Japan

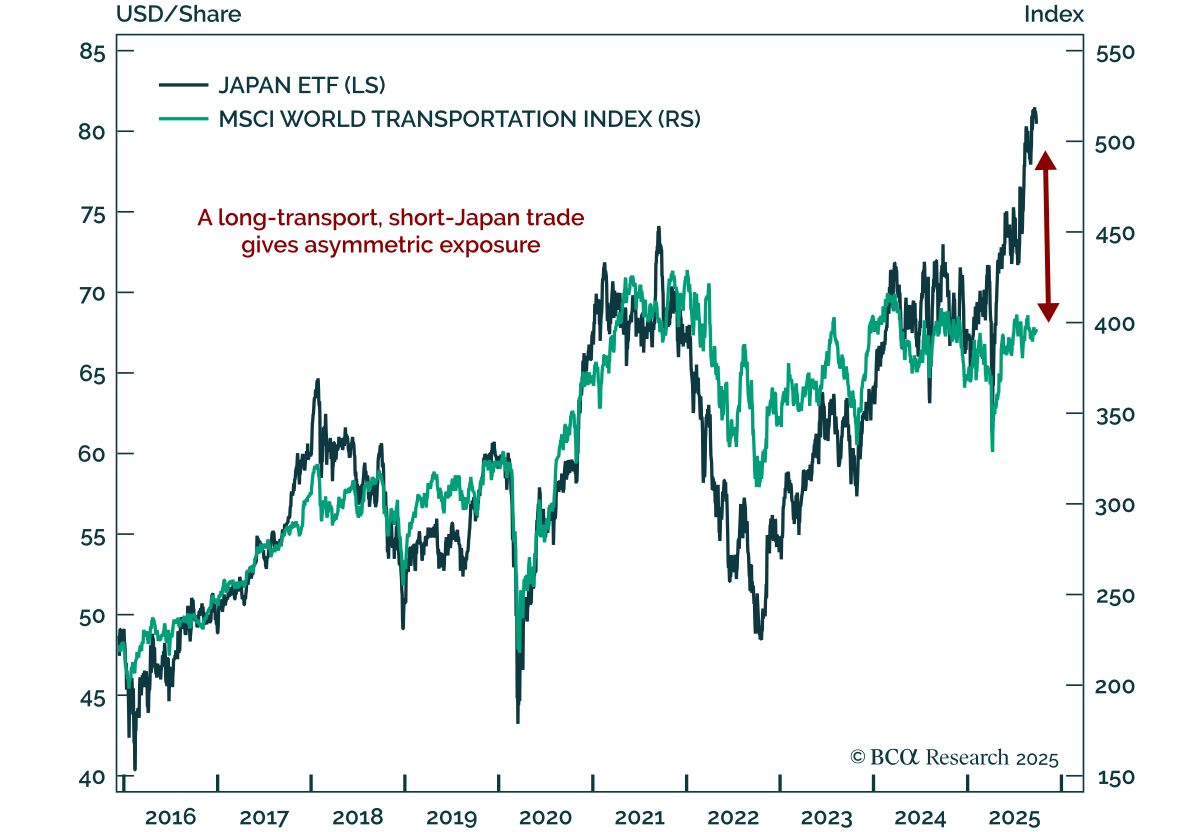

Sell Japanese equities and buy global transportation stocks to capture an overdue mean-reversion in trade-exposed assets. Our Chart Of The Week comes from Mathieu Savary, Chief DM ex. US Strategist. The post-Liberation Day rally lifted the unhedged…

