Japan

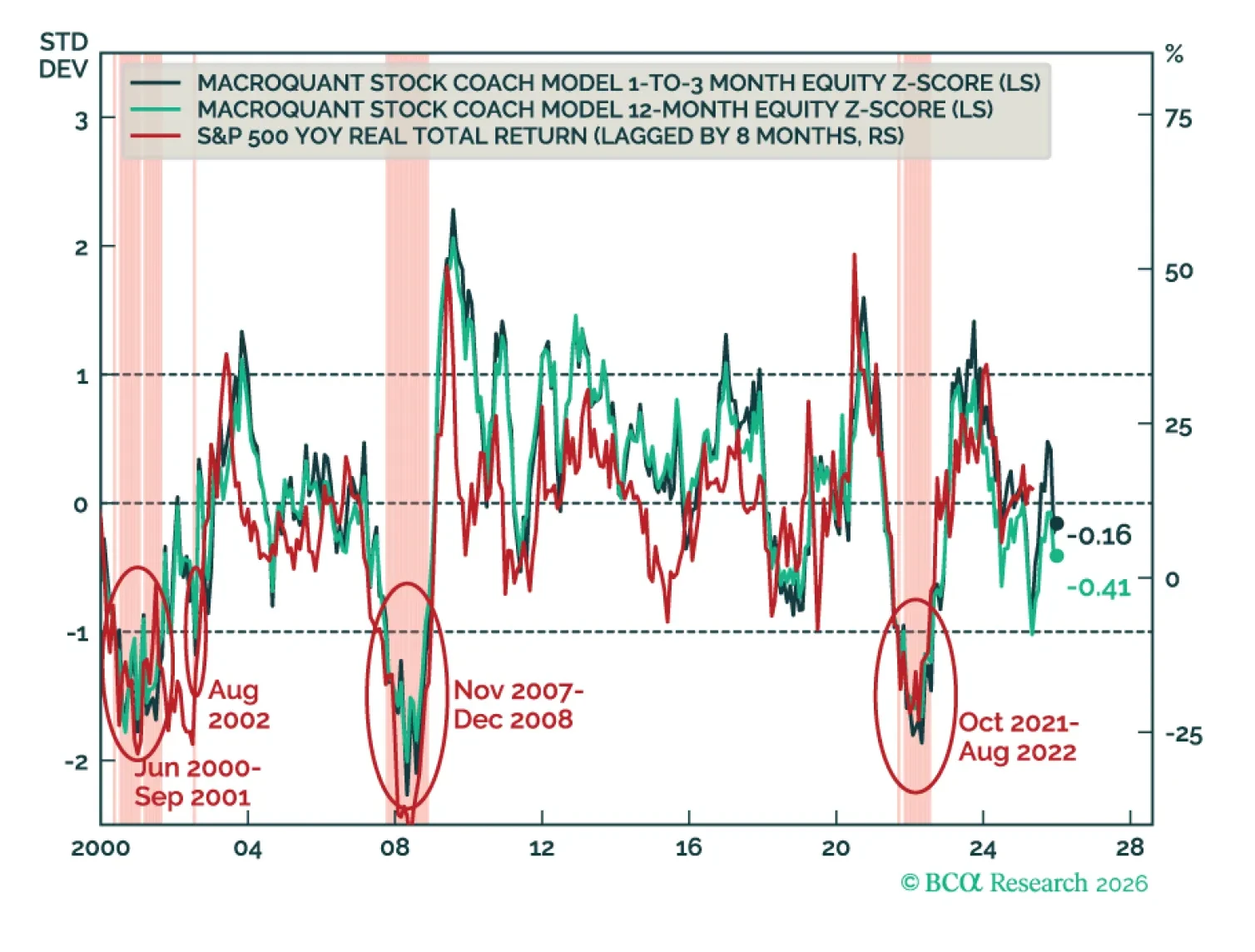

MacroQuant recommends a slight underweight in equities, favors a below-benchmark duration stance in fixed-income portfolios, remains bearish on the US dollar, has upgraded oil and copper to overweight, and is bullish on gold.

