Labor Market

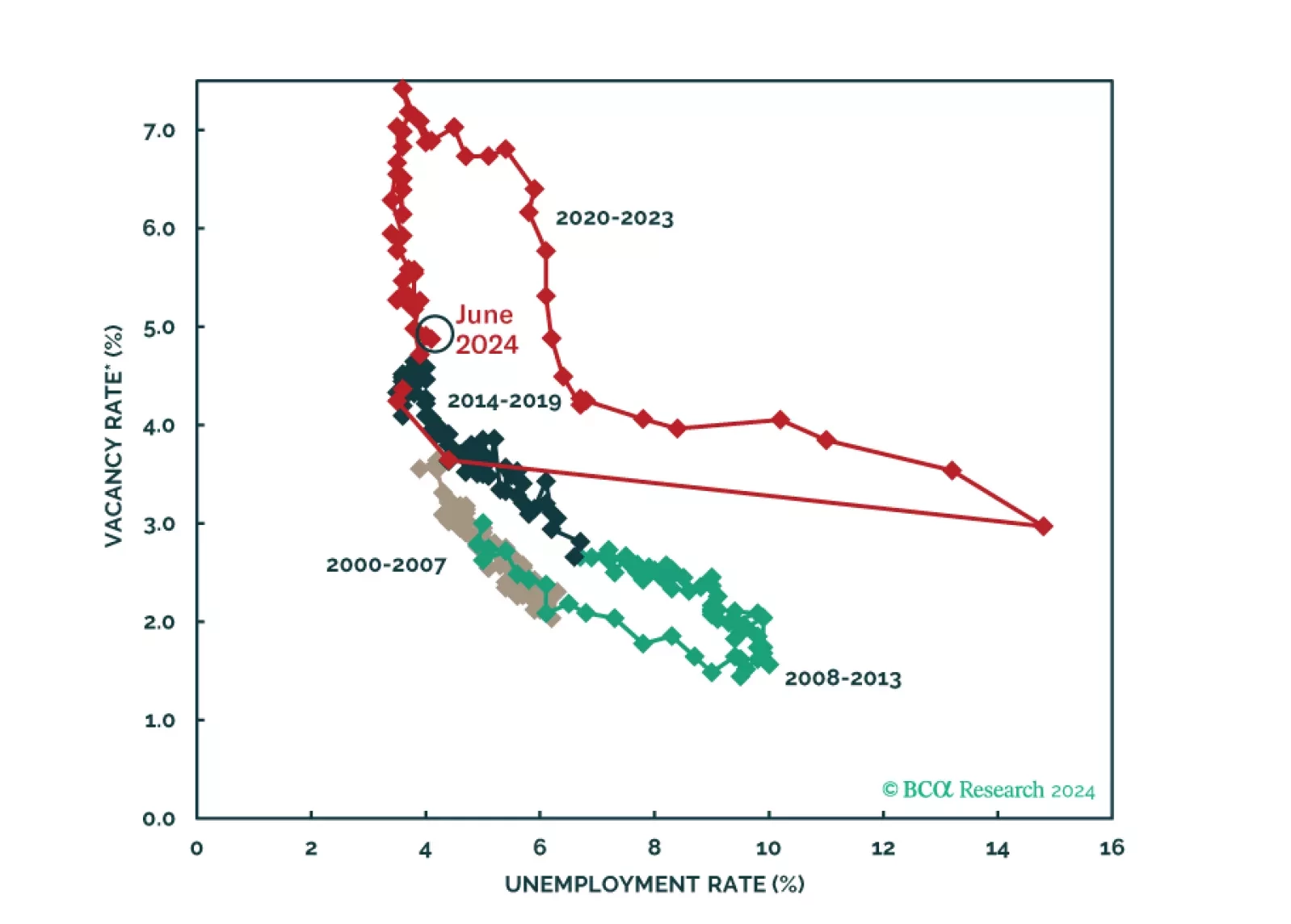

July nonfarm payrolls expanded by 114 thousand workers, a sharp slowdown from June’s downwardly revised 179 thousand, and significantly disappointing expectations of 175 thousand. The unemployment rate unexpectedly edged 0.2ppt higher to 4.3% in July,…

The Sahm Rule – a widely watched real-time recession indicator – signals the early stages of a recession when the 3-month moving average of the unemployment rate rises at least half a percentage point above its past 12-month low. The surprise rise in the…

