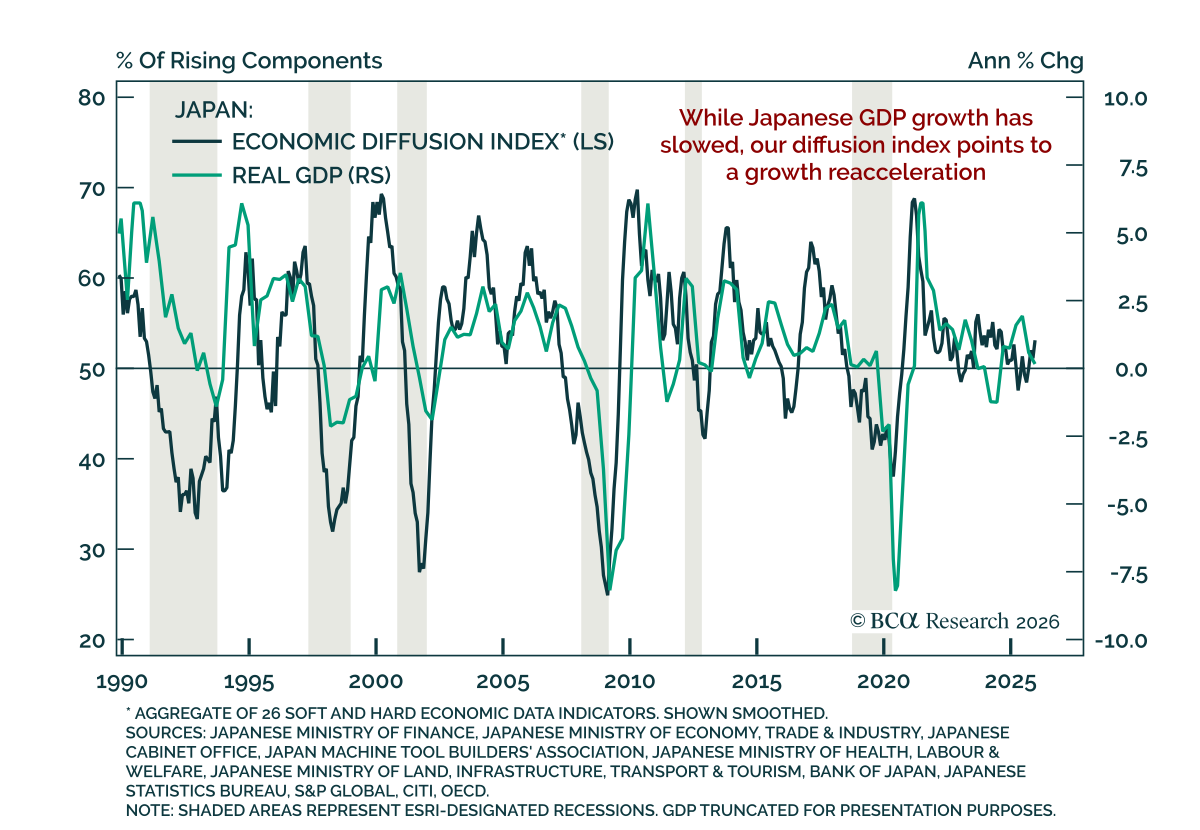

Japan

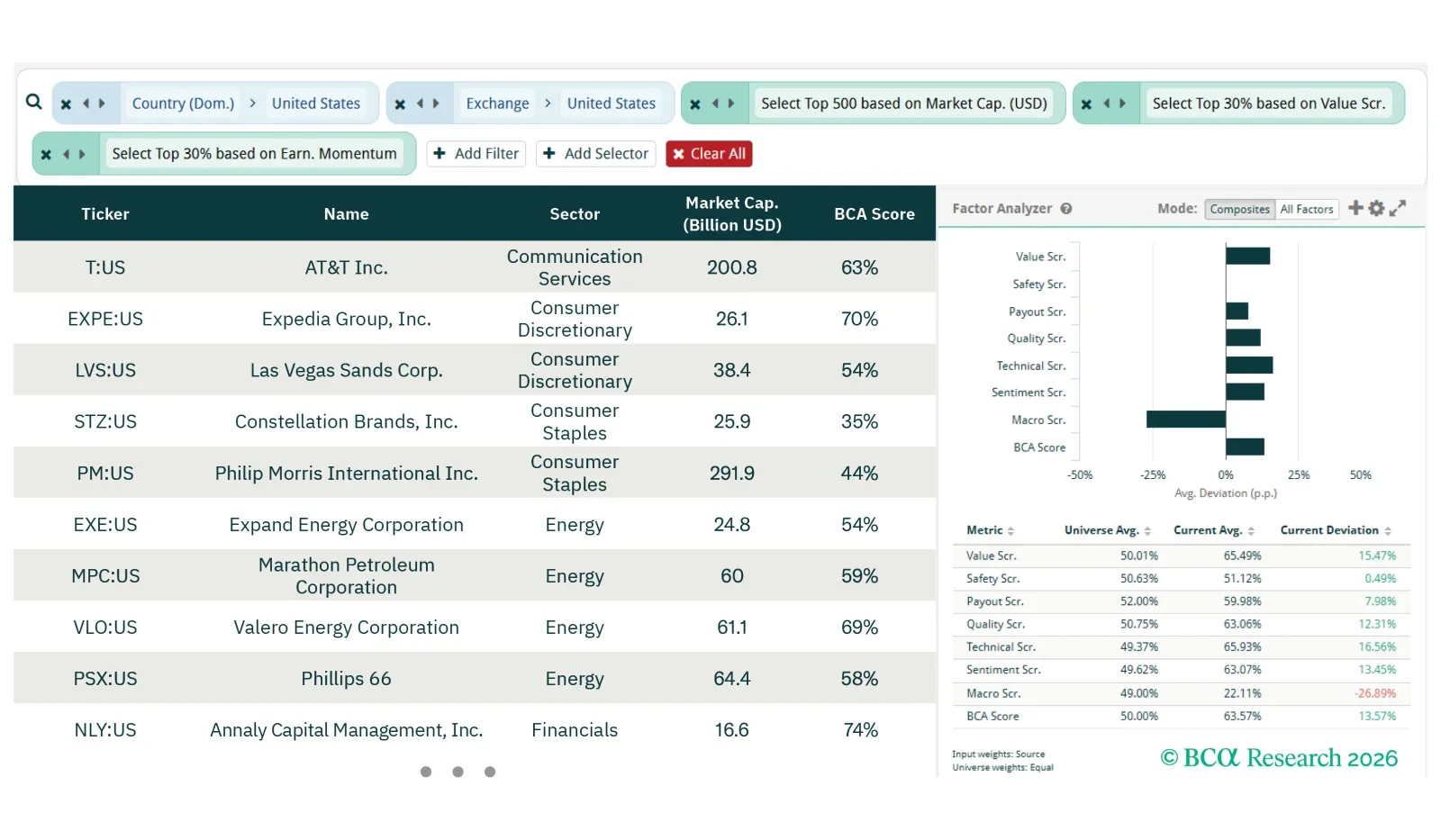

For this screener report, we explore opportunities in laggards with earnings momentum, Japanese semiconductors and US rate-sensitive stocks.

We spent last week meeting investors in Switzerland. This Strategy Insight revisits the most prominent topics we discussed, including repatriation fears, SNB intervention, and Dutch pension reform.

