Labor Market

The US Employment Cost Index for Q4 delivered a positive signal that the disinflation process is intact. The ECI’s slowdown from 1.1% q/q to 0.9% q/q came in softer than anticipations of 1.0% q/q. This marks the slowest pace of quarterly increase since 2021Q2…

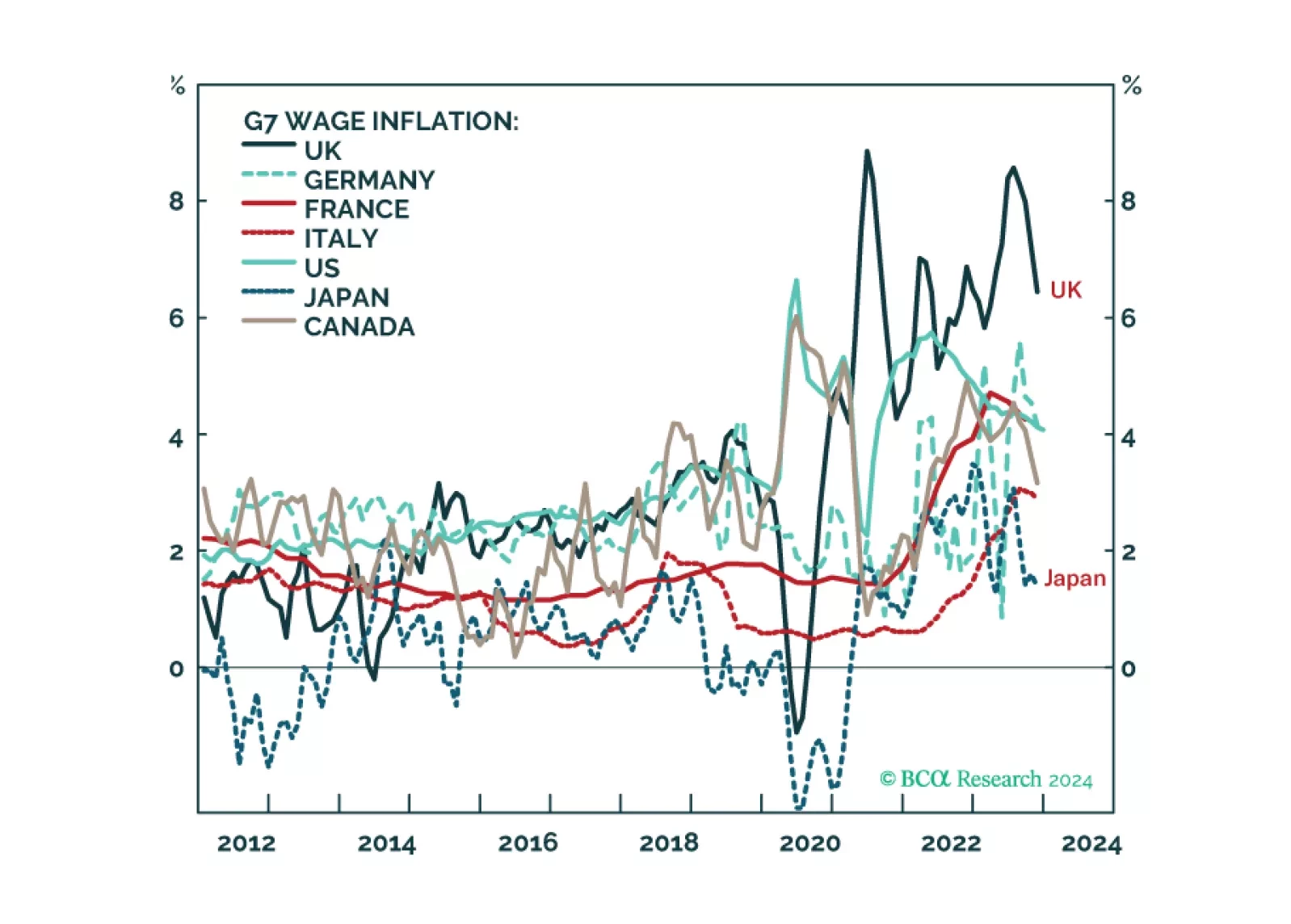

We describe and explain the wide disparity of wage inflation across G7 economies, and discuss what it means for the Fed, ECB, BoE, and BoJ policy moves in the coming year. Plus: we highlight two investments ripe for reversal, and two investments ripe for rebound.

The December JOLTS survey delivered a positive surprise on Tuesday. Job openings rose from an upwardly revised 8.93 million in November to a three month high of 9.03 million in December, beating expectations of 8.75 million. In addition, the hiring rate…

Since the low of 27 October last year, MSCI US has rallied by 19.1% and this rally has been firmly driven by cyclical sectors. Performance-wise Information Technology (IT), Communication Services and Financials and Real Estate have been the top performing…

Results of regional Fed surveys suggest that the US manufacturing sector is starting the year on a weak footing. Monday’s report from the Dallas Fed– the last to release its results for January – showed the headline manufacturing activity index collapse from…

Friday’s US Personal Income and Outlays report for December delivered a positive update on the US economy. On the growth side, the data confirm the signal from the Q4 GDP release that consumer spending continues to power the US economy. The robust 0.5%…

According to BCA Research’s The Bank Credit Analyst service, there are two important flaws in the market’s “Goldilocks” narrative. First, investors are assuming inflation will fully return to target this year because core inflation ex-housing is already at…

With the latest PCE release confirming that the disinflation process is intact (see The Numbers), a key question facing investors is around the timing of the Fed’s pivot to rate cuts. Indeed, the US inflation surprise index has collapsed from its mid-2021…

Over the past few months, falling inflation has provided a boost to real wages in the Euro Area which returned to growth in 2023Q3 after 9 consecutive quarters of decline. This dynamic in turn improved the purchasing power of households, boosting their morale…

Low inflation argues for the Fed to move relatively quickly toward rate cuts. Continued above-trend GDP growth poses a risk to this view, but leading indicators point to slower growth in the coming quarters.