Japan

Global semiconductor stocks have returned 50% YTD in USD terms, and a whopping 200% since their September 2022 lows. However, they may have peaked back in July. Our Emerging Market strategists highlight a significant bifurcation between the revenues of…

Many currencies have registered sizable gains against the US dollar over the last two months. Most notably, the yen has been one of the best G7 performers since the greenback began depreciating. It now trades at 143 against the US dollar, marking a 11% gain…

Tokyo’s CPI is a timely leading indicator of nationwide price pressures. In August, the headline, core (ex-food) and the “core core” (ex-food and energy) measures all accelerated by larger-than-expected margins, reaching 2.6%, 2.4% and 1.6% y/y, respectively.…

Preliminary estimates suggest that with the exception of the UK (see Country Focus), manufacturing activity remains lackluster in DM economies. Manufacturing declined at a slower pace in Japan and Australia but the contractions unexpectedly accelerated in the…

Singapore is a small open economy sensitive to global trade dynamics. Its non-oil exports (NODX) are thus a good bellwether for global growth conditions. They rebounded sharply in July from a previous contraction, largely exceeding expectations. Notably,…

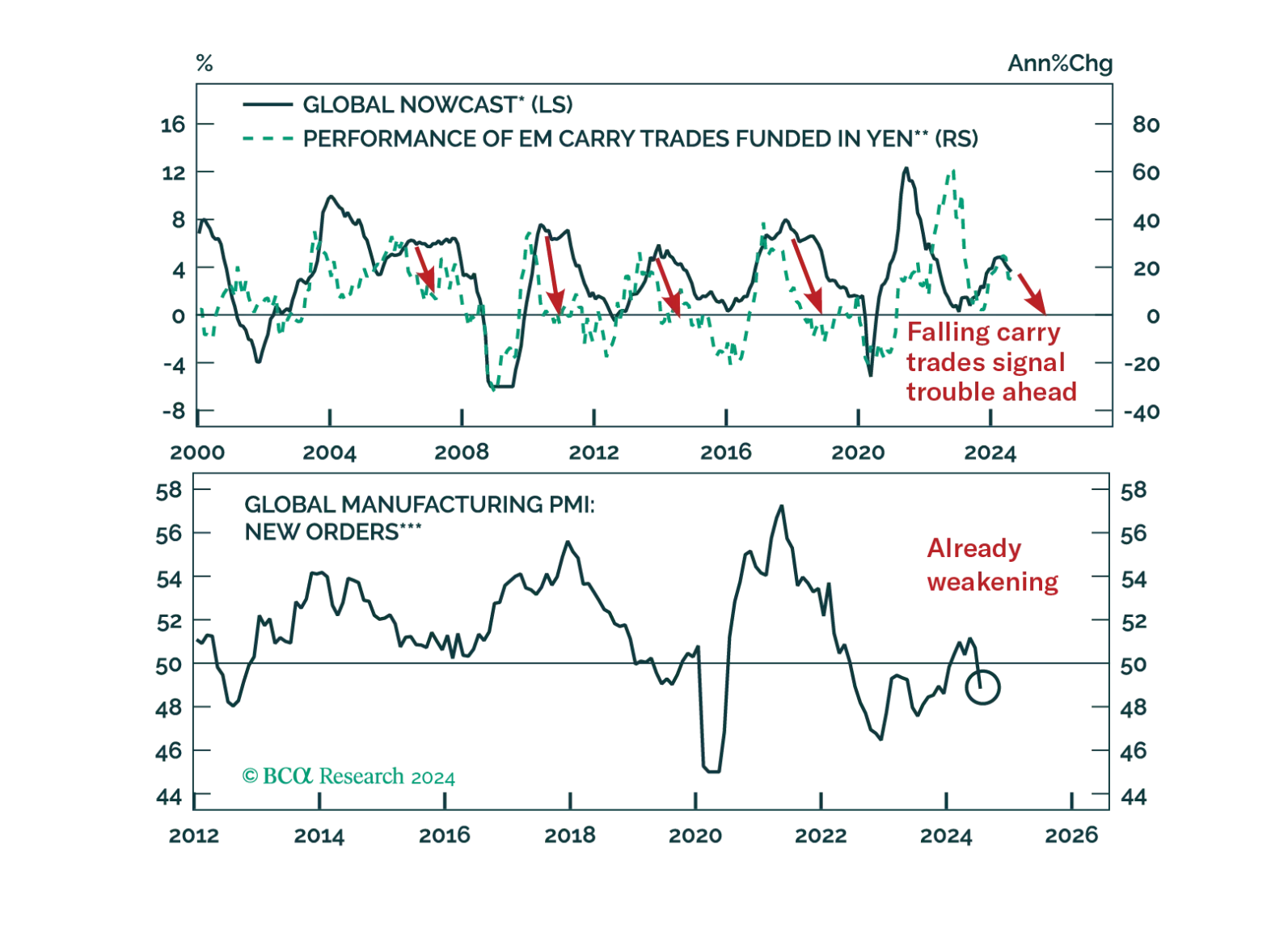

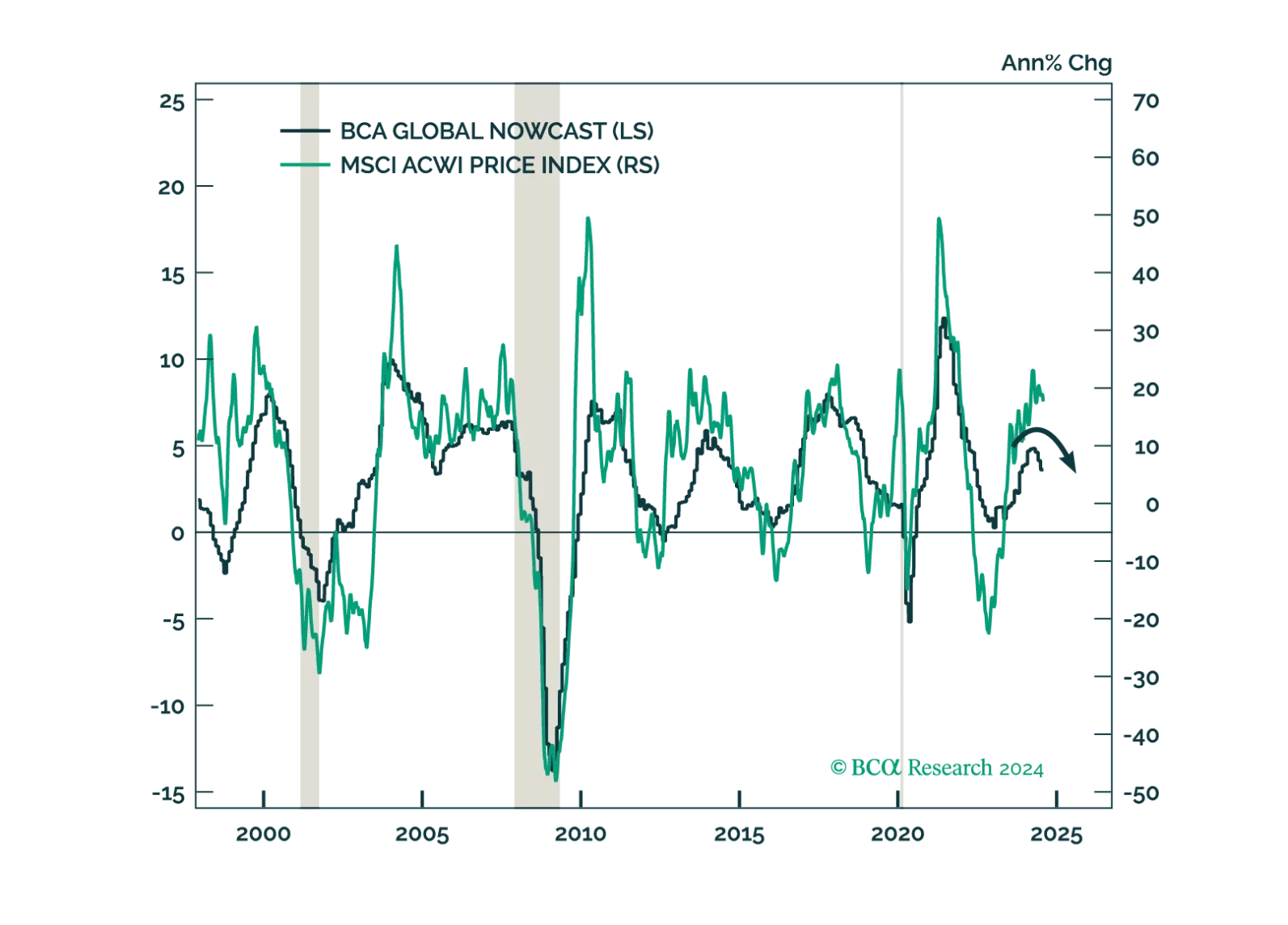

The unwind of yen carry trades caused violent tremors across the globe. Was this shock a one-off event or the prelude to more troubles?

