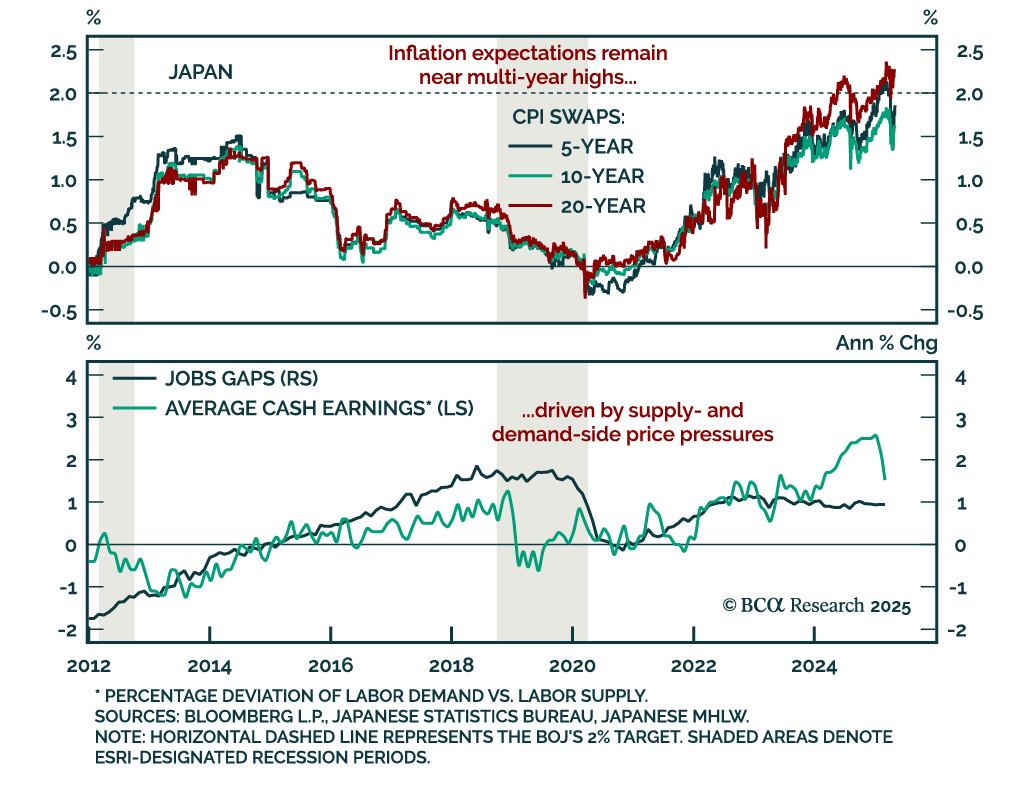

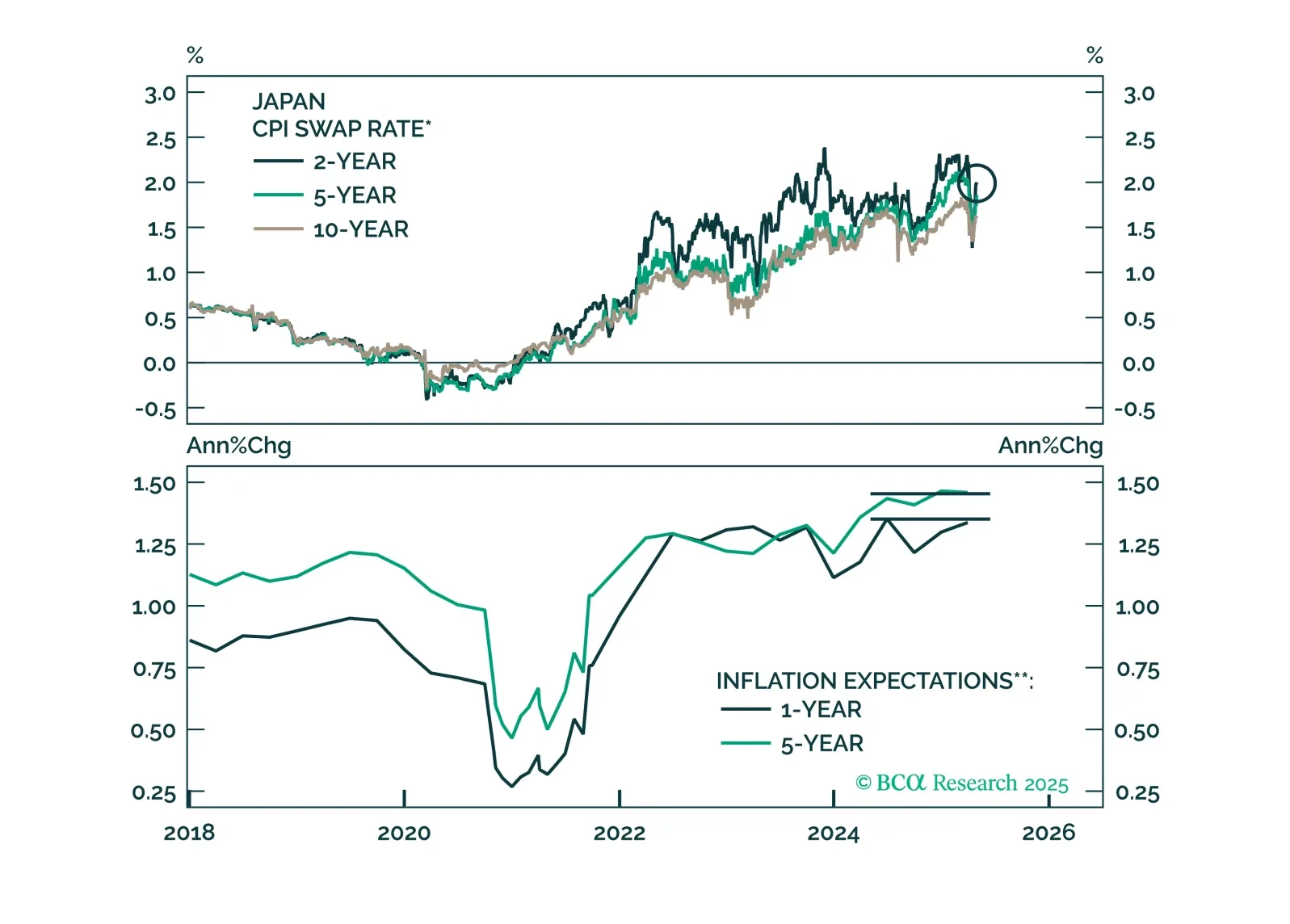

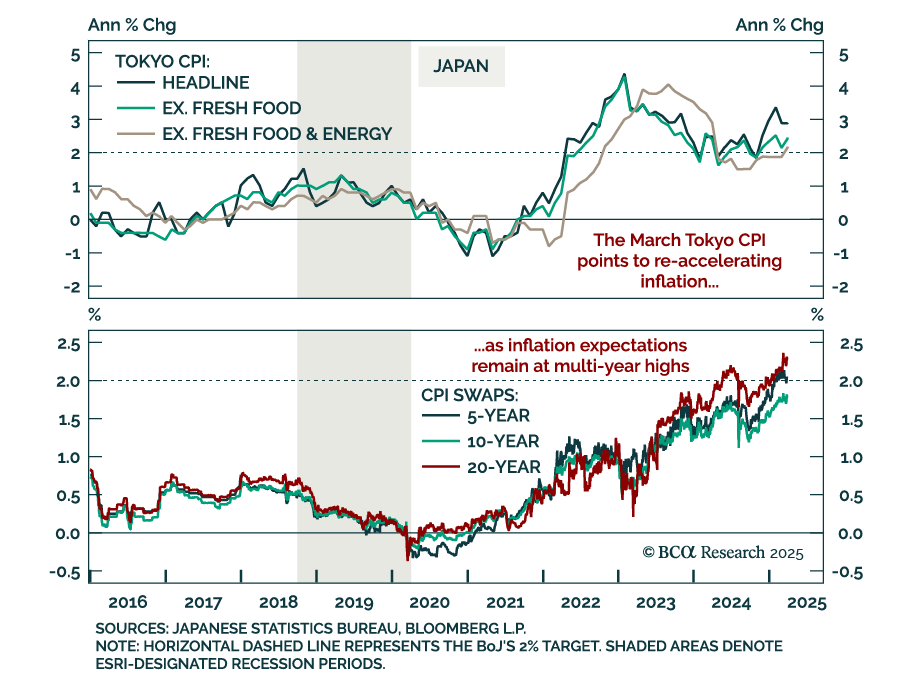

