Japan

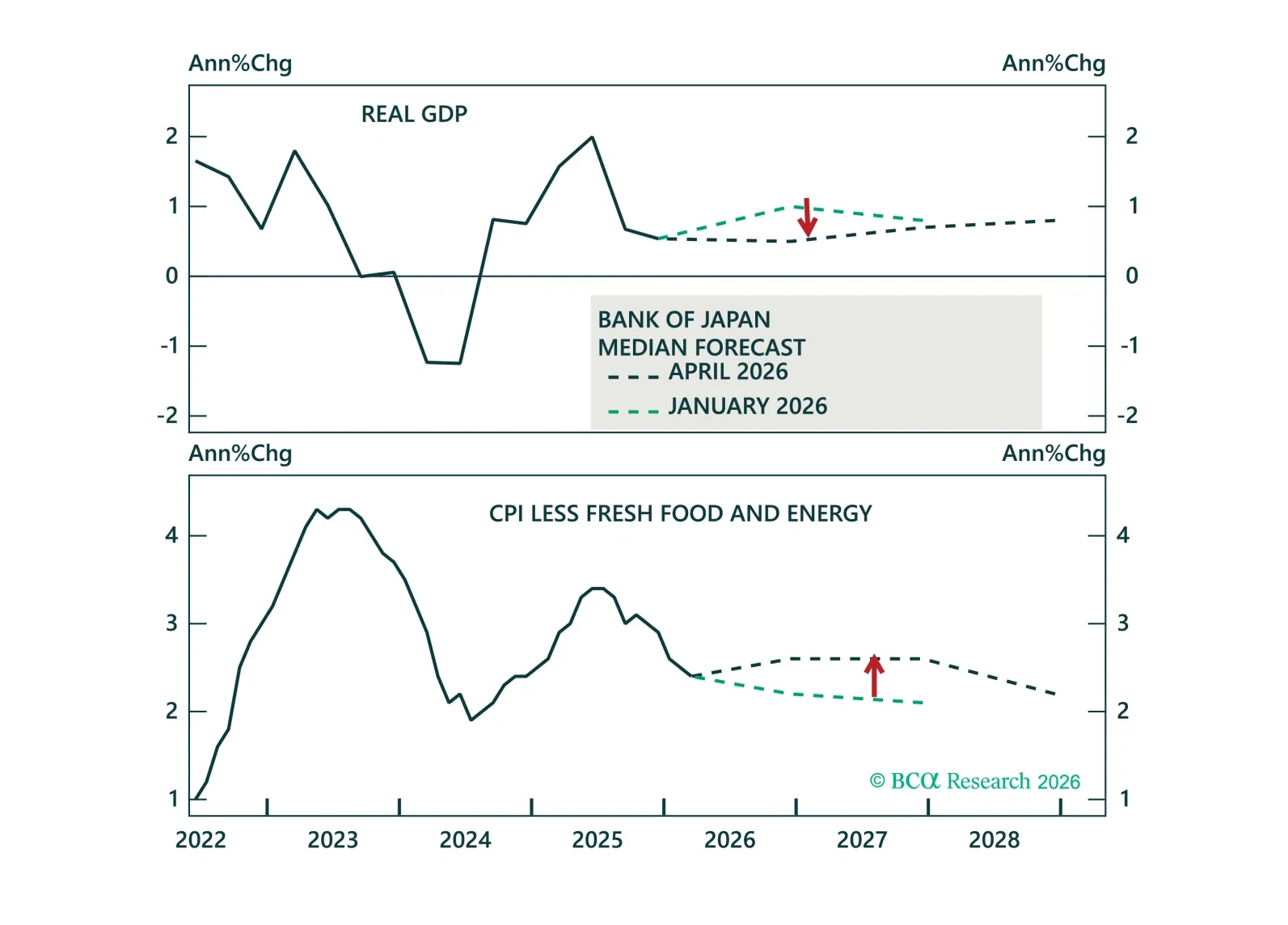

The Bank of Japan held rates at 0.75%, but the meeting still leaned hawkish. The hold was expected, but had a hawkish tone with 3 dissents in favor of a hike. That signal came alongside upward revisions to the BoJ’s inflation forecasts for 2026 and 2027, and…

The BoJ held rates overnight, but the direction of travel hasn’t changed. We discuss how stronger wages, rising inflation, and a weak yen point to further tightening ahead.

