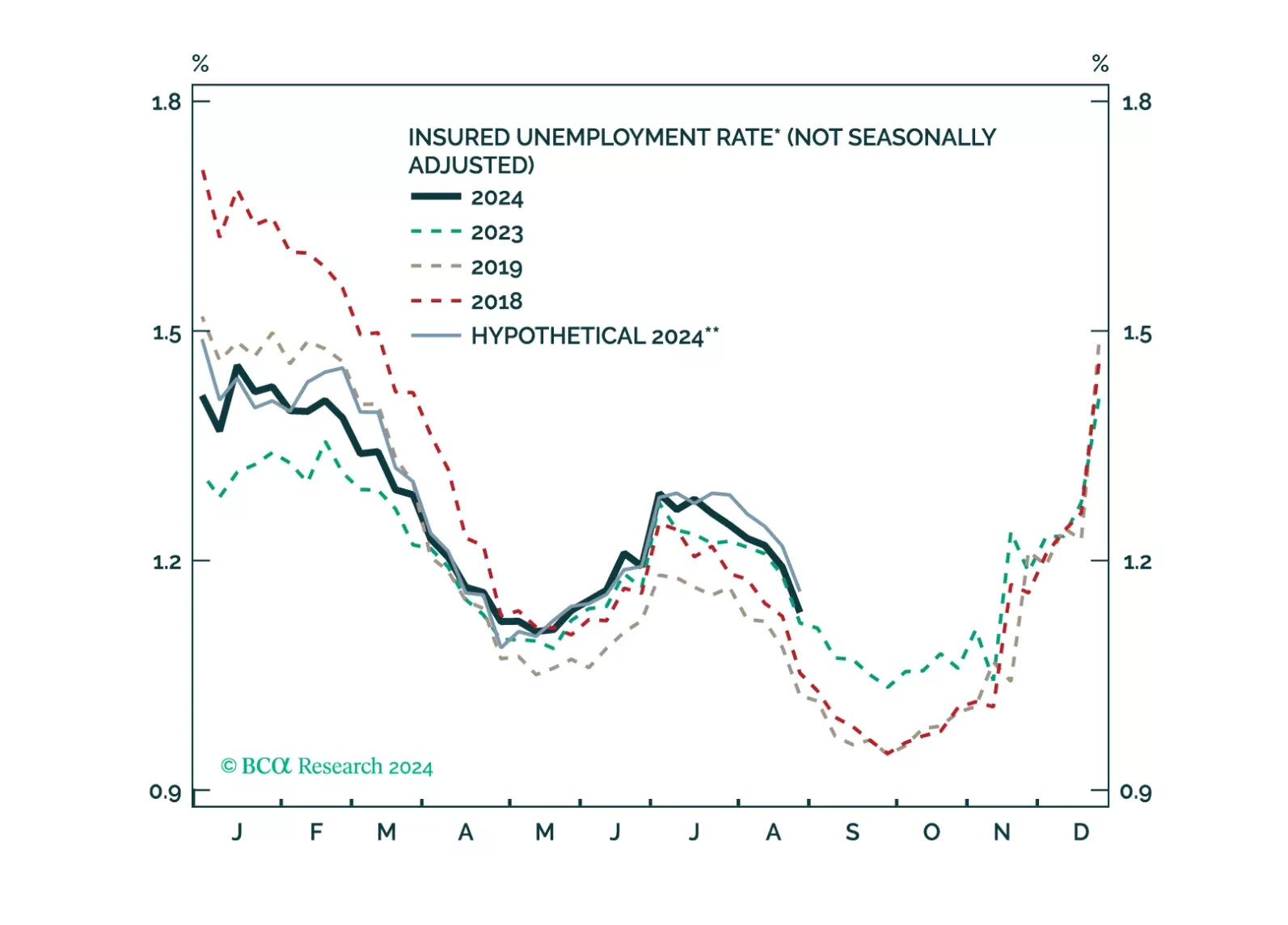

Labor Market

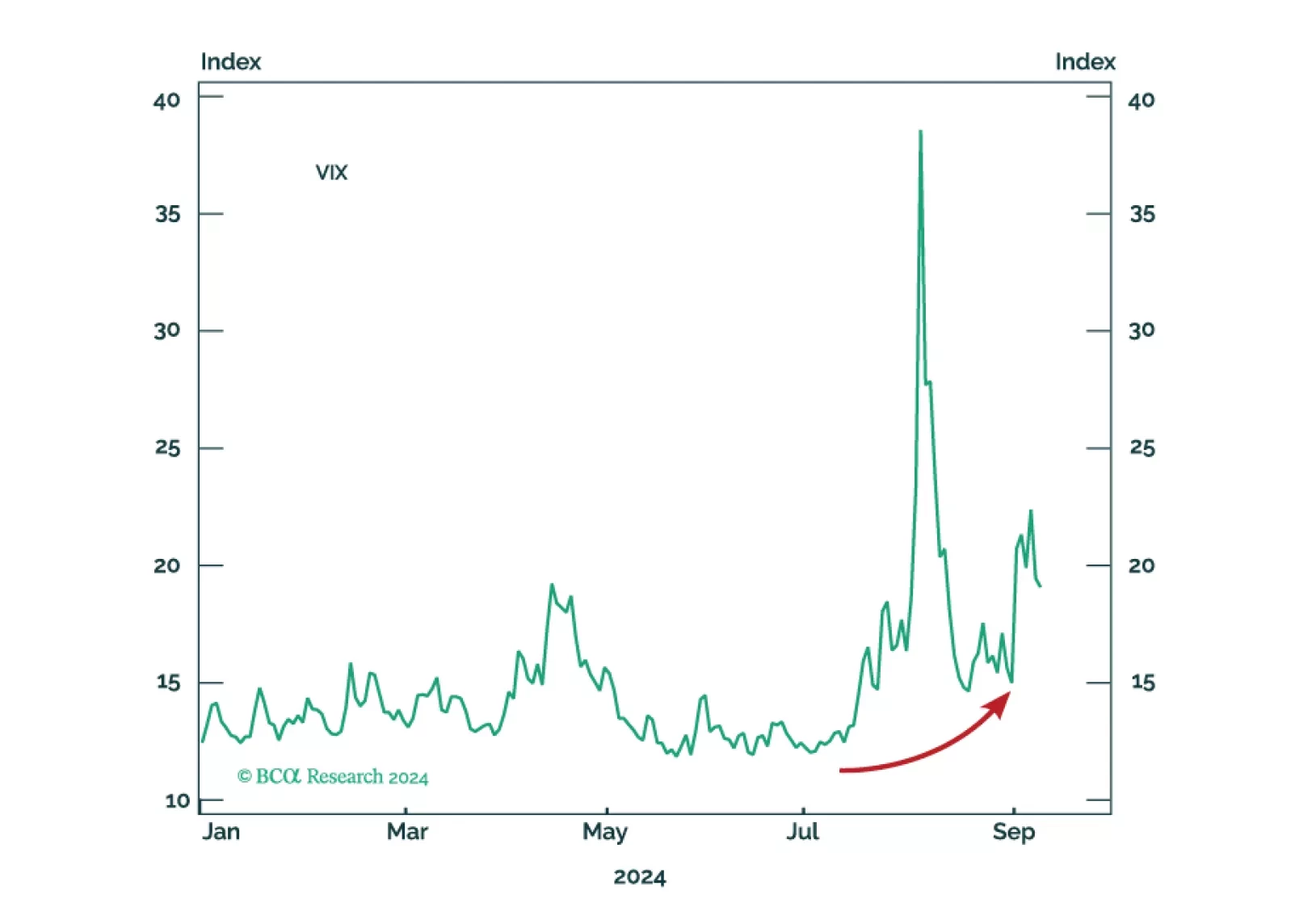

The US suffers from enough imbalances to produce a mild recession. Unfortunately, such a recession could lead to a significant bear market in stocks, just as it did during the very mild 2001 recession.