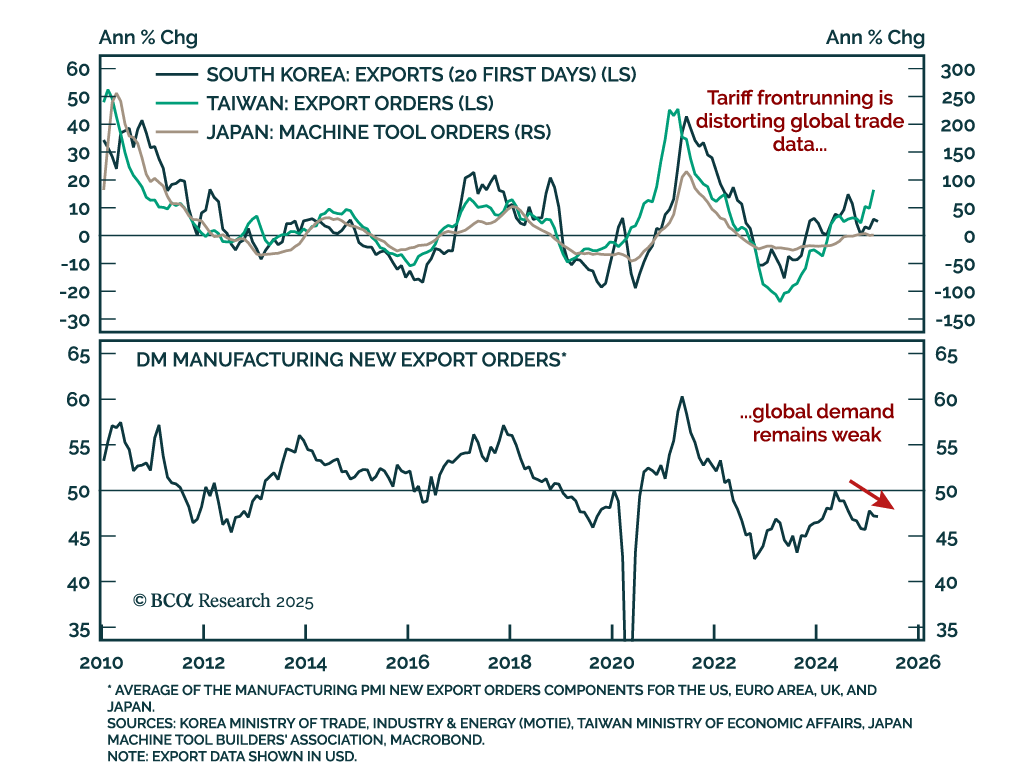

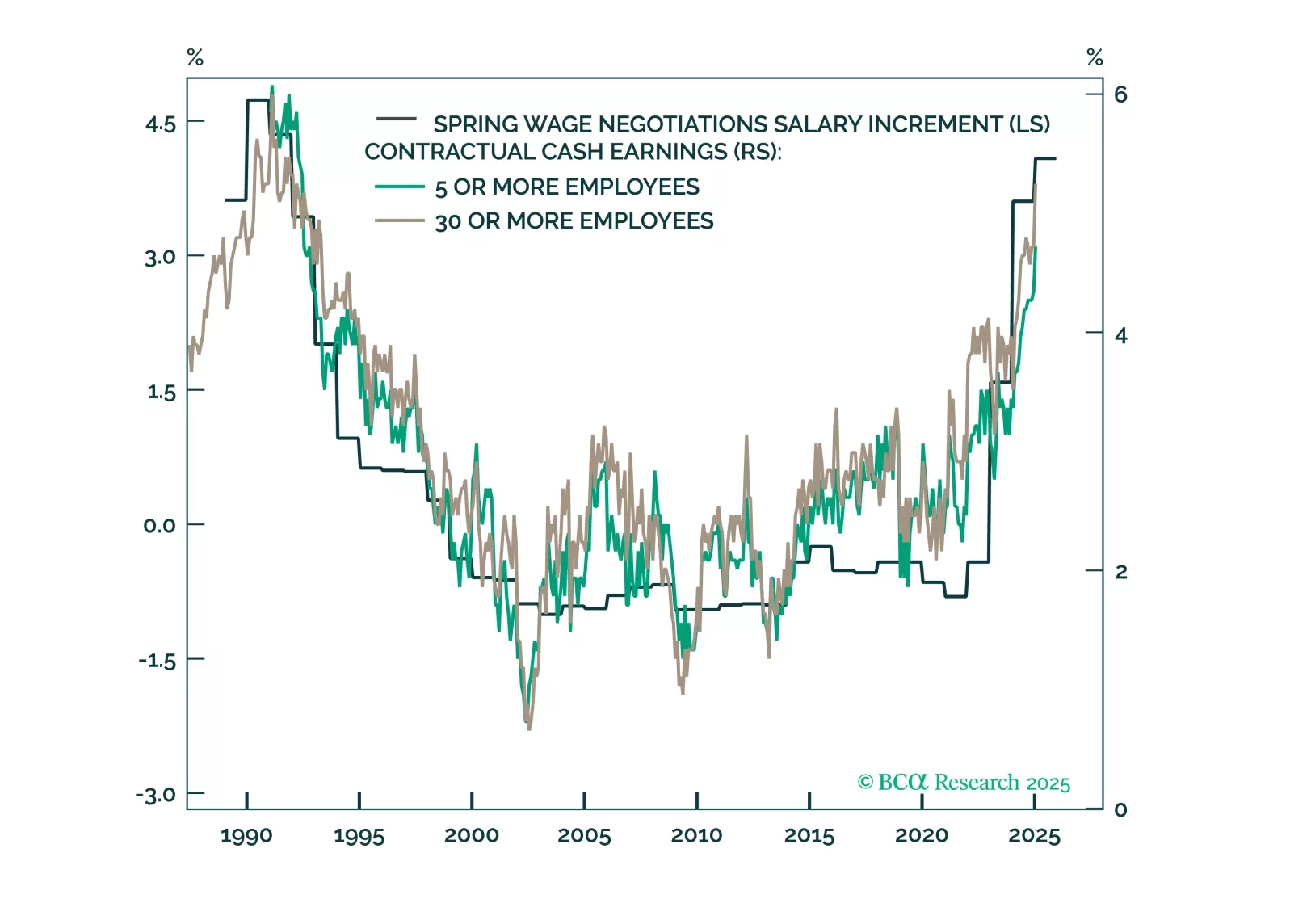

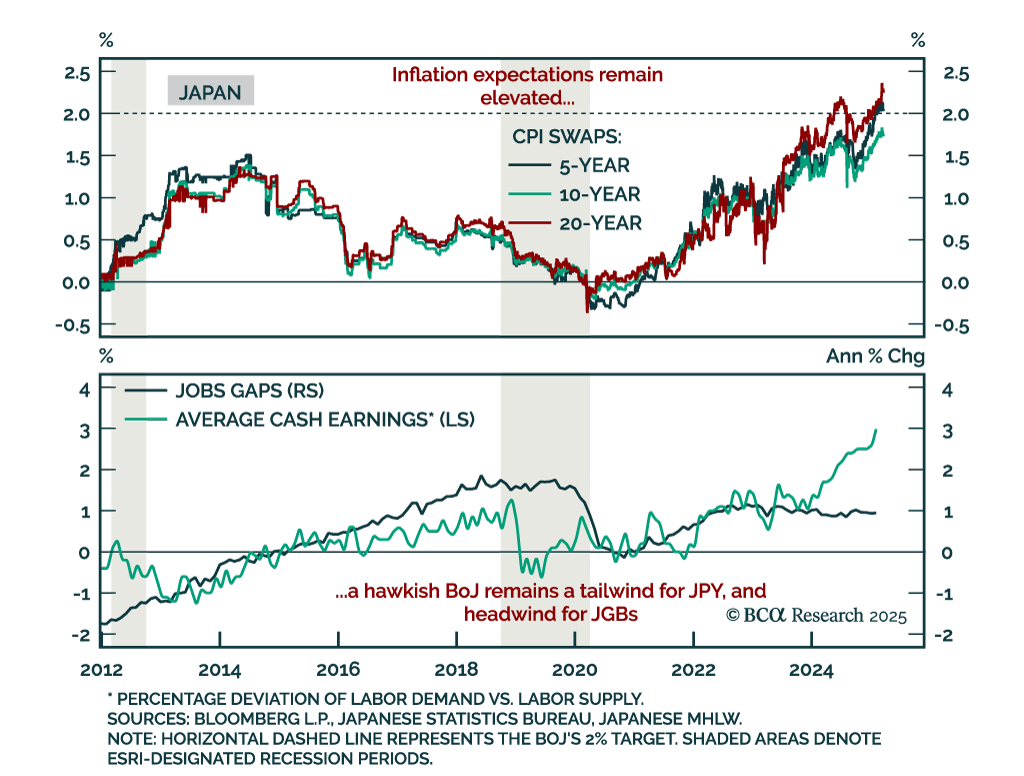

Japan

This week’s report looks at Japan, with the recent BoJ meeting. While a trade war has injected uncertainty into the Japanese economy, our conviction remains high that JGBs will underperform other government bond markets, and the yen will ultimately rally. That said, JPY is due for a tactical pullback.

