Japan

In a largely expected move, the Bank of Japan kept its policy rate unchanged at 0-0.1% in June. It maintained the pace of bond buying at JPY 6tr per month but signaled it would lay out a plan to reduce its balance sheet next month, without offering any…

The Bank of Japan exited negative interest rate policy in March, but subsequent softer-than-expected CPI inflation prints have complicated its path towards tightening. The central bank is widely expected to stay put when it meets this week. Governor Kazuo…

In this report, we gauge the outlook for the dollar given client visits in Africa.

Our Global Investment strategists highlighted back in November 2022 that structural deflationary forces in Japan were weakening, thus setting the stage for inflation to make a historic comeback in Japan. About a year later, they highlighted that 2024…

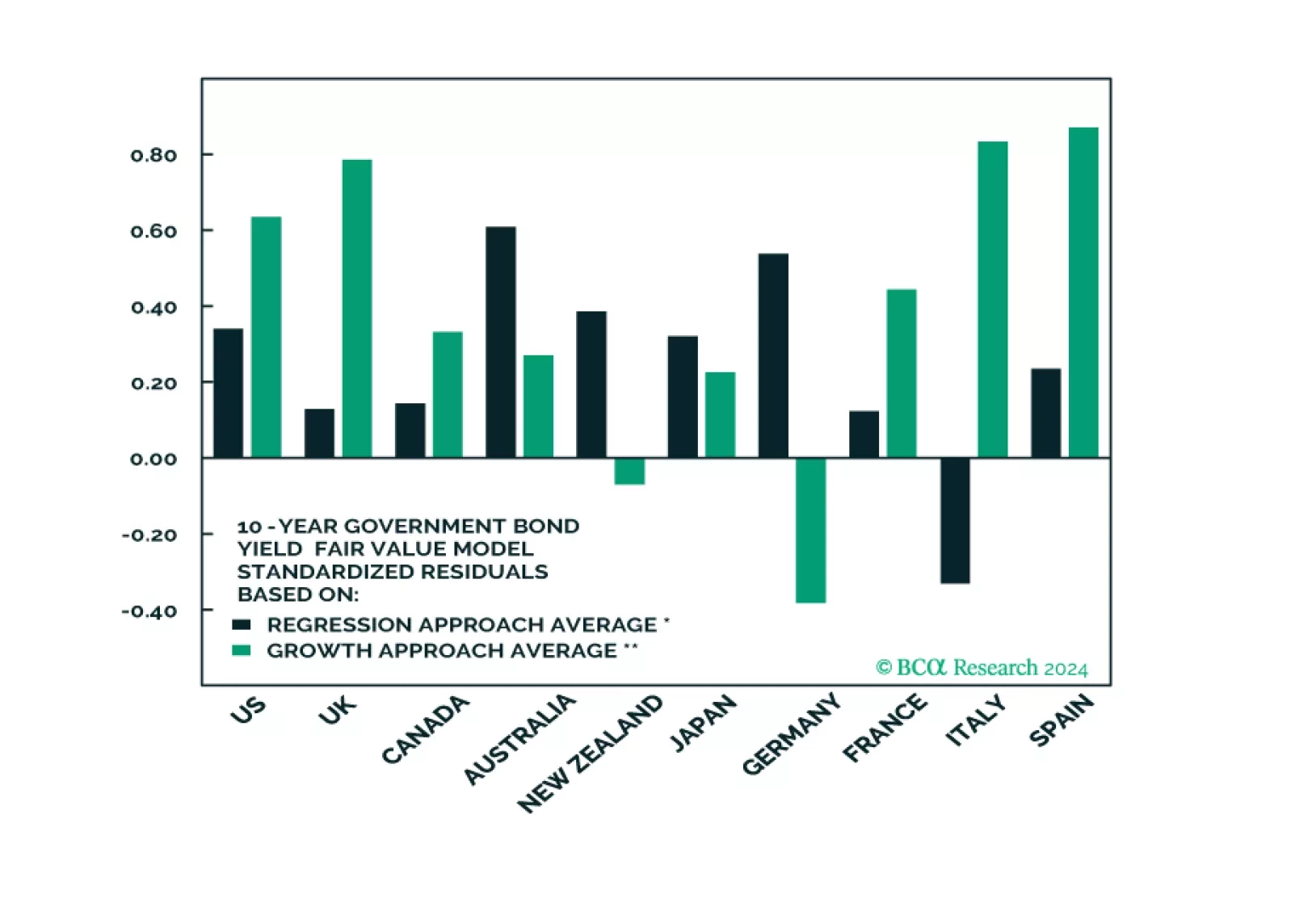

In this Special Report we assess the absolute and relative attractiveness of developed market government bonds using several fair value models. Longer-term investors who are focused on value should overweight US long-maturity bonds, and favor Spanish, Australian, and potentially UK government bonds within a DM ex-US allocation.

