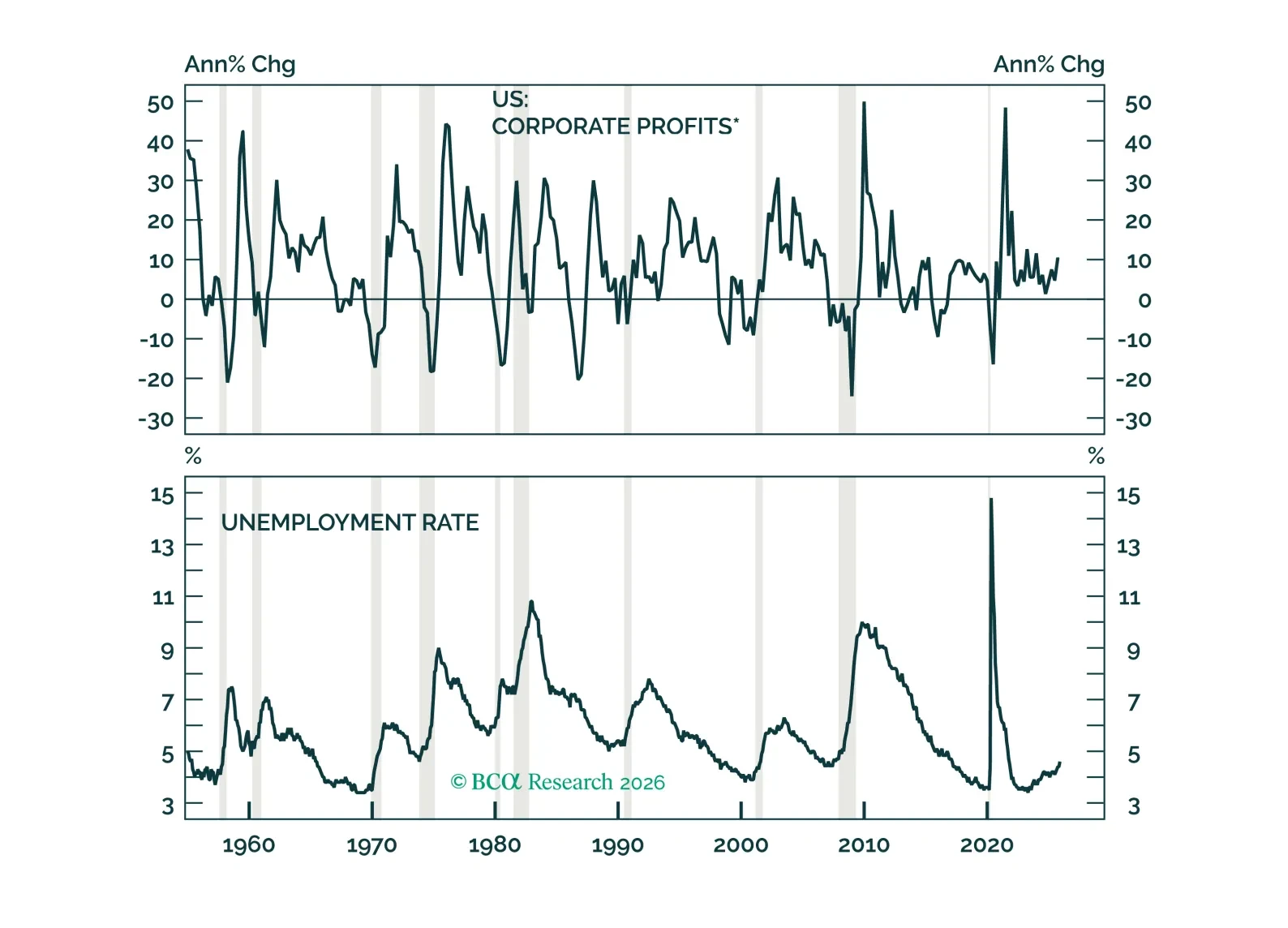

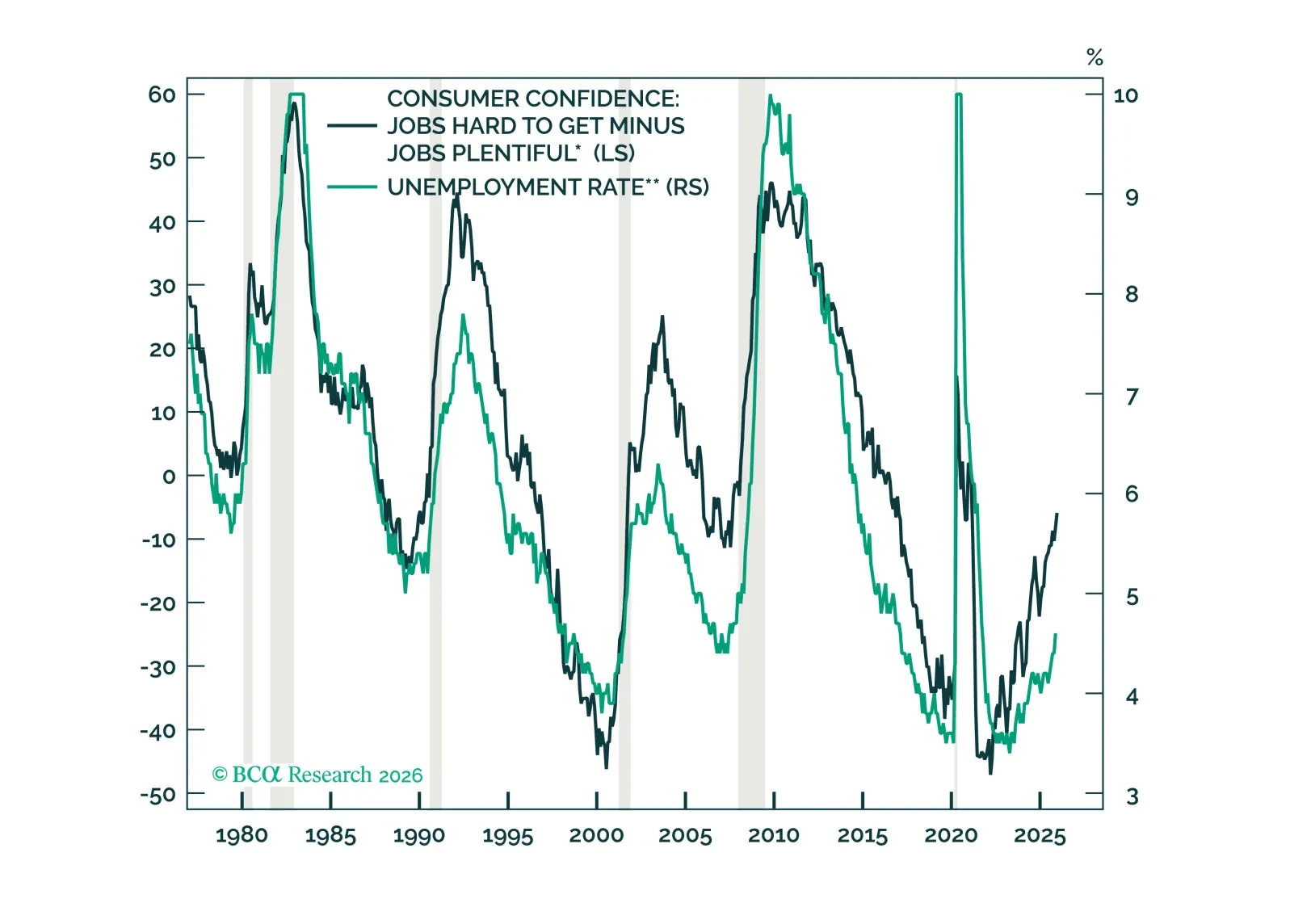

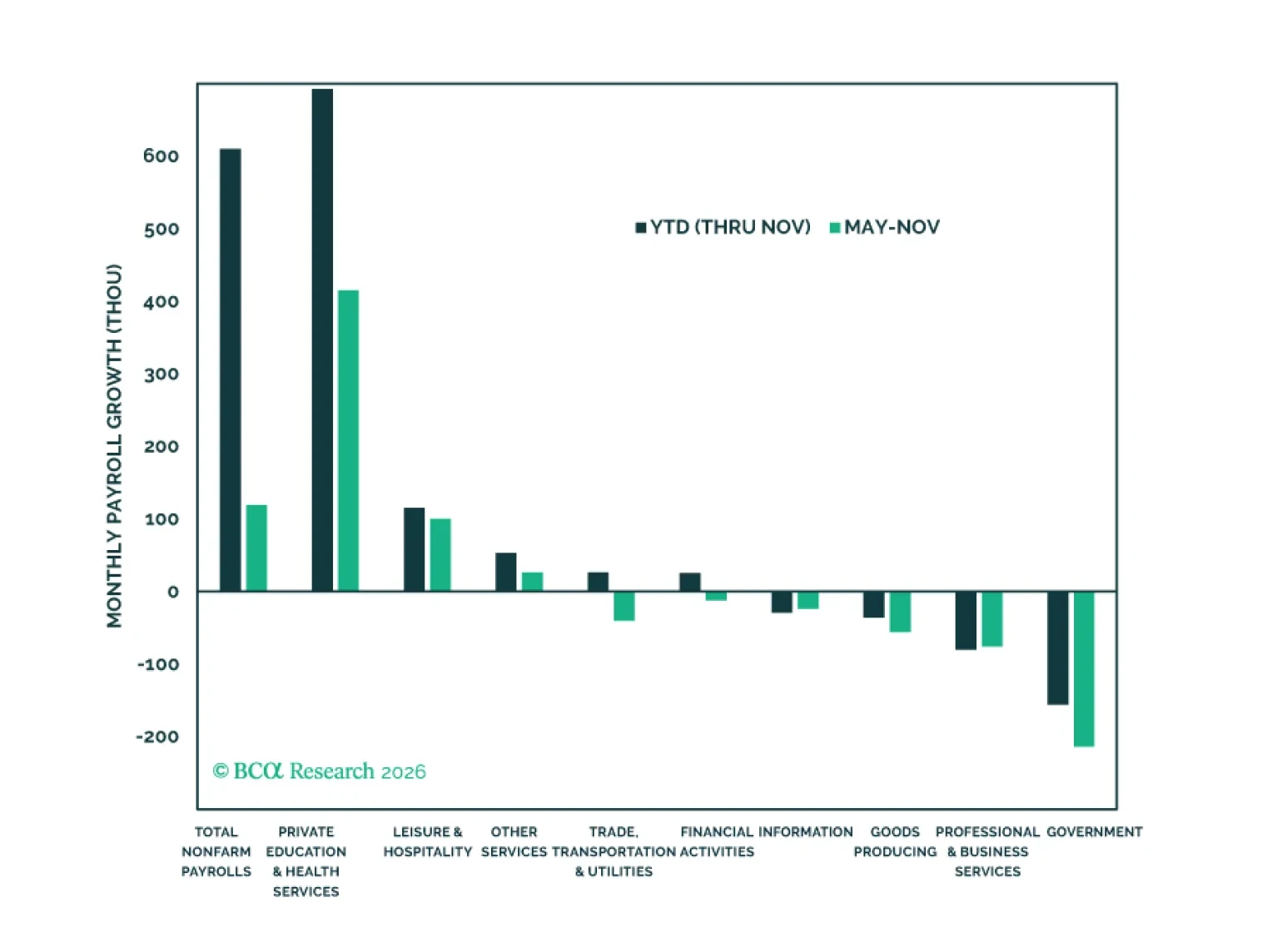