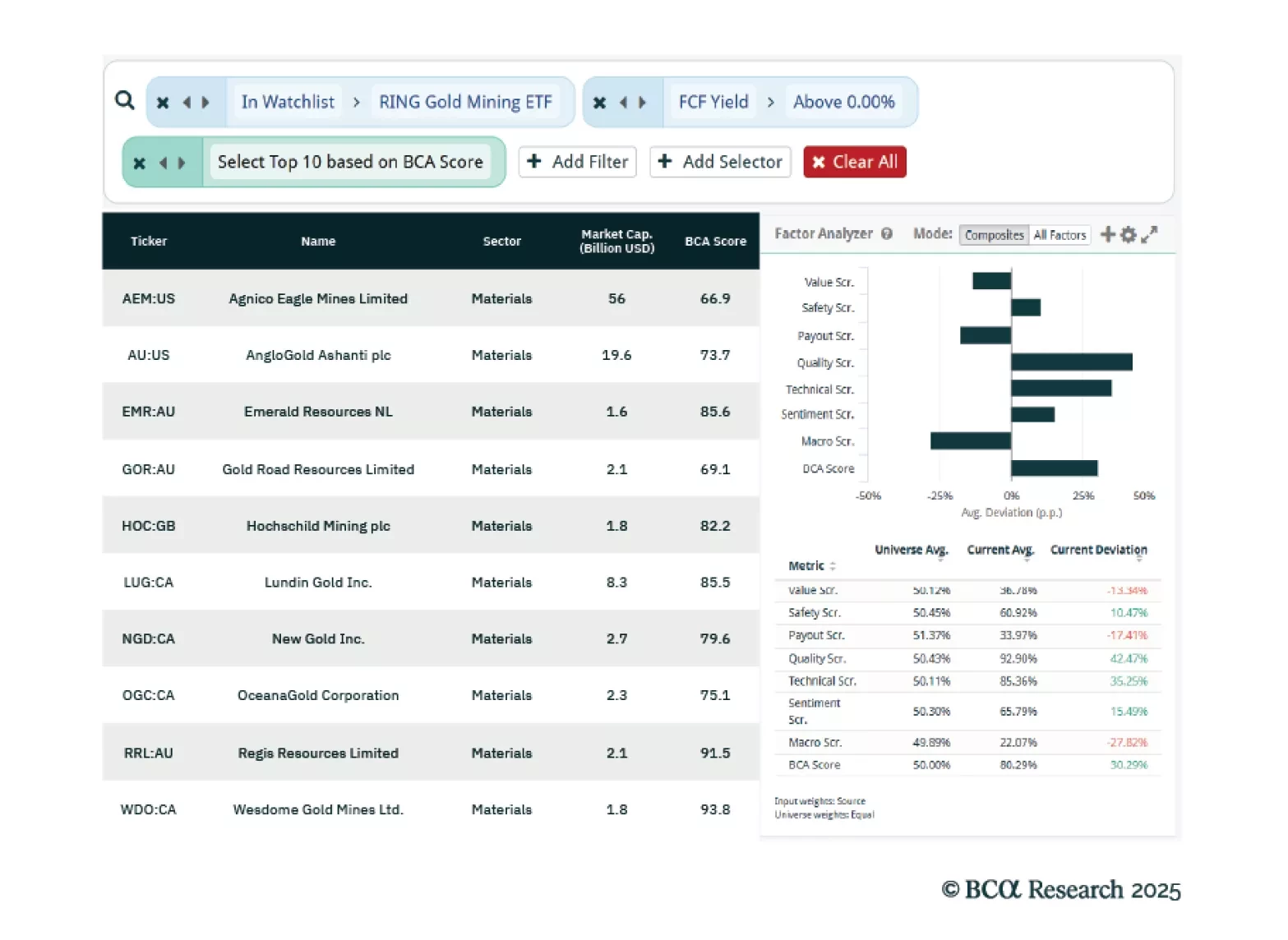

This week, our three screeners cover equity plays in: Gold mining stocks, Japanese Staples, and Implicit Dividend Yield.