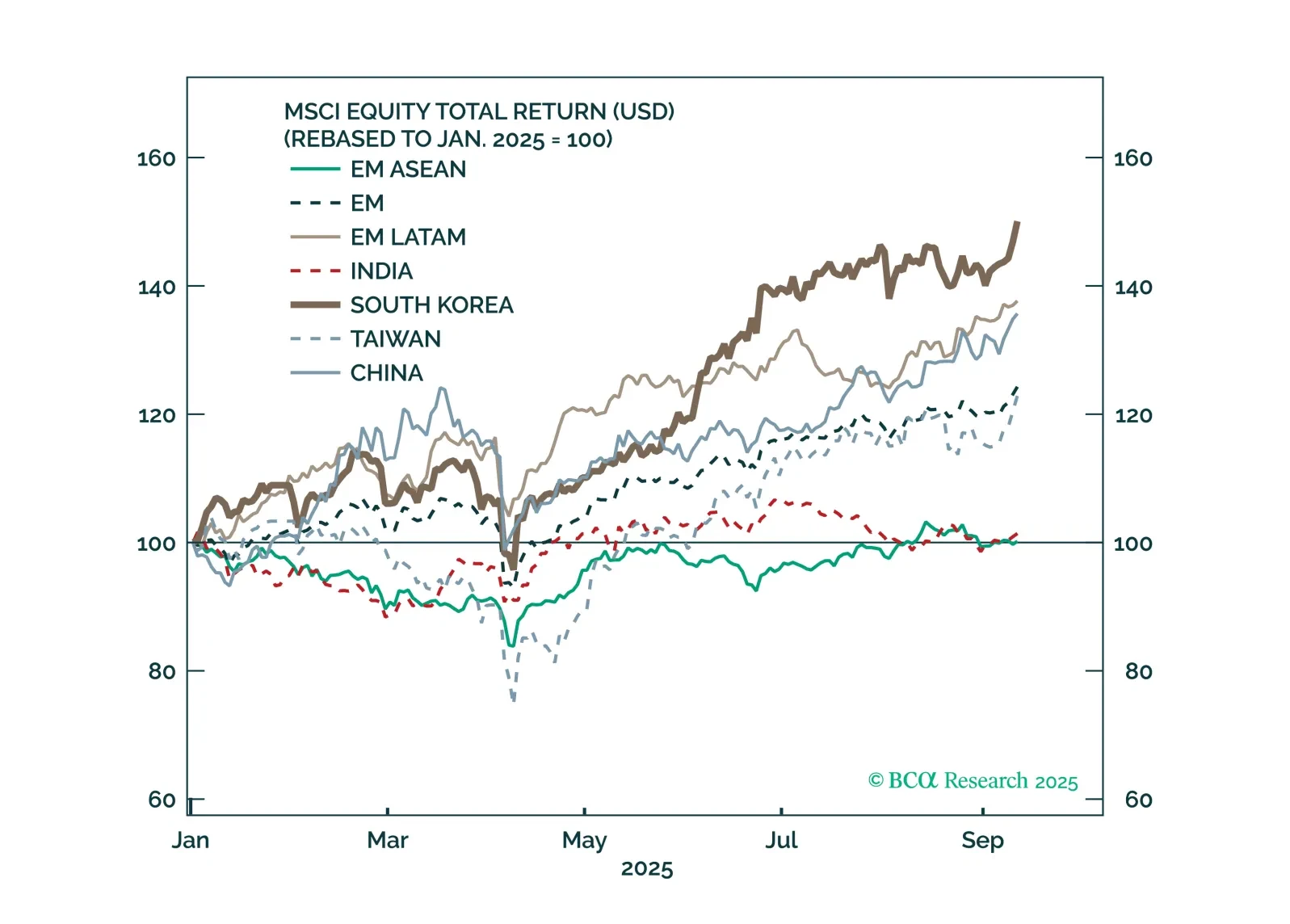

Political instability across Asia is colliding with the trade war fallout, forcing Southeast Asian economies to ease monetary and fiscal policy, while pushing the Bank of Japan in the opposite direction.