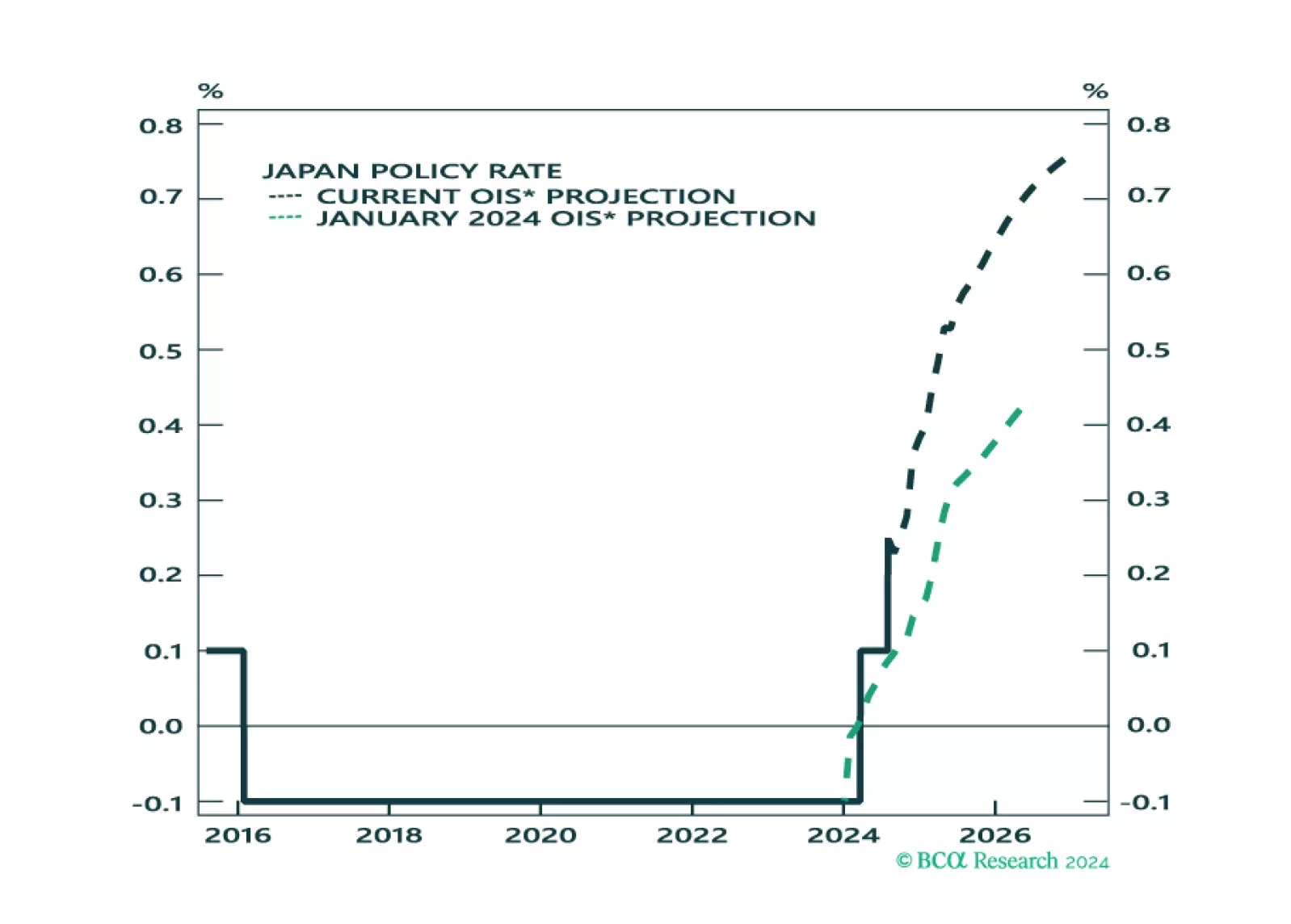

The BoJ delivered a surprise rate hike last week, then proceeded to sending a more dovish signal on Wednesday. Deputy Governor Shinichi Uchida strongly hinted at a central bank that would refrain from hiking further in times of market instability. The yen,…

The market is pricing in a soft landing, but we see growing signs that the global economy is faltering. Investors should be defensively positioned.

We assess the investment implications of the BoJ and Fed meetings, and give our take on the next policy moves. We also assess the impact on asset markets.

The Bank of Japan hiked its policy rate by 15 bps from 0.10% to 0.25% on Wednesday, and announced further quantitative tightening, reducing its pace of monthly bond buying from JPY 6 trillion to JPY 3 trillion. While the central bank had previously…