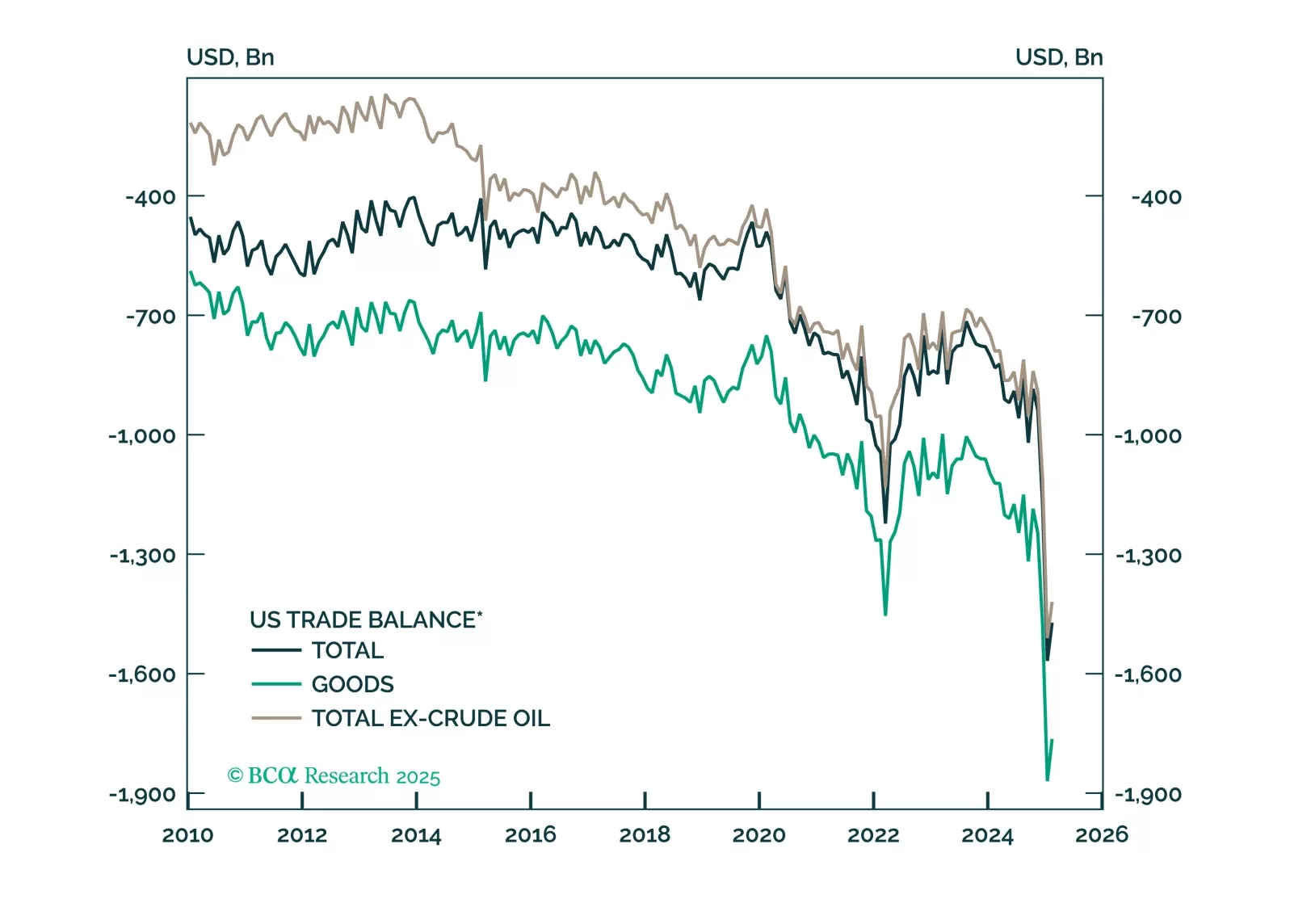

This report looks at the FX implications of the Trump tariffs, and the review of our Q1 trades.