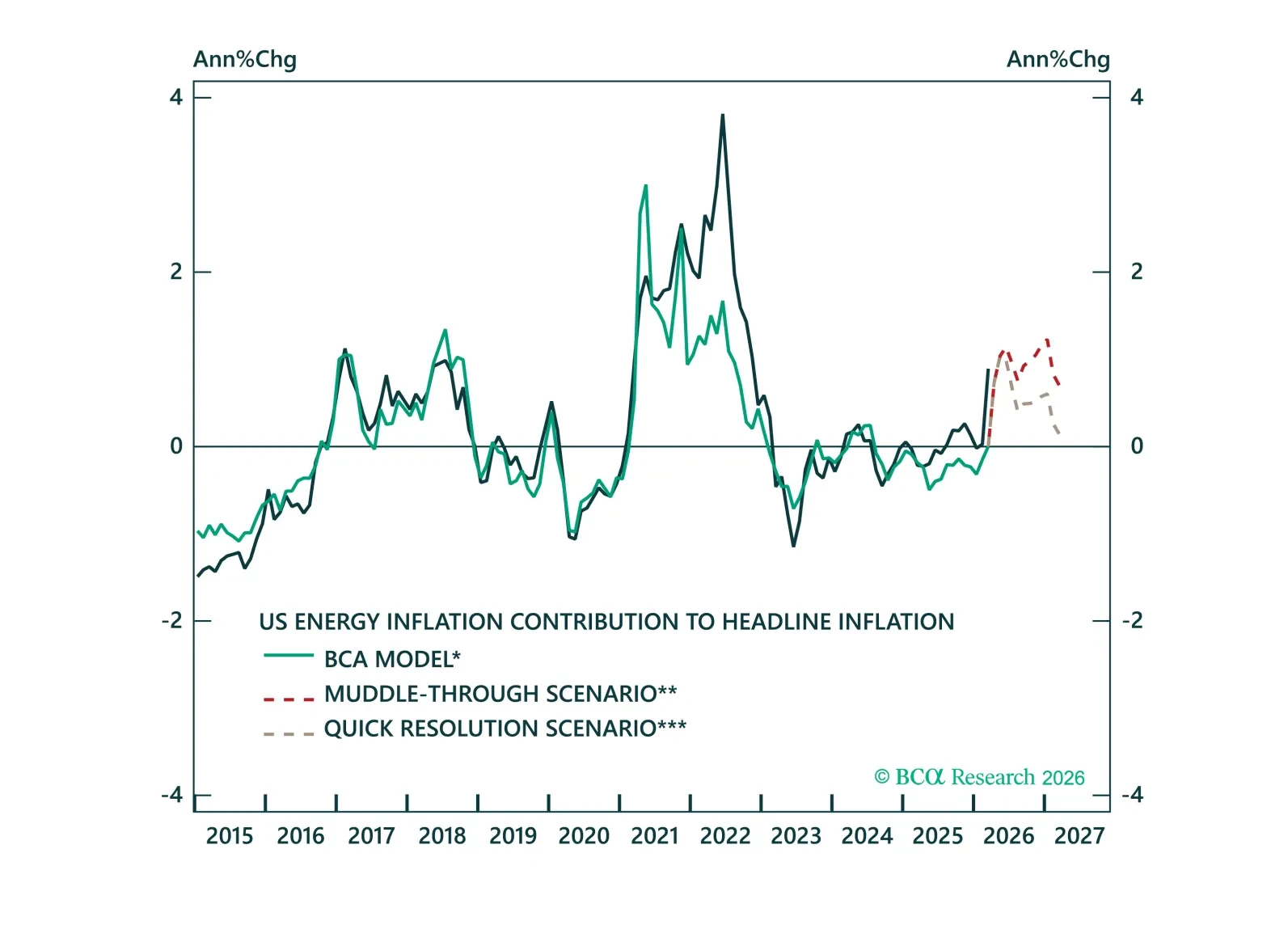

Volatility is high, but the path for yields is clearer than it looks. Across three oil scenarios, we show how policy responses shape fixed income markets and why the balance of risks still points to lower yields.

