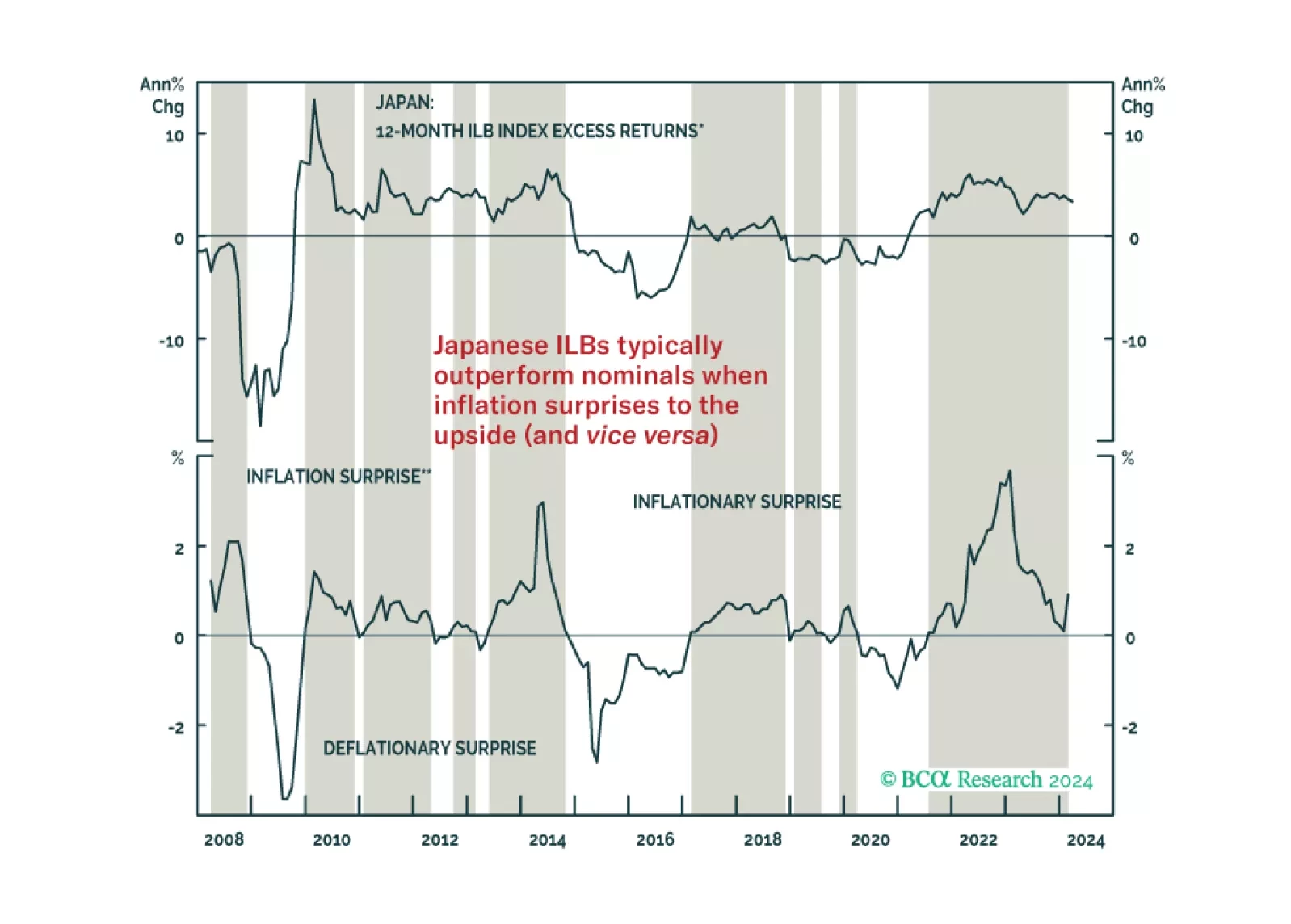

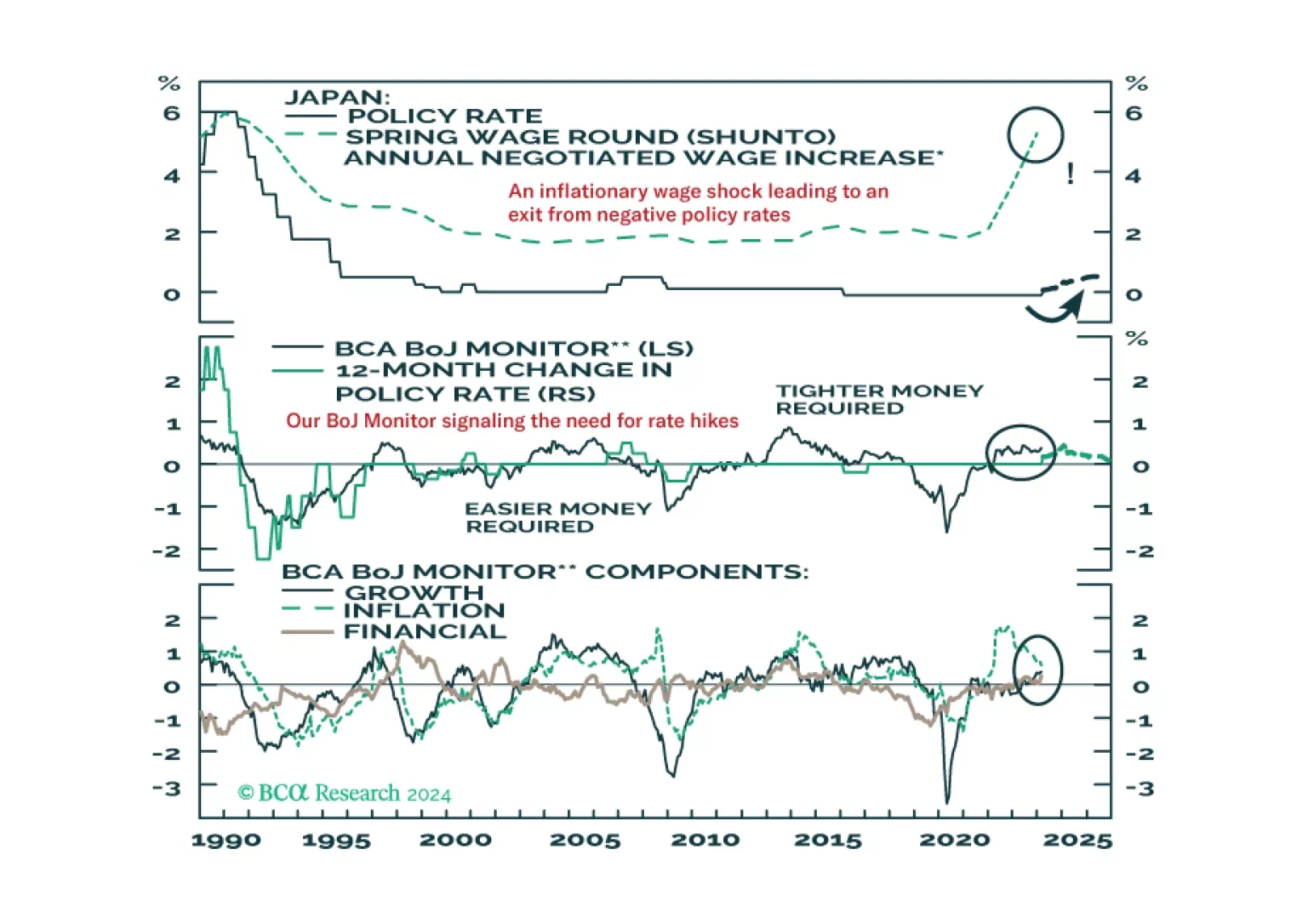

Japan

The global economy is wobbling precariously between slowing growth and reaccelerating inflation. This is unlikely to end well. Stay cautious, and hedge against both recession and inflation.

In this Insight, we continue our series of reports outlining investment frameworks for inflation-linked bonds in the developed markets, this time focusing on Japan. Our Japanese Inflation-Linked Golden Rule suggests that investors should overweight Japanese inflation-linked bonds versus nominal JGBs on a strategic (6-12 month) investment horizon. Our new Japanese inflation models suggest that there is a material risk that Japanese inflation exceeds the current level of market-based inflation expectations over the next year.

