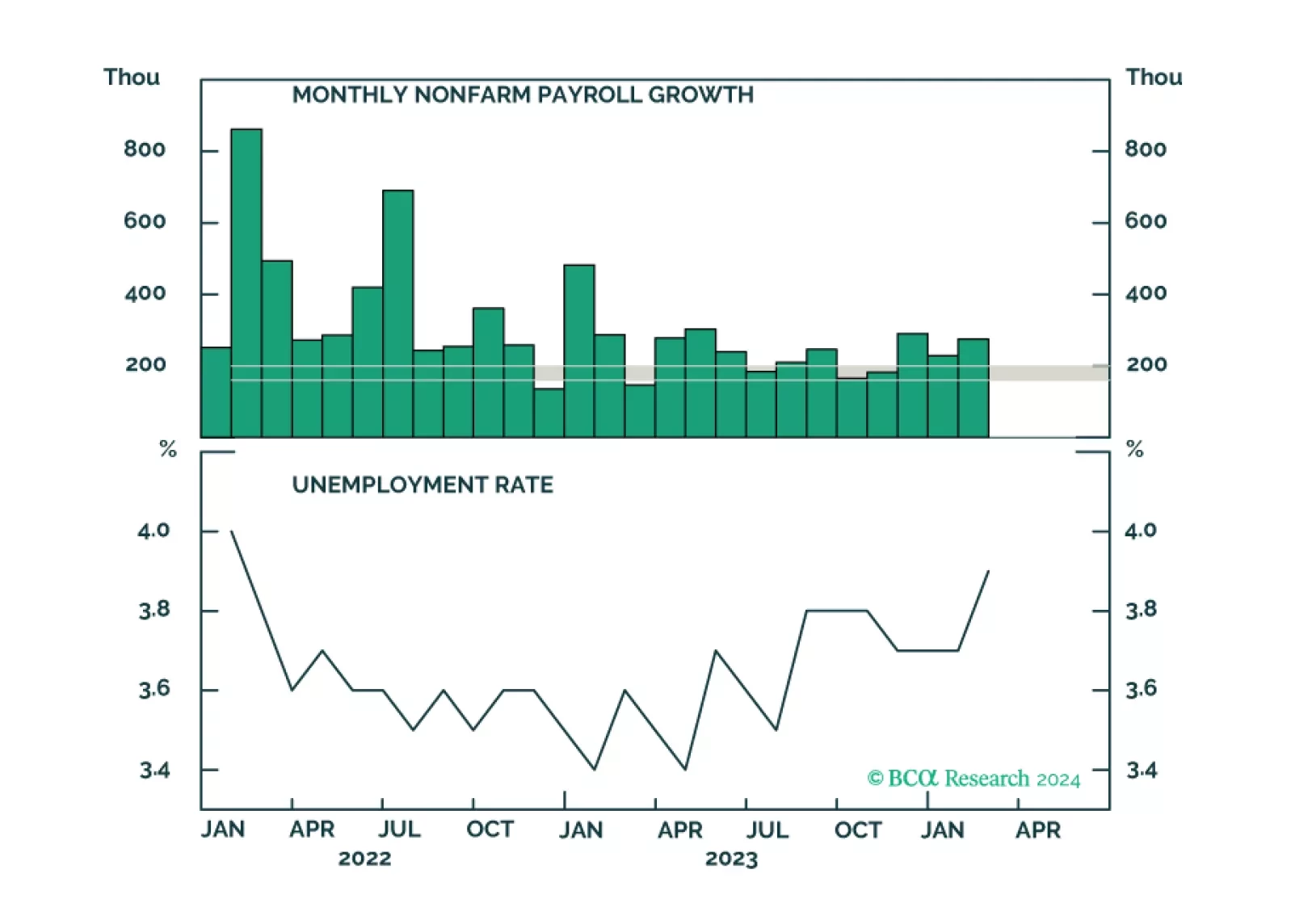

Labor Market

We update the indicators in our duration checklist following this morning’s employment report.

