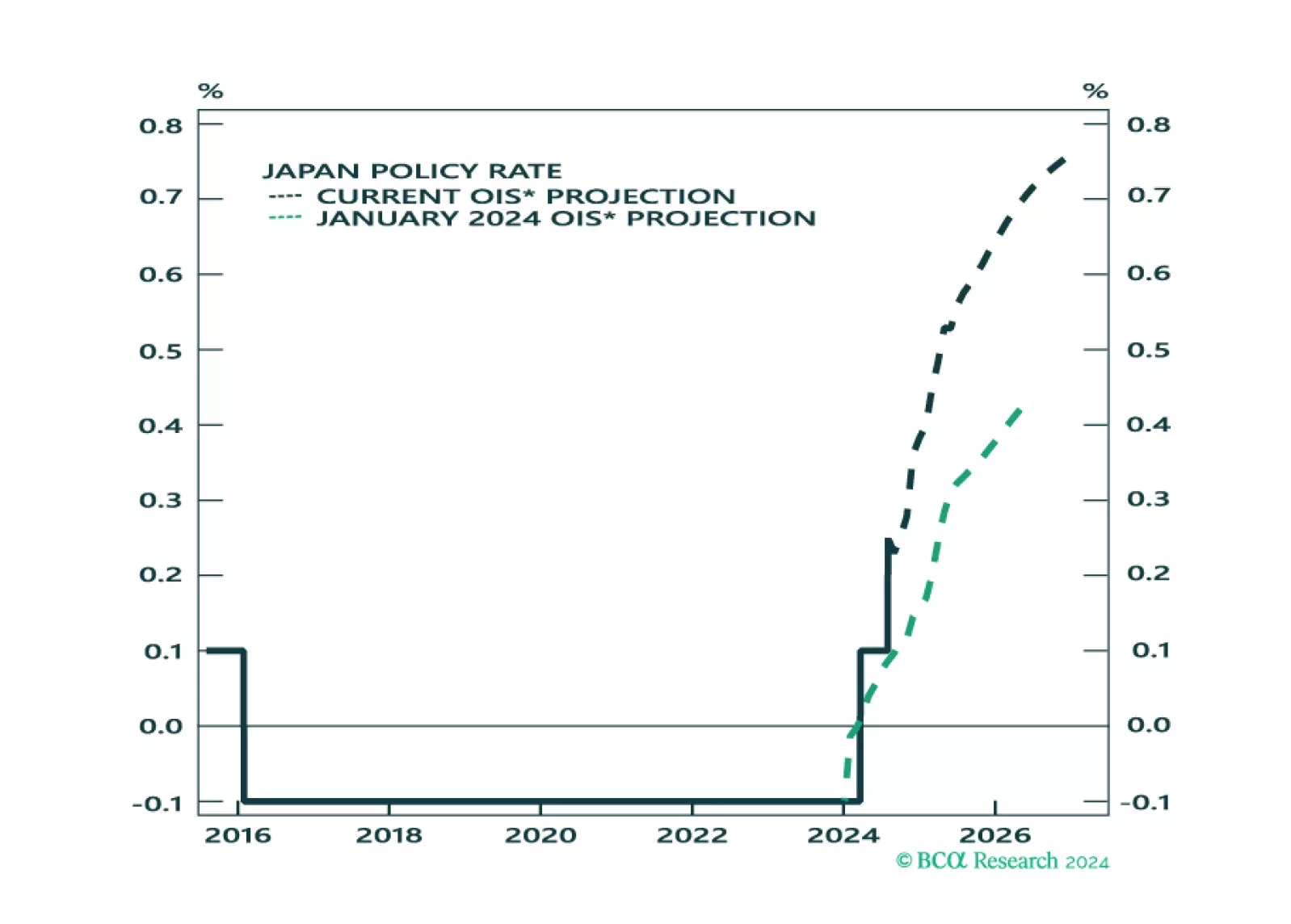

Japanese Yen

We assess the investment implications of the BoJ and Fed meetings, and give our take on the next policy moves. We also assess the impact on asset markets.