The Bank of Japan delivered a historic policy adjustment this week, ending both negative interest rates and Yield Curve Control. In this Insight, BCA’s global fixed income and currency strategists discuss the immediate implications of the move for Japanese bond yields and the yen, and the potential for additional tightening actions.

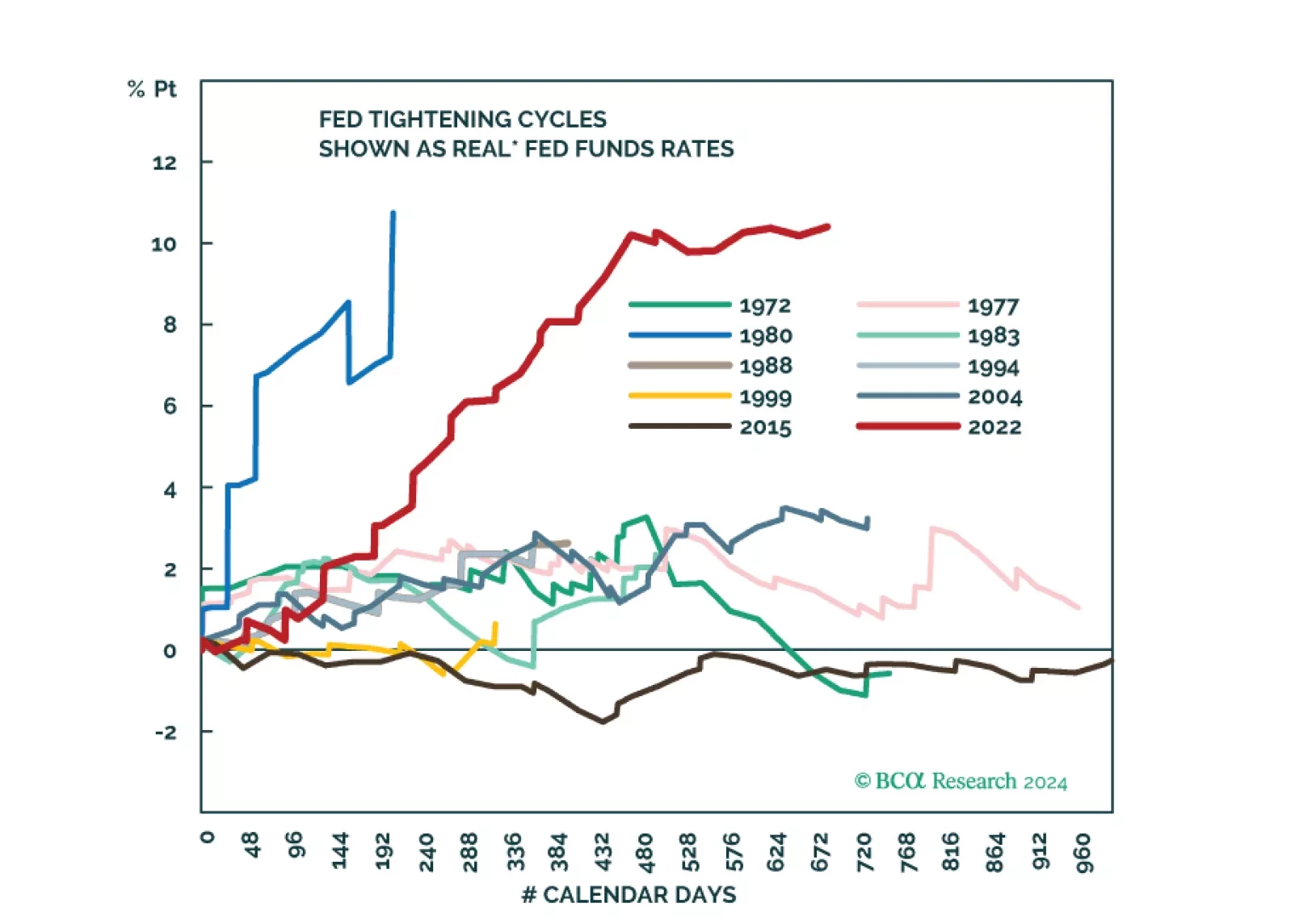

Amid patchy global growth, the US economy remains resilient. However, tight monetary policy will eventually trigger a recession in the US too. The stock market rally has been very narrow. Stay underweight risk assets.