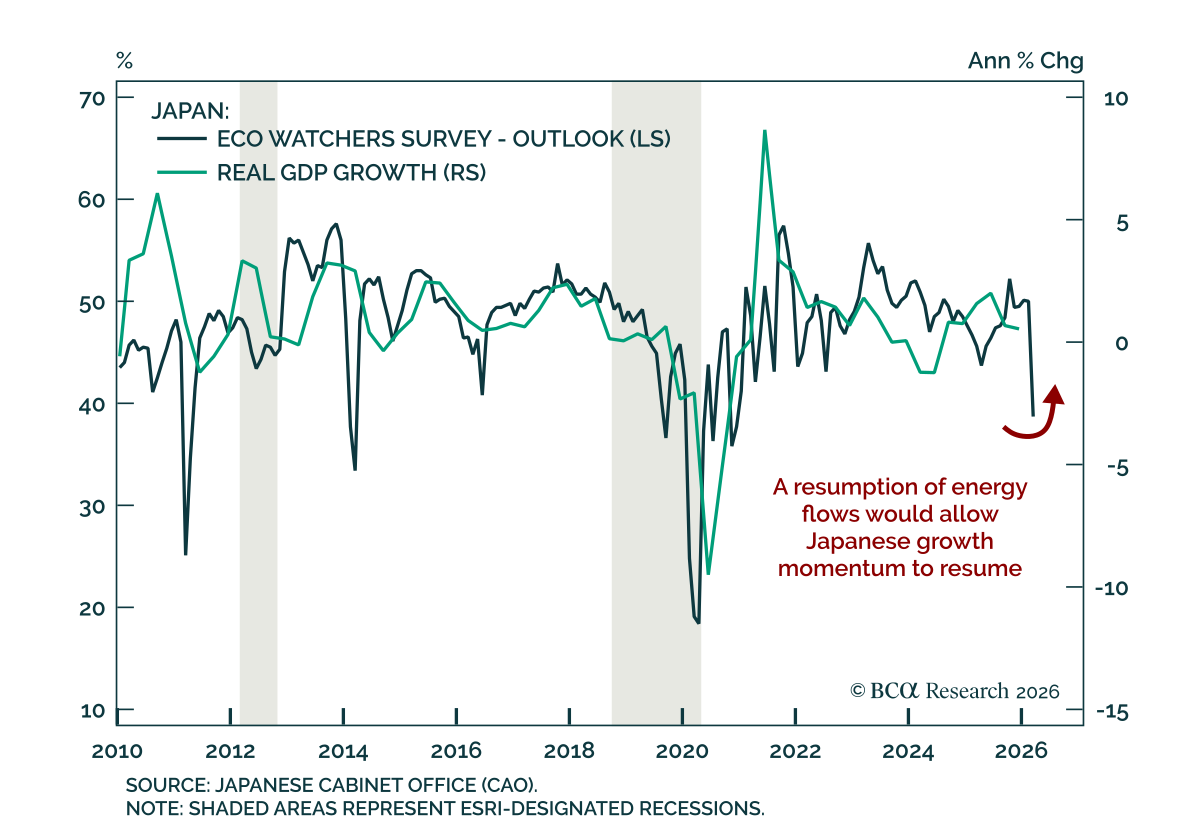

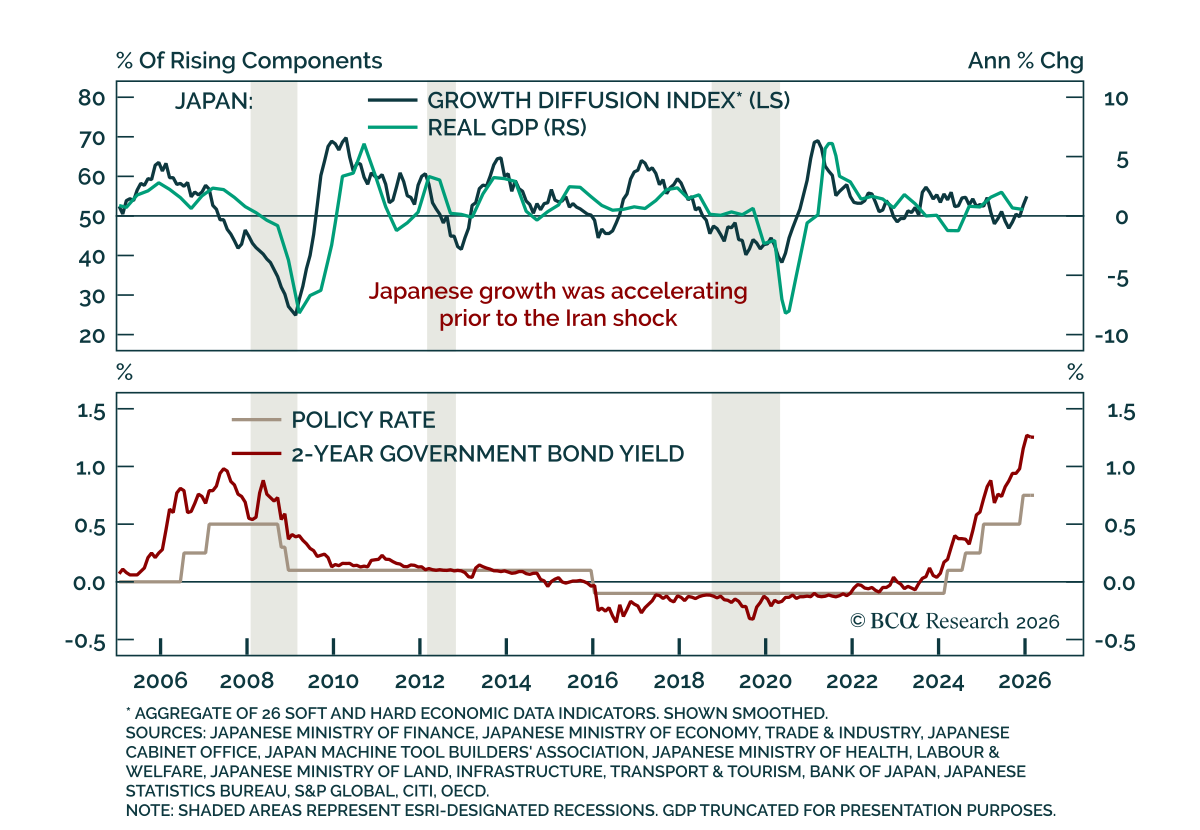

Japan’s March Eco Watchers Survey missed estimates, interrupting the improvement in momentum seen since last April. The current conditions index fell to 42.2 from 48.9, while respondents’ outlook plunged to 38.7 from 50. Improving momentum had been supported…