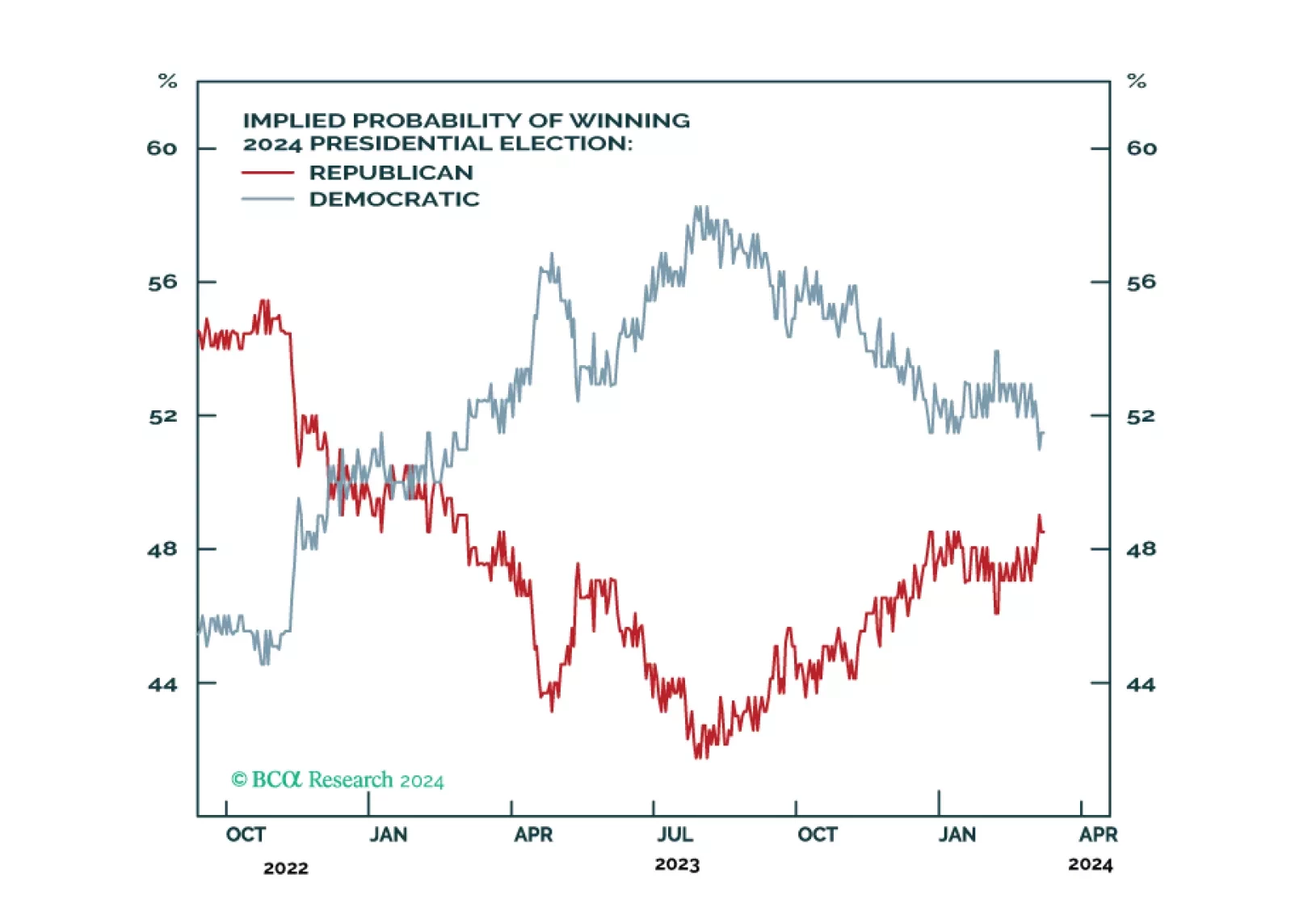

Democrats are still slightly favored for reelection as the incumbent party is presiding over a growing economy. However, Biden’s strong showing in the primary election is not lifting his popular approval yet, and that is a worrying sign. Policy uncertainty should rise sharply, which is marginally negative for the stock market.