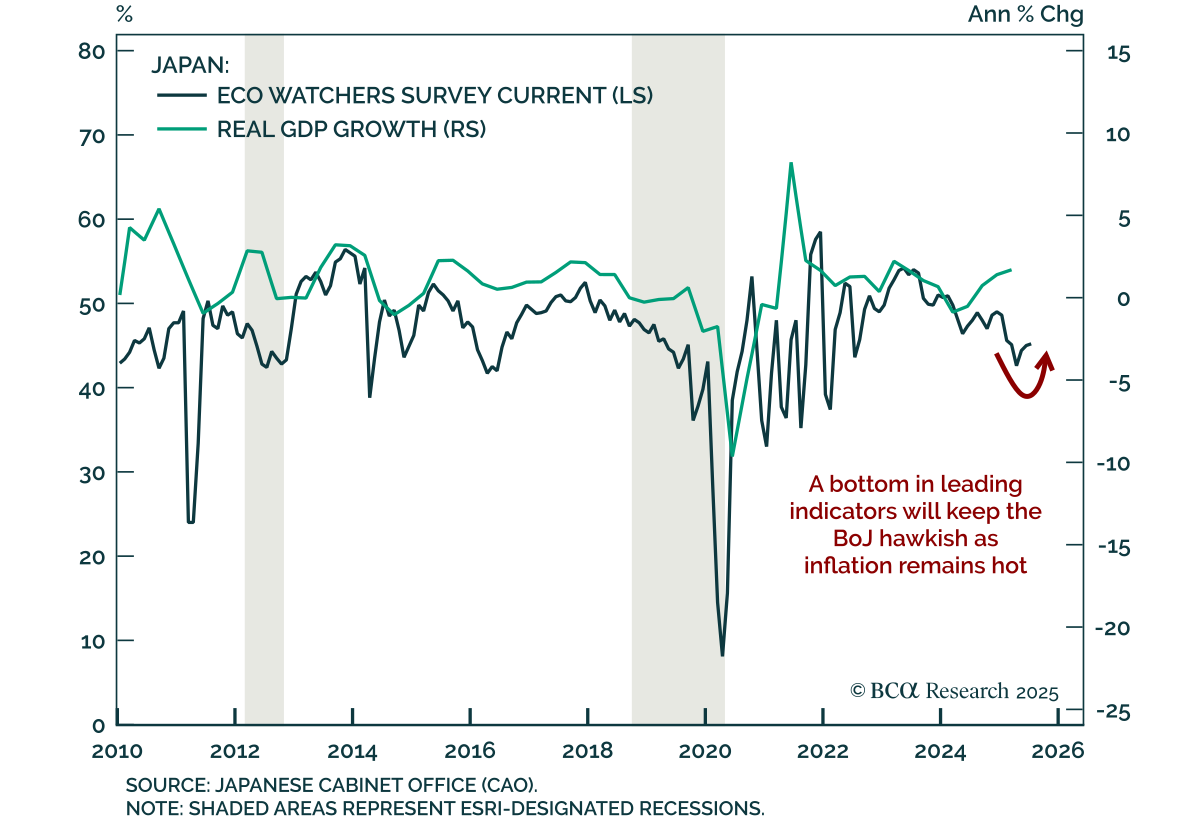

Japan’s Eco Watchers Survey points to stabilization; JGBs remain unattractive and the yen’s near-term setup is less favorable versus USD. The August survey modestly beat expectations, with the current component rising to 46.7 from 45.2 and expectations…

A fleeting greenback rally post Fed rate cut will offer a final chance to reset short dollar exposures. See why undervalued Asian FX are poised to lead the next leg lower in USD and how to position now.

Japan’s Eco Watchers survey suggests growth has troughed, making JGBs vulnerable in both global slowdown and reacceleration scenarios. The July survey showed current conditions ticking up to 45.2 and expectations improving to 47.3. While both remain…