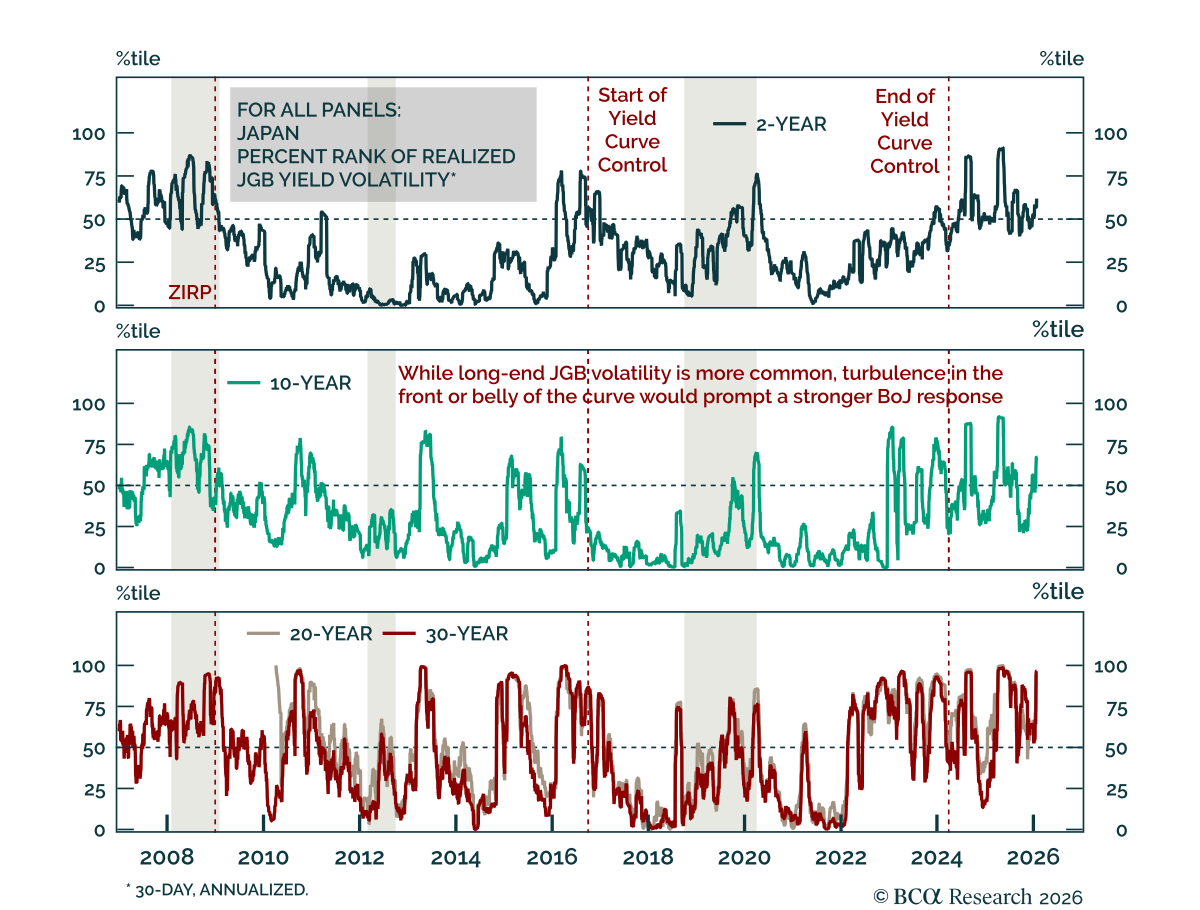

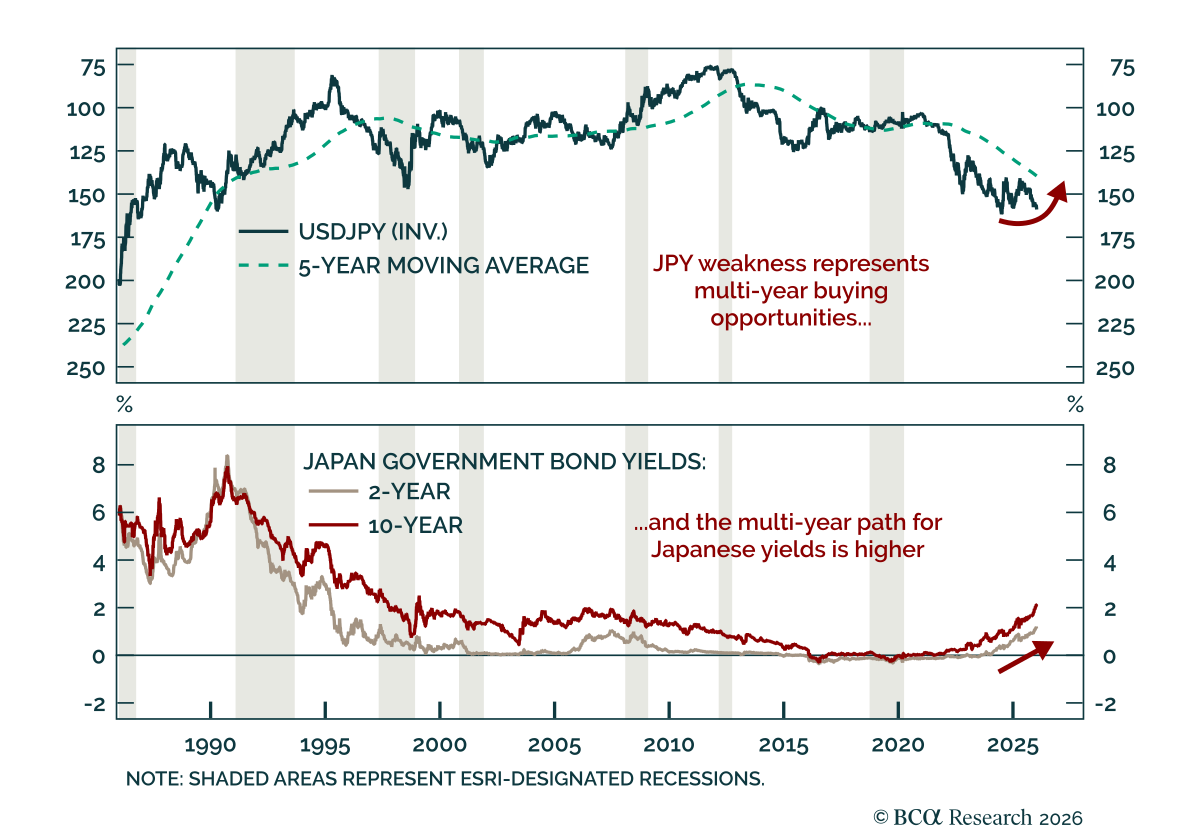

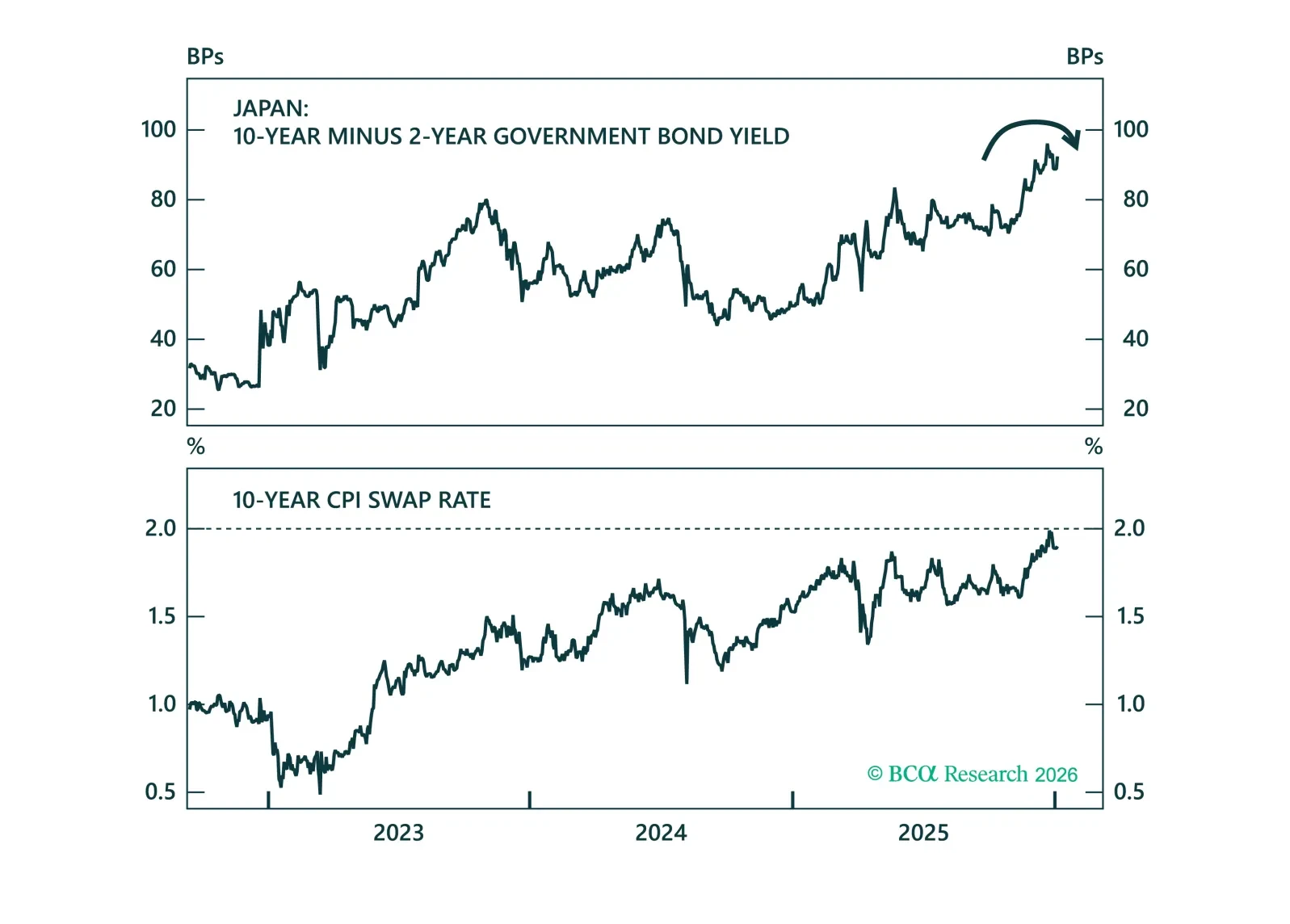

