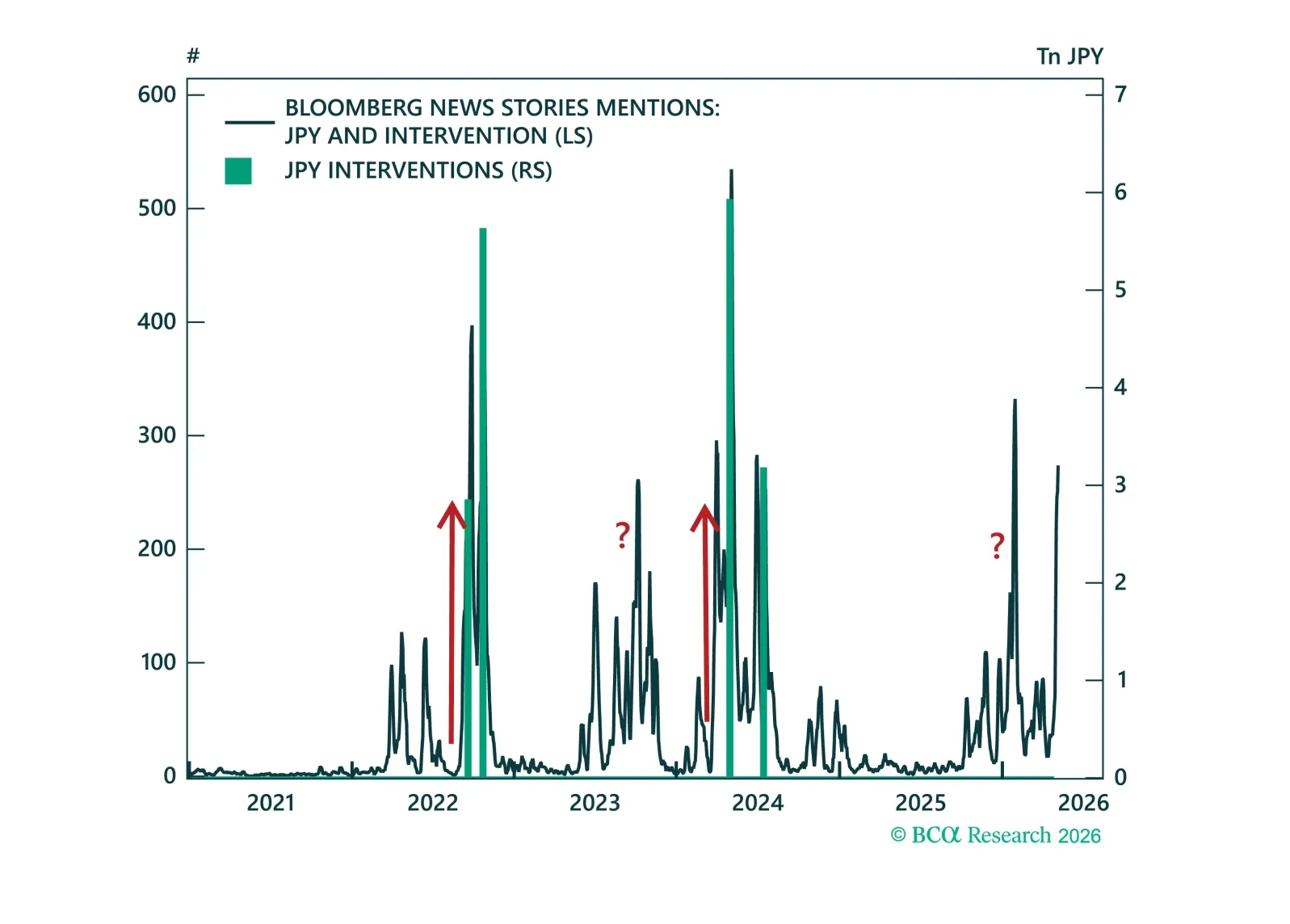

The dollar has had a strong run but its key supports from Fed repricing, positioning, and terms of trade are starting to fade. We close our tactical long USD positions and turn to short USD/JPY, where intervention risk makes yen shorts look increasingly dangerous.

