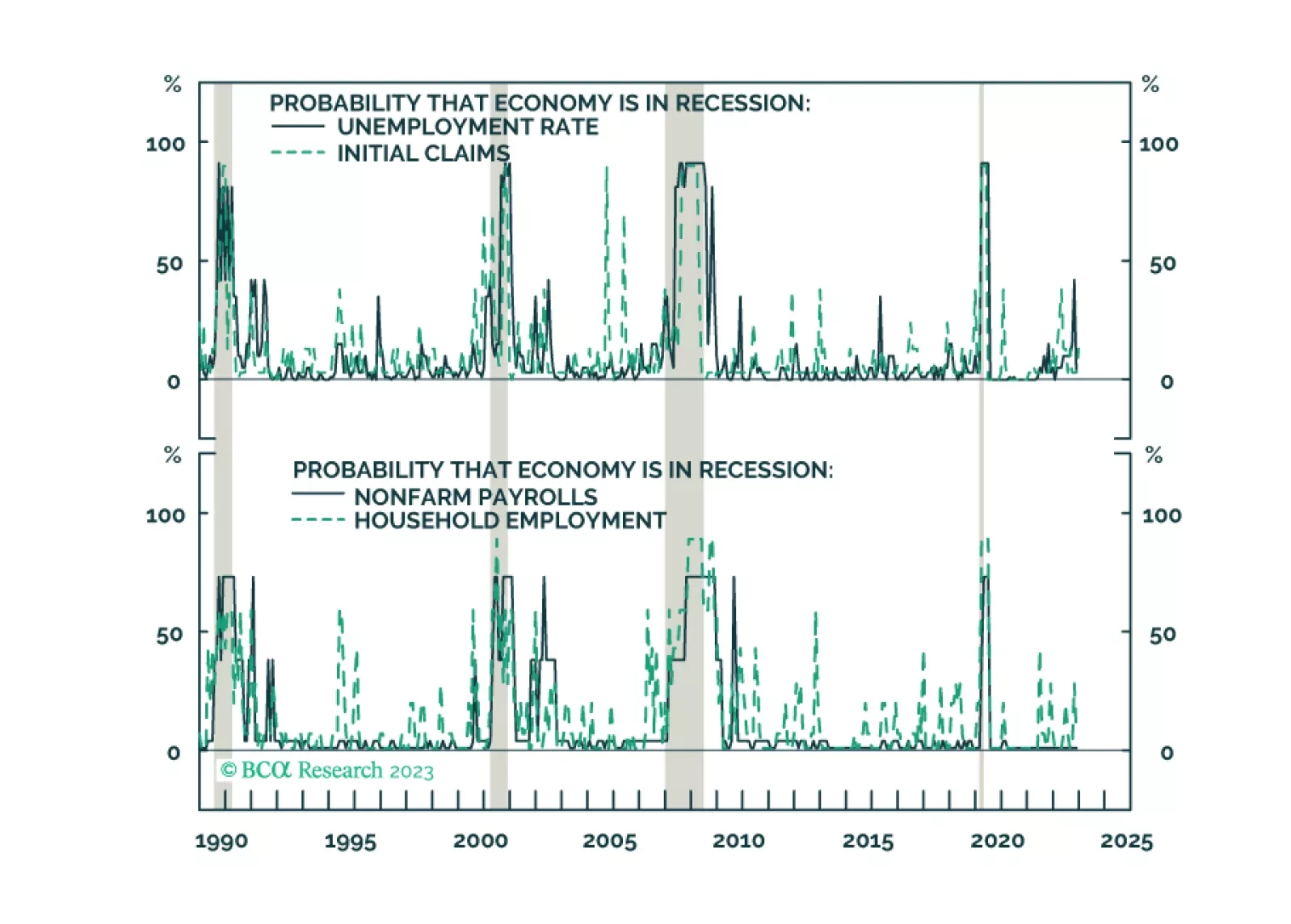

Labor Market

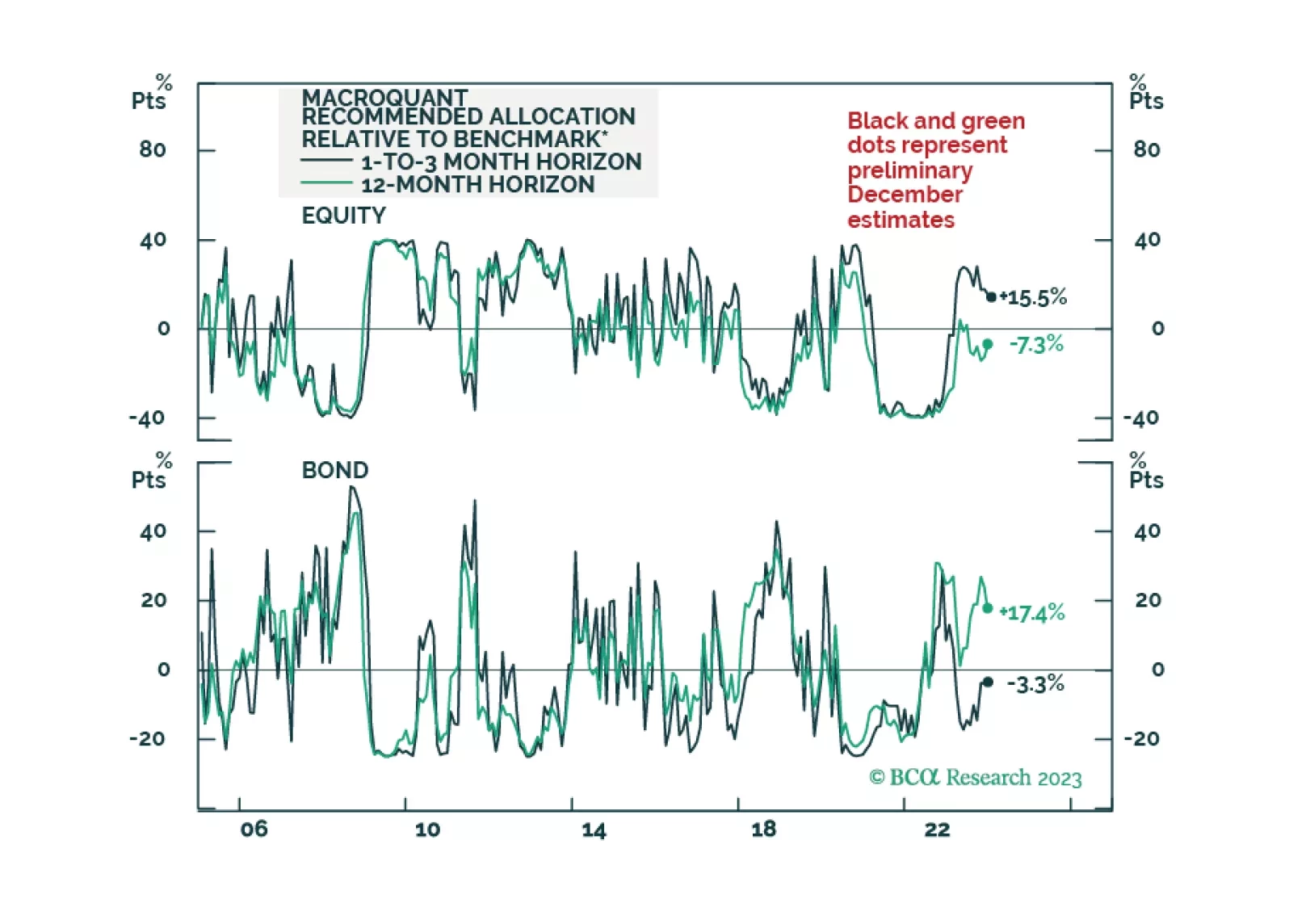

Our US fixed income team’s key investment views for 2024.

