Labor Market

As expected, US personal income growth moderated from an upwardly revised 0.4% to 0.2% in October. However, disposable personal income growth experienced a less pronounced slowdown from 0.4% to 0.3% -- particularly in real terms which expanded for the first…

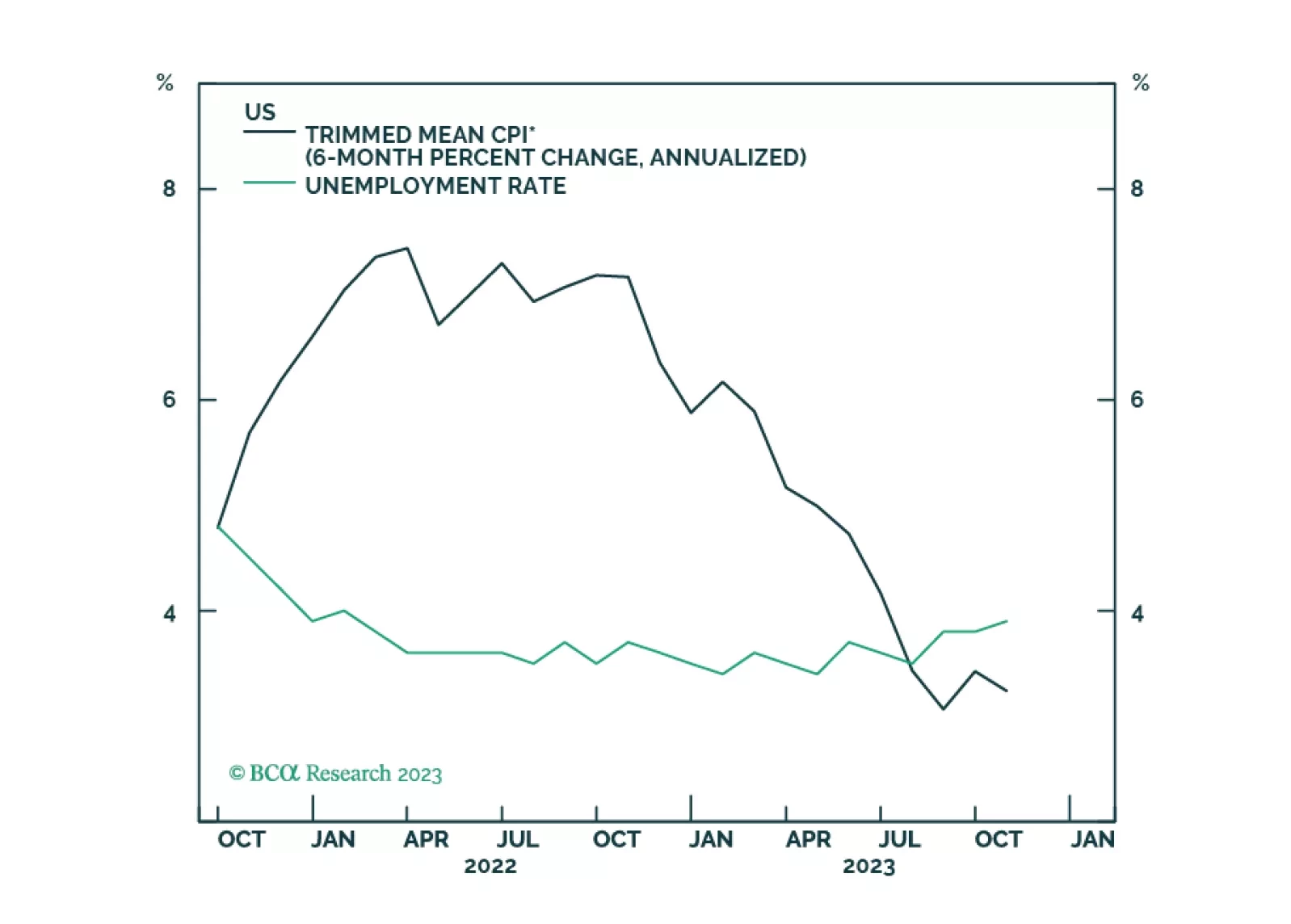

According to our Global Investment Strategy (GIS) service, so far this year, inflation in the US has declined sharply even though employment growth has remained strong. There are many factors that have contributed to this constructive situation, including…

Today, we are sending you the BCA annual outlook for 2024. The report is an edited transcript of our recent conversation with Mr. X and his daughter, Ms. X, who are long-time BCA clients with whom we discuss the economic and financial market outlook for the next twelve months toward the end of each year.

The US flash PMI sent a mixed signal about economic activity in November. The Composite index was unchanged at 50.7 – beating expectations of a slight decline to 50.4. The stable reading comes on the back of a deterioration in manufacturing and a slight…

The US nonfarm payroll report is an important monthly data release that investors scrutinize for updates on the state of the US labor market and economy more broadly. In the current context, the updates help gauge whether the US economy is heading toward…

Our kinked Phillips curve framework predicted the immaculate disinflation of 2023. That same framework is now warning that the global economy is heading towards a recession in the second half of 2024.

