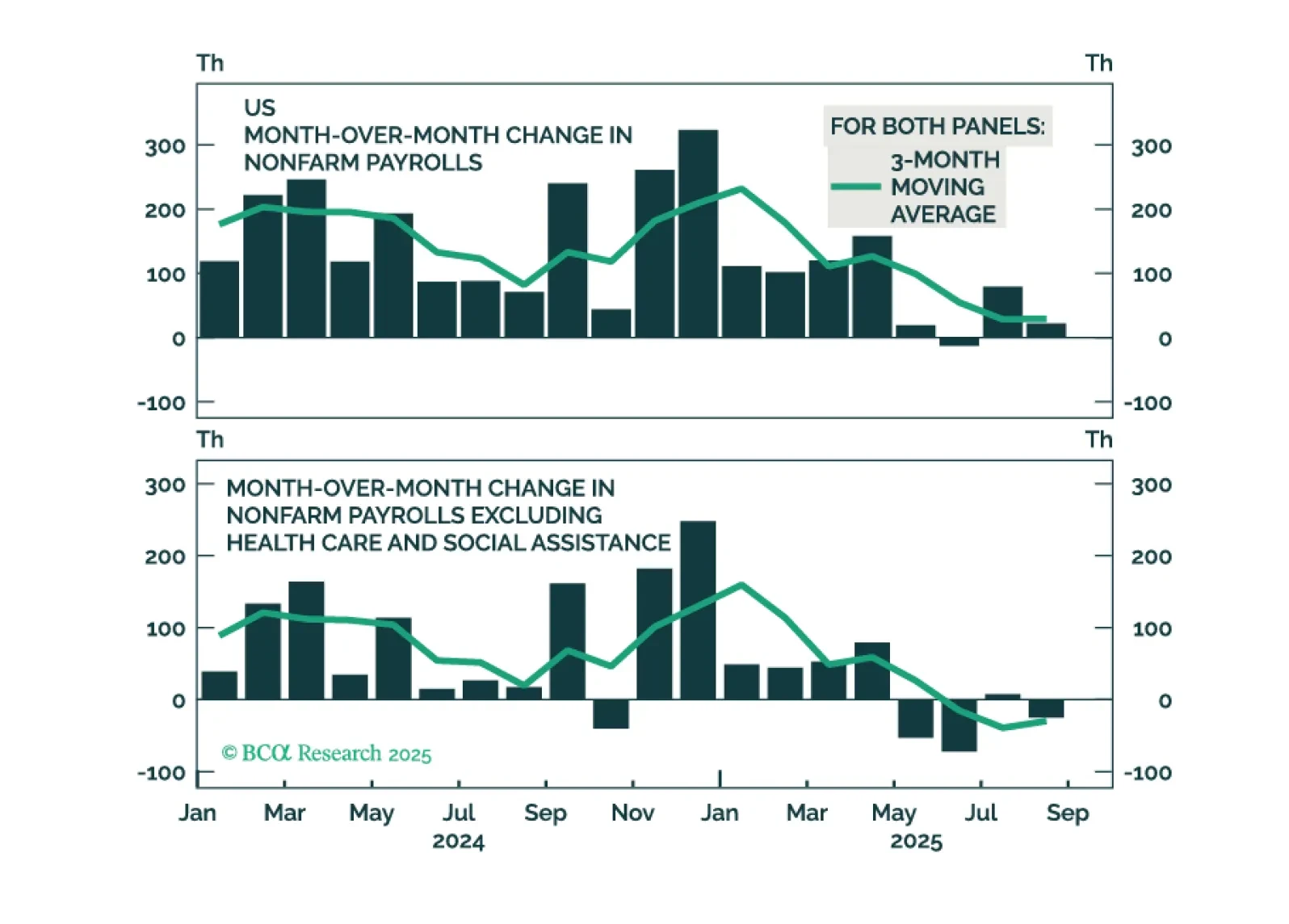

Labor Market