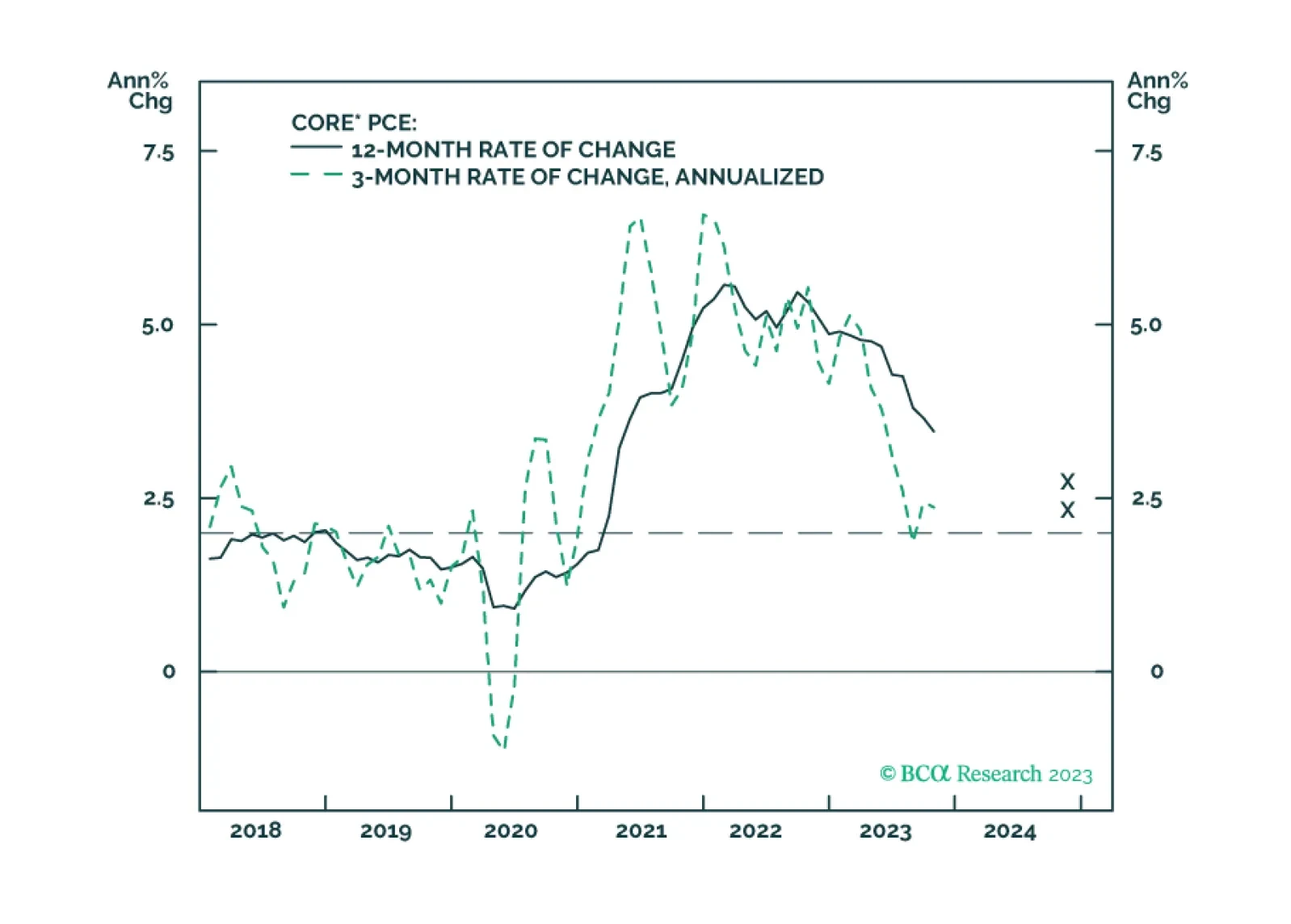

Global Investment Strategy predicted the surge of inflation in 2021/22 and the immaculate disinflation of 2023. Now their unique framework is predicting a recession in the second half of 2024.

