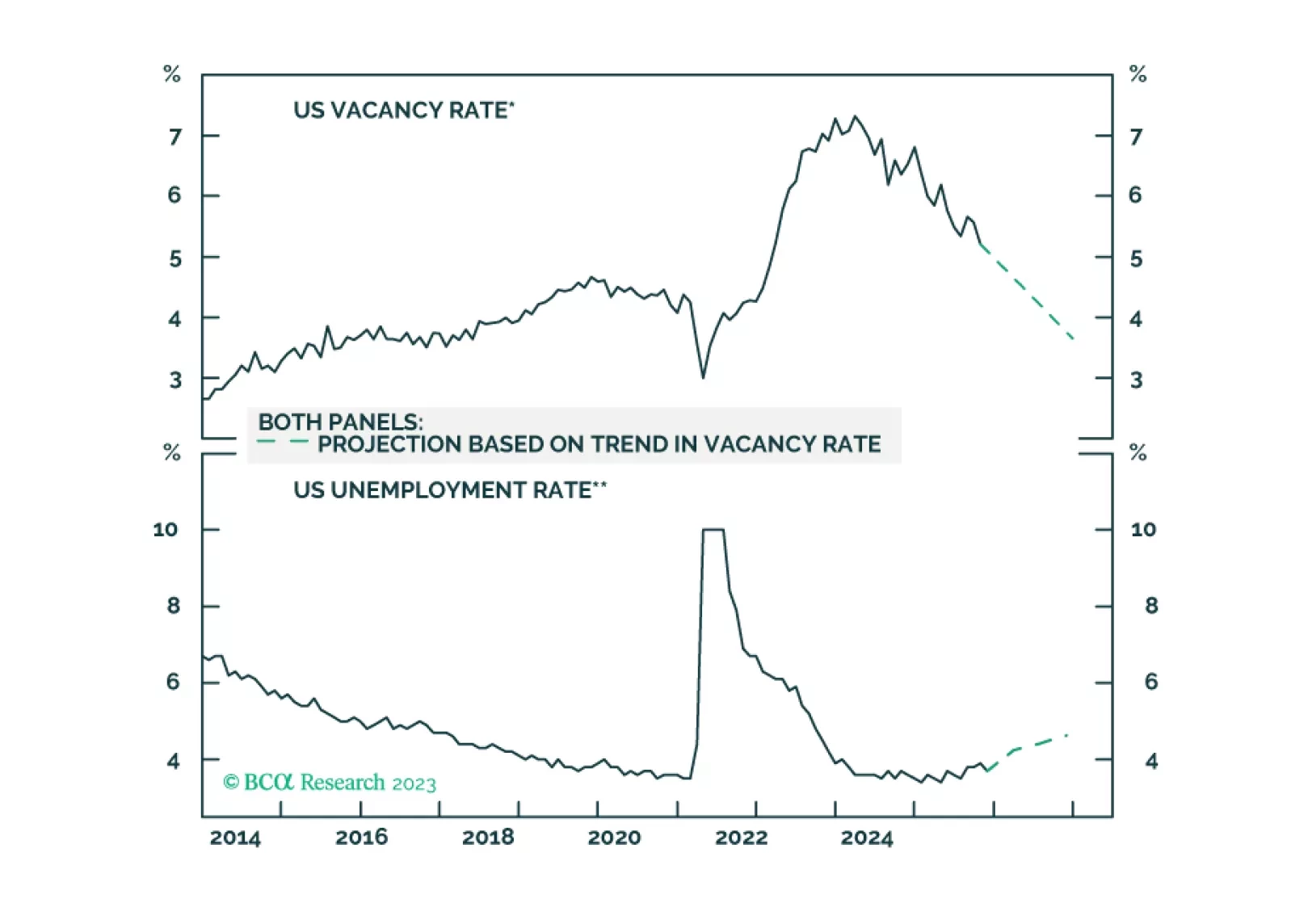

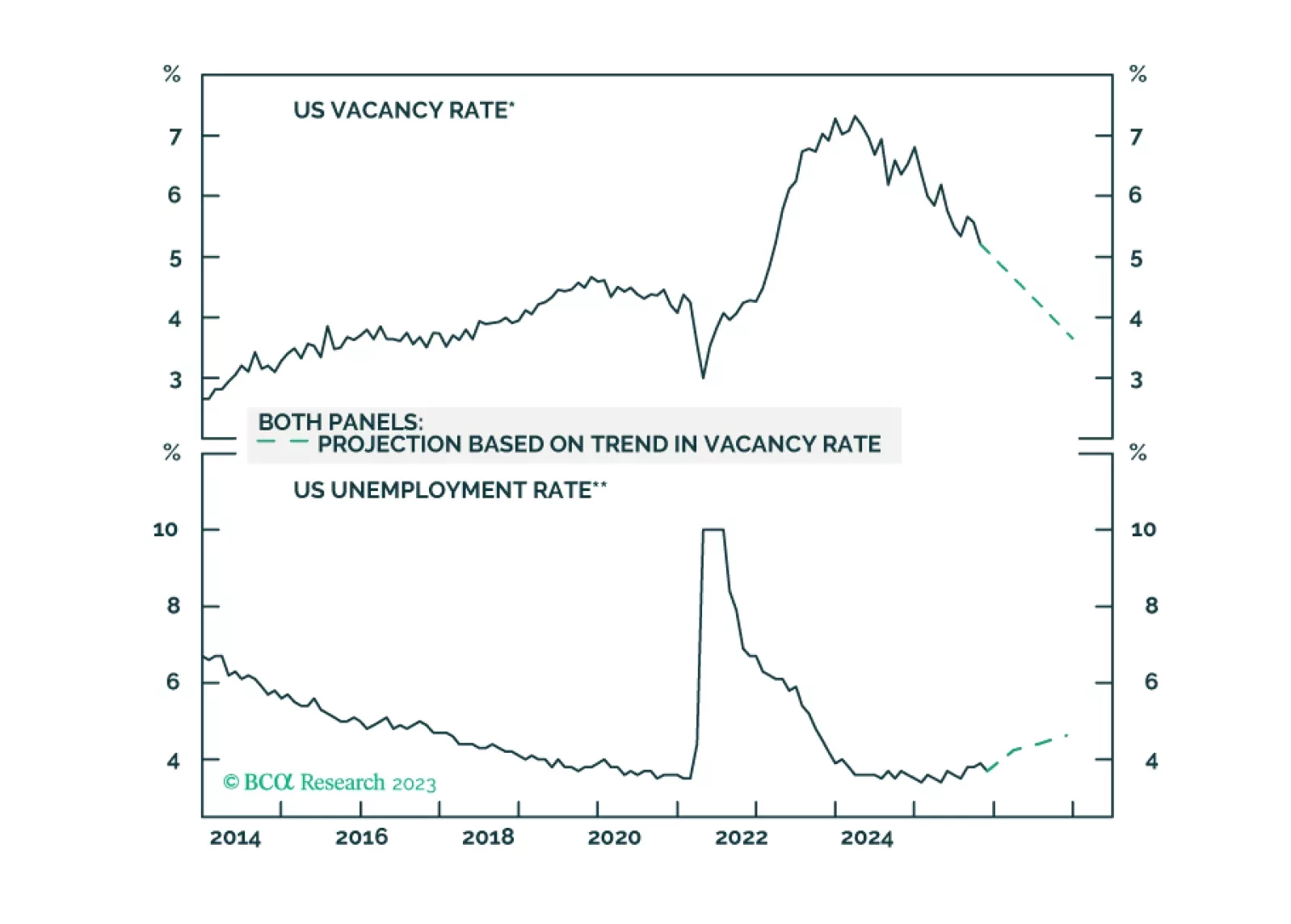

Labor Market

The market is excited by the idea that the Fed will cut rates early this year, even without a recession. But is that likely, with inflation still set to be around 2.8% mid-year?

Economists have been consistently revising up their 2024 US GDP forecasts over the past 4 months. The consensus now anticipates US growth to clock in at 1.3% this year. According to the latest estimate from the Atlanta Fed’s GDPNow model, this will follow…

