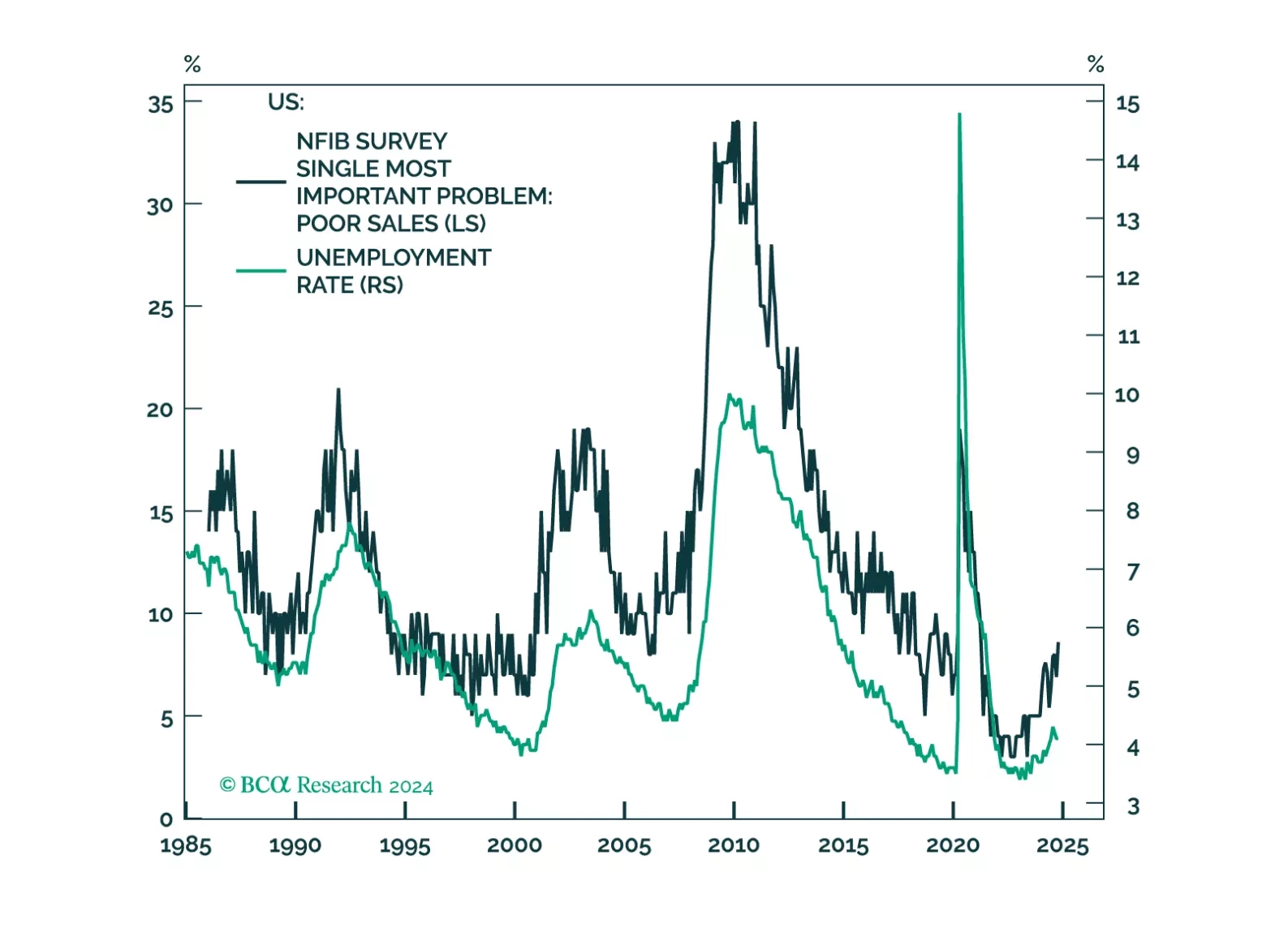

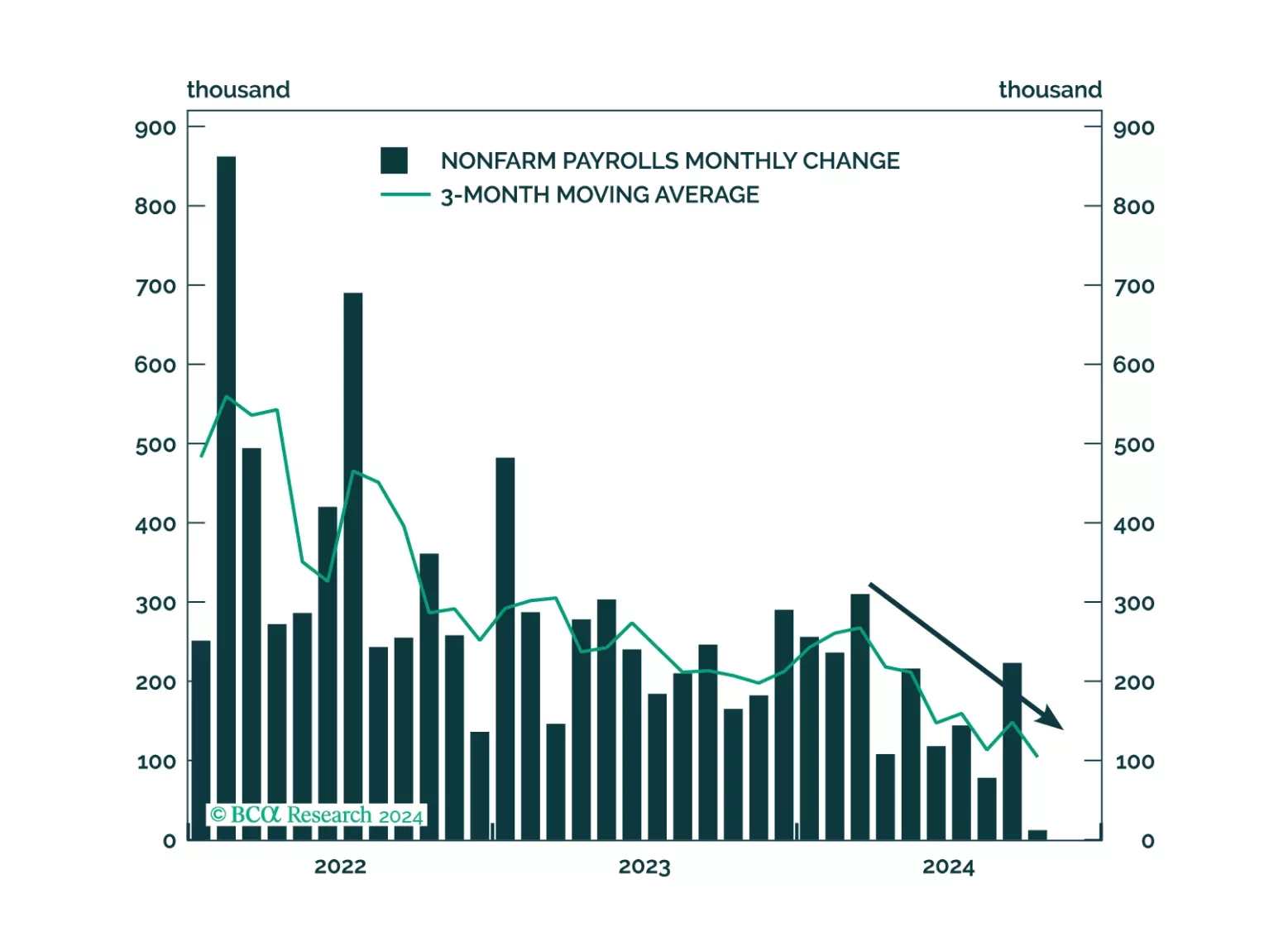

Labor Market

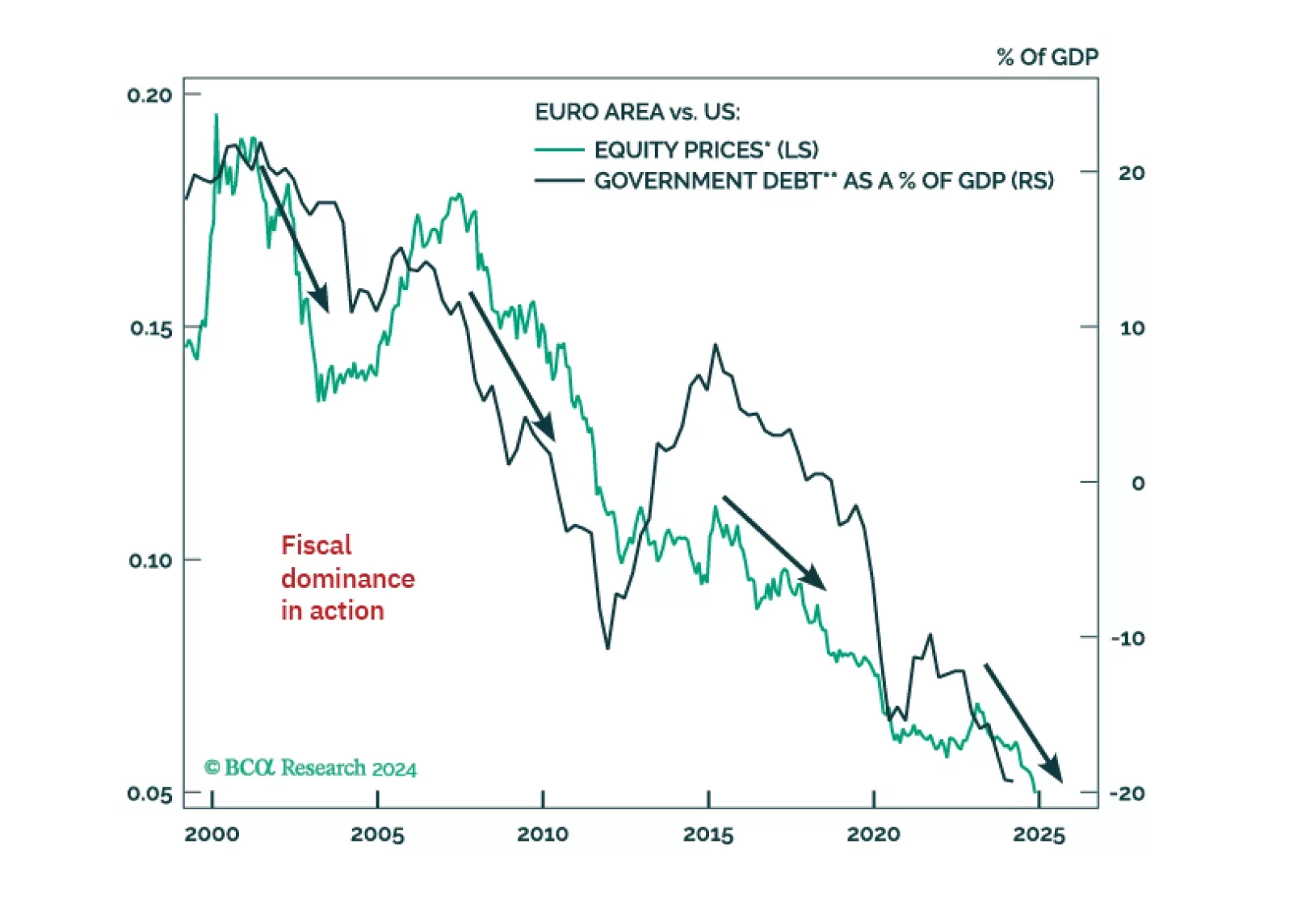

Investors have given up on European assets, which now suffer exceptional discounts to US ones. However, tighter US fiscal policy, the end of Europe’s austerity and deleveraging, the LNG Tsunami about to hit European shores, and the global capex fueled by the Impossible Geopolitical Trinity mean that Europe’s time to shine will soon come back.

The post-COVID recovery has been one of excesses. Government deficits have ballooned, tight labor markets have led to a windfall of consumer spending, and equity valuations have soared on the back of lofty growth expectations. But these excesses will no longer be sustainable in 2025. Our theme for next year is Thin Is Back In. Government budgets, economic growth, and equity valuations will be leaner than investors expect. We discuss this the reasoning behind this macro view and the asset allocation implications that follow from it.