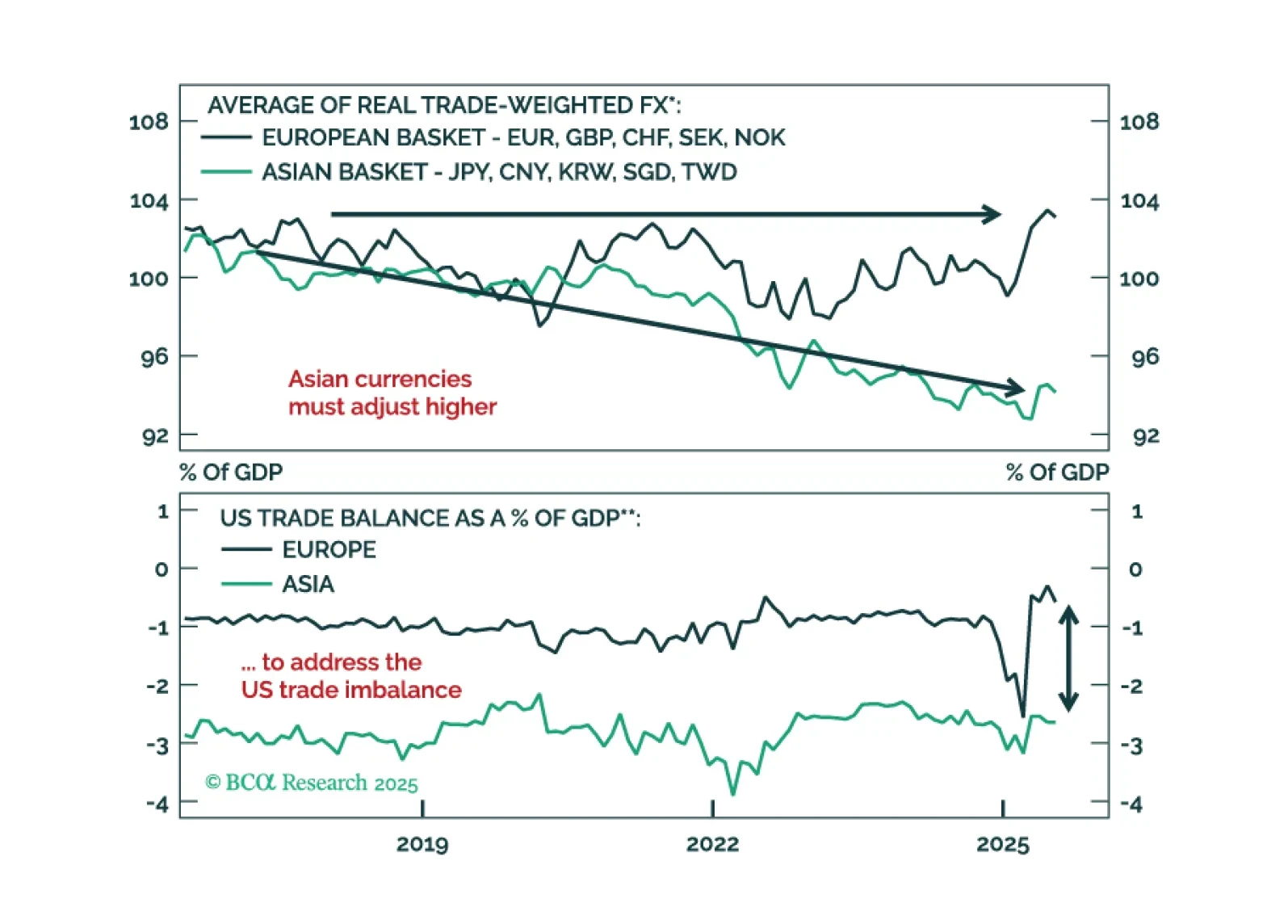

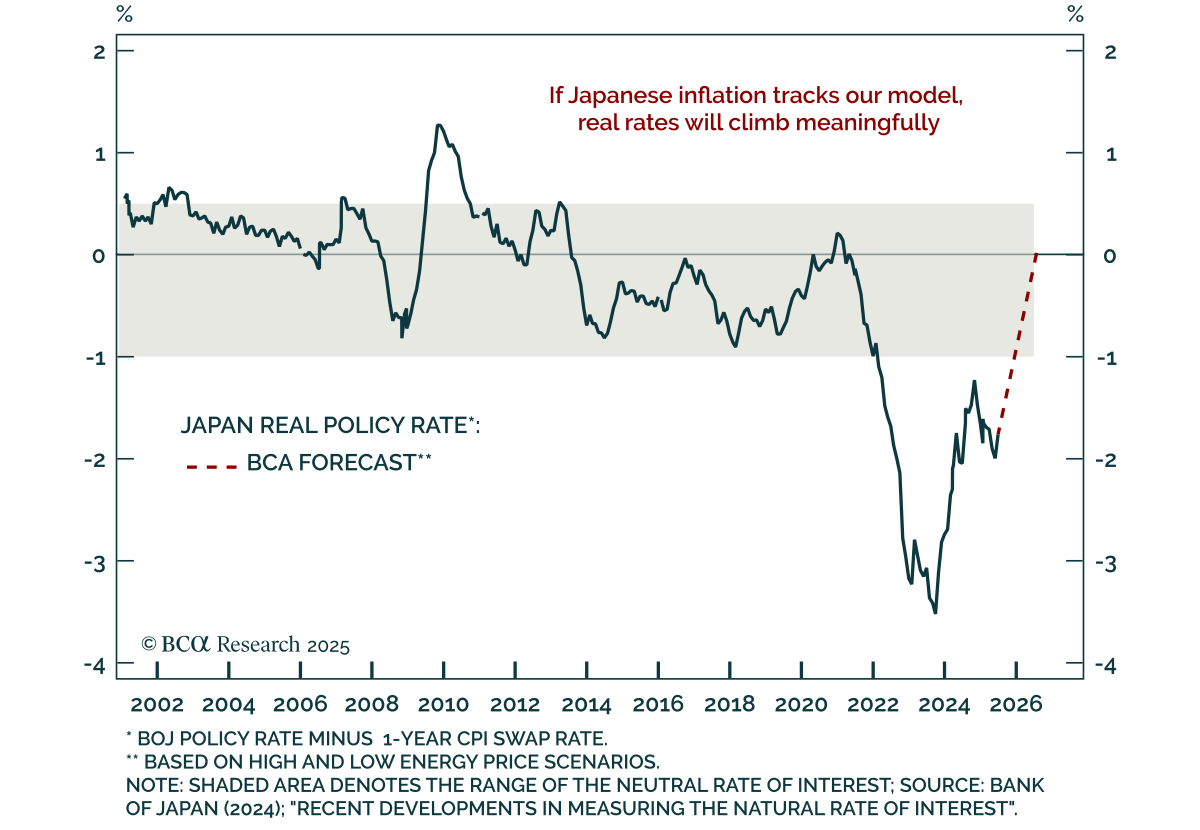

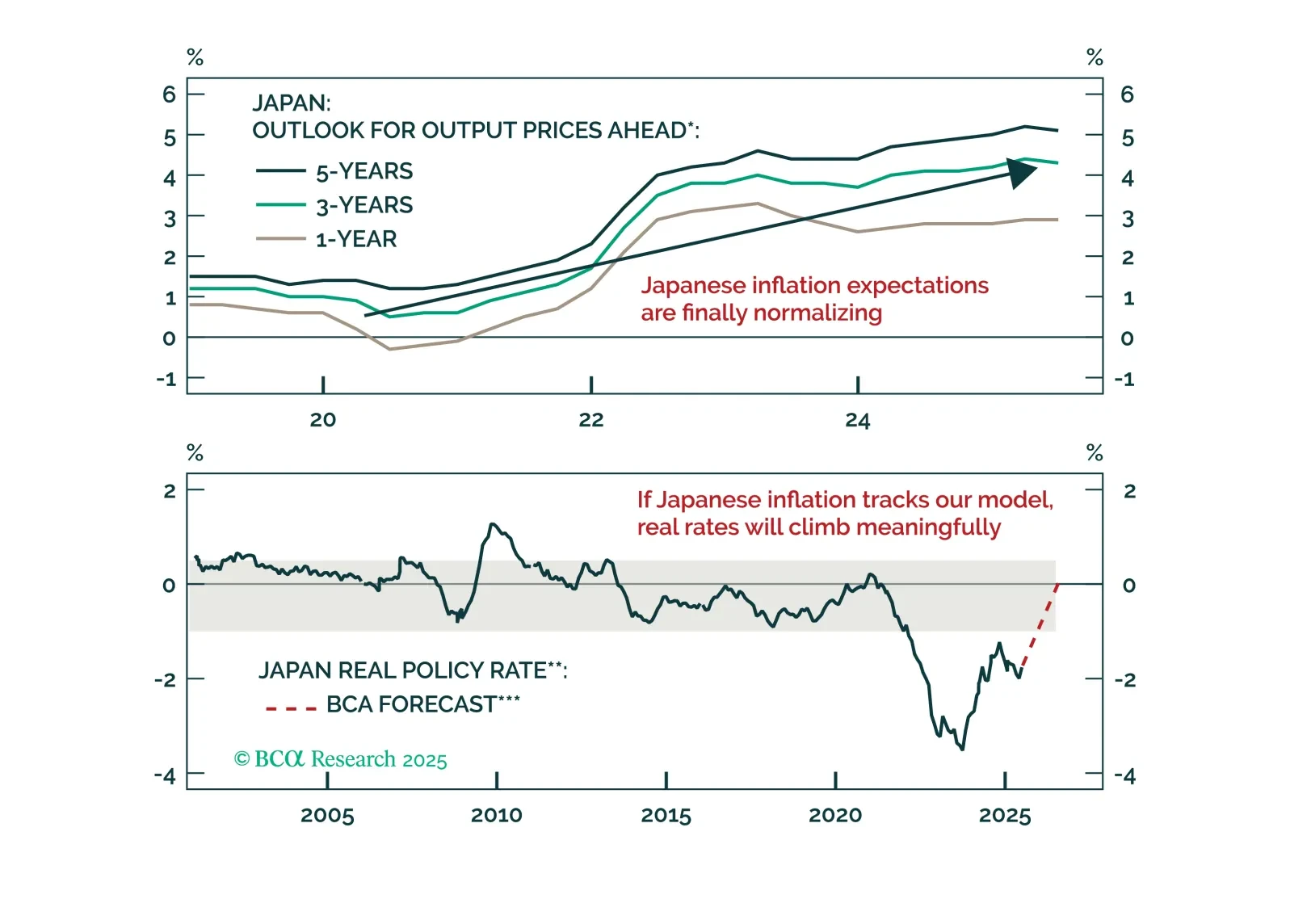

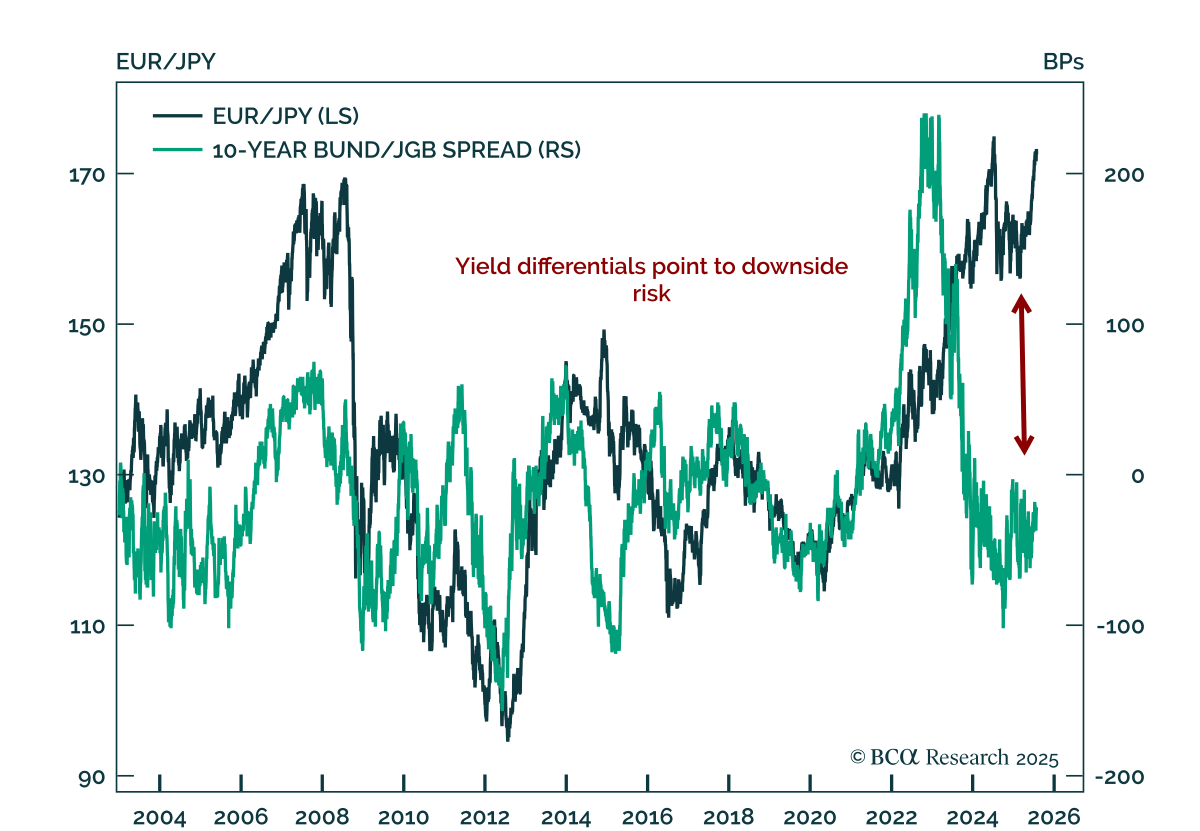

Our DM ex. US strategists see the yen entering a multi-year rally and recommend shorting EUR/JPY now while preparing to short USD/JPY as Fed cuts approach. The yen remains deeply undervalued across PPP, unit labor cost, and real trade-weighted metrics, near…

The yen’s discount, surplus, and rising real rates line up for a multi-quarter surge. Find out why EUR/JPY is the first short and when USD/JPY follows.

Our strategists recommend shorting EUR/JPY, citing stretched valuations and rising reversal risks. The cross has surged more than 6% since late May, triggering new short positions from the Counterpoint, European Investment Strategy, and Global Investment…