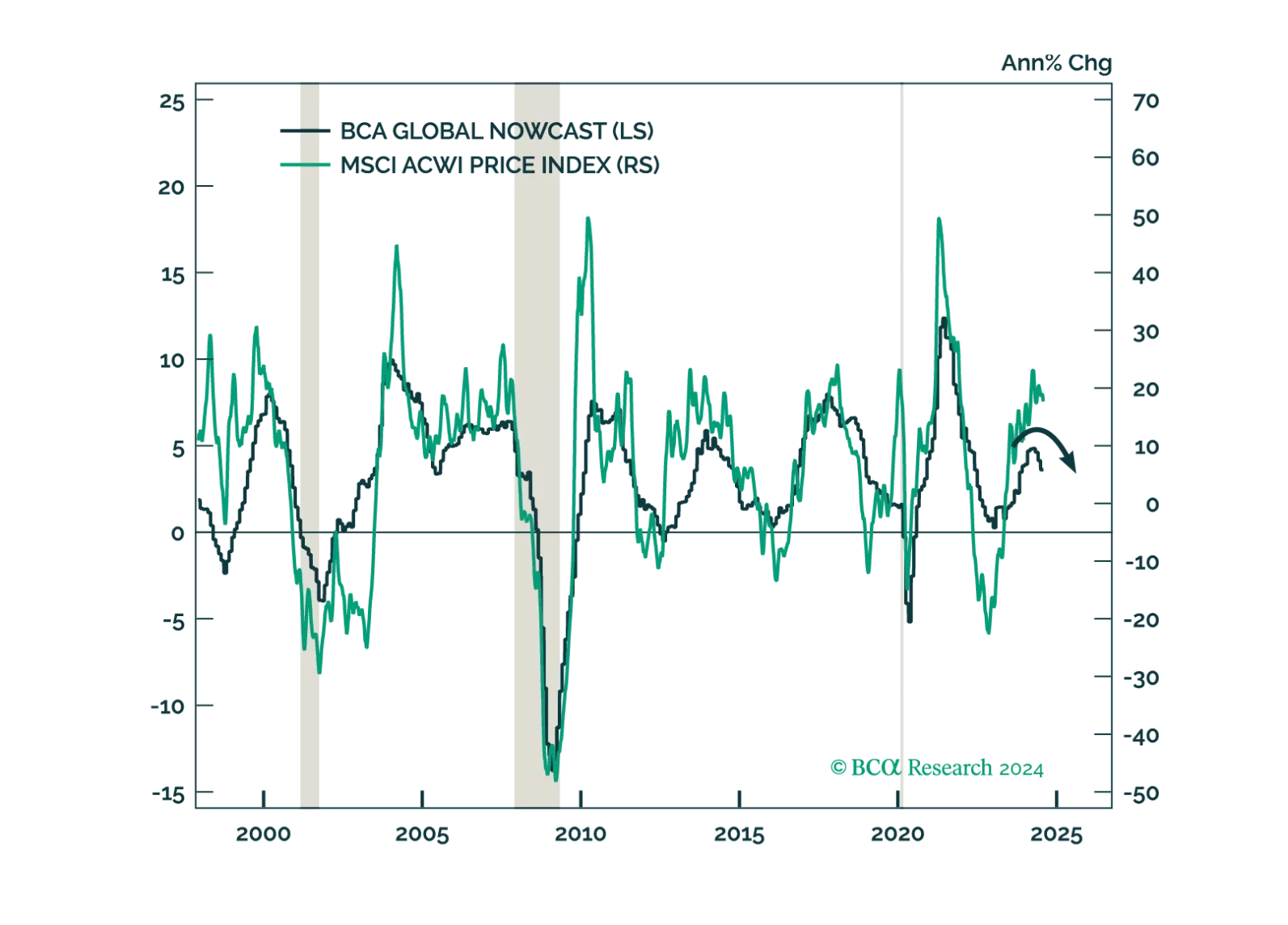

According to BCA Research’s Global Asset Allocation service, there are clear signs that growth is weakening. BCA’s Global Nowcast has been slowing for three months. Behind this slowdown is the fact that the US consumer – the biggest factor keeping growth…

The market is pricing in a soft landing, but we see growing signs that the global economy is faltering. Investors should be defensively positioned.

FOMC members unanimously voted in favor of keeping rates on hold in July but signaled that a September cut is on the table. Inflationary pressures have indeed continued to ease over the past several months. Notably, the Employment Cost Index (ECI) – the…

The Bank of Japan hiked its policy rate by 15 bps from 0.10% to 0.25% on Wednesday, and announced further quantitative tightening, reducing its pace of monthly bond buying from JPY 6 trillion to JPY 3 trillion. While the central bank had previously…

The Fed kept rates steady today, but teed up an initial rate cut in September while putting more emphasis on the employment side of its dual mandate.