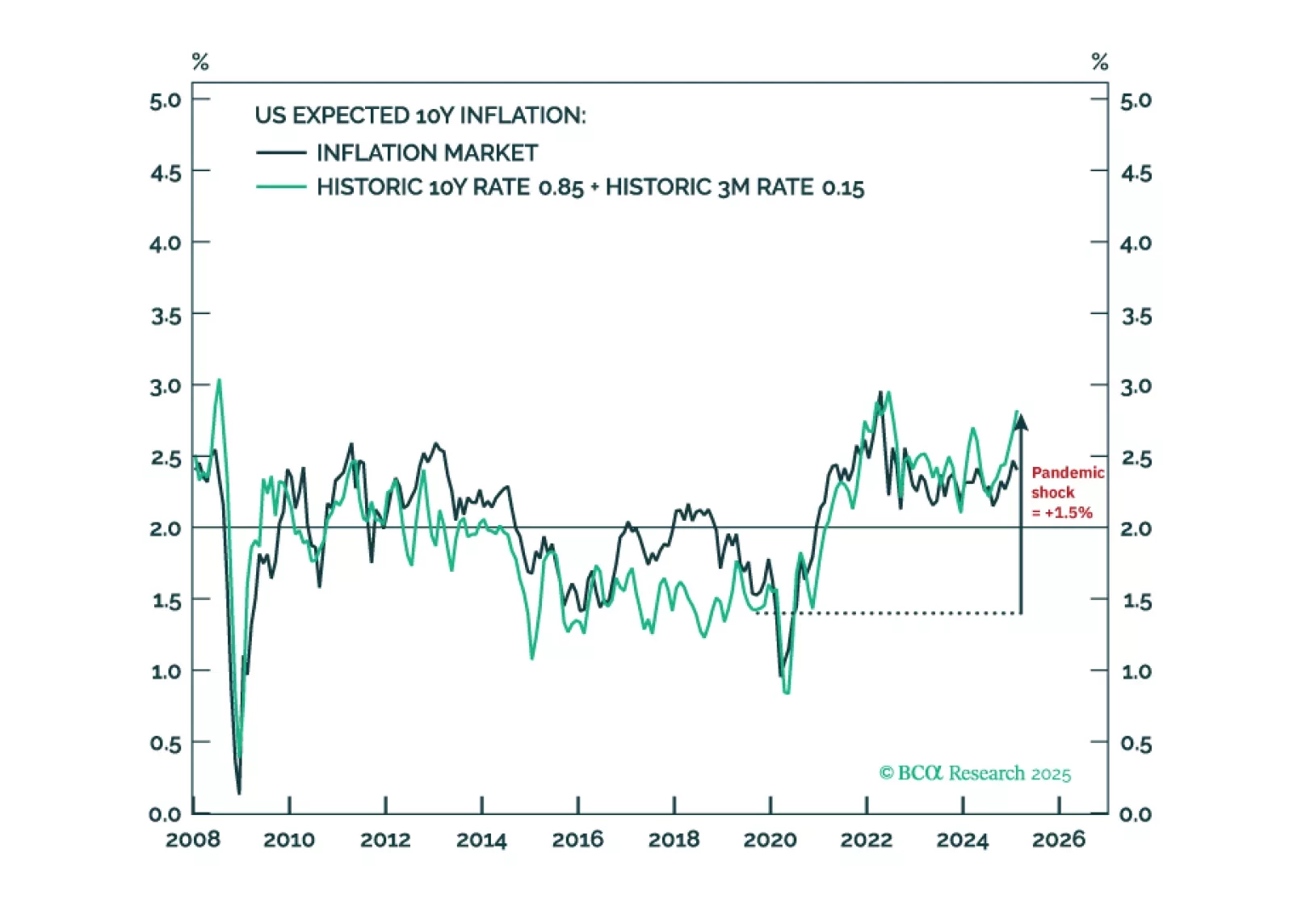

Tariffs will make a difficult job almost impossible. Hitting and sustaining a precise 2 percent inflation target is more about luck than judgement. It requires both the starting point for inflation expectations and any inflation/deflation shock to combine perfectly to 2 percent. While structural inflation expectations in the euro area and Japan could be close to 2 percent, those in the US and the UK will be stuck uncomfortably above 2 percent. We discuss the investment implications for rates and FX. Plus: gold is vulnerable to a tactical reversal.