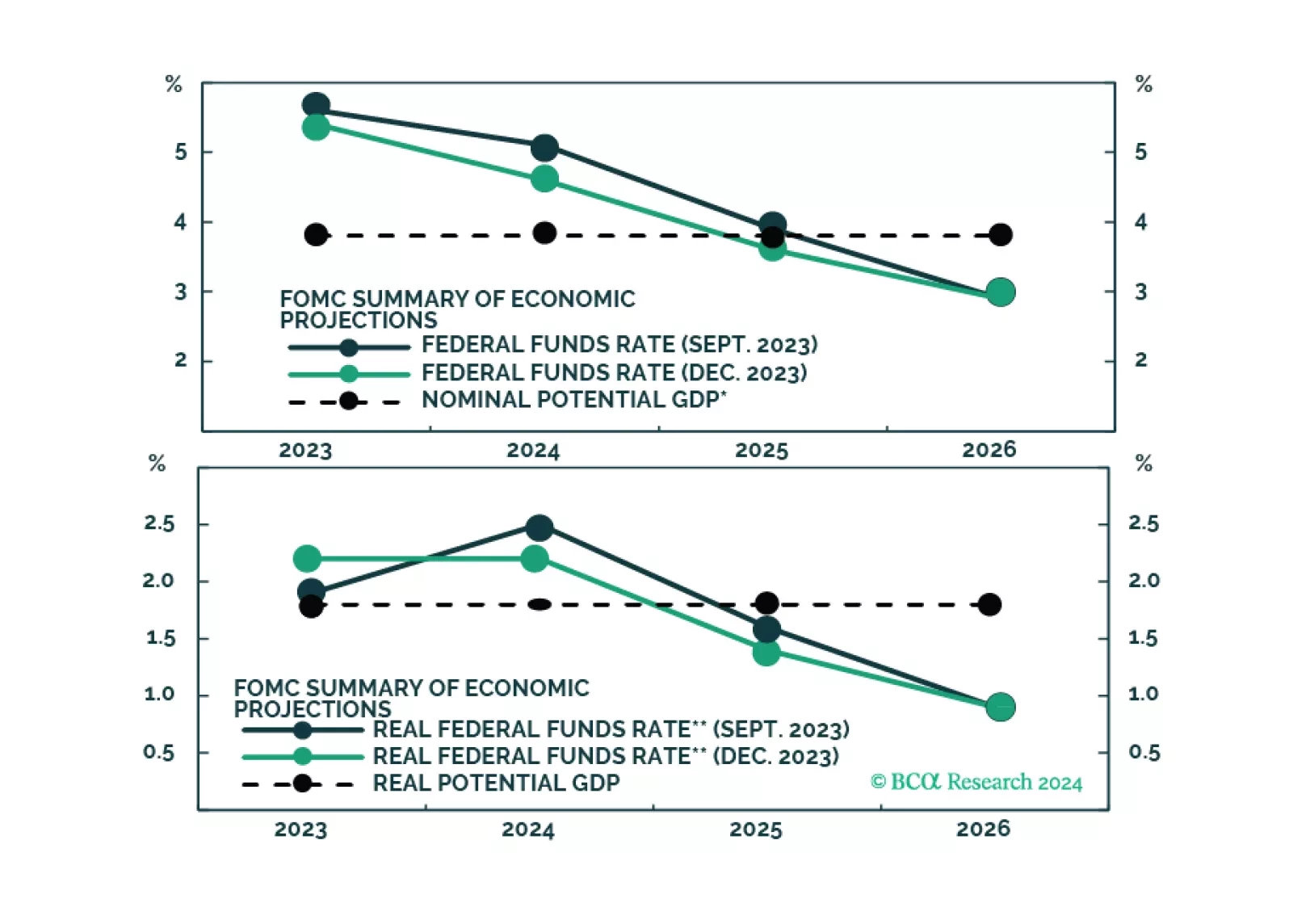

Our outlook for the Fed’s interest rate and balance sheet policies in 2024.

Our outlook for the Fed’s interest rate and balance sheet policies in 2024.

Our last publication of 2023 is an illustrated guide to our view that the economy will enter a recession around midyear. We expect equities will underperform Treasuries and cash over much of 2024, but we are waiting to turn tactically defensive until more investors are drawn into the soft-landing camp, capping the equity rally.

Explore the eight main themes that will drive the returns of European assets in 2024.