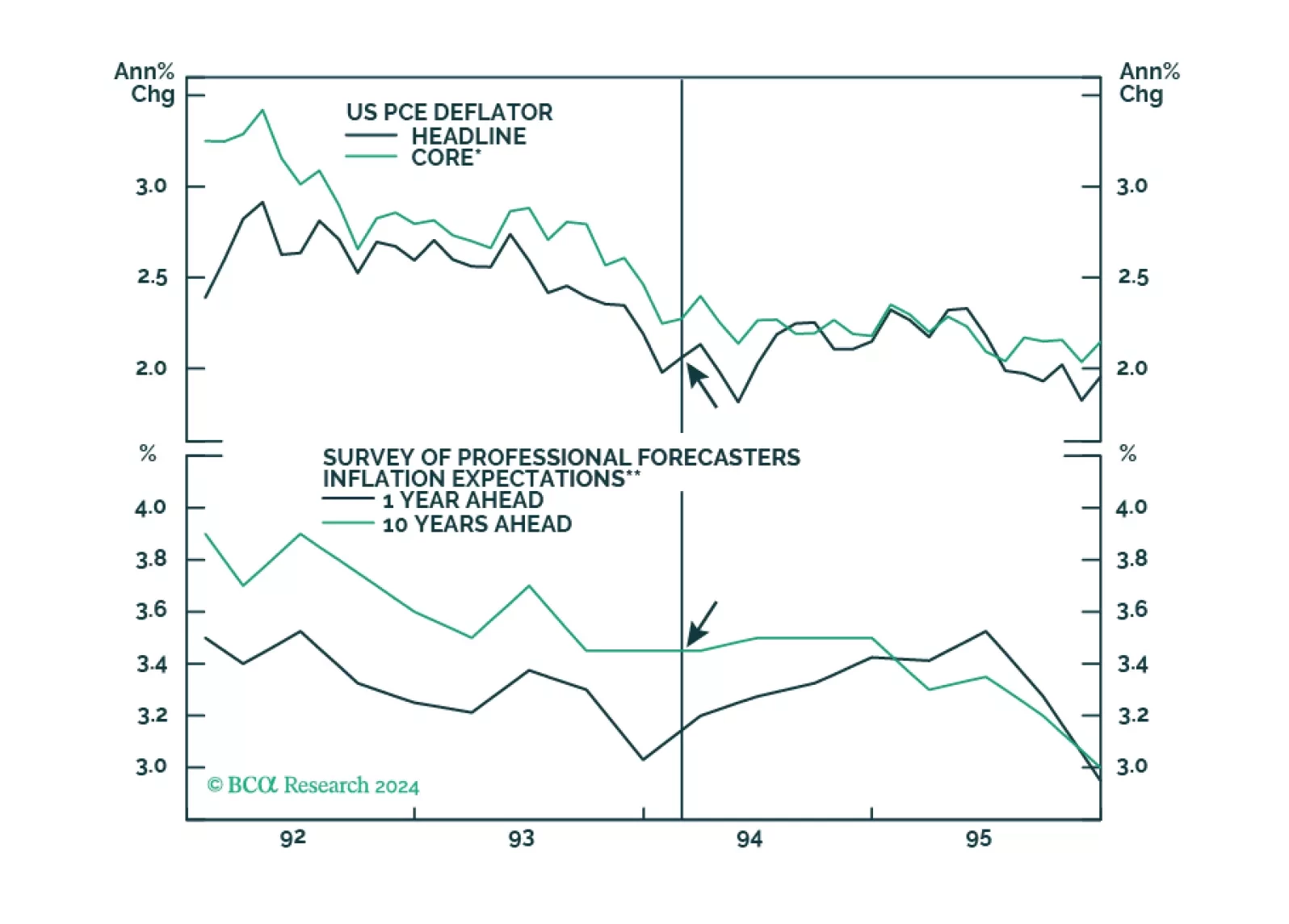

Many investors have cited the 1994 tightening cycle as an example of how the Fed managed to raise rates without triggering a recession. However, the unemployment rate was 6.5% in early 1994, which meant that inflation was less of a risk than it is today. Productivity growth also accelerated starting in the mid-1990s. While something similar may happen again thanks to AI, so far this is not visible in the aggregate productivity data.

We feel as good about spurning the soft-landing narrative today as we did about spurning the recession narrative a year ago, but we are not giving into complacency. This week’s report looks at two key ways that we may be getting it wrong: by underestimating households’ asset support and the labor market’s durability. We remain tactically neutral but continue to look for opportunities to turn defensive.