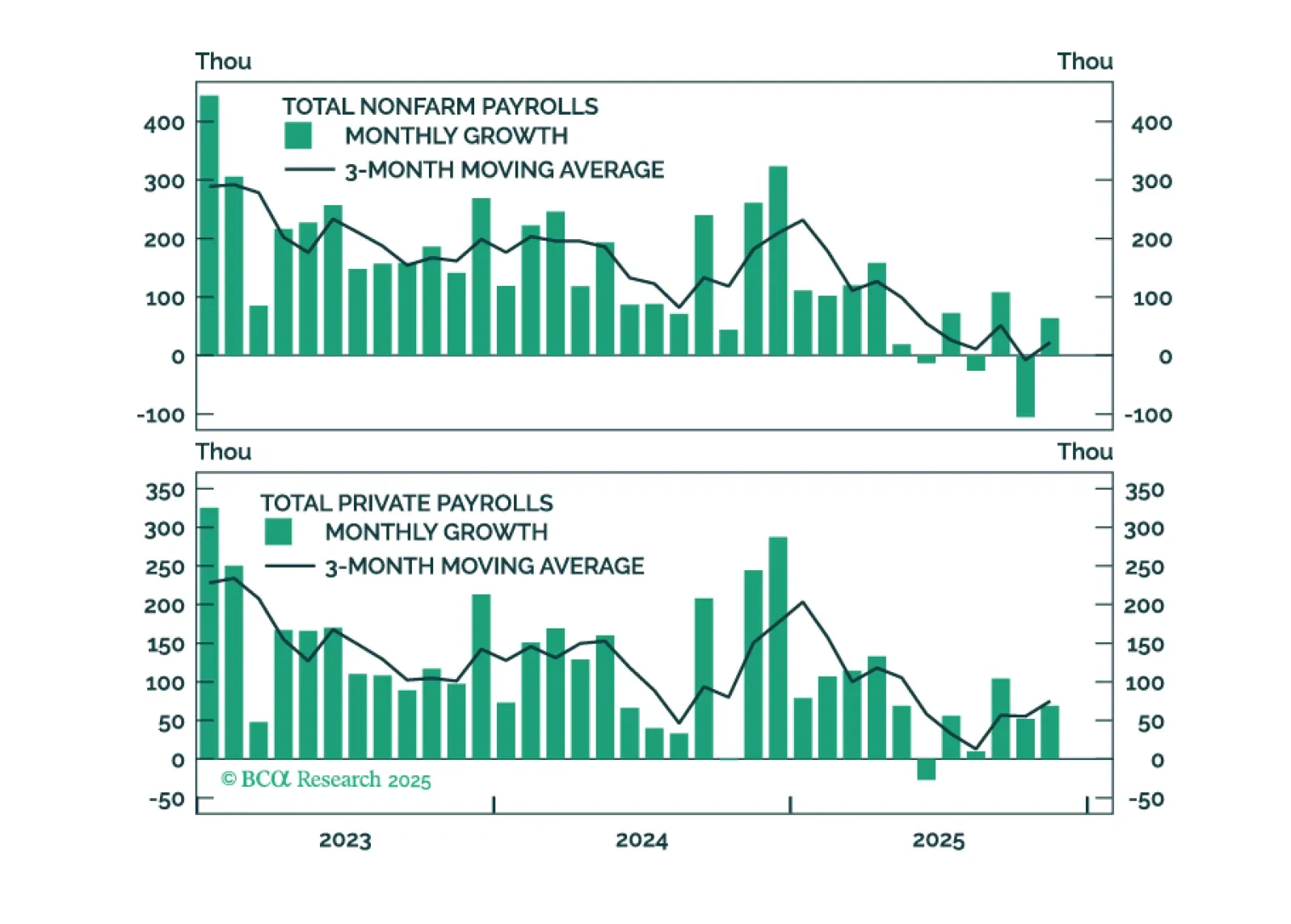

Labor Market

To start 2026, we answer what we believe are the most important questions facing investors surrounding the labor market, monetary and fiscal policy, and AI stocks. Overall, we reiterate our overweight views on risk assets and highlight the risks surrounding the upcoming tariff decision.

