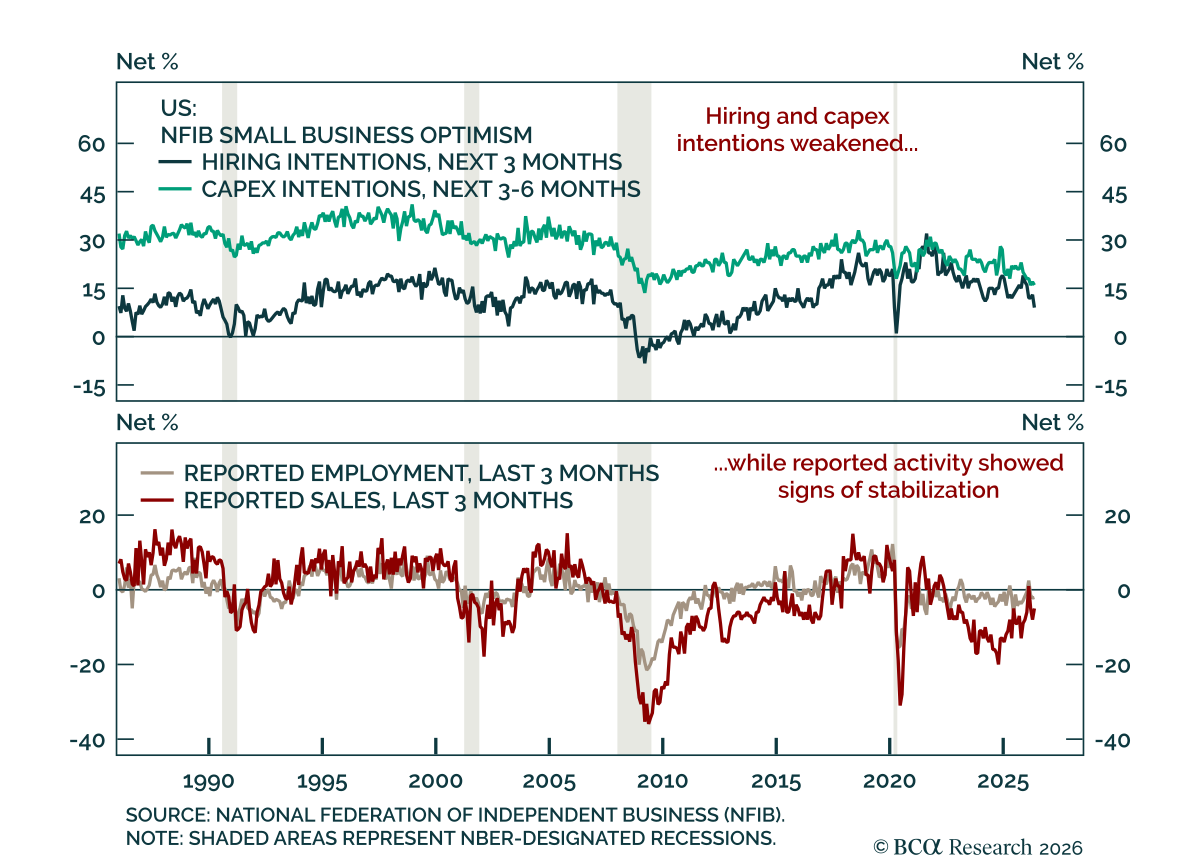

Labor Market

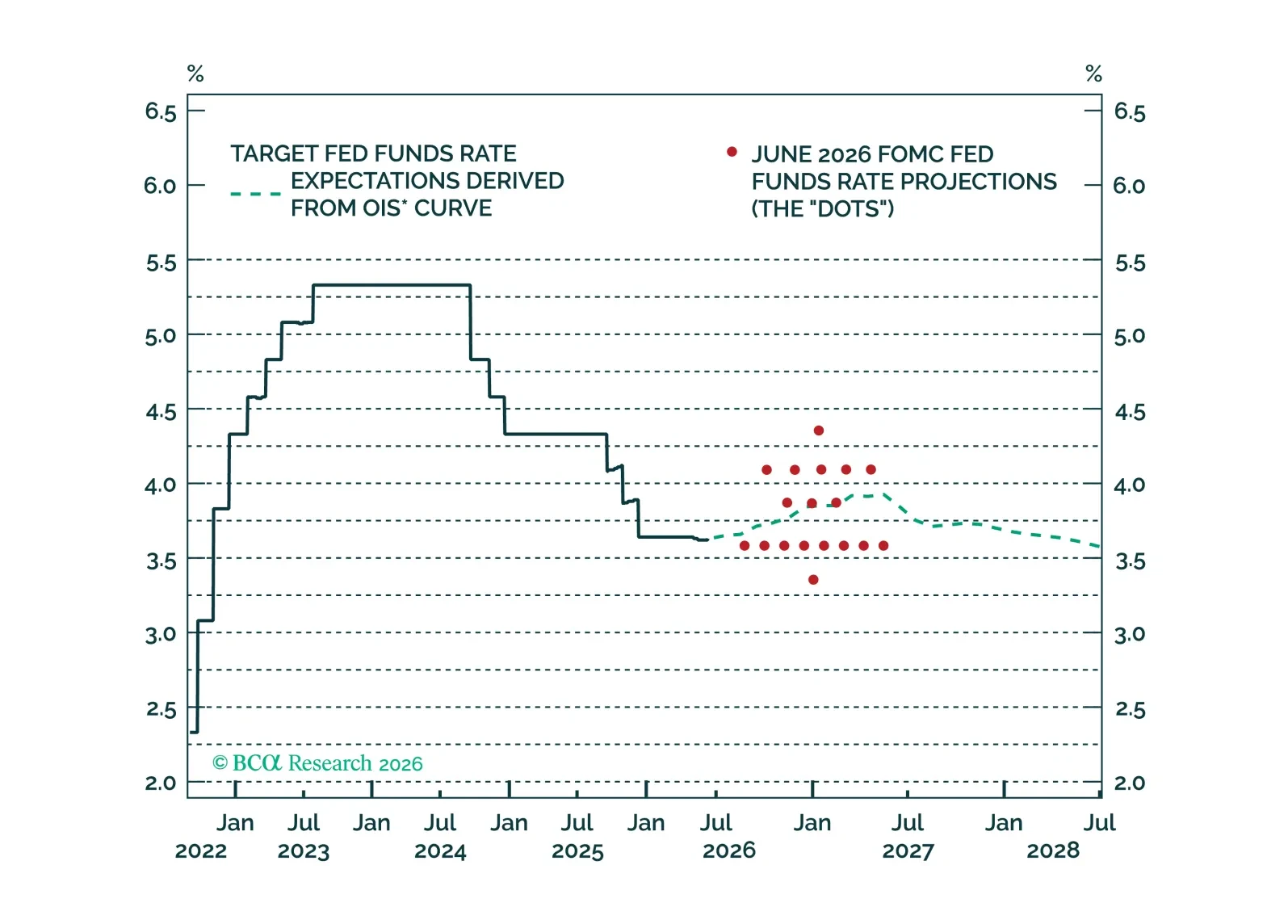

Kevin Warsh announced an ambitious reform agenda for the Federal Reserve. We discuss the potential impact and the current outlook for interest rates.