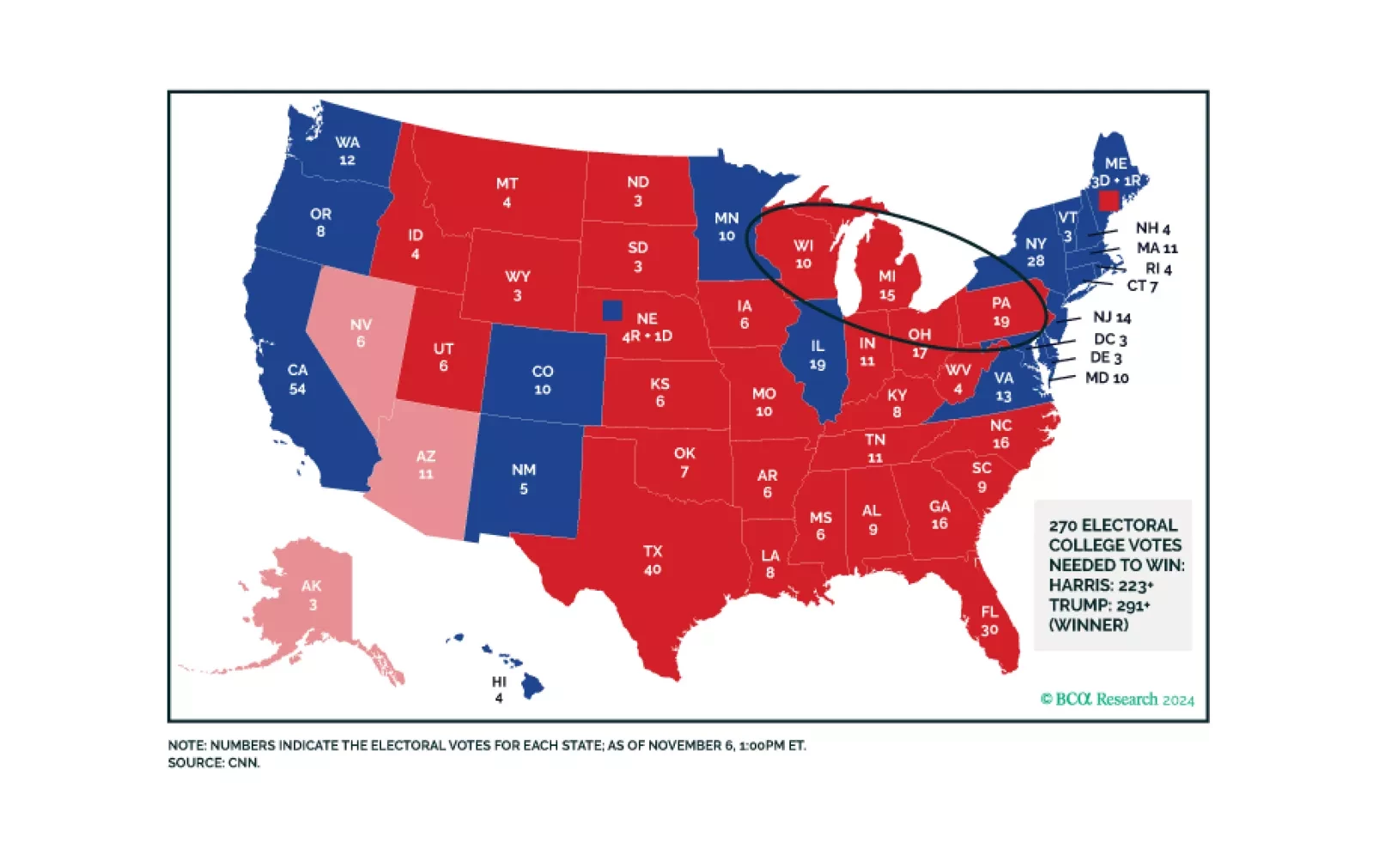

Trump’s resounding victory brings a popular mandate that ensures deregulation and higher trade tariffs. Higher budget deficit and immigration reform are also in the cards as the Republicans look like they may squeak a thin margin in the House of Representatives. Foreign policy will become more unilateral, with US assets outperforming initially.

Trump’s resounding victory brings a popular mandate that ensures deregulation and higher trade tariffs. Higher budget deficit and immigration reform are also in the cards as the Republicans look like they may squeak a thin margin in the House of Representatives. Foreign policy will become more unilateral, with US assets outperforming initially.

The force of the post-election momentum leads us to believe we could be stopped out of our defensive positioning before the week is out, but we still believe in our recession call. If we are eventually stopped out, we will seek a more opportune entry point to bet against risk assets once the election fever runs its course.