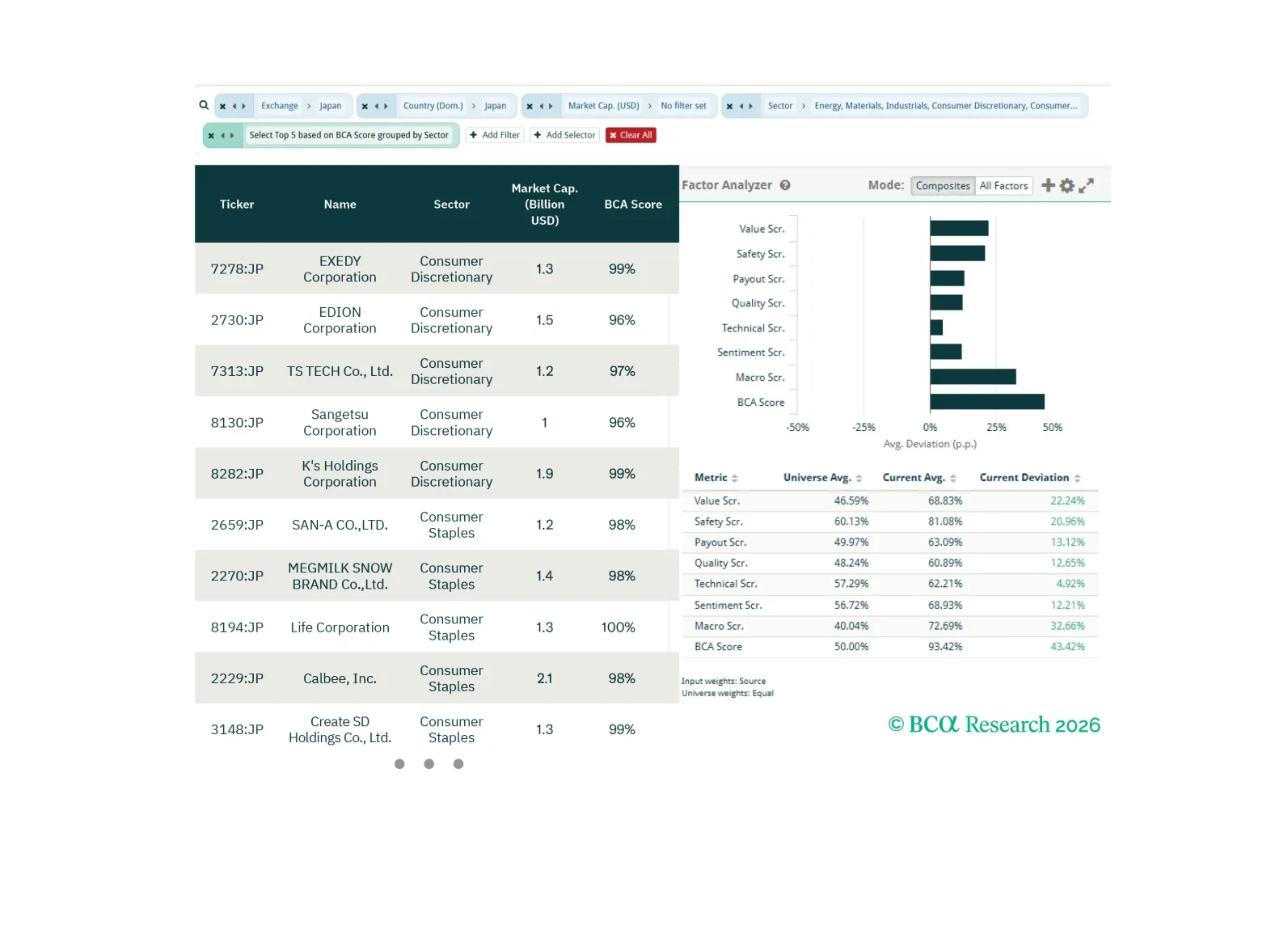

In this screener report, we explore opportunities in Japanese Non-TMT equities, El Niño hedges, and US consumer-facing equities.

