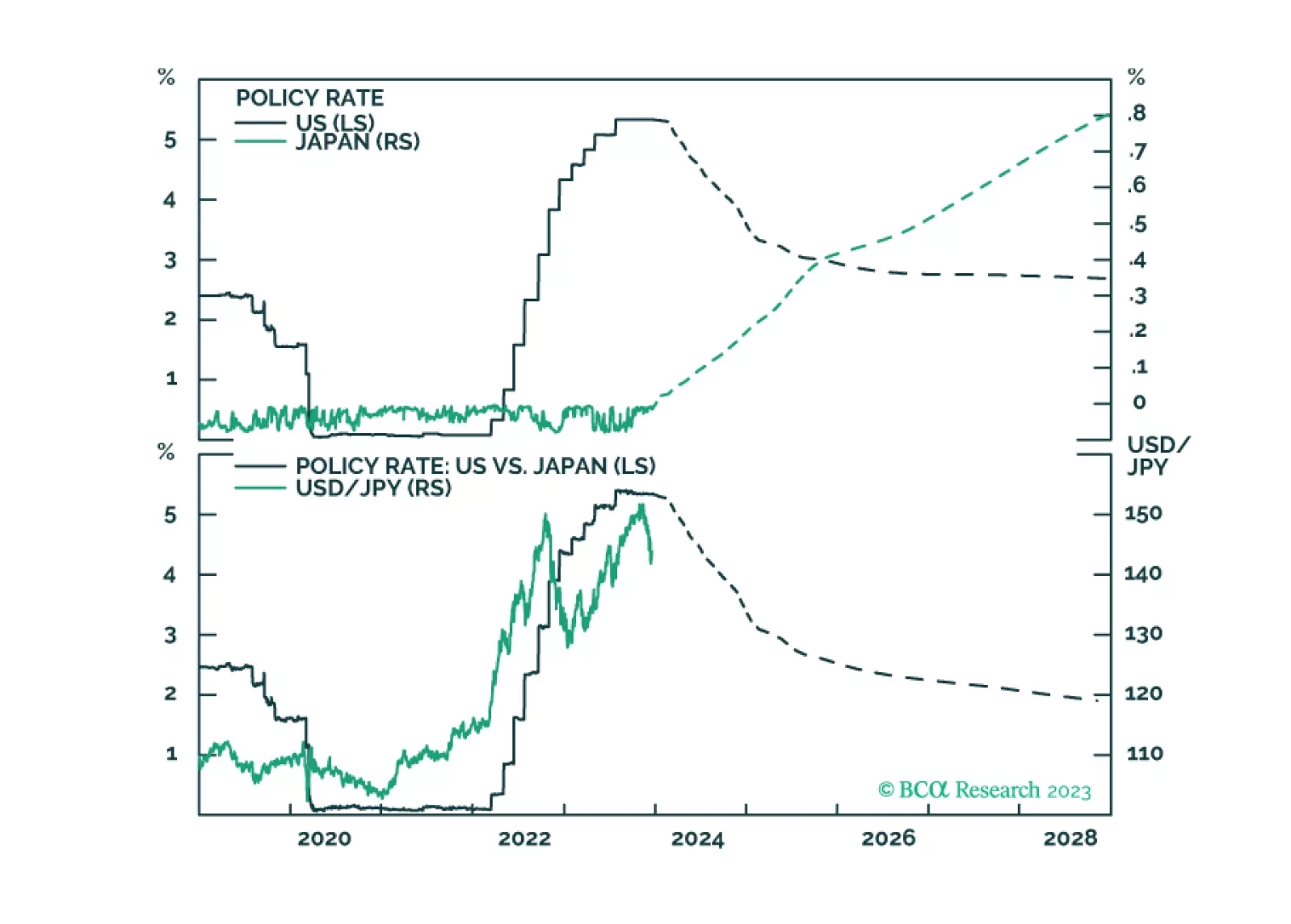

Japan

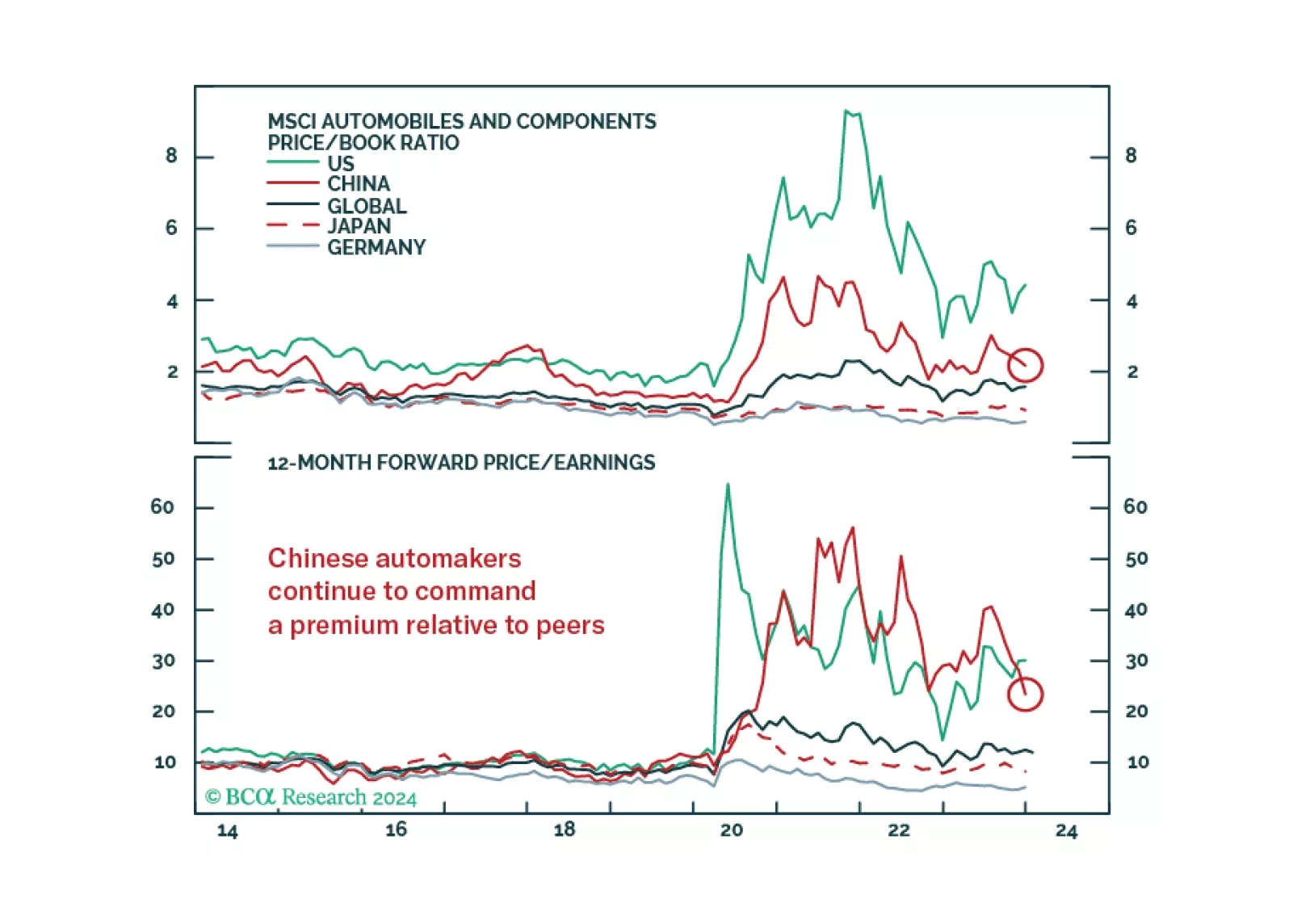

The expectation that China is best placed to win the global EV race presumes the persistence of the status quo. Reality, however, may differ as the sector looks set to be hit by a range of changes. If nonlinearity were to emerge in the global auto sector, as it often does, then the EV transition could end up spawning a very unexpected list of winners and losers.

