Labor Market

Contrary to conventional wisdom, most leading indicators suggest that the US labor market is weakening, including our very own “Mel rule.” After being overweight stocks last year, we moved to neutral at the start of 2024, and are now putting equities on downgrade watch with the expectation of shifting them to underweight later this year.

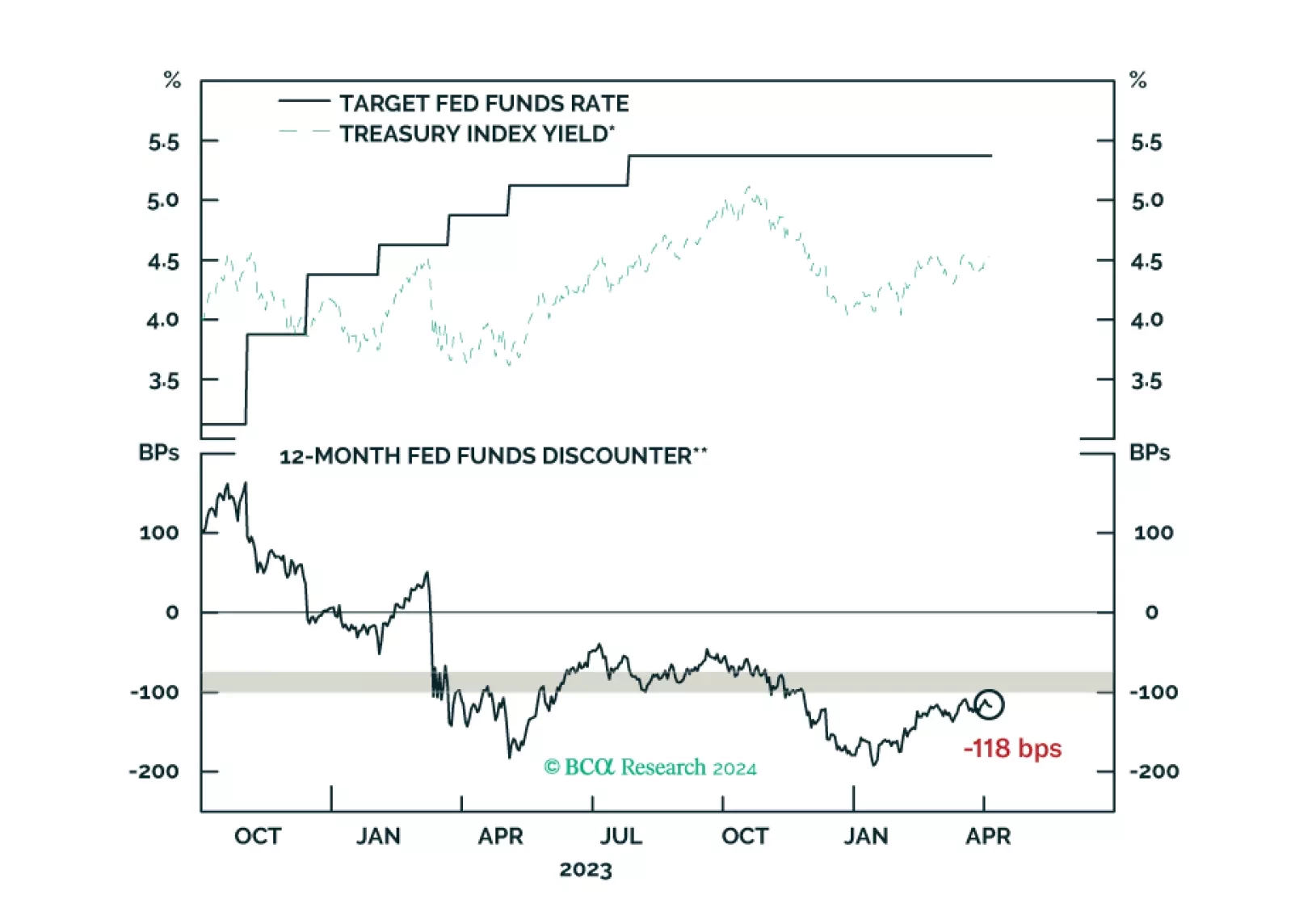

Our reaction to this morning’s employment report and bond market moves.