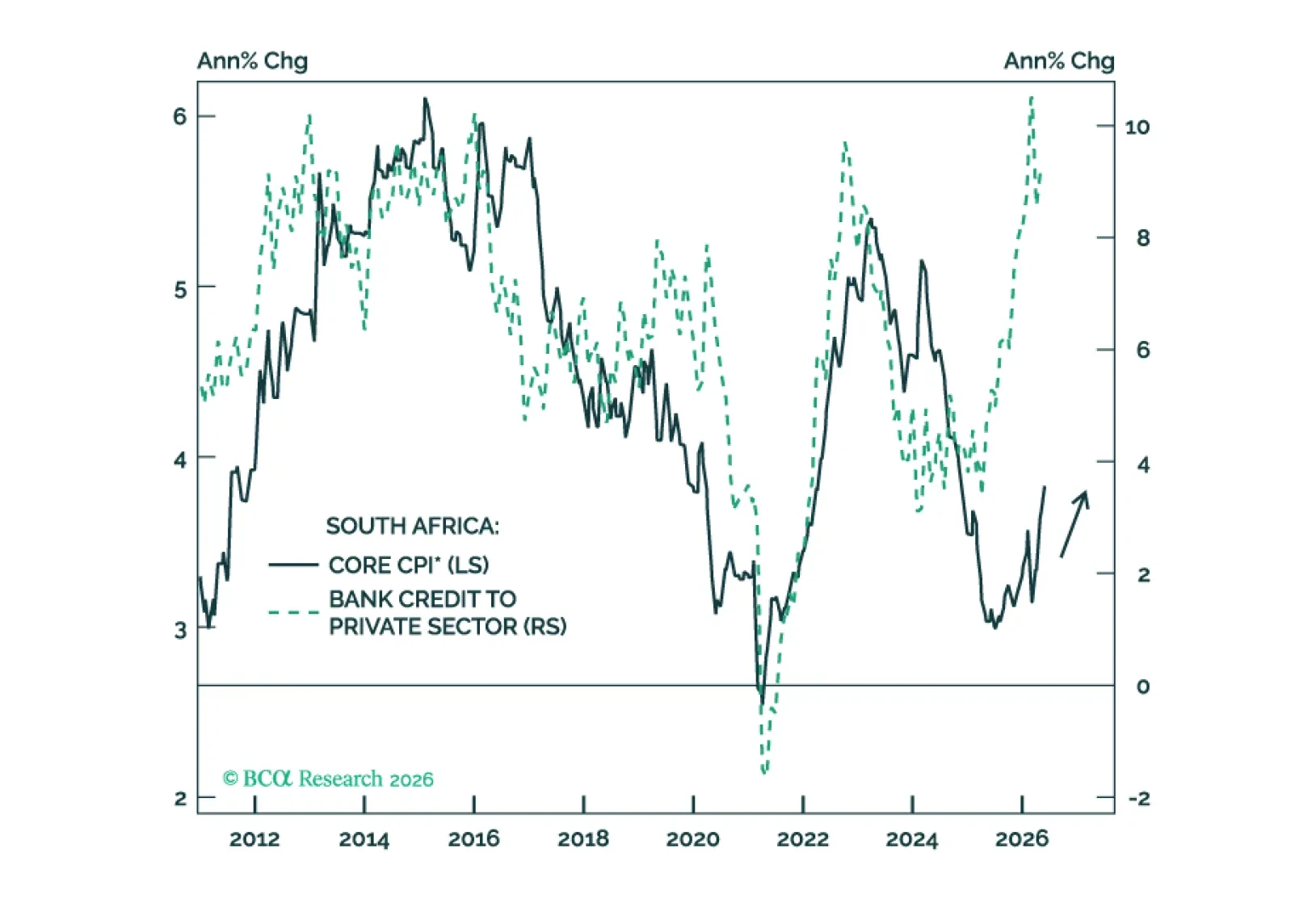

South Africa’s ambitious reform agenda will take time to bear fruit. Meanwhile, the country faces a stagflationary squeeze as inflation rises while growth slows. South African stocks, bonds, and currency are all vulnerable.