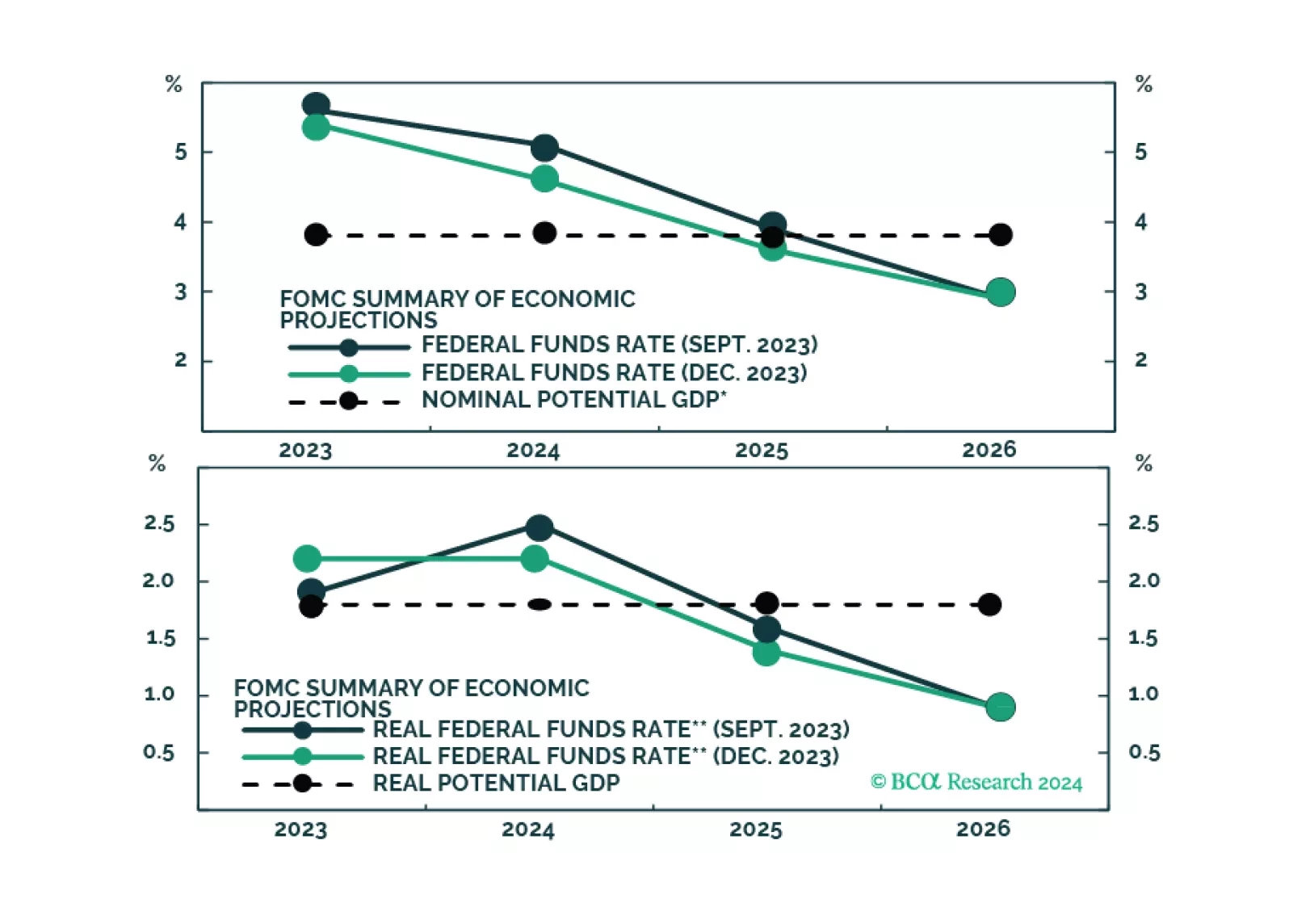

The market is excited by the idea that the Fed will cut rates early this year, even without a recession. But is that likely, with inflation still set to be around 2.8% mid-year?