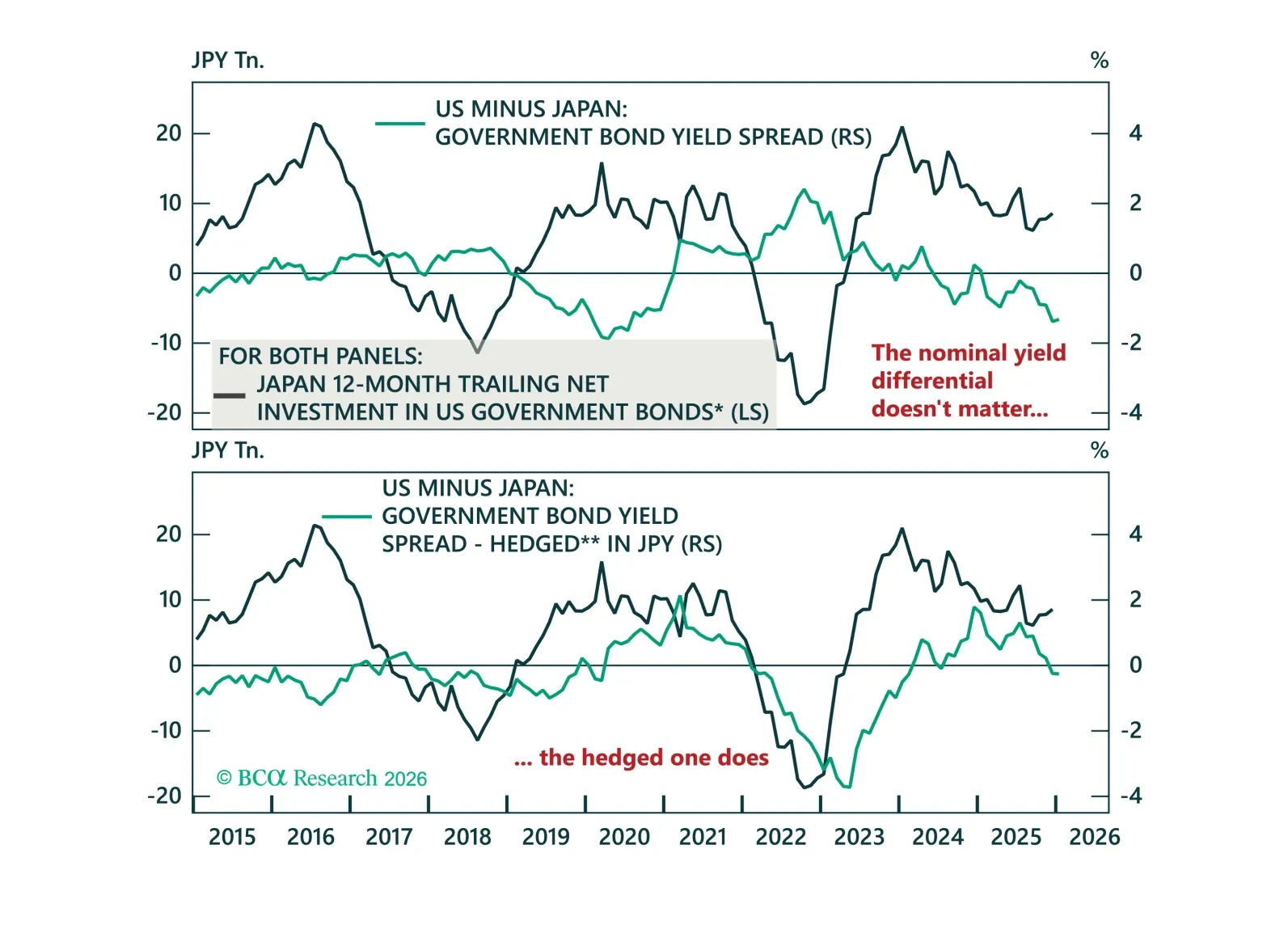

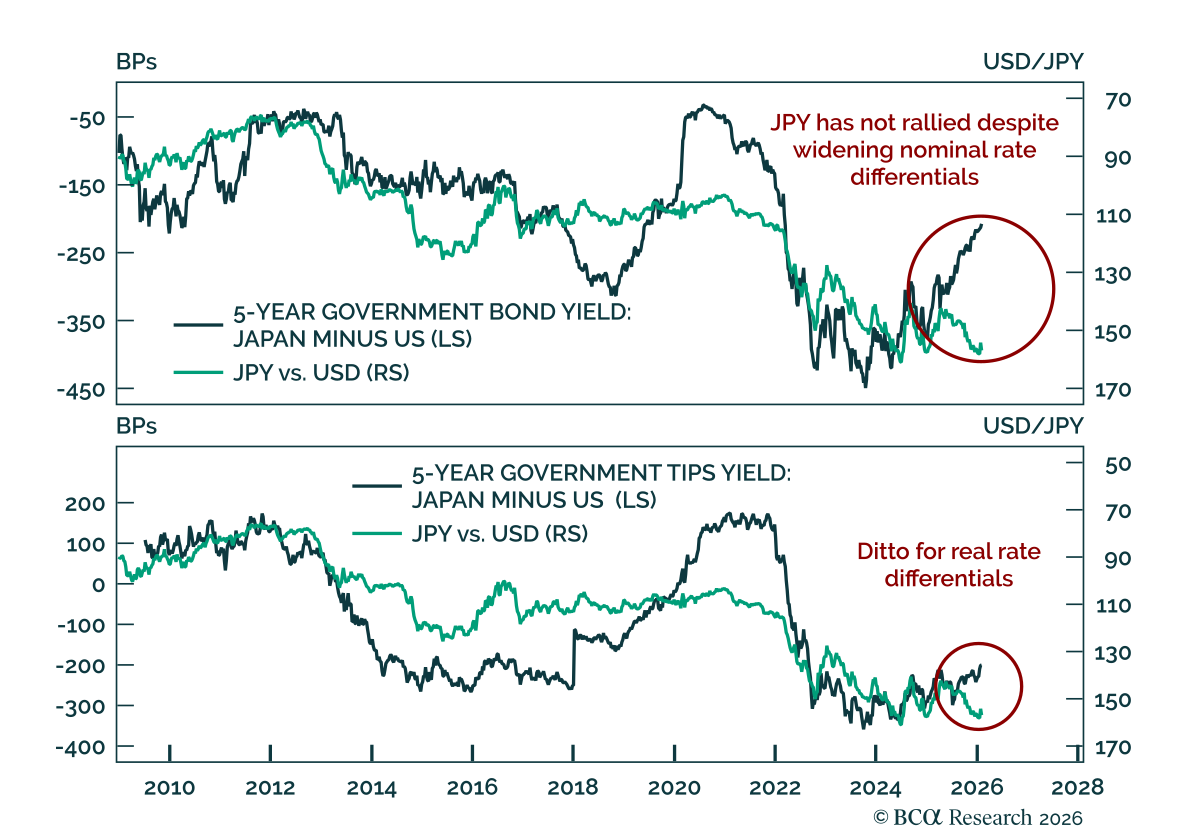

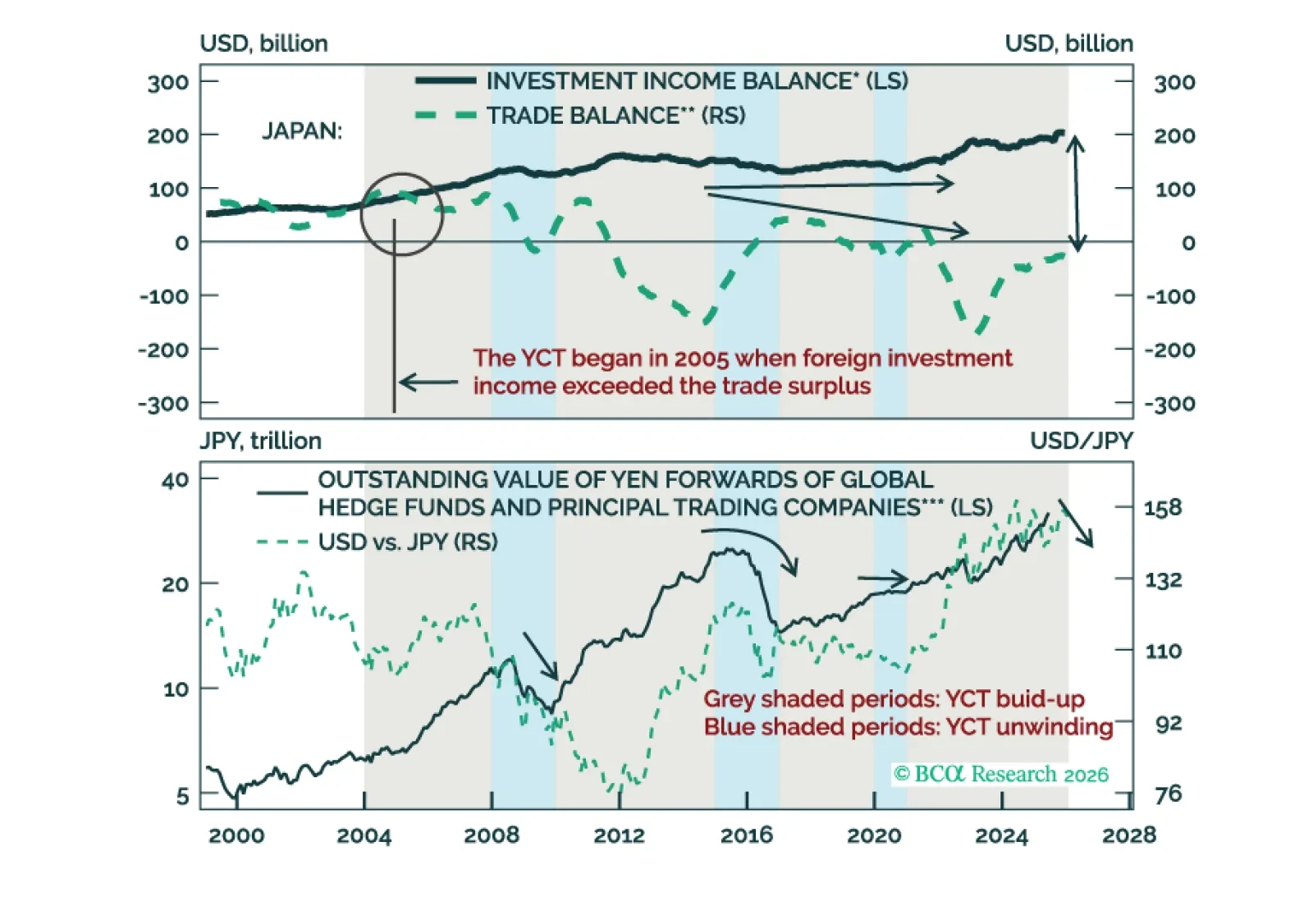

