Labor Market

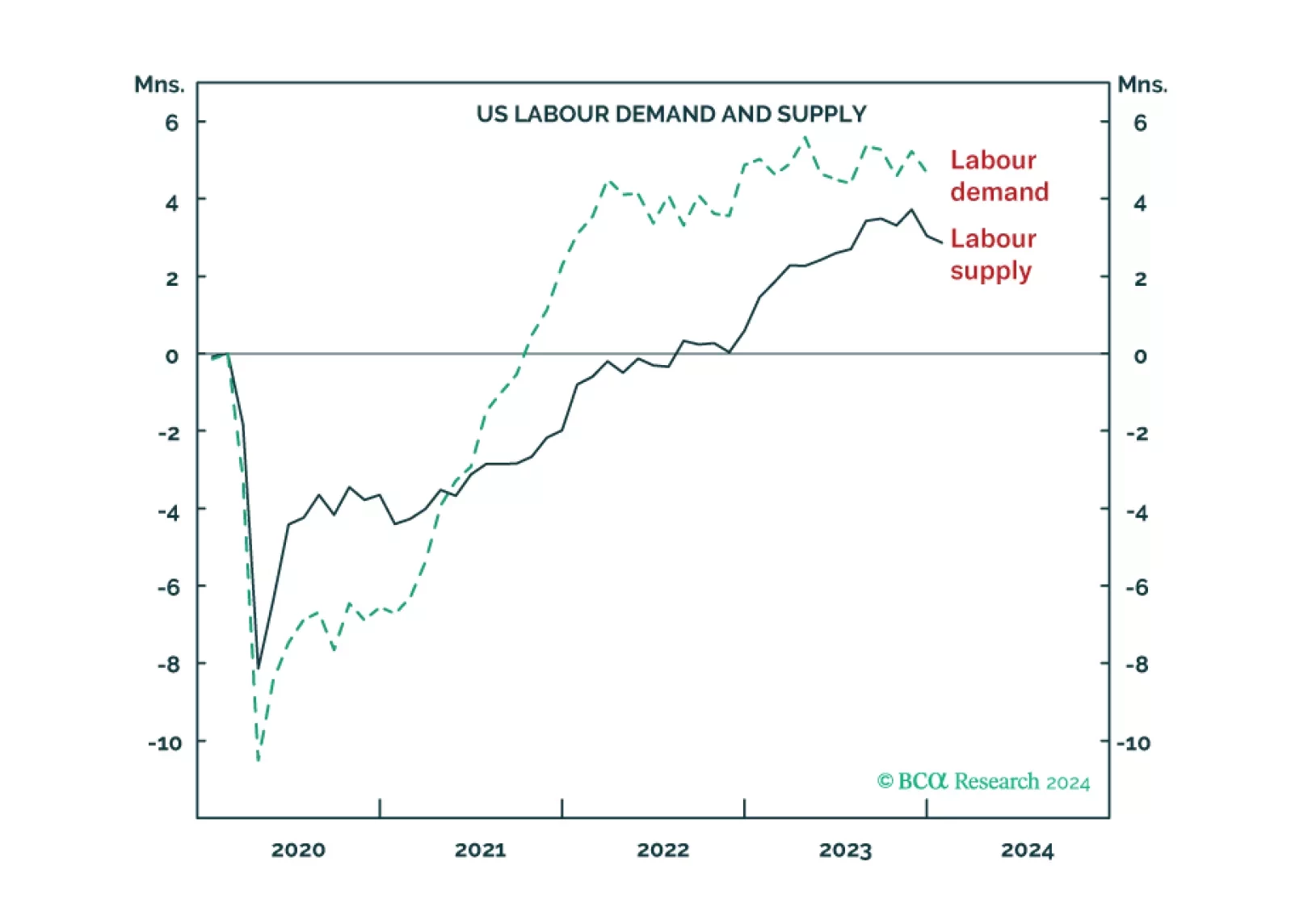

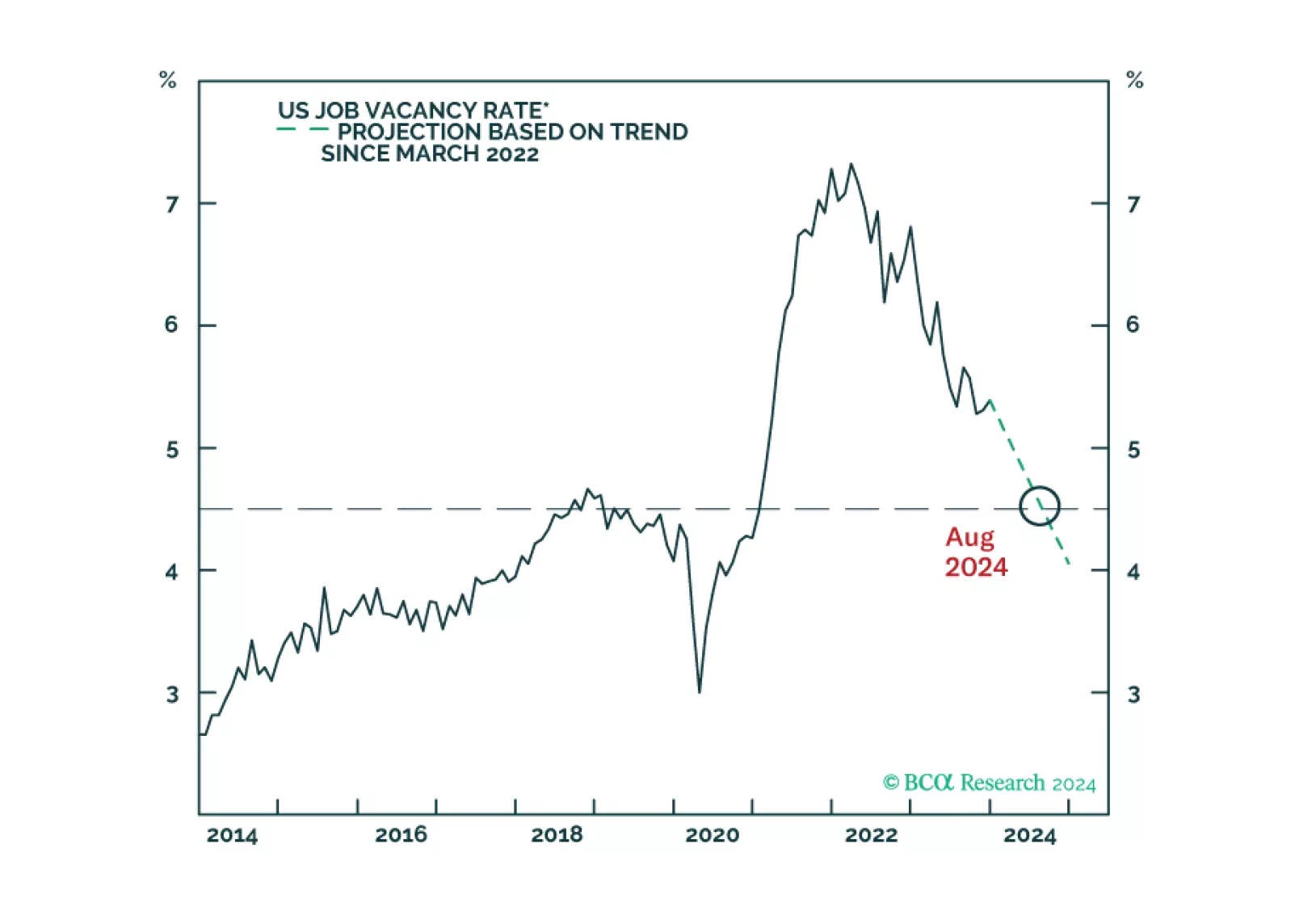

The US ‘immaculate disinflation’ has run its course, given that labour force participation is topping out. This leaves the Fed with a dilemma. Settle for price inflation stabilising at 3 percent, and cut rates early to avoid higher unemployment. Or, not cut rates early and go the final mile to 2 percent price inflation, at the risk of higher unemployment. We discuss which way the Fed is likely to tilt, and the investment implications. Plus: China is oversold while Japan is overbought.

The first in a series of Strategy Insights where we present a checklist for extending duration in each major government bond market. This first entry focuses on the US.

Households have ramped up their cash holdings since the end of 2019, but the absence of an empirical link between cash and consumption leads us to believe that we’ve modestly overestimated the risk of consumer-driven overheating.