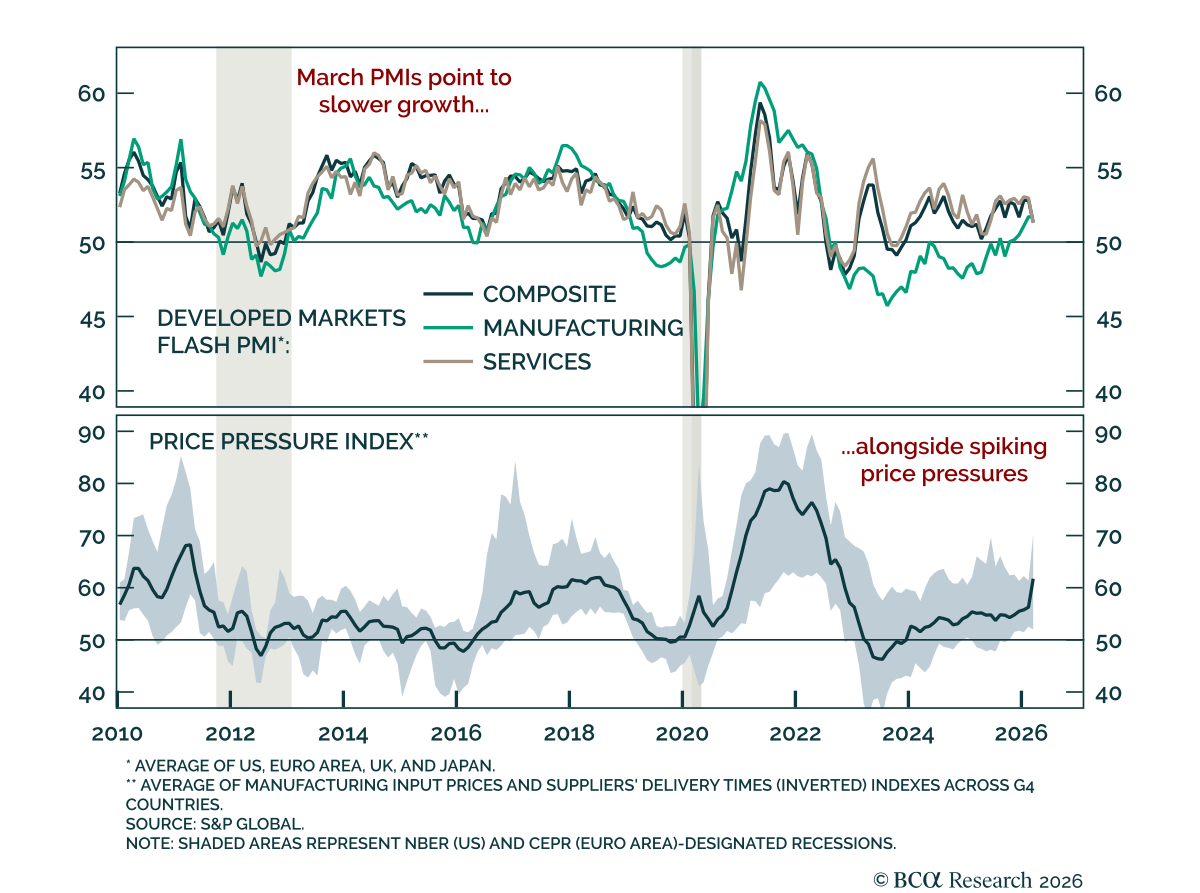

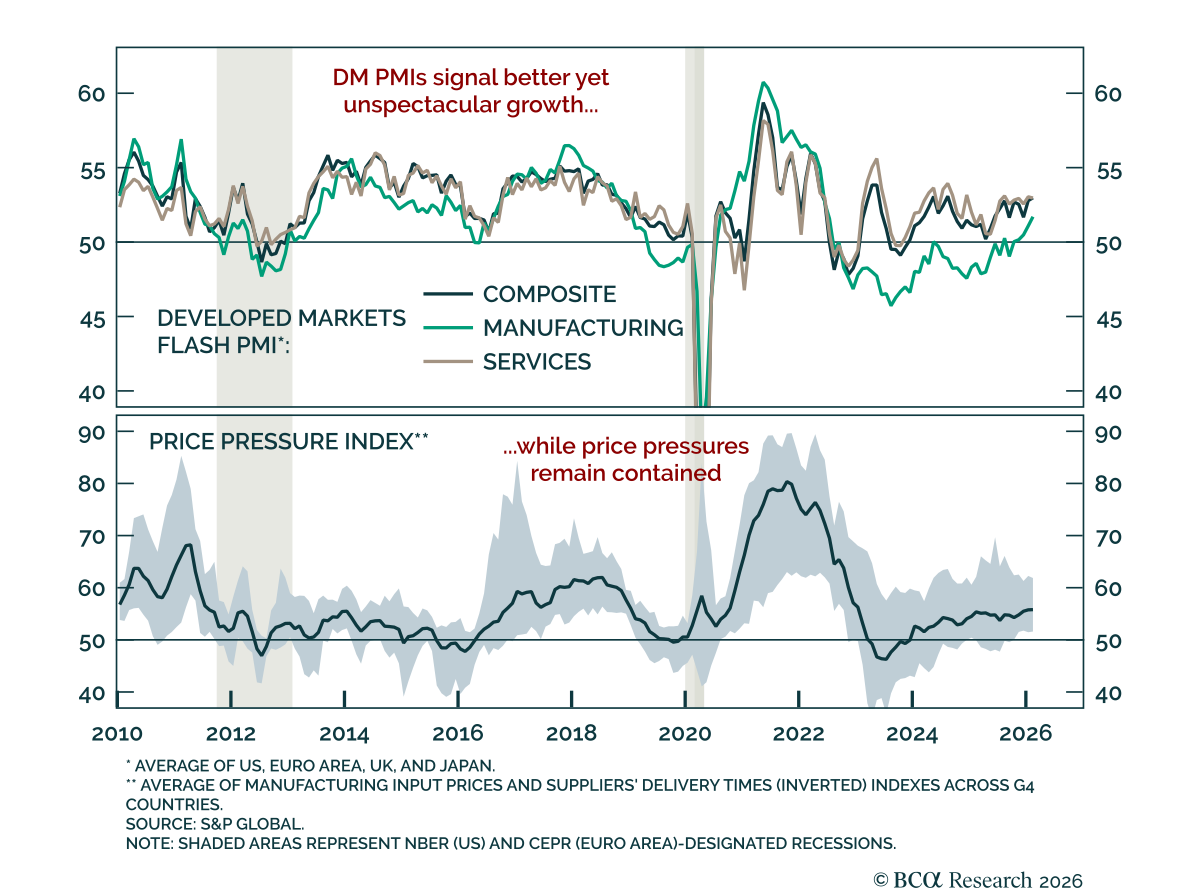

March flash PMIs point to rising inflation pressures, with the US more resilient than its DM peers. Input costs rose and delivery times lengthened across developed markets. Manufacturing was resilient, but services PMIs declined. The US PMIs pointed to…