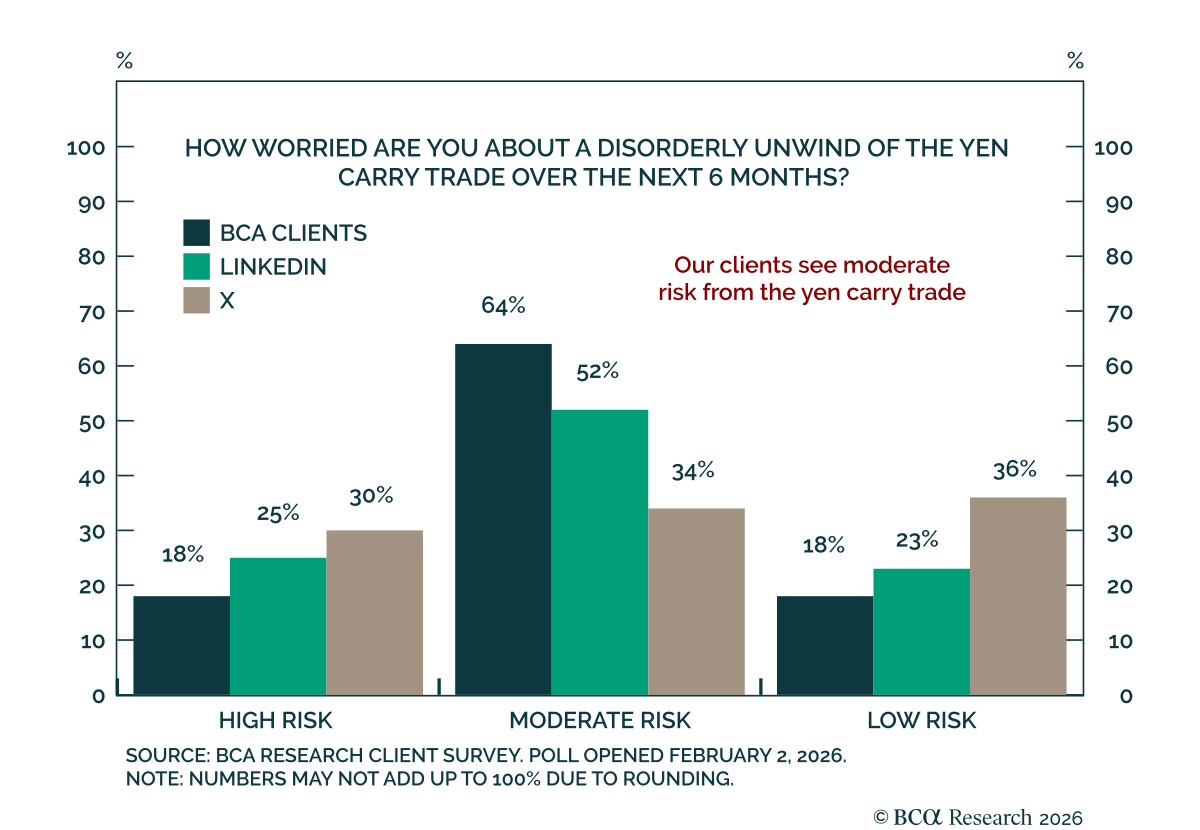

The yen carry trade will unwind this year. However, it will be triggered by a drop in “carry asset” prices and a spike in the JPY/USD, rather than by Japan’s improving interest rate differentials. Go long JPY against the USD.