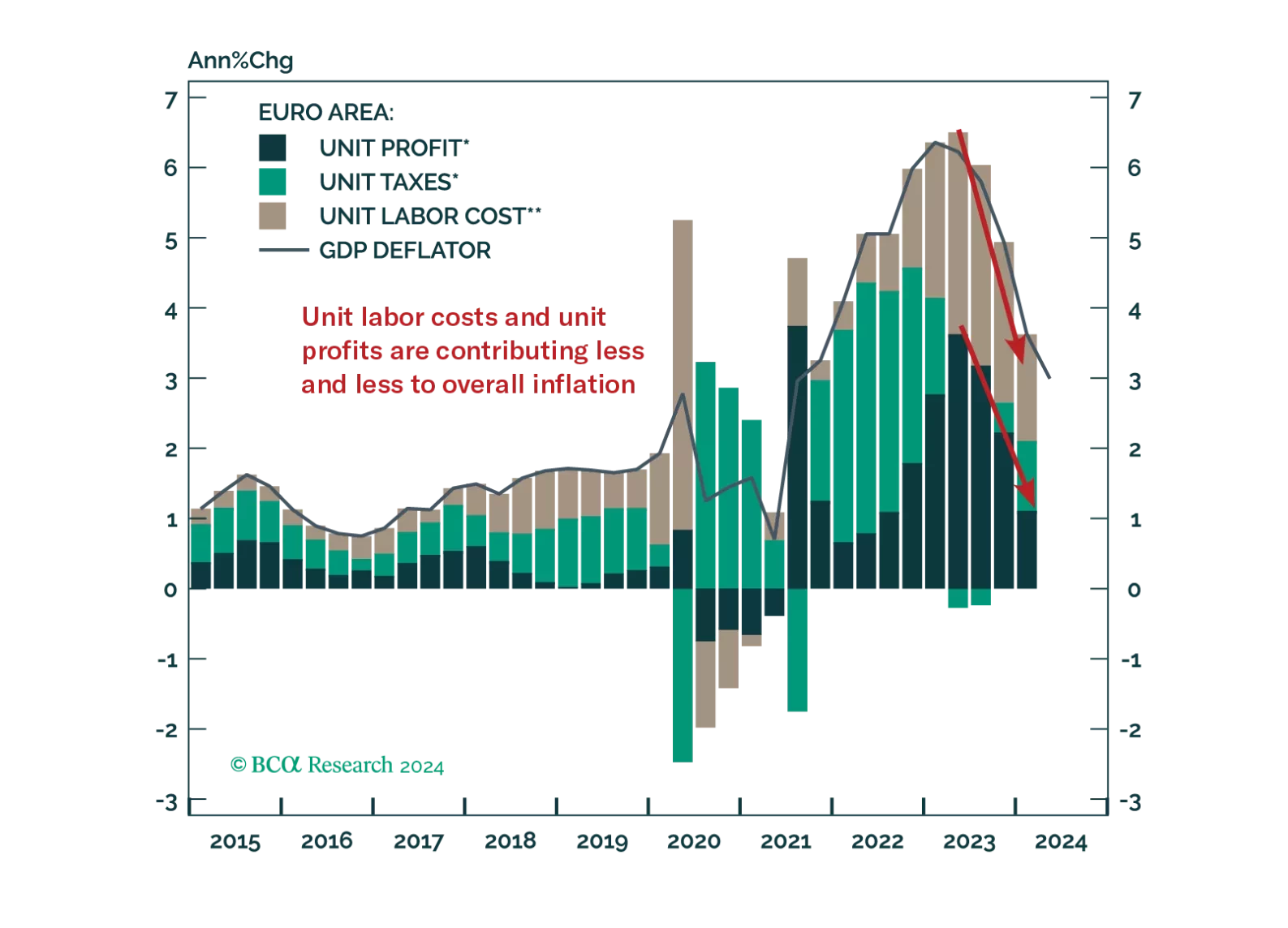

The ECB will cut rates once more this year; however, markets underprice how far it will ease next year.

Some thoughts on this morning’s US claims report and a preview of next week’s FOMC meeting.

Despite the disastrous performance by former President Trump in the debate with Vice President Kamala Harris, there are still paths for him to come back to power. The economy and global instability could flare up anytime between now and election day, while quirks in the Electoral College ensure that the election will be close. The race is still competitive and policy uncertainty and volatility will be elevated.