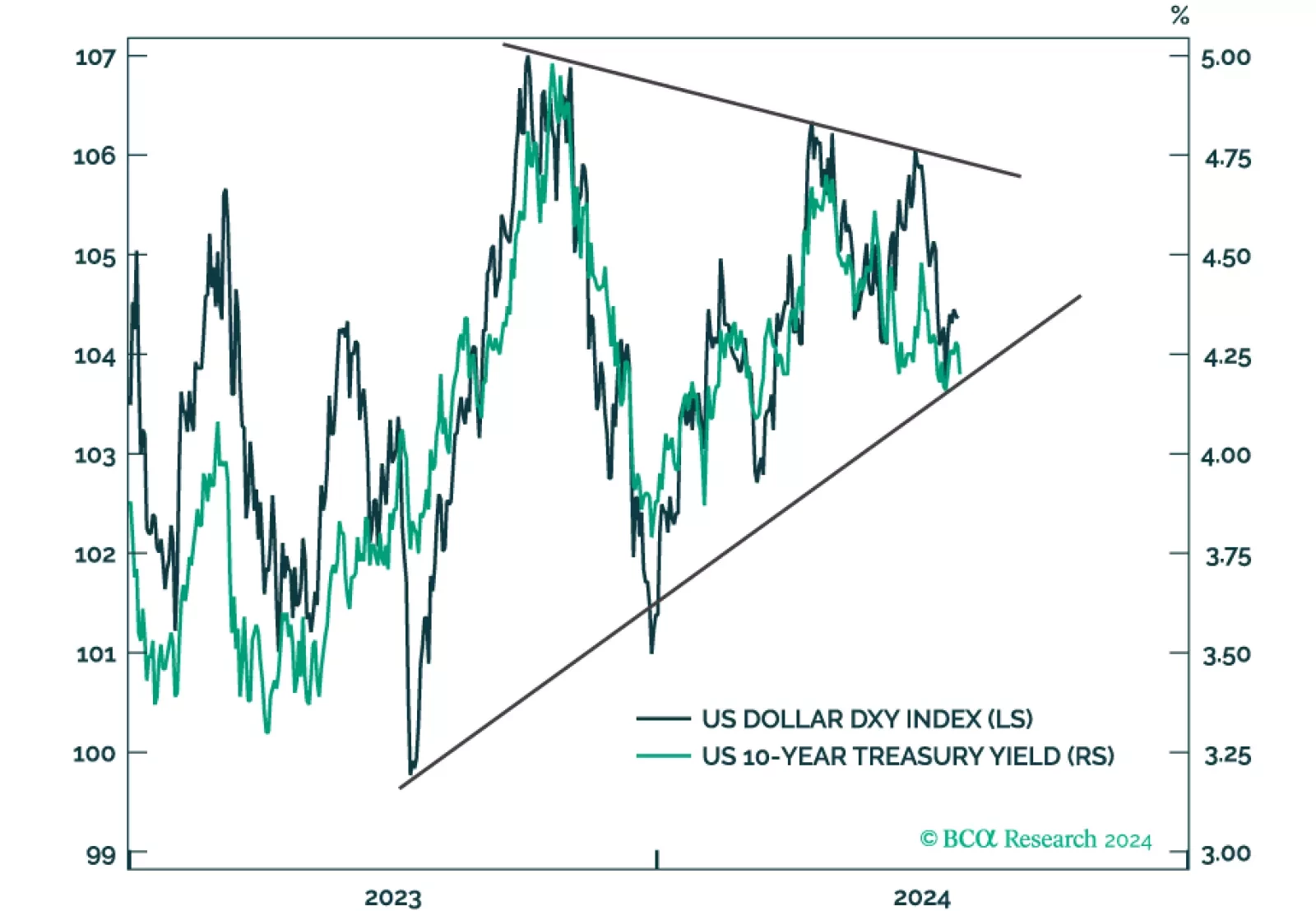

This report takes a look at bond and FX market technical indicators and calibrates the decision to increase portfolio duration and get long the US dollar.