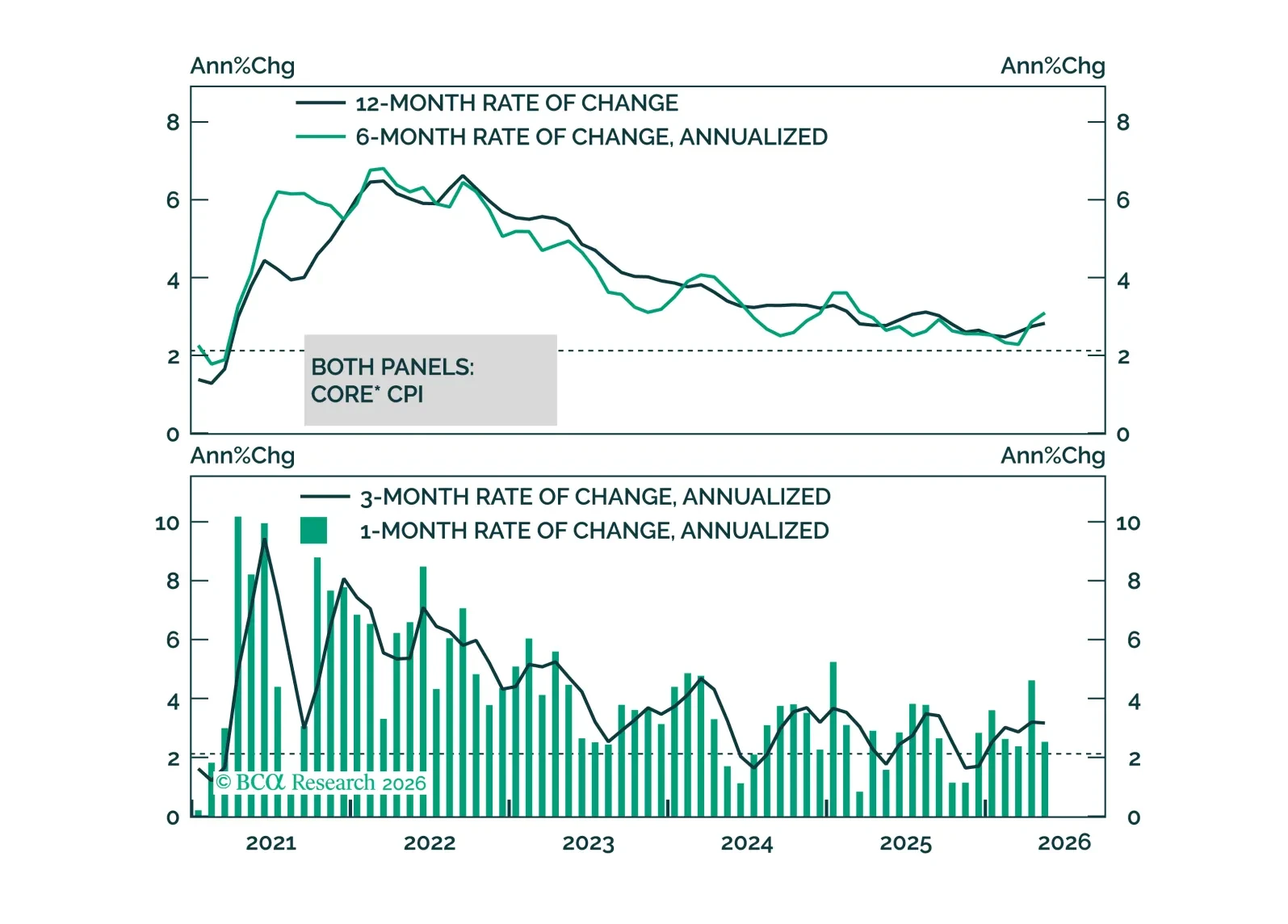

May CPI data show no evidence of passthrough from energy prices to core inflation. This will keep the Fed on hold for the time being.