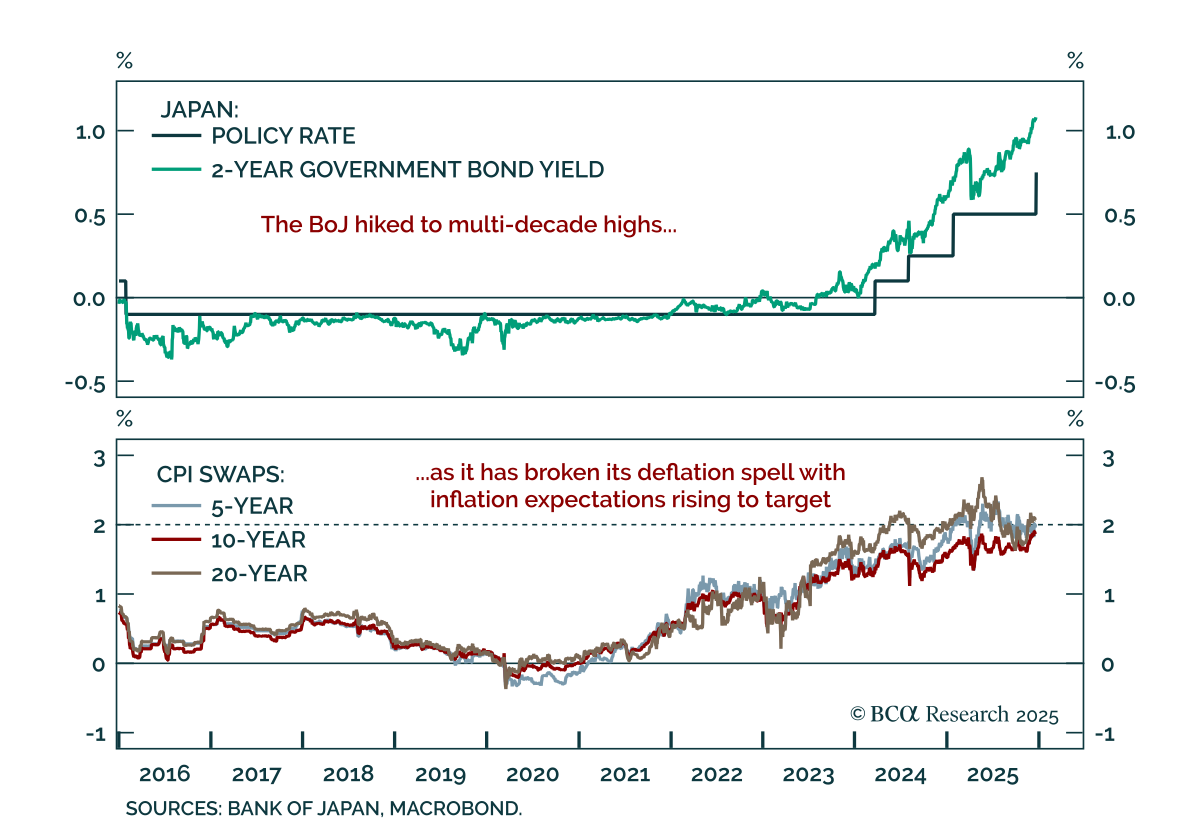

Japanese yields are heading higher as Japan exits its deflationary regime. Japan is exiting decades of deflation and ultra-accommodative policy, and markets are trying to find their footing. While attention has been focused on policy at the front end of the…