Given the meetings between the Bank of Japan, the Bank of England, and the Swiss National Bank, our highest convictions views are:

Overweight UK Gilts. It is also time to sell sterling. We are short sterling, as of 1.30.

Underweight JGBs. Correspondingly, be long the yen.

A short CHF/JPY position remains a core holding. Selling GBP/JPY is also a great trade.

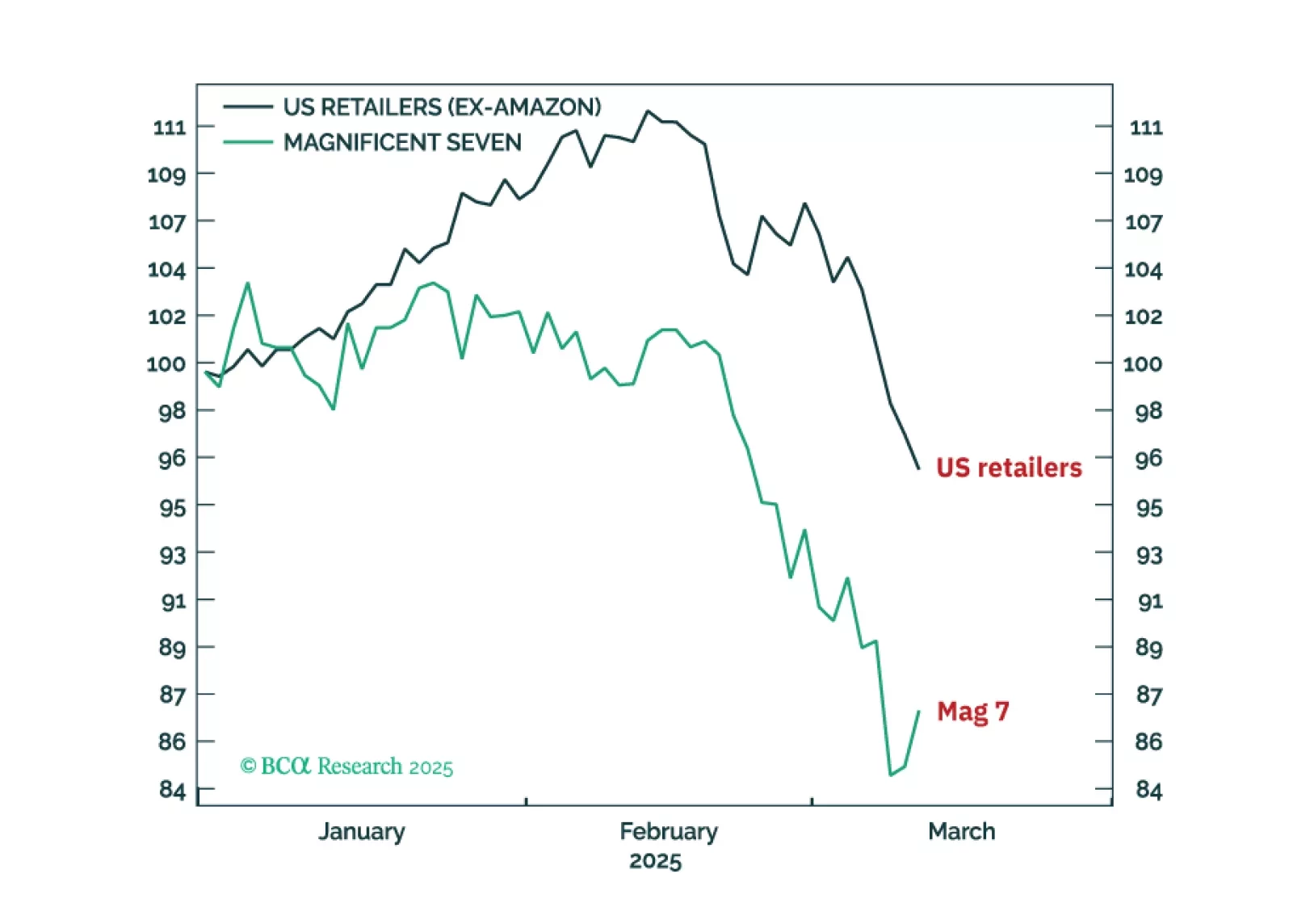

The Trump slump is nearing a temporary reprieve, with a playable countertrend rally in stocks and a tactical rebound in the dollar. Go tactically long USD/SEK. For long-term investors though, the AI bubble still has a lot of air to come out.