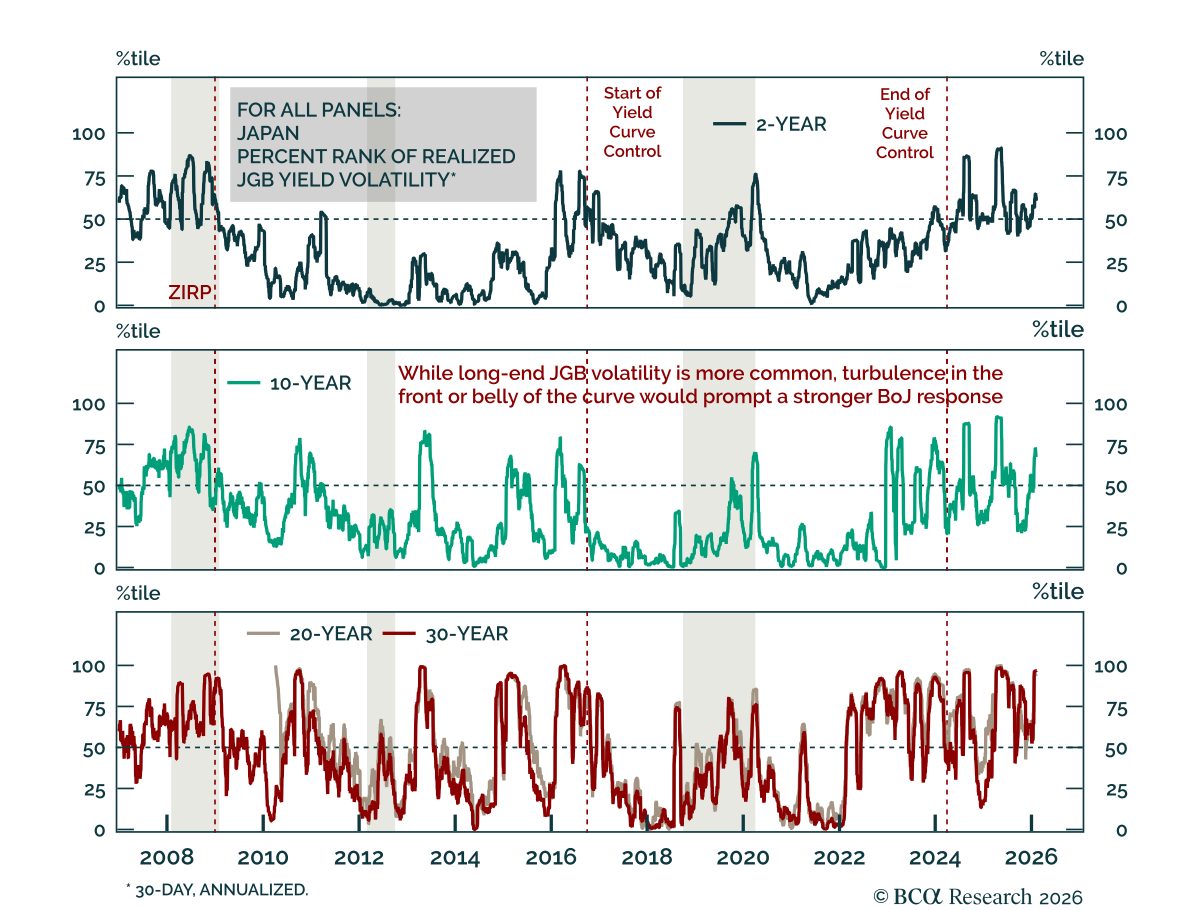

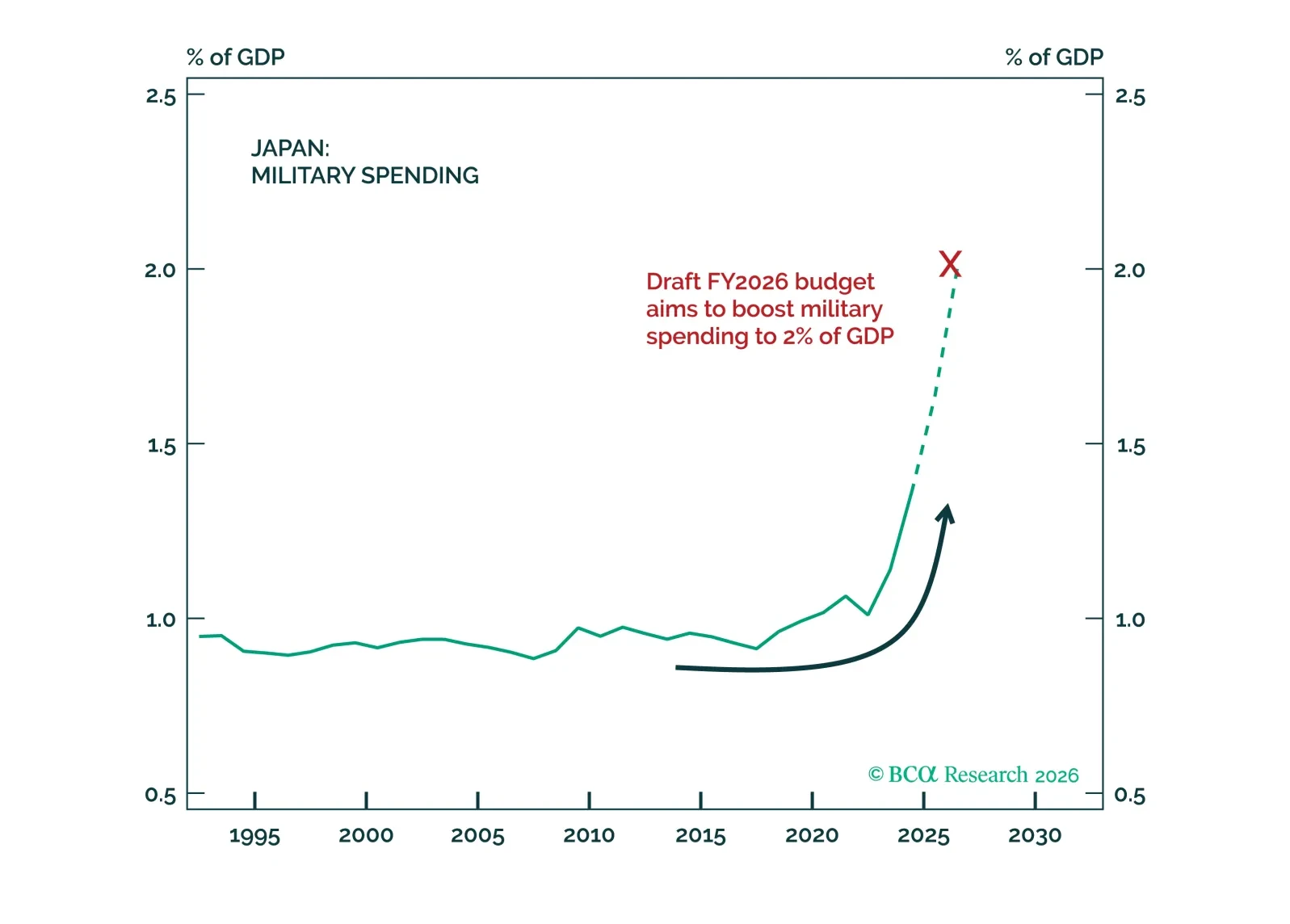

Ignore Japan's constitutional debate. Rearmament will accelerate anyway. Tech, defense stocks, and industrials will benefit. The threat to JGBs is real but will probably be contained.