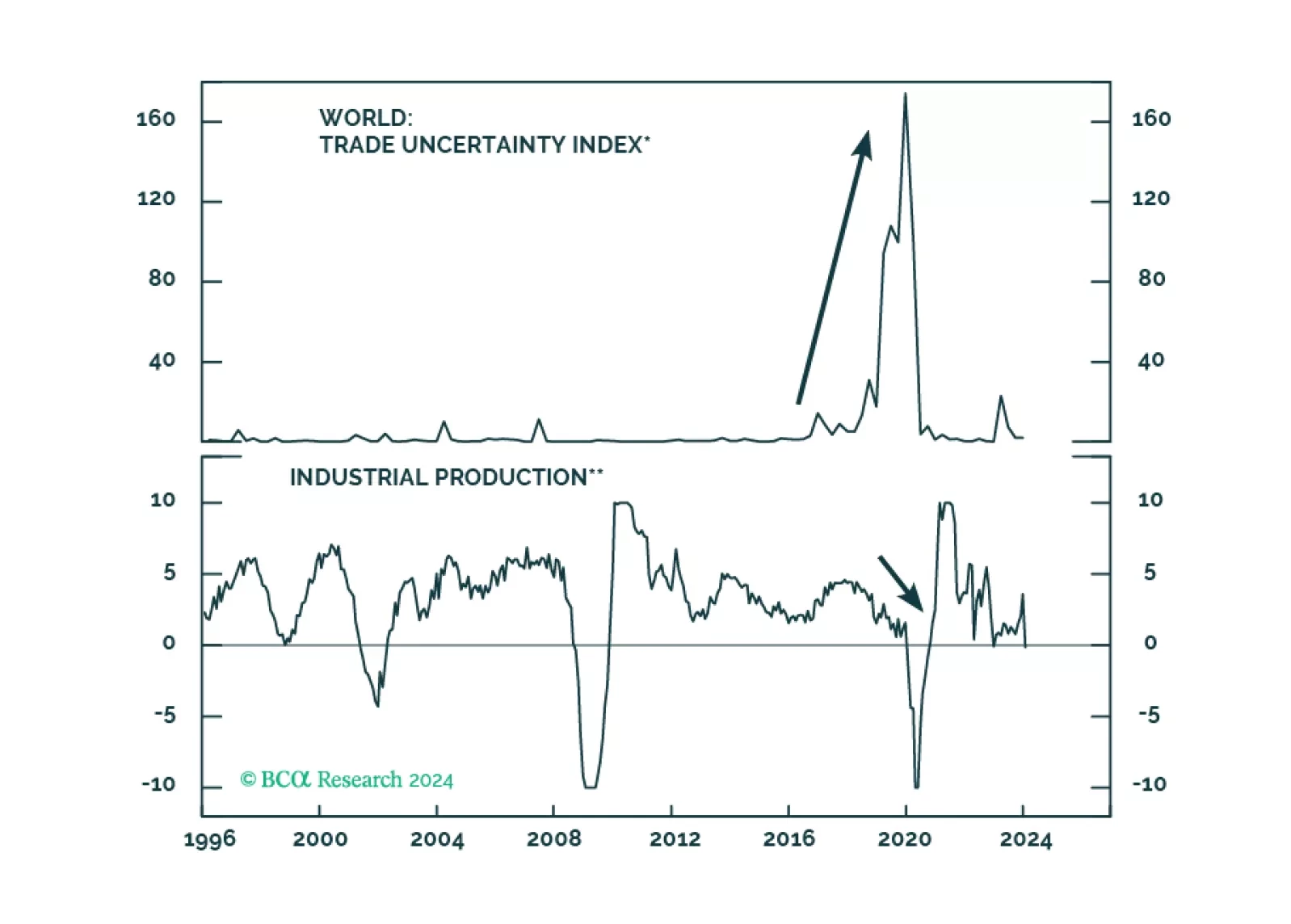

In this BCA Special Report, we ask what policies investors should expect if Donald Trump wins the 2024 Presidential election. The answer is that a second Trump term would be much less positive for risky assets than the first. While the US will remain democratic and geopolitically preeminent no matter the outcome of the 2024 election, a second term Trump administration would likely oversee large budget deficits, continued wealth inequality, labor shortages, high import prices, and an erosion of checks and balances, possibly including at the Federal Reserve. Trade policy under a second Trump presidency represents the greatest cyclical risk to investors, and the sequencing of policies in general will be important to monitor. An early legislative priority of immigration over tax cuts, alongside the rapid imposition of new tariffs, would be the worst alignment for risky assets.