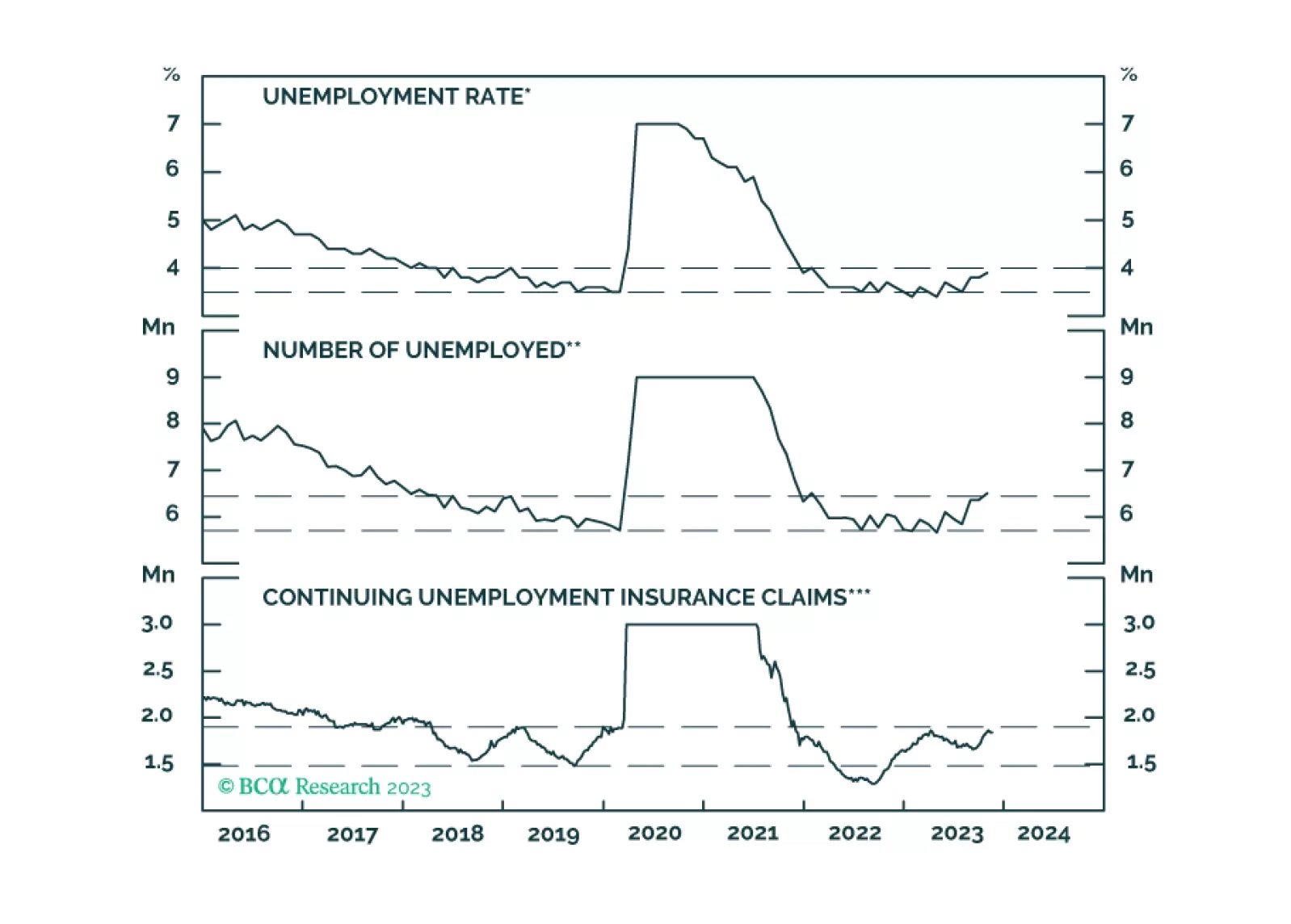

We investigate the recent increase in unemployment with the goal of determining whether it is flagging an imminent US recession.

US jobless claims have been trending higher in recent weeks, confirming that labor market conditions are deteriorating. Initial claims came in slightly above consensus estimates on Thursday, increasing by 231 thousand versus expectations of a 220 thousand…

To the extent that US small businesses are typically more exposed to domestic economic conditions than larger firms, results of the NFIB Small Business Economic Trends survey are instructive. One important trend is that the October survey results…

BCA Research's Global Investment Strategy service assigns 25% odds of the recession starting in 2025 or later. Our colleagues continue to think that the US will succumb to a recession in 2024, probably in the second half of the year. They see the…