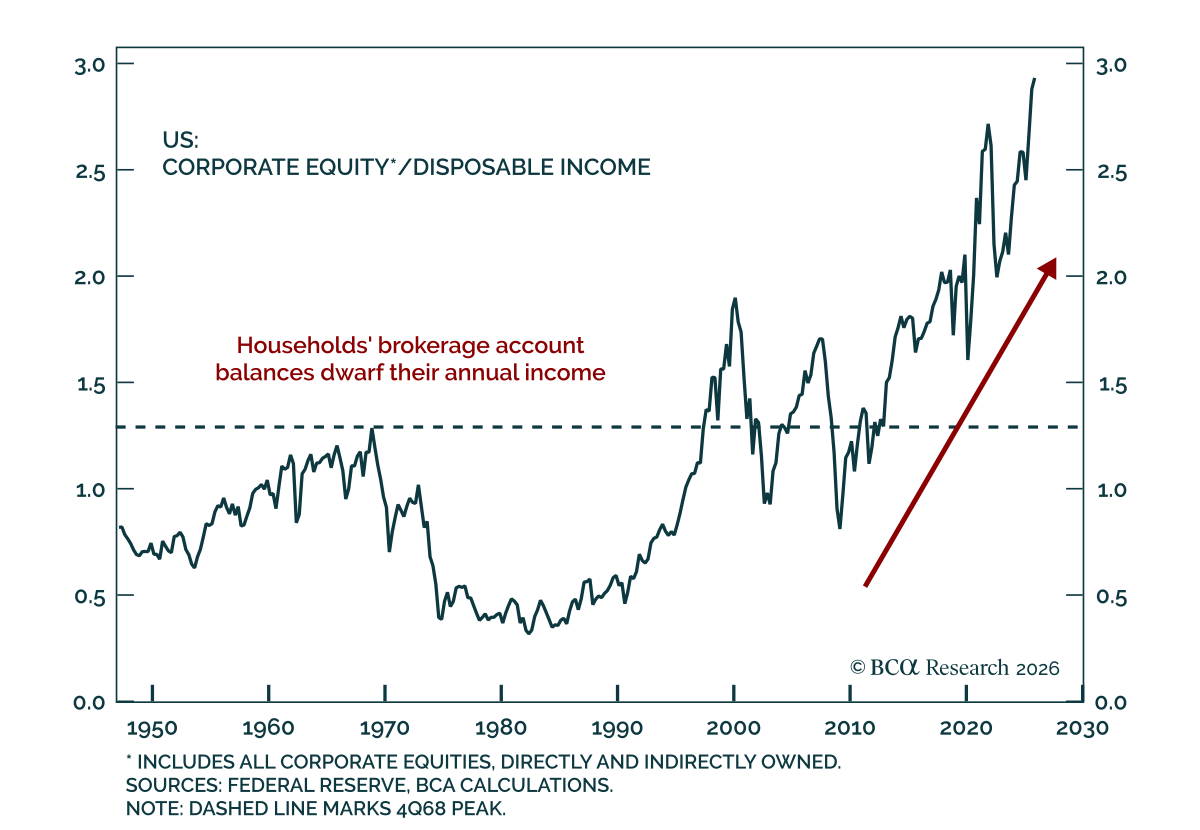

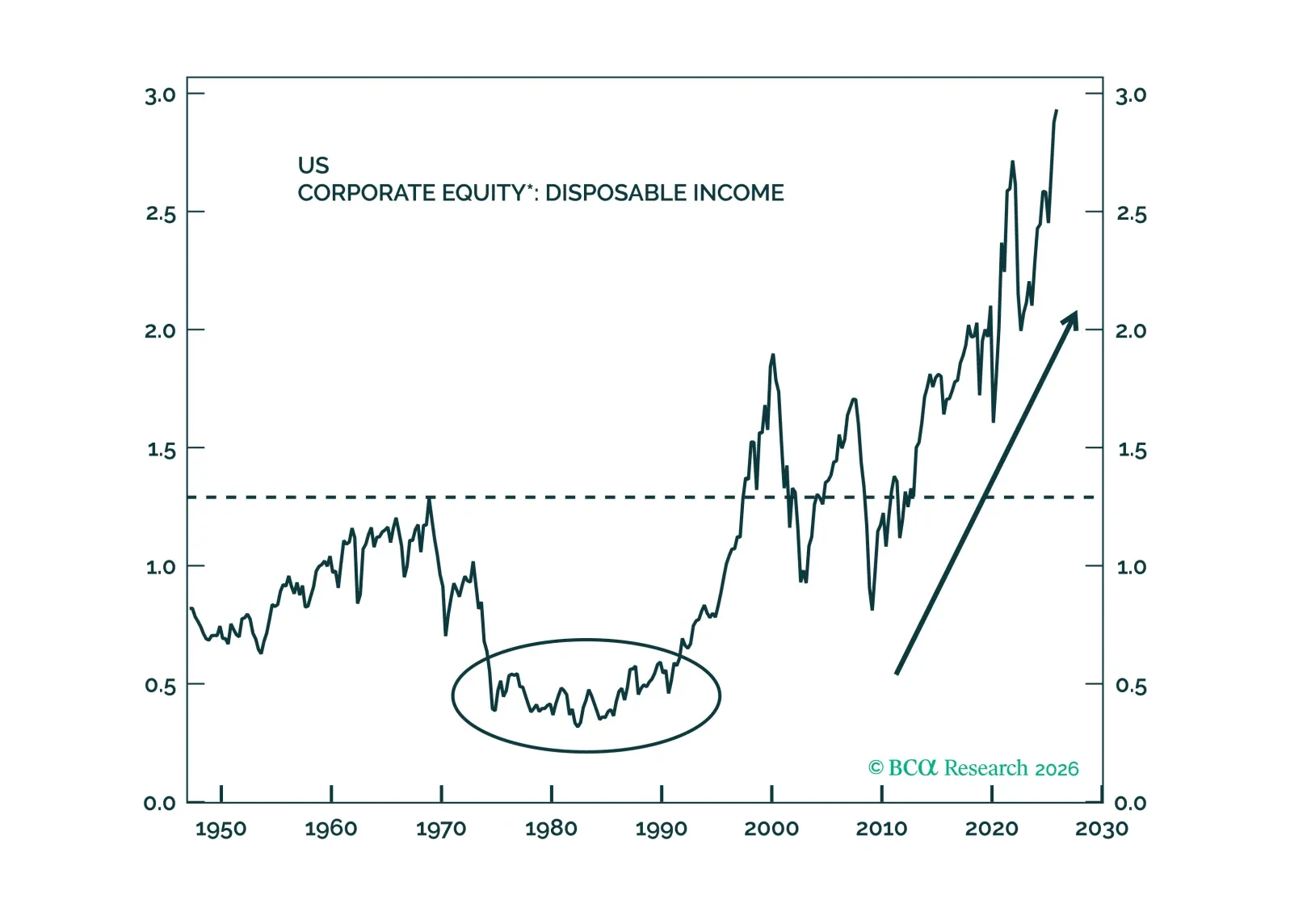

Although the multi-decade surge in the value of households’ equity holdings has made US activity more vulnerable to a stock selloff, the latest income, spending and employment data suggest that consumption growth can carry on at a 2% inflation-adjusted pace.