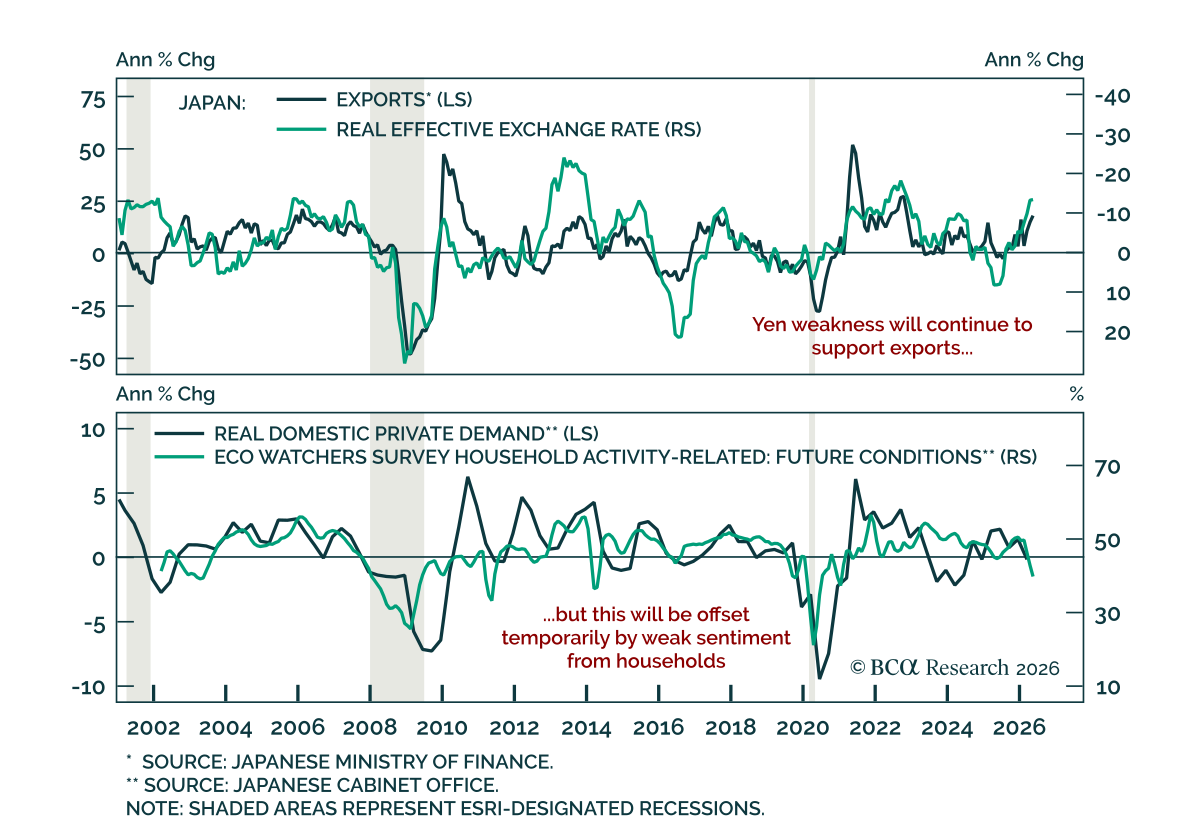

MoF FX intervention has drawn a line at 160, triggering a sharp yen squeeze. But with near-term fundamentals still stacked against the currency, USD/JPY remains poised to retest the highs before any durable turn.