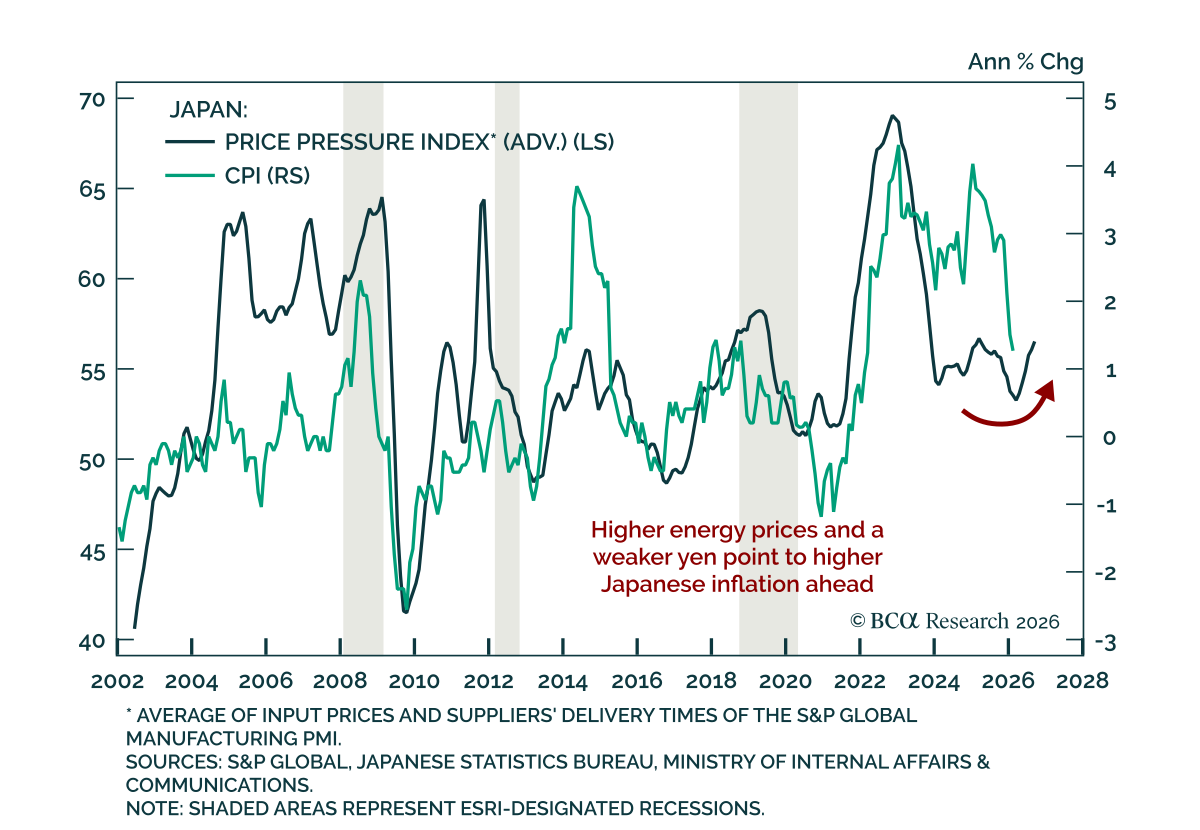

Japanese February inflation came in cooler than expected, but leading indicators still point to higher inflation ahead. Headline inflation ticked down to 1.3% y/y from 1.5%. Core measures also missed estimates, with ex. fresh food falling to 1.6% from 2.0%,…