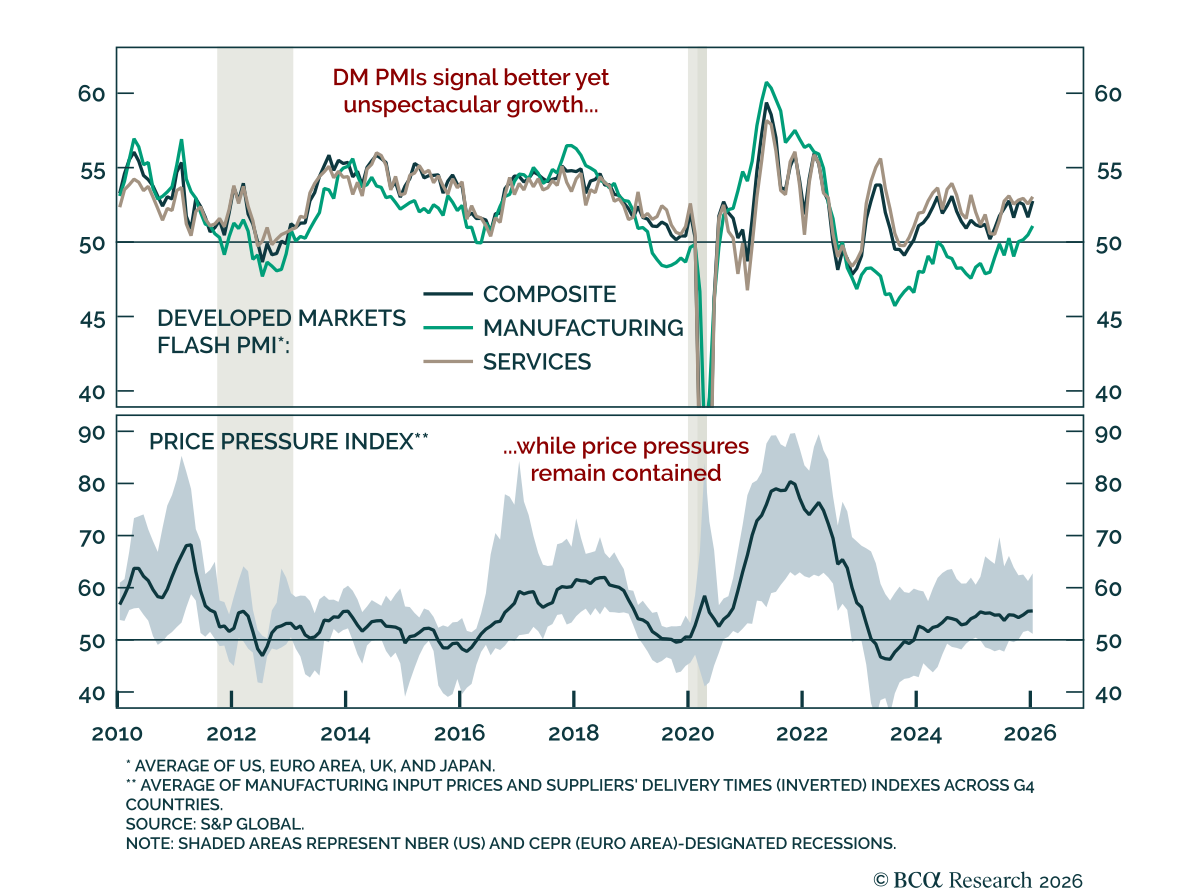

January flash PMIs point to better, though unspectacular, global growth momentum. Developed markets PMIs showed improvement in global growth momentum. PMIs have largely moved sideways through 2025, with manufacturing now recovering after trade uncertainty and…