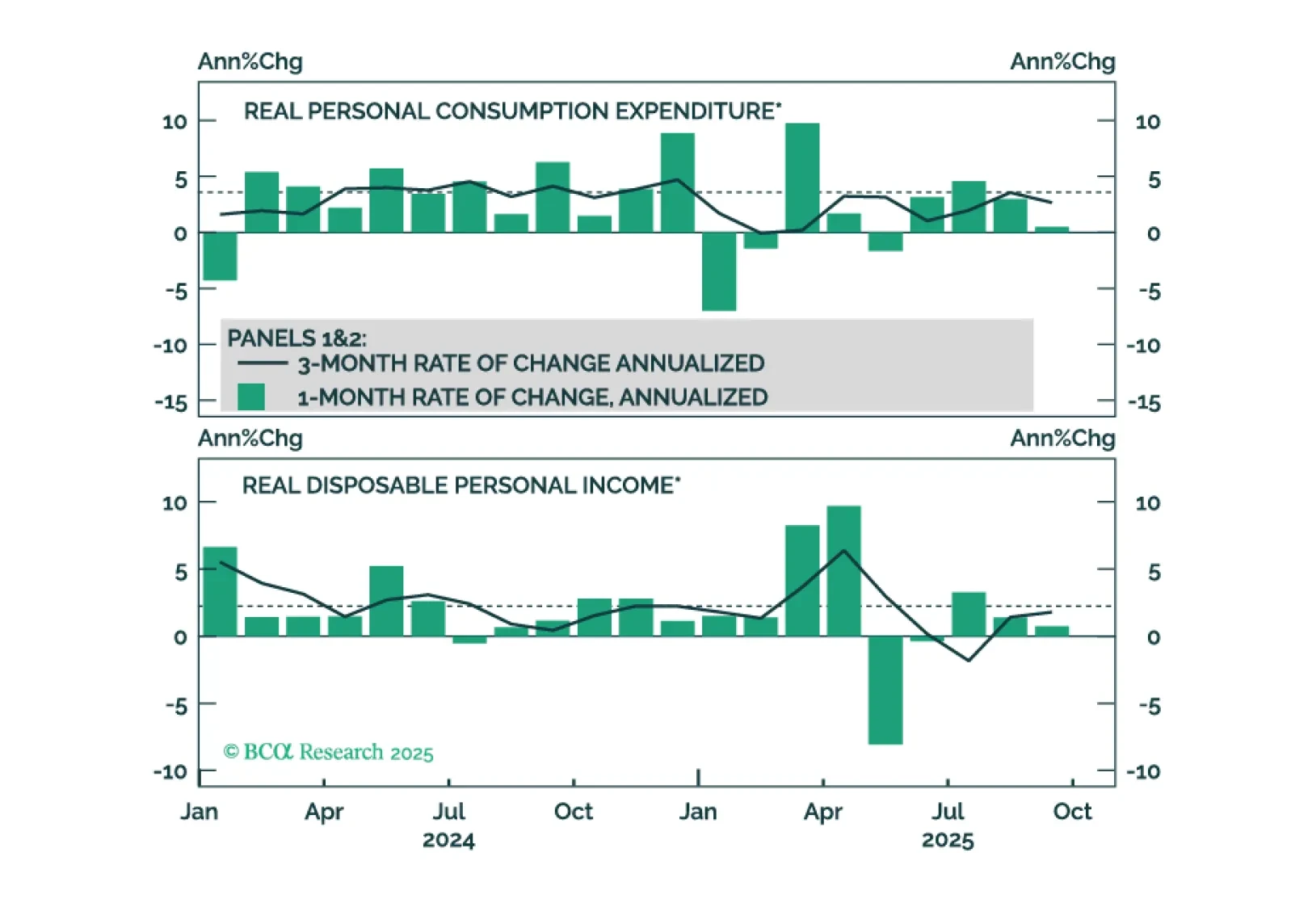

We have been surprised that consumption has held up well despite anemic payrolls growth. This brief considers ways that consumption might continue to beat our base-case expectations.