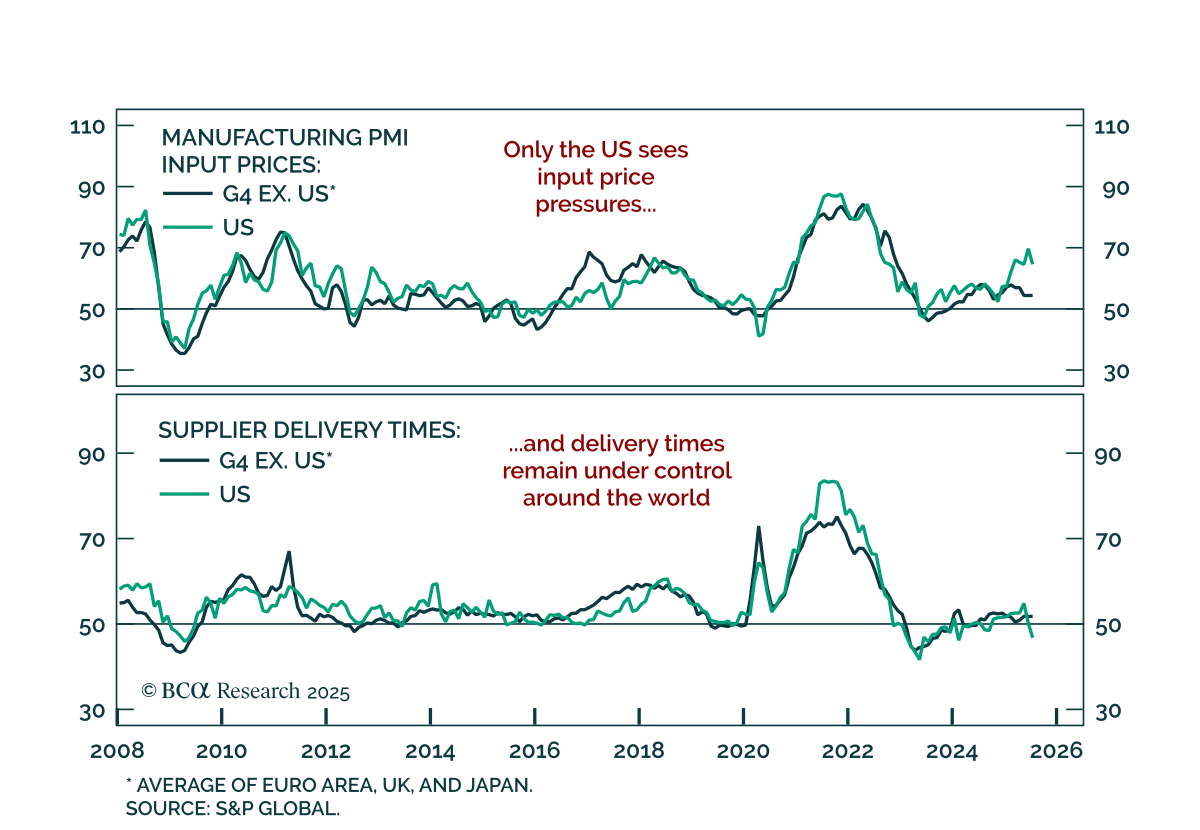

Cresting price pressures and weak global growth reinforce our long duration stance, with labor market slack limiting inflation upside across most major economies. Our price pressure indexes show moderate input inflation outside the US and stable global…