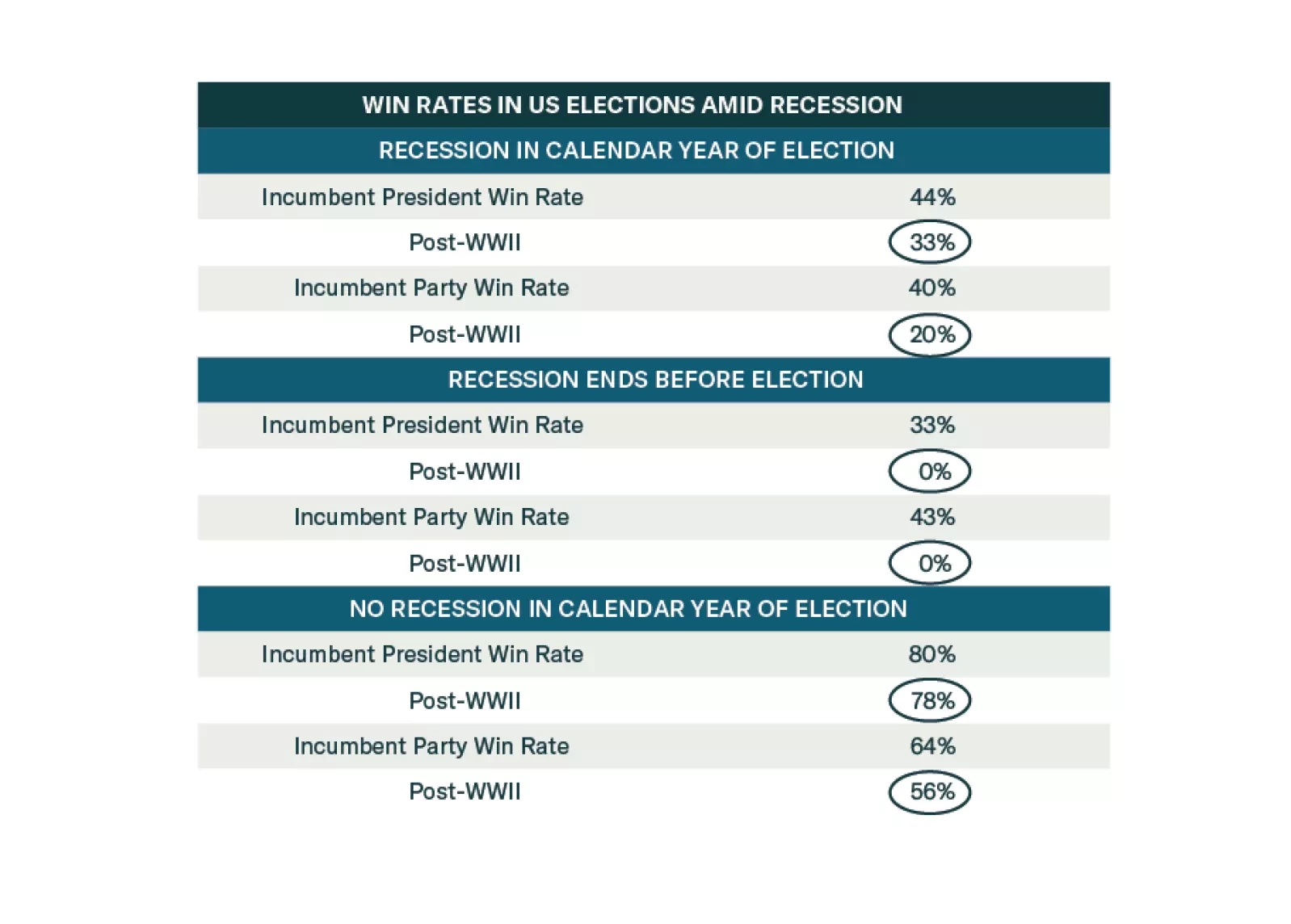

Democrats are favored to win the election until recession materializes. But recession risks are high. Investors should adopt a defensive and conservative strategy in 2024 amid extreme US policy uncertainty.

We enter 2024 as we were across the last four months of 2023, tactically equal weight across the board until the S&P 500 rally is complete and we gain a better entry point for underweighting equities and overweighting fixed income.

Treasury yields will sketch out a range between now and Q1 2024, with the upside determined by inflation and the downside determined by labor markets.