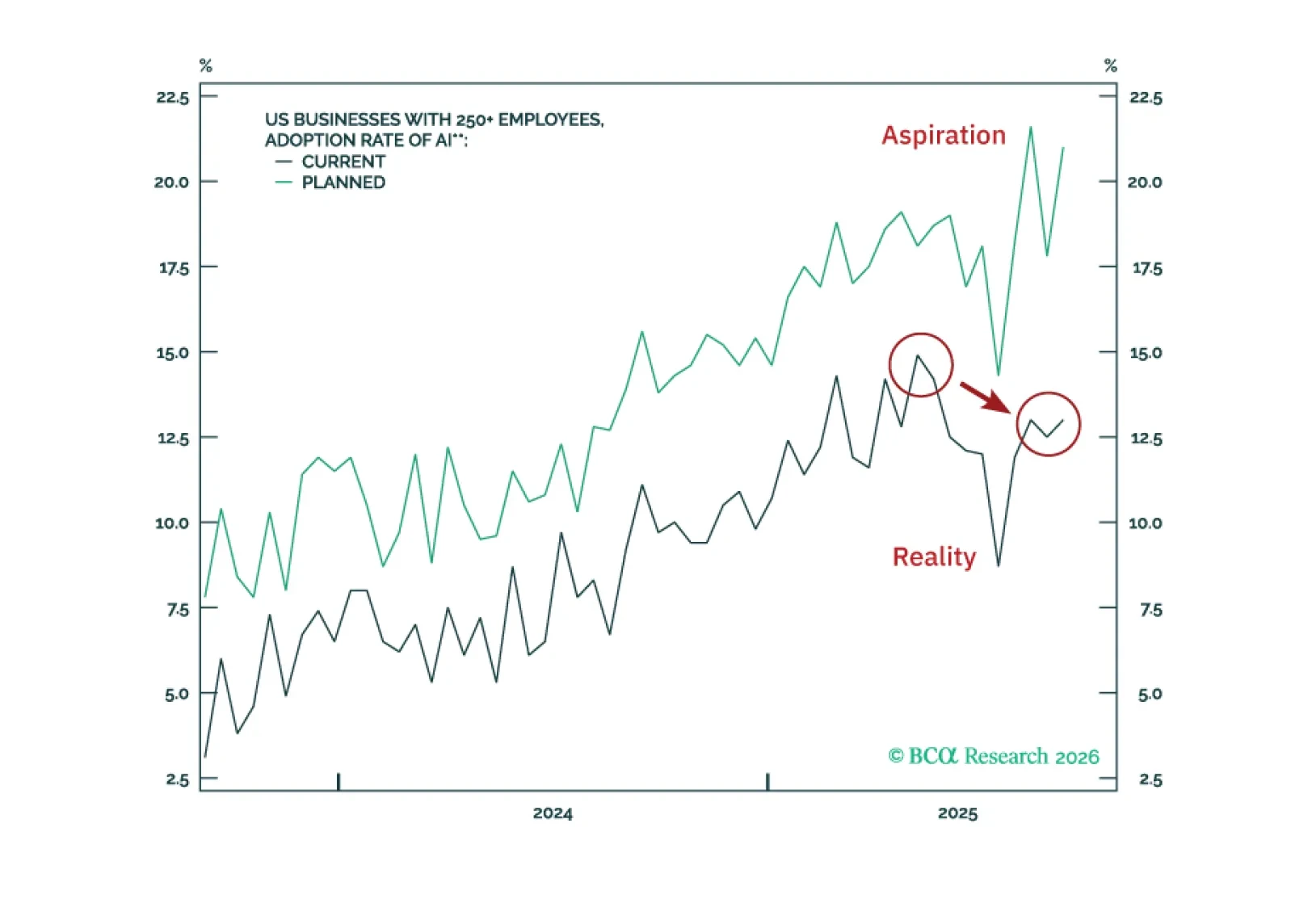

In Section II, Jonathan updates the BCA Artificial Intelligence Productivity Checklist and concludes that the evidence of an AI-driven productivity boom is not convincing.

In Section I, Doug underscores that the US labor market remains weak, crimping the outlook for disposable income growth. It is too soon to decisively bet against the bull market, but downside risks remain quite elevated. In Section II, Jonathan updates the BCA Artificial Intelligence Productivity Checklist and concludes that the evidence of an AI-driven productivity boom is not convincing.