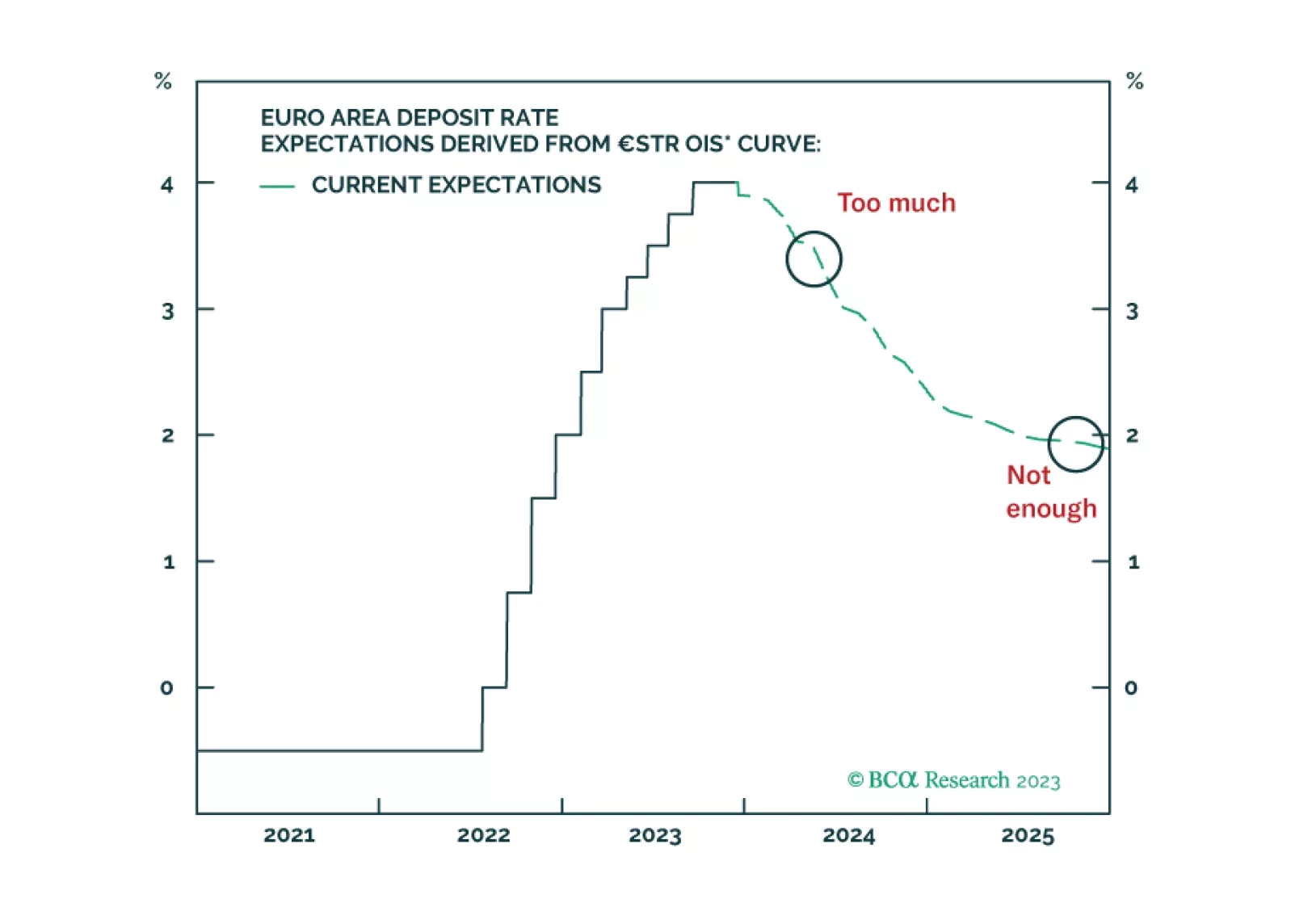

As expected, the ECB kept its policy rate unchanged on Thursday. In the updated macroeconomic projections, the central bank revised down its inflation and growth forecasts for next year. It now expects inflation to ease to 2.7% in 2024 – 0.5 percentage…

The November US retail sales release for November delivered a positive signal about consumer spending. Overall retail sales unexpectedly increased by 0.3% m/m, surprising expectations of a 0.1% m/m decline. The details of the report were also favorable. Eight…

According to BCA Research’s US Bond Strategy service, Treasury curve steepeners will pay off handsomely once the next recession hits. However, curve flatteners (aka barbelled Treasury portfolios) offer better value for the near term. A barbelled Treasury…

The November US CPI release came in broadly in line with consensus expectations on Tuesday. On an annual basis, headline CPI inflation eased from 3.2% y/y to 3.1% y/y while core inflation was unchanged at 4.0% y/y. On a monthly basis, both headline and core…