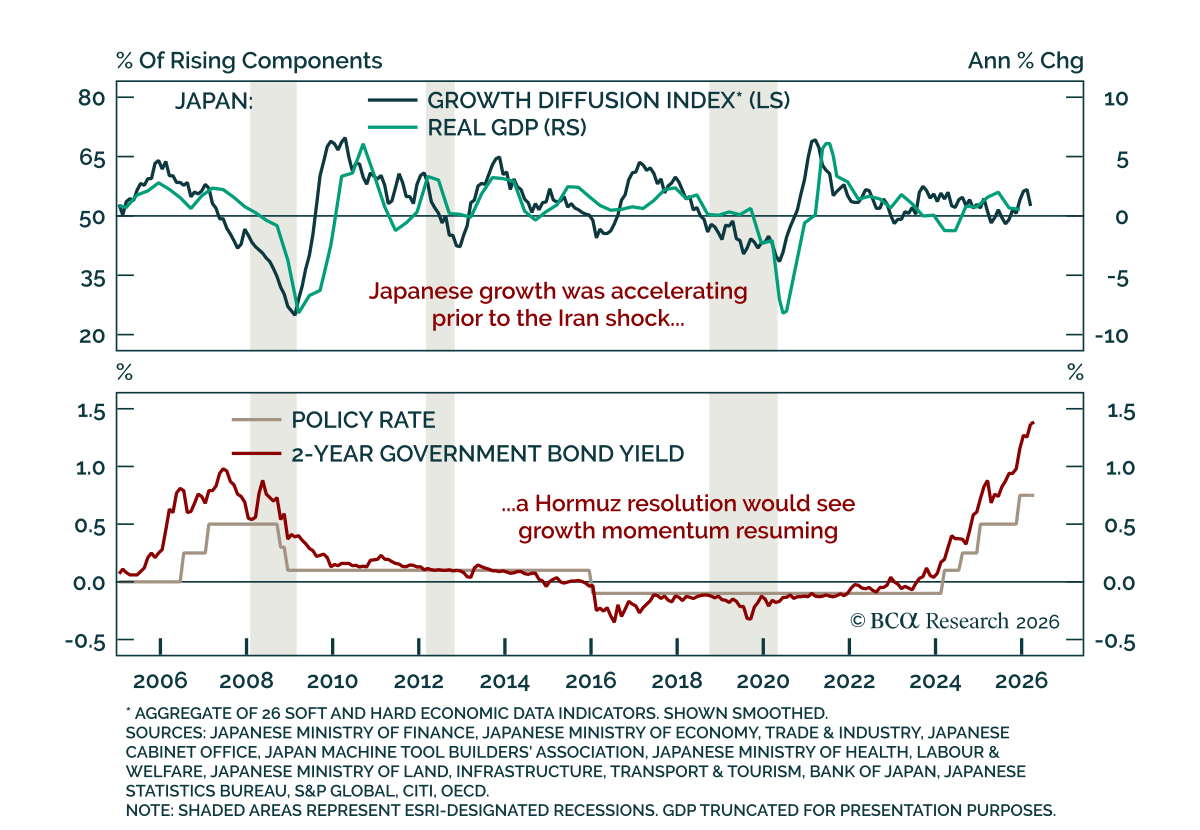

The Bank of Japan held rates but kept the door open to further hikes despite energy shock uncertainty. The policy rate was left at 0.75%, with Governor Ueda signaling that a temporary energy shock should not derail the underlying upward inflation trend. As…