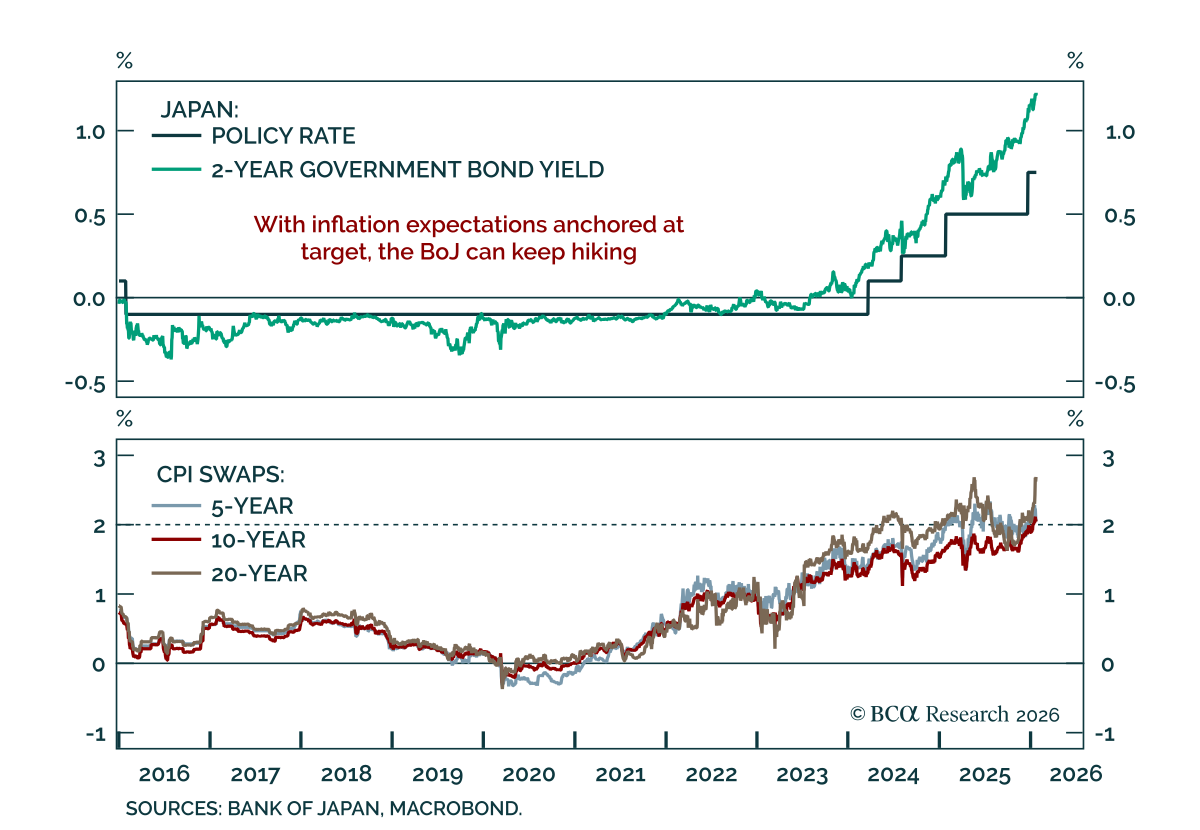

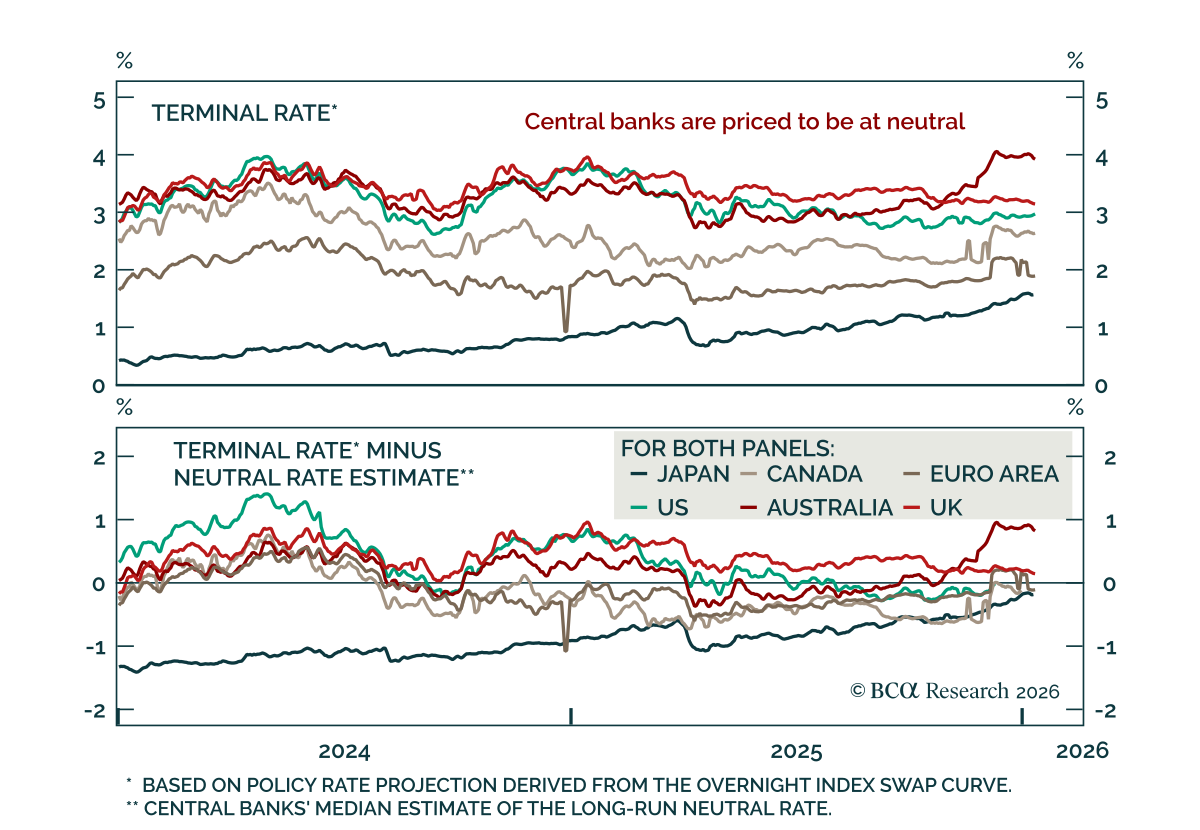

Favor JPY on dips and Japanese 2-year/10-year curve flatteners as the BoJ’s tightening path remains underpriced. The Bank of Japan held its policy rate at 0.75%, with one dissenting vote in favor of a hike; the same member had dissented ahead of the December…

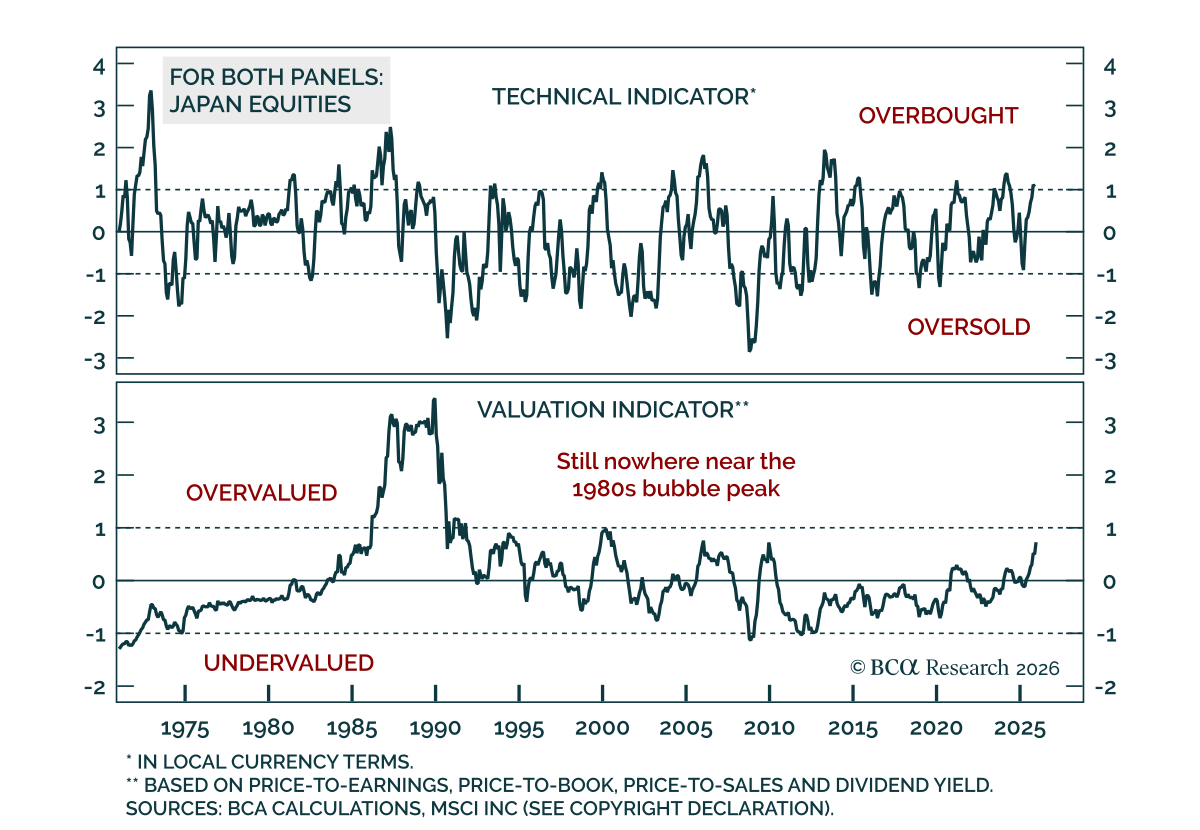

Japanese equities have entered a prolonged period of outperformance, both in local currency and common currency terms. Our GeoMacro strategists have a high conviction view that given recent market volatility, investors now have the opportunity to buy the…

Japan's new government will continue, but politics and foreign policy have become more competitive.