The Bank of Japan’s Economy Watchers Survey – a gauge of sentiment among business owners – disappointed in April. The Current Conditions and the Outlook indices deteriorated from 49.8 to 47.4 (20-month low) and from 51.2 to 48.5 (16-month low), below…

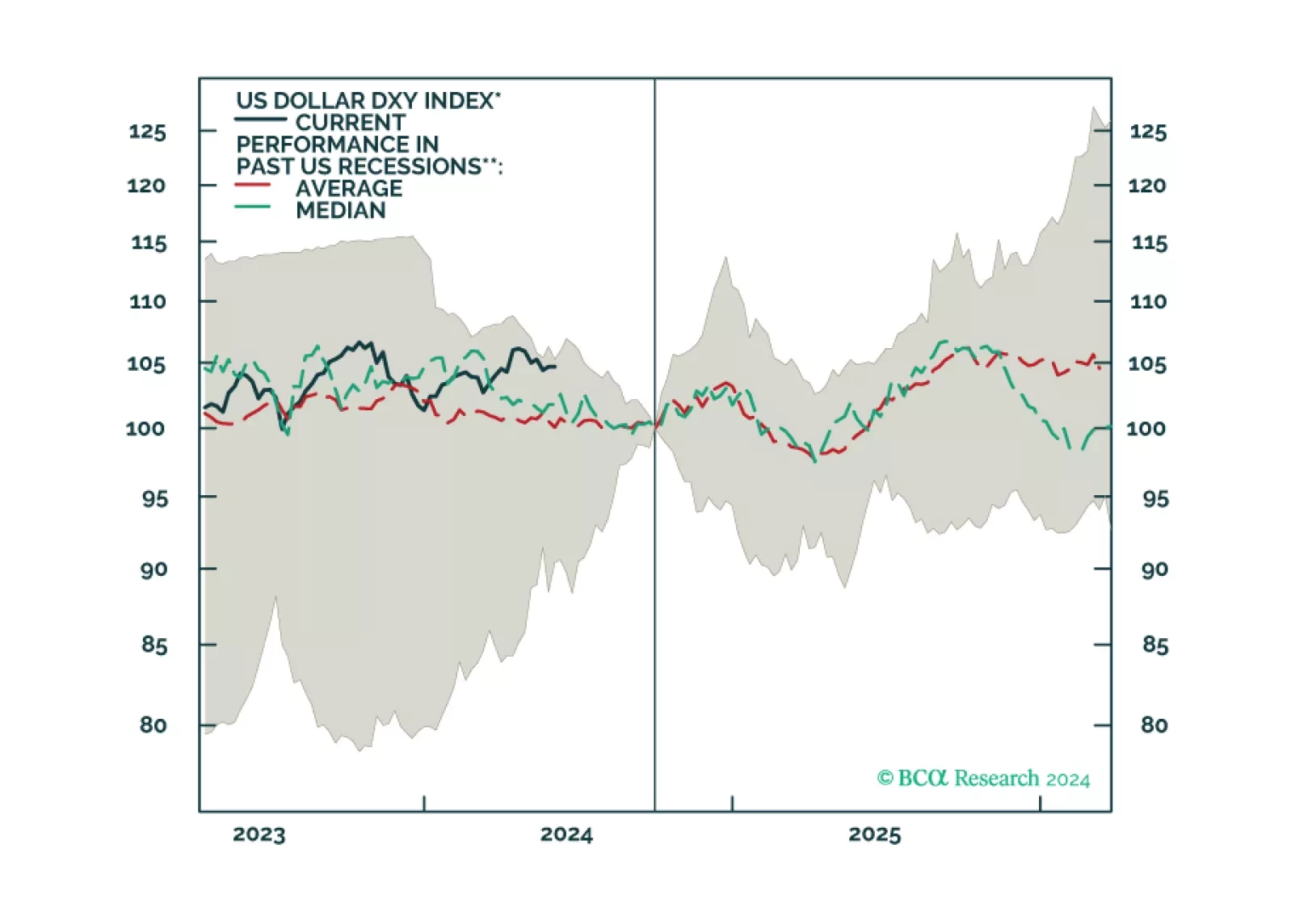

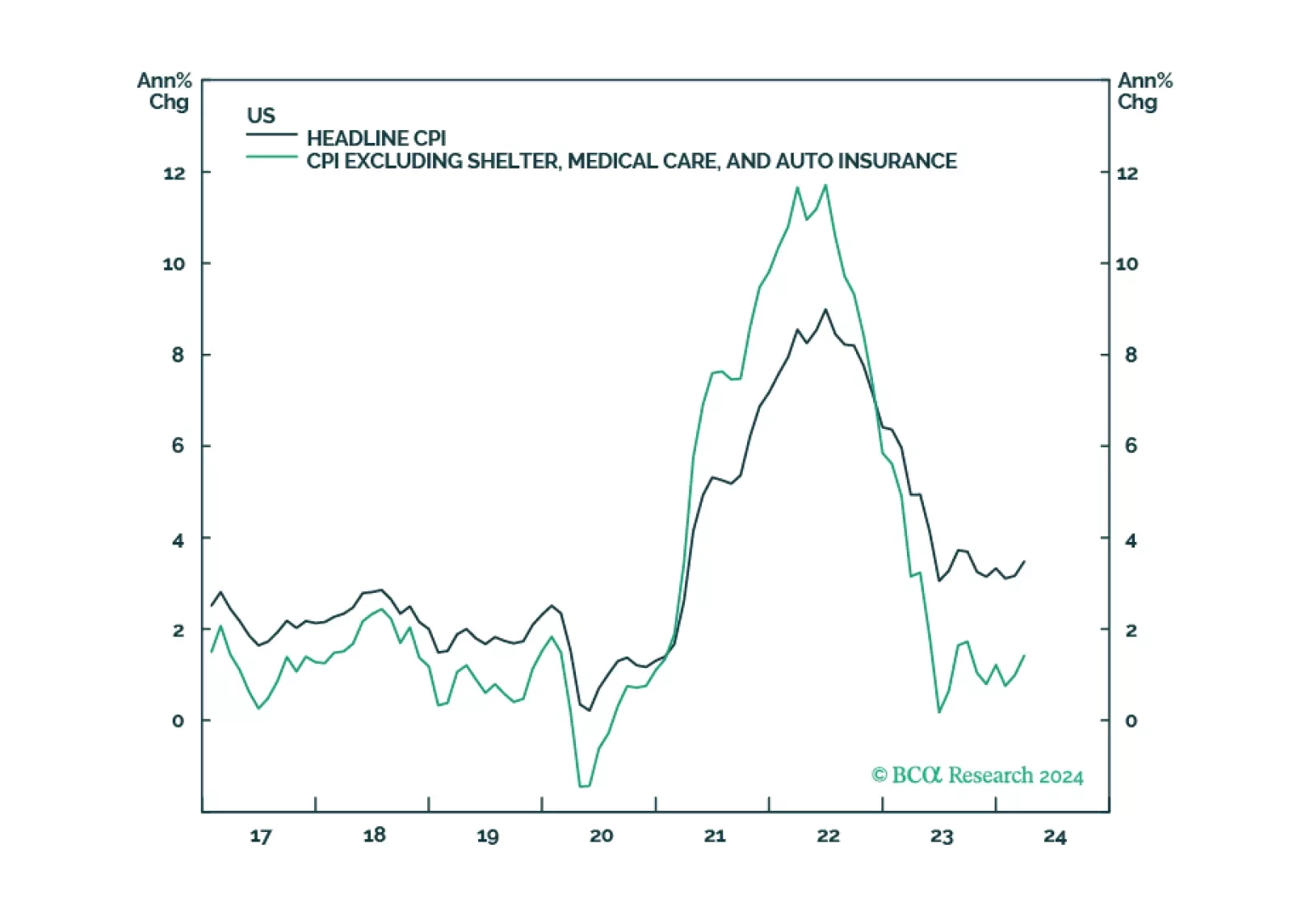

In this week’s report, we defend four out-of-consensus claims. Claim #1: Underlying inflation in the US is not reaccelerating. Claim #2: The US labor market is set to weaken abruptly. Claim #3: The S&P 500 will drop to 3700 in 2025. Claim #4: Japan is not in danger of a currency crisis.

The Tokyo inflation release for April came in on the soft side on Friday, with every single metric coming in below expectations. Tokyo headline inflation declined from 2.6% y/y to 1.8% y/y, versus expectations of a much more muted decline to 2.5% y/y.…

USD/JPY has appreciated by over 10% so far in 2024, making the yen the worst performing G10 currency year-to-date. This cross has also surpassed the 150 threshold which historically is the level at which the Bank of Japan begins to intervene. Today, it stands…

Japan’s national CPI inflation unexpectedly cooled in March, falling to 2.7% y/y versus consensus estimates it would remain at 2.8% y/y. Notably, measures of underlying inflation such as core CPI (ex-fresh food) and “core-core” CPI (ex-fresh food and energy)…