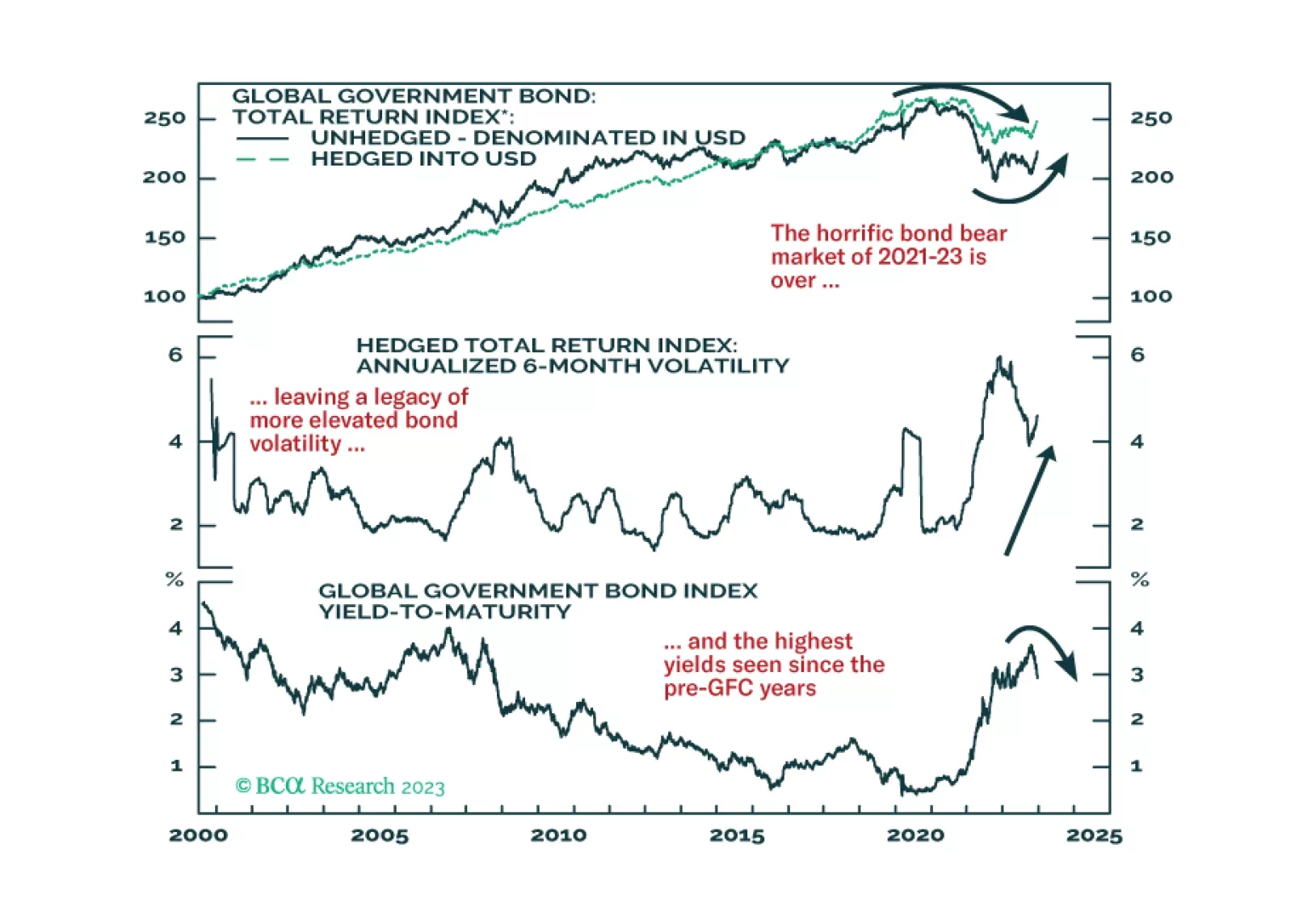

In this, our final report of the year, we present our main global fixed income investment themes and recommendations for 2024.

A post-mortem of our trades for the year, and also comments on future yen and sterling moves from the recent BoJ meeting, and the UK inflation report.