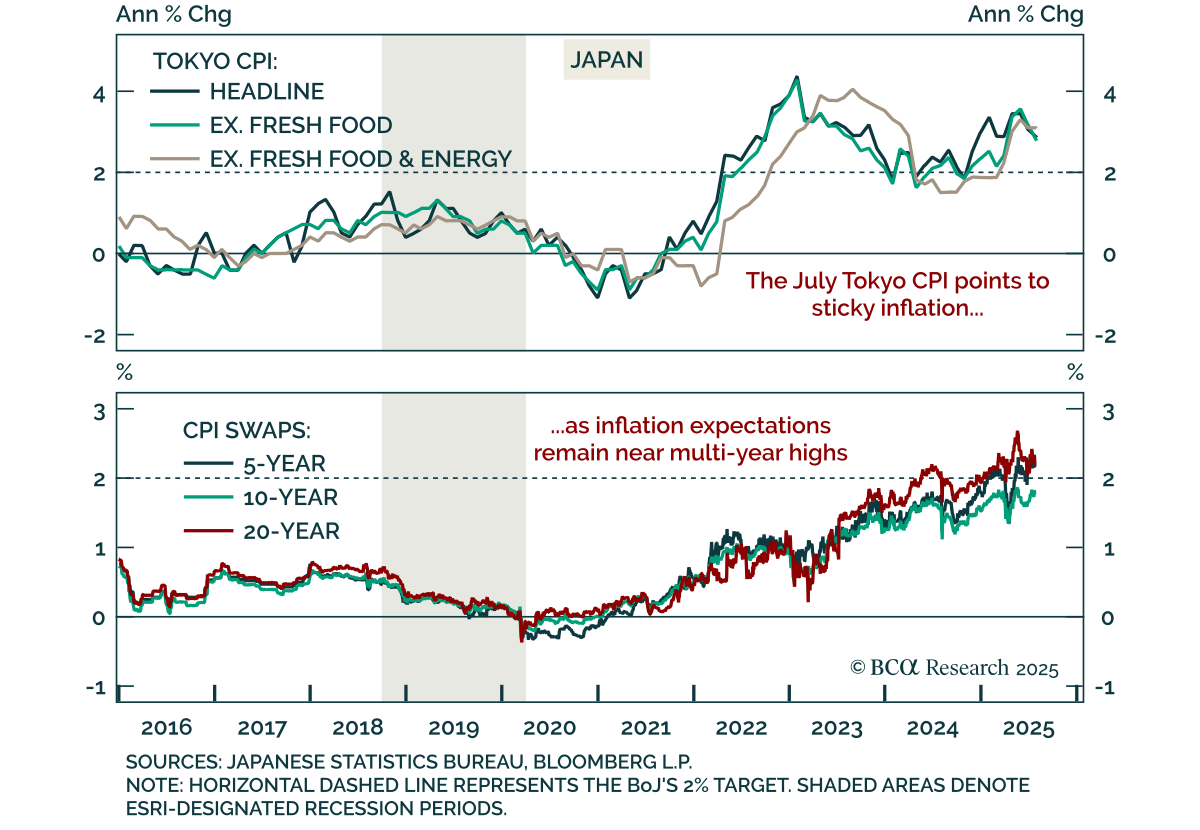

Tokyo CPI data confirms persistent inflation pressures in Japan, keeping the BoJ on a hawkish footing and reinforcing our underweight in JGBs and bullish stance on the yen. July Tokyo CPI came in broadly in line, falling to 2.9% y/y from 3.1%, with core and…