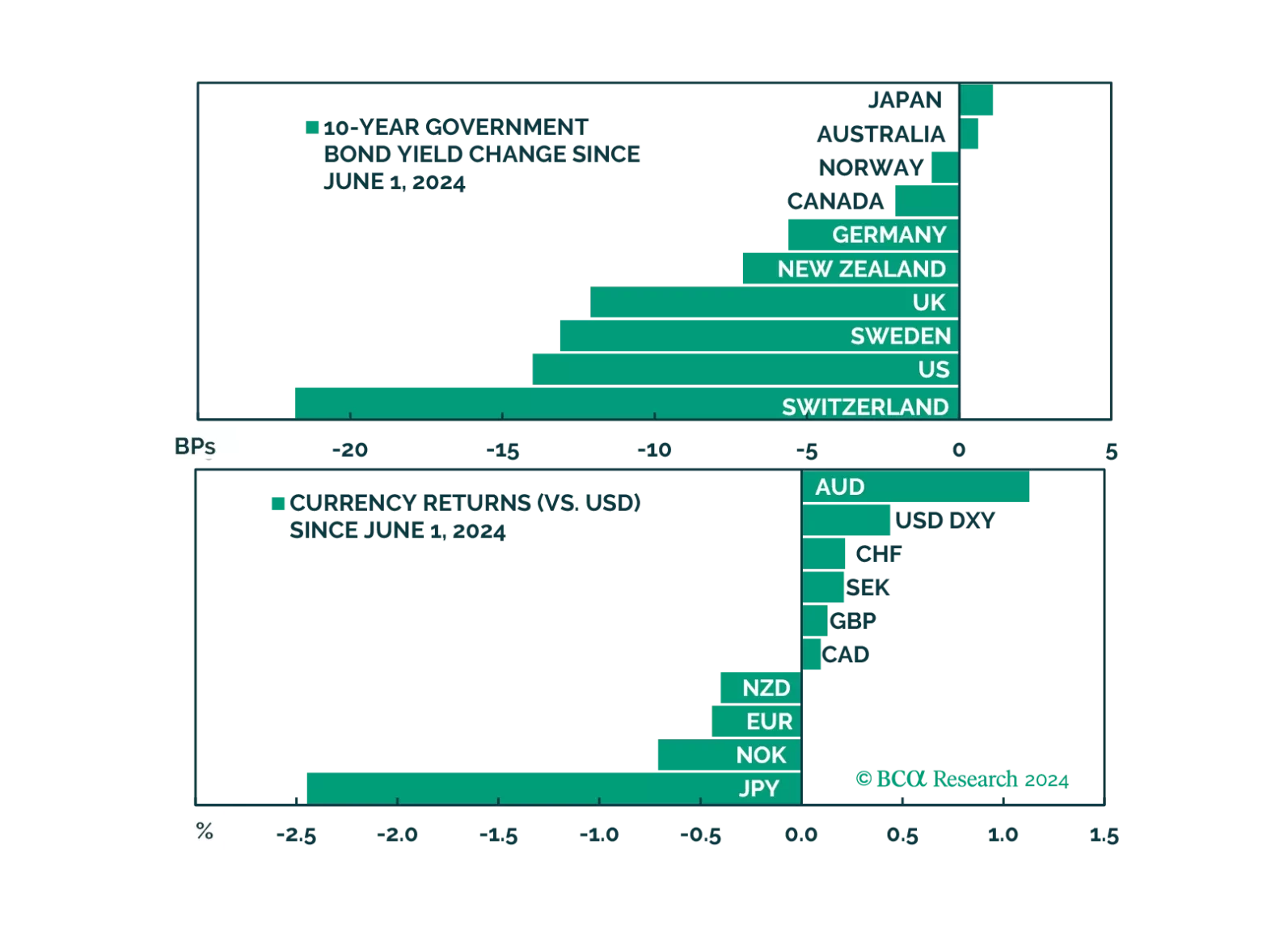

We review some of the key data releases this week that we find have an impact on our currency strategy. Long yen positions make sense today. Long sterling and the euro bets are more of a judgment call, and we will fade any strength in these currencies. This report delves into these nuances, and suggests a few trade ideas.