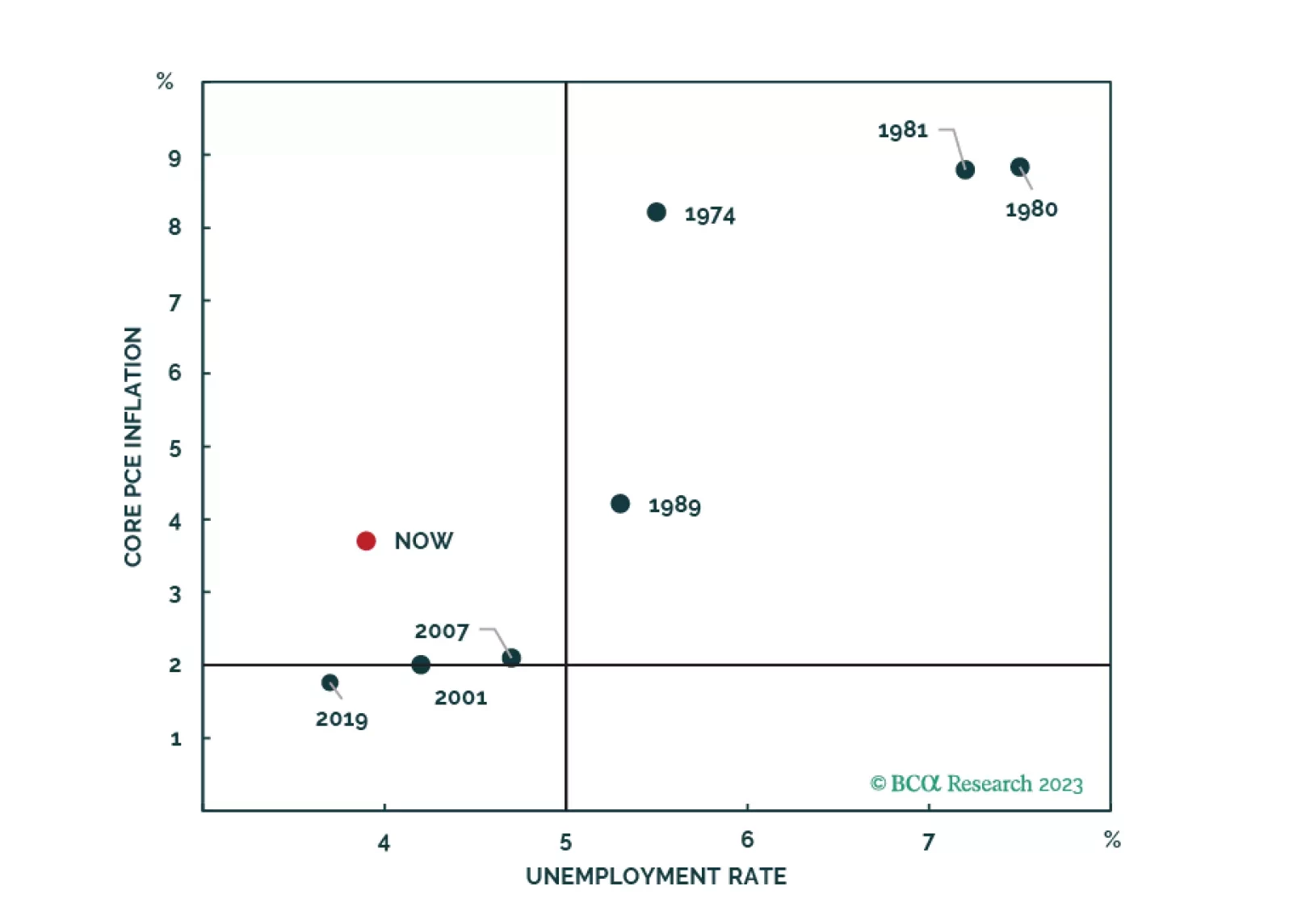

Global Investment Strategy predicted the surge of inflation in 2021/22 and the immaculate disinflation of 2023. Now their unique framework is predicting a recession in the second half of 2024.