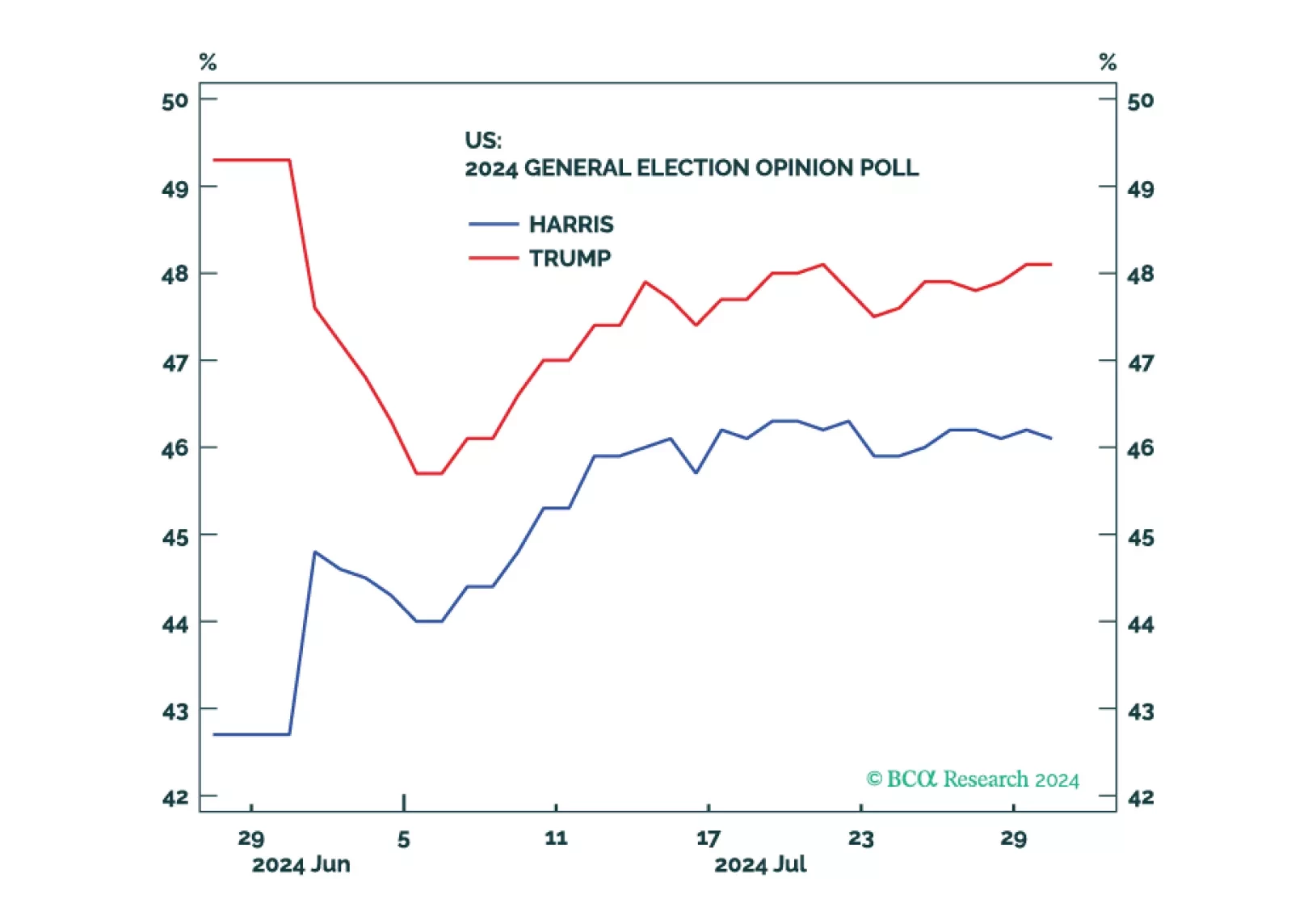

Republicans are favored but the election is still competitive. Equities, corporate credit, and cyclical sectors will fall until policy uncertainty is reduced.

US job openings grew by 8.18 million in June, exceeding expectations of 8 million, but below May’s 8.23 million openings. The pro-cyclical manufacturing sector accounted for the largest drag, withdrawing 100 thousand openings, or one-sixth of its May total.…

Eurozone GDP surprised to the upside in Q2, growing by 0.3% q/q annualized against expectations of 0.2%. Stronger-than-expected expansions in France (0.3% q/q vs 0.2%) and Spain (0.8% q/q vs 0.5%), as well as steady growth in Italy (0.2% q/q), offset a…