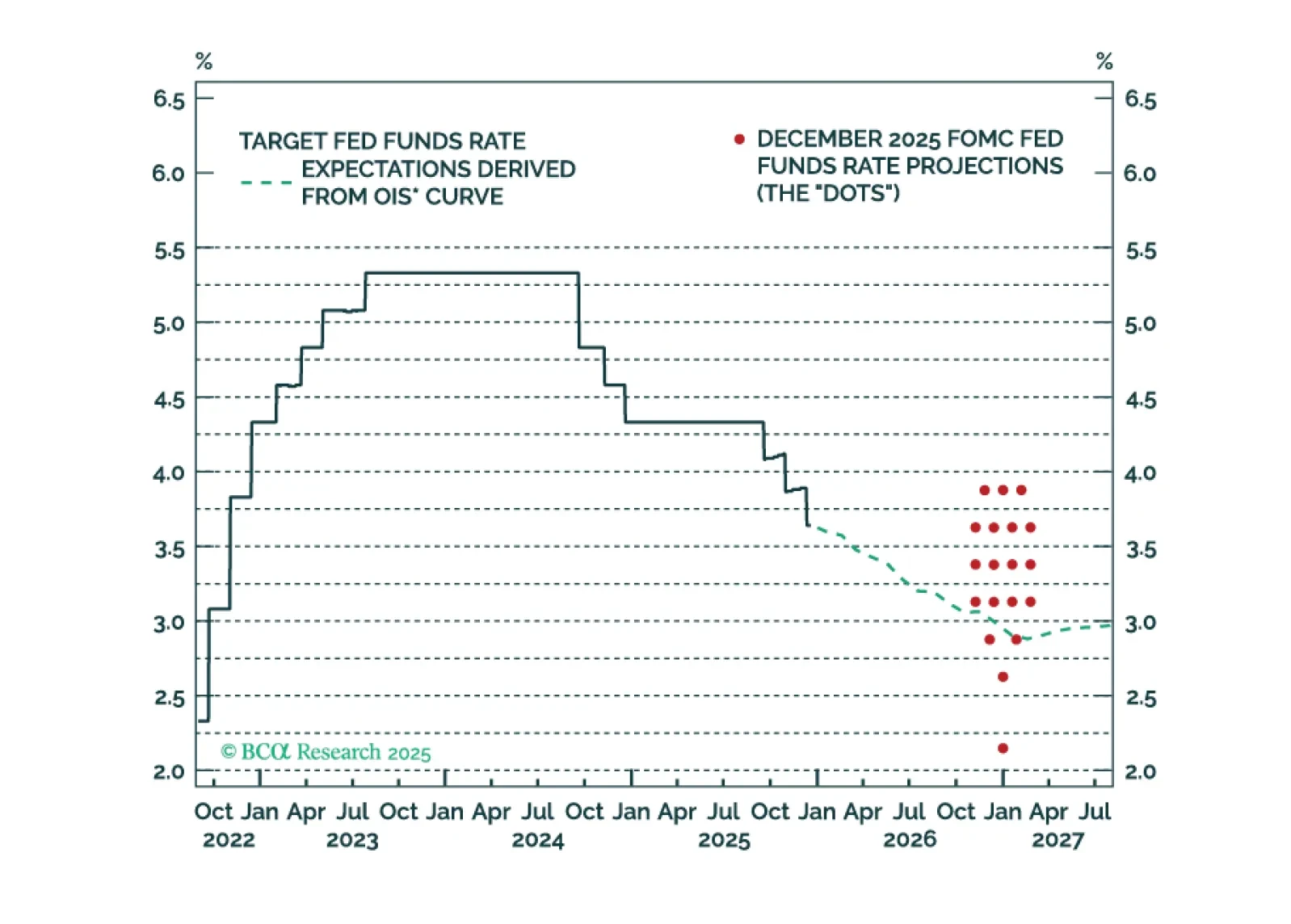

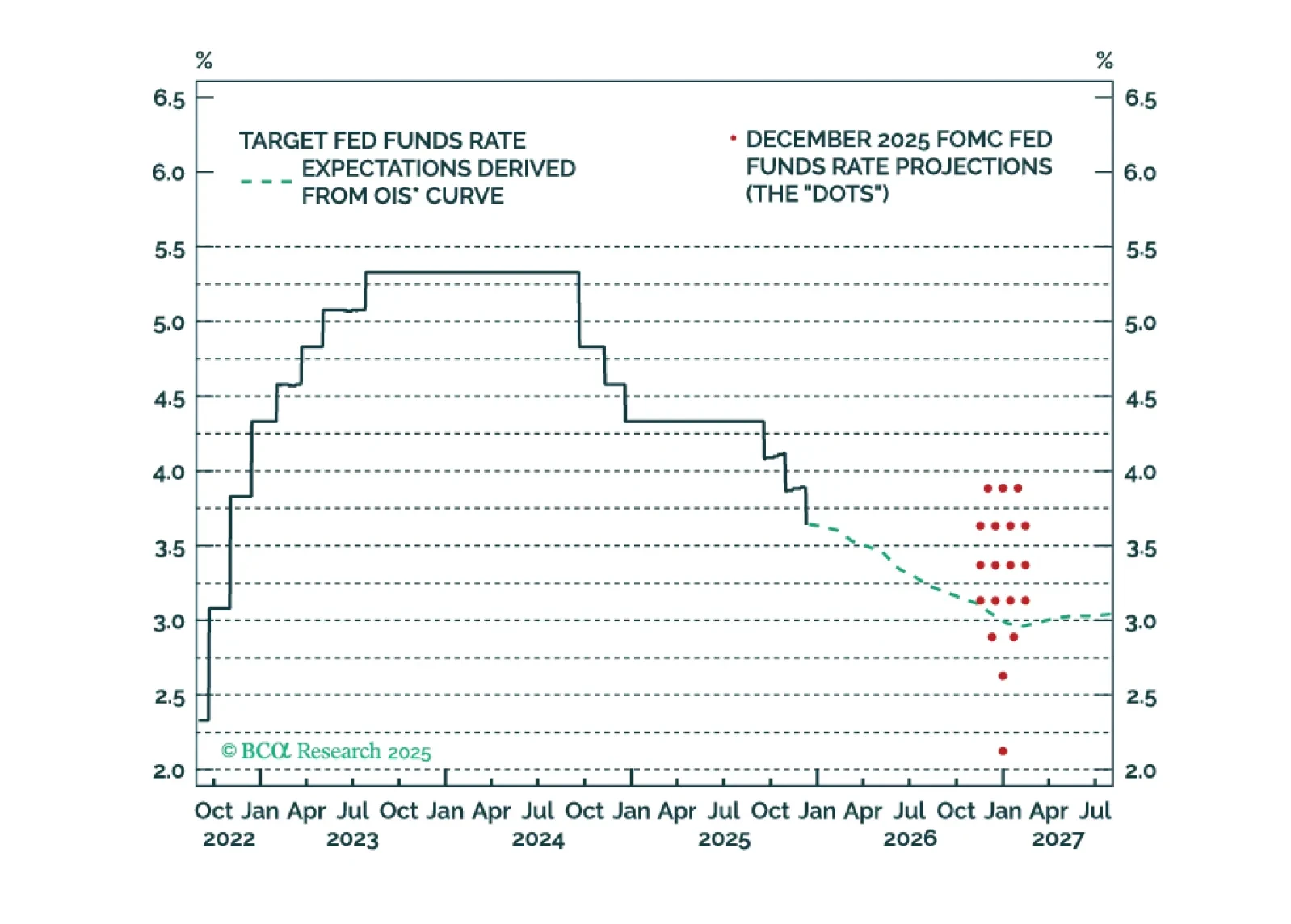

Our outlook for Fed policy in 2026.

Employment Data Point To Dovish Policy Surprises In 2026

Weak, narrowly concentrated job growth in fields that pay poorly bodes ill for the economy, but we enter 2026 recommending benchmark allocations because we are wary of the potential for an AI-driven meltup. Investors should bide their time before turning defensive.

This year, we once again present our 2026 outlook as a retrospective from the future – a future in which the AI boom turned to bust.

Next week, please join me for a Webcast on Wednesday, December 17 at 10:30 AM EST (3:30 PM GMT, 4:30 PM CET) to discuss the economy and financial markets. We will also host a Webcast for APAC on Tuesday, December 16 at 8:00 PM EST (9:00 AM HKT+1 day).

And with that, I will sign off for the year. I wish you and your loved ones a very happy and healthy 2026. We will be back on Friday, January 2 with our MacroQuant Model Update.

The Fed is on hold for now, but its 2026 economic projections are far too optimistic. The Fed will ease more next year than it currently anticipates.

September’s weak consumer spending data challenge the K-shaped recovery narrative and suggest that spending will slow to match already-weak employment growth.