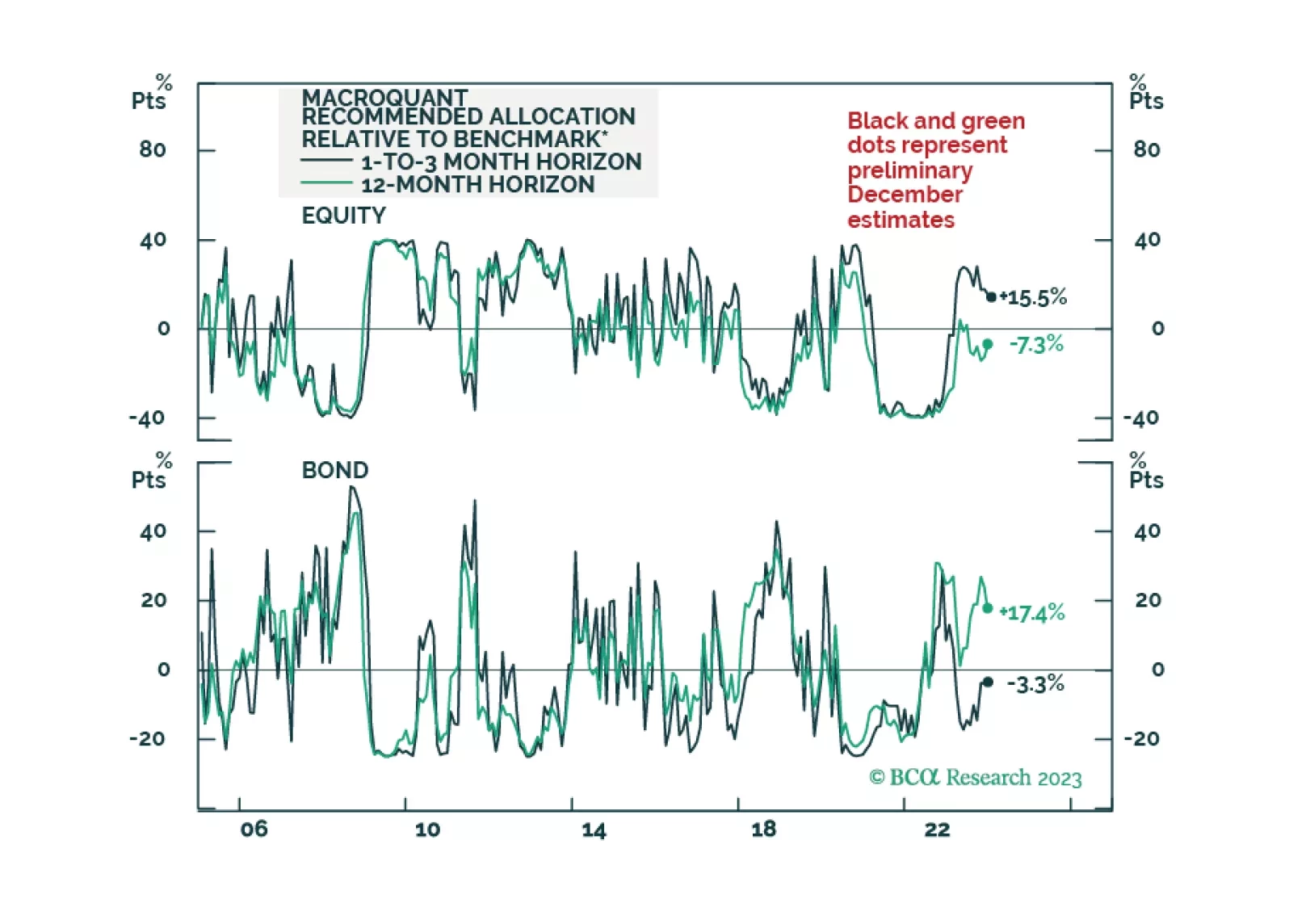

Inflation won’t fall fast enough for the Fed to cut rates preemptively before recession arrives. The risk/rewards balance is unfavorable for risk assets. Stay overweight bonds versus equities.