We are not yet ready to downgrade equities on a tactical basis but continue to expect we will eventually do so. We present a checklist of indicators that we are watching to determine when to de-risk.

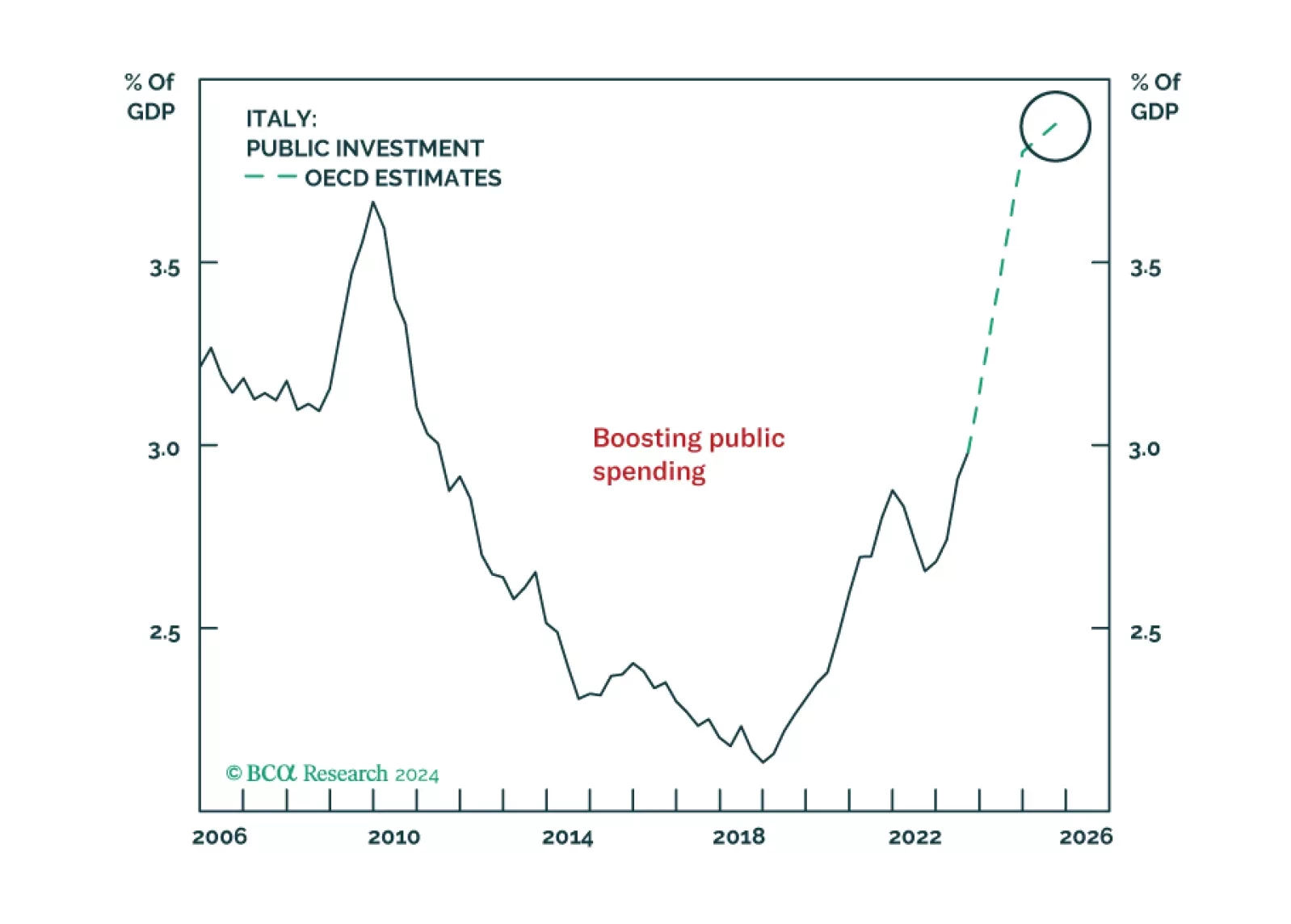

Italy is no longer Europe’s problem child. Investors will be better off reassessing their views of Italian assets, which represent a buying opportunity on a structural time horizon.