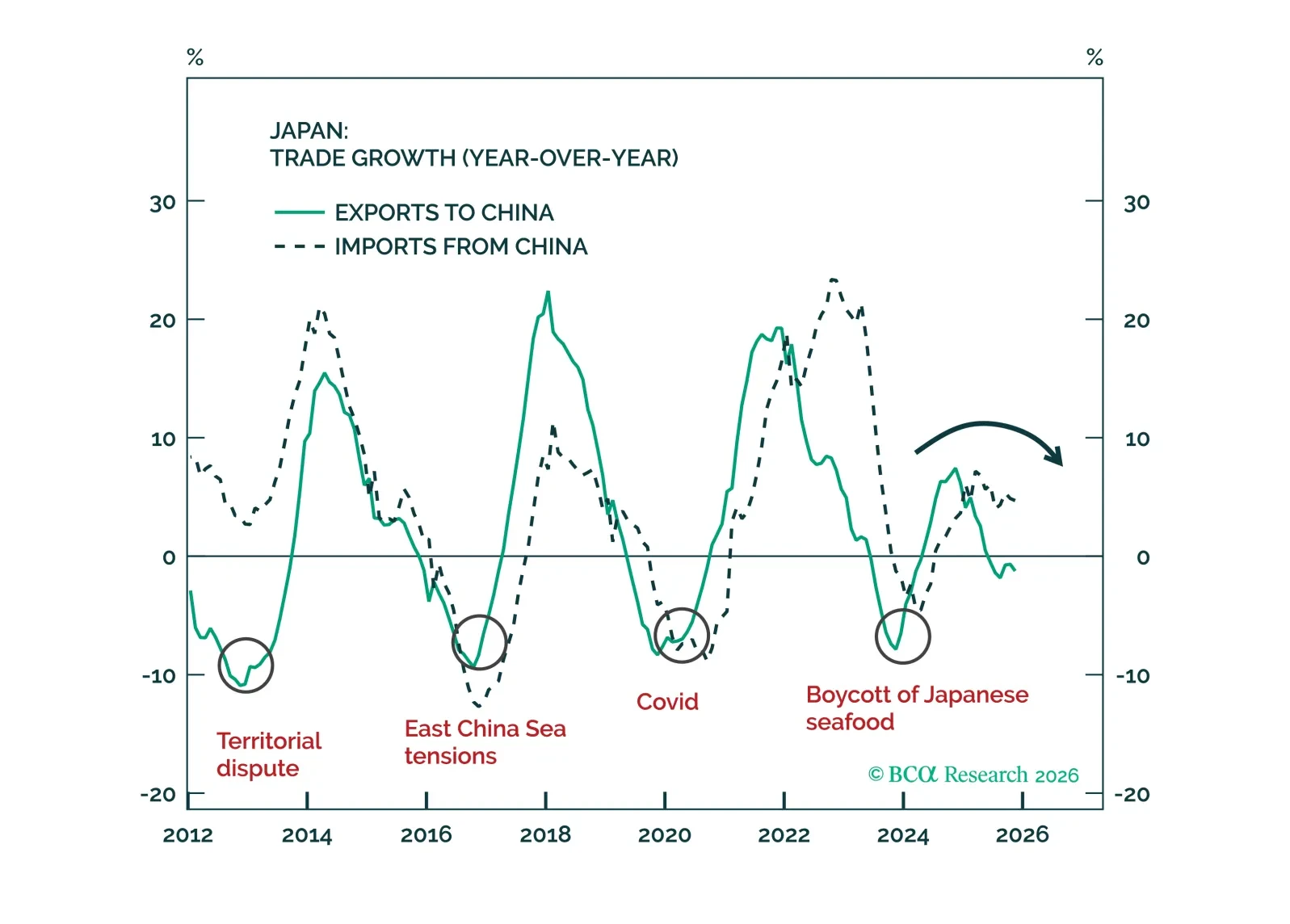

Favor JPY on dips and Japanese curve flatteners despite possible elections delays for BoJ hikes. Reports that Prime Minister Takeshi may call a snap election triggered a sharp equity rally, consistent with historical patterns of Japanese stocks performing…

Our Global Fixed Income strategists maintain an above-benchmark duration stance as labor market risks continue to support downside yield potential, even as the global easing cycle winds down. With policy normalization largely complete, monetary policy is…

From steepening to flattening. As the BoJ continues to tighten in 2026, we show why curve flatteners are finally the right trade.

The BoJ’s tightening path remains steeper than markets price, leaving JGBs unattractive in bond portfolios. The Bank of Japan raised rates by 25 bps to 0.75%, a multi-decade high, and signaled that further hikes are likely. However, the indicated pace fell…