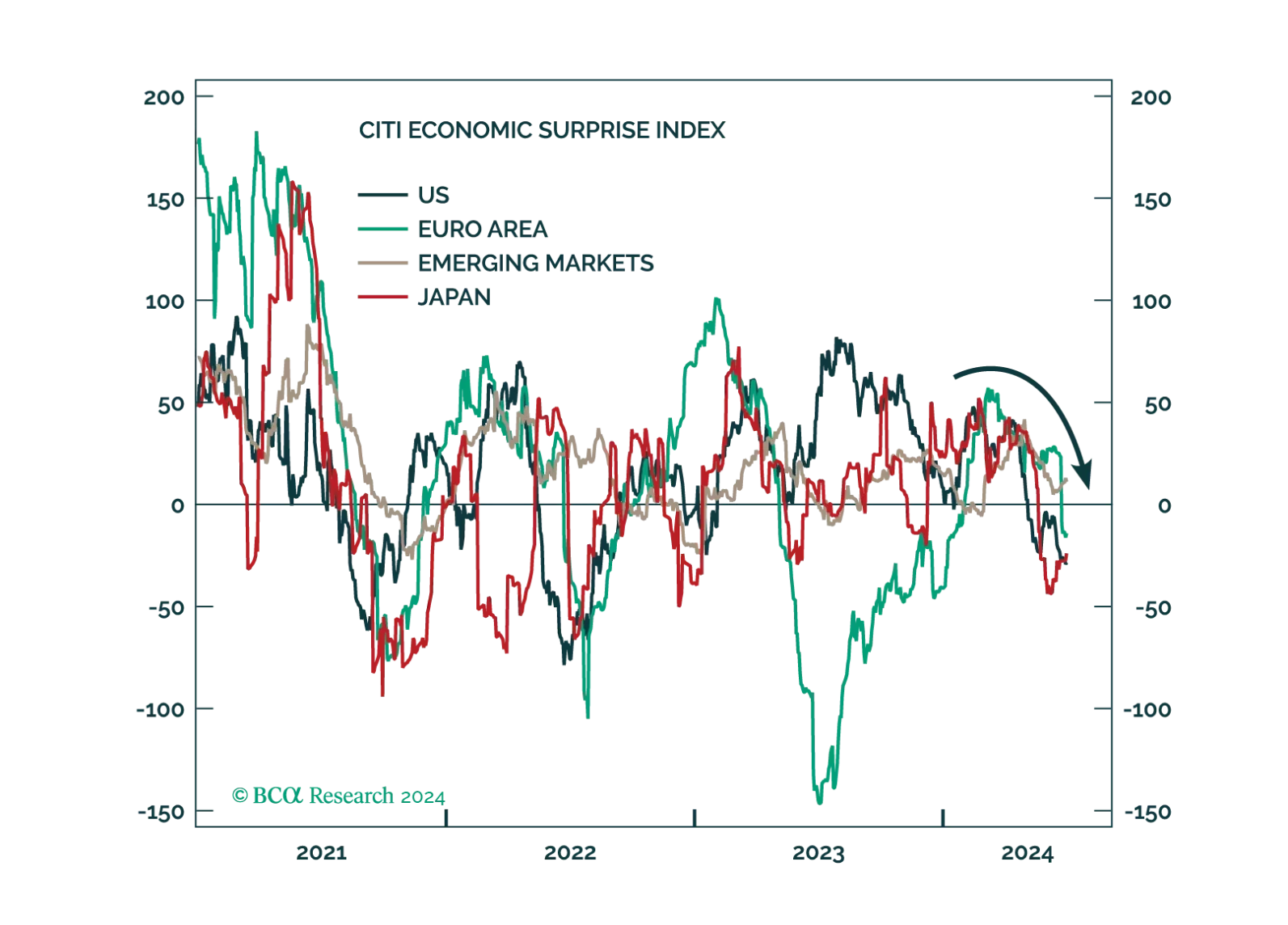

In this week's report, we review the impact of political developments, as well as incoming fundamental data, on our positioning.

Concerns about the global economy have shifted from sticky inflation to faltering growth. Tight monetary policy is finally starting to bite. We suggest increasing portfolio defensiveness.

In this report, we try to gauge how long the exceptional performance of the US can last, but from a more nuanced angle – inflows into US assets and the impact on the dollar and bond yields. Our work suggests that investors should not make any huge bets on the dollar today, but should be short over the longer term (3-5 years). Empirical evidence also suggests you want to be long US bonds into any downturn, relative to global-ex-US duration-matched government securities, but that view becomes less certain if the global economy avoids a downturn in the next few months. What is interesting in this report are high some conviction views across currencies, bonds and precious metals.