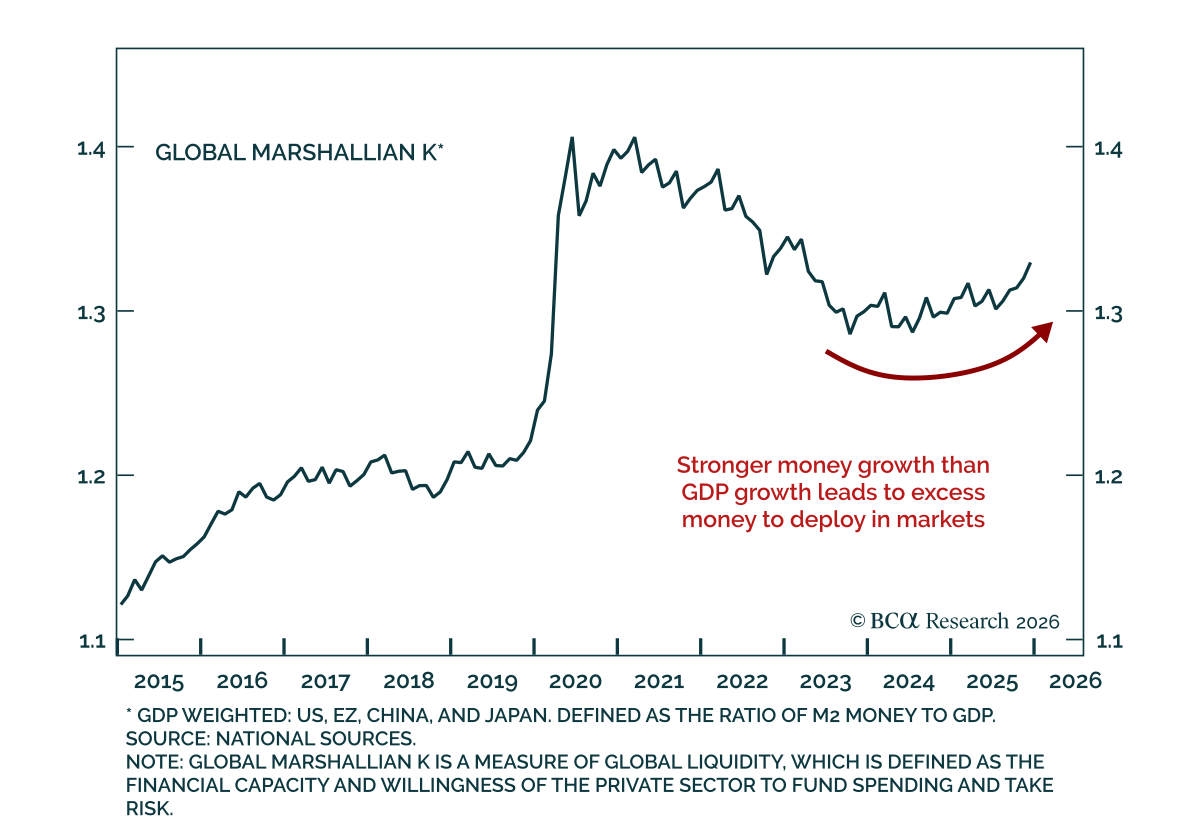

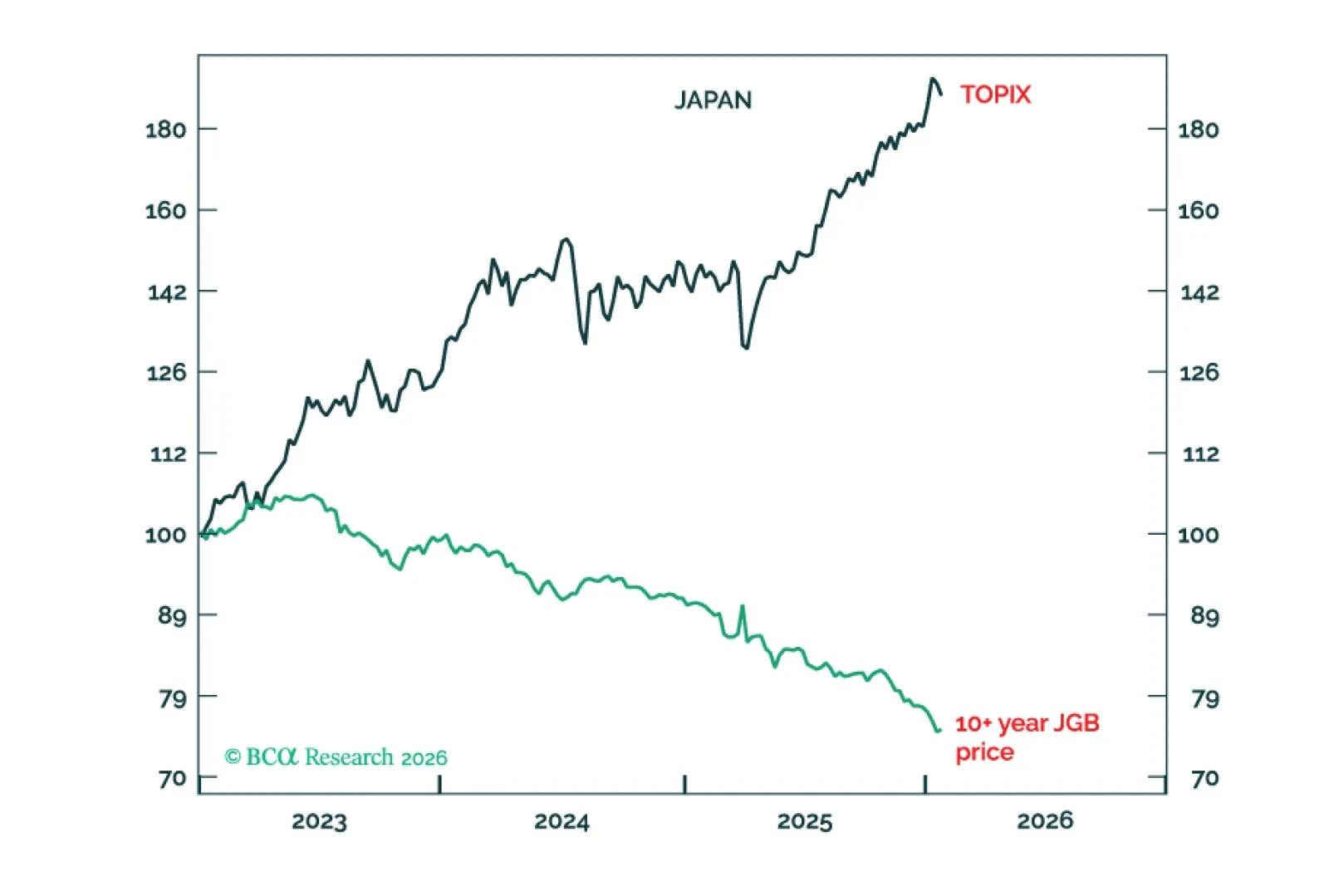

The US and Japan are in the same predicament: save the bond market or save the stock market? How this predicament will be resolved is the biggest global macro call of 2026-27. Plus: a new tactical trade is to go short AUD/JPY.