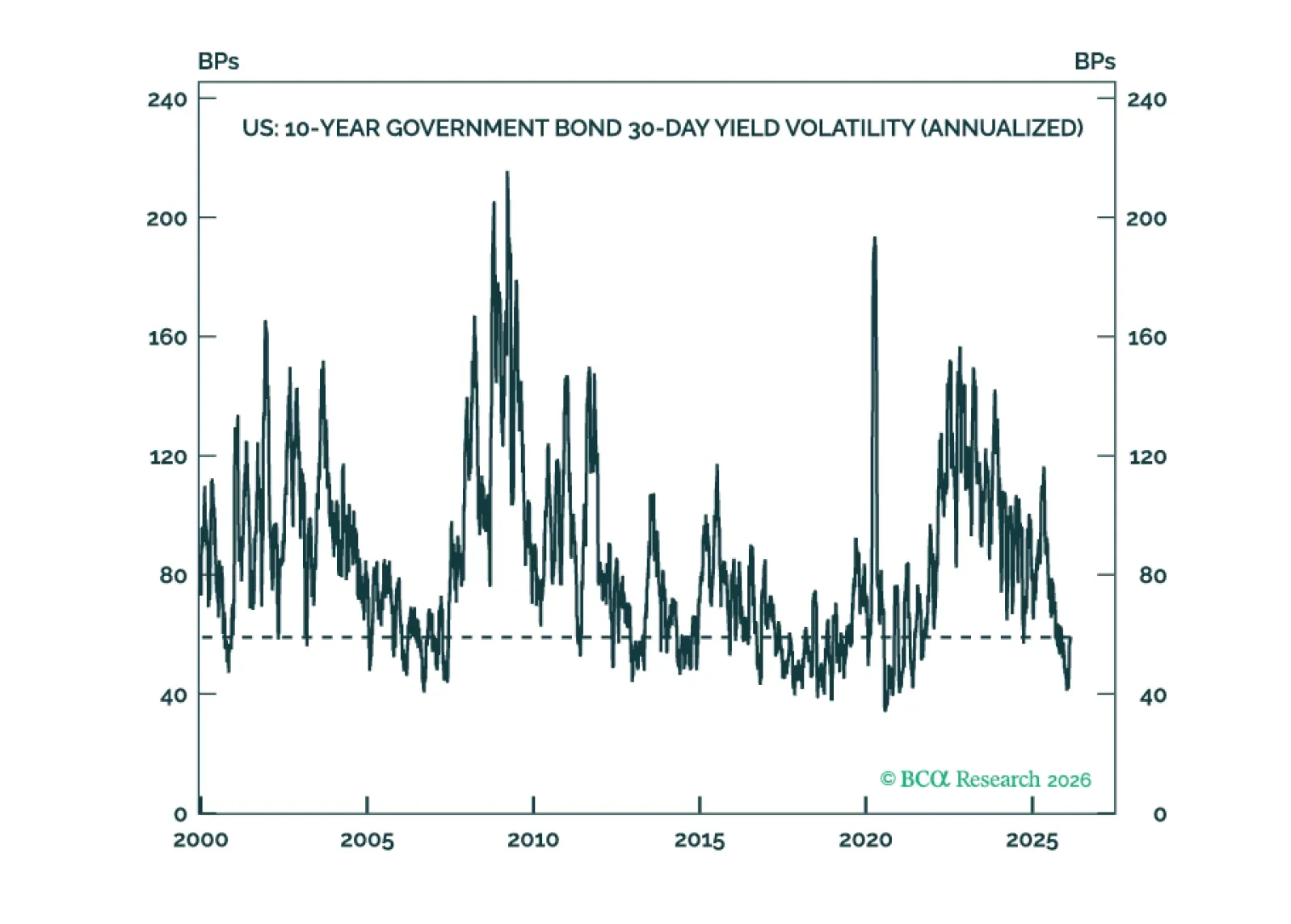

Interest rate volatility is very low across developed market fixed income. Investors should maximize the carry in their portfolios to outperform in a low rate vol environment.

February flash PMIs edged higher, pointing to gradual improvement in global growth. After moving mostly sideways through 2025, developed markets PMIs are picking up. Manufacturing is showing decent momentum, rebounding after being weighed down by trade…

Japanese stocks’ bull market has many more years to run, and it will extend to the JPY. The TOPIX’s negative correlation with the yen should thus fade, and a stronger JPY may increasingly coincide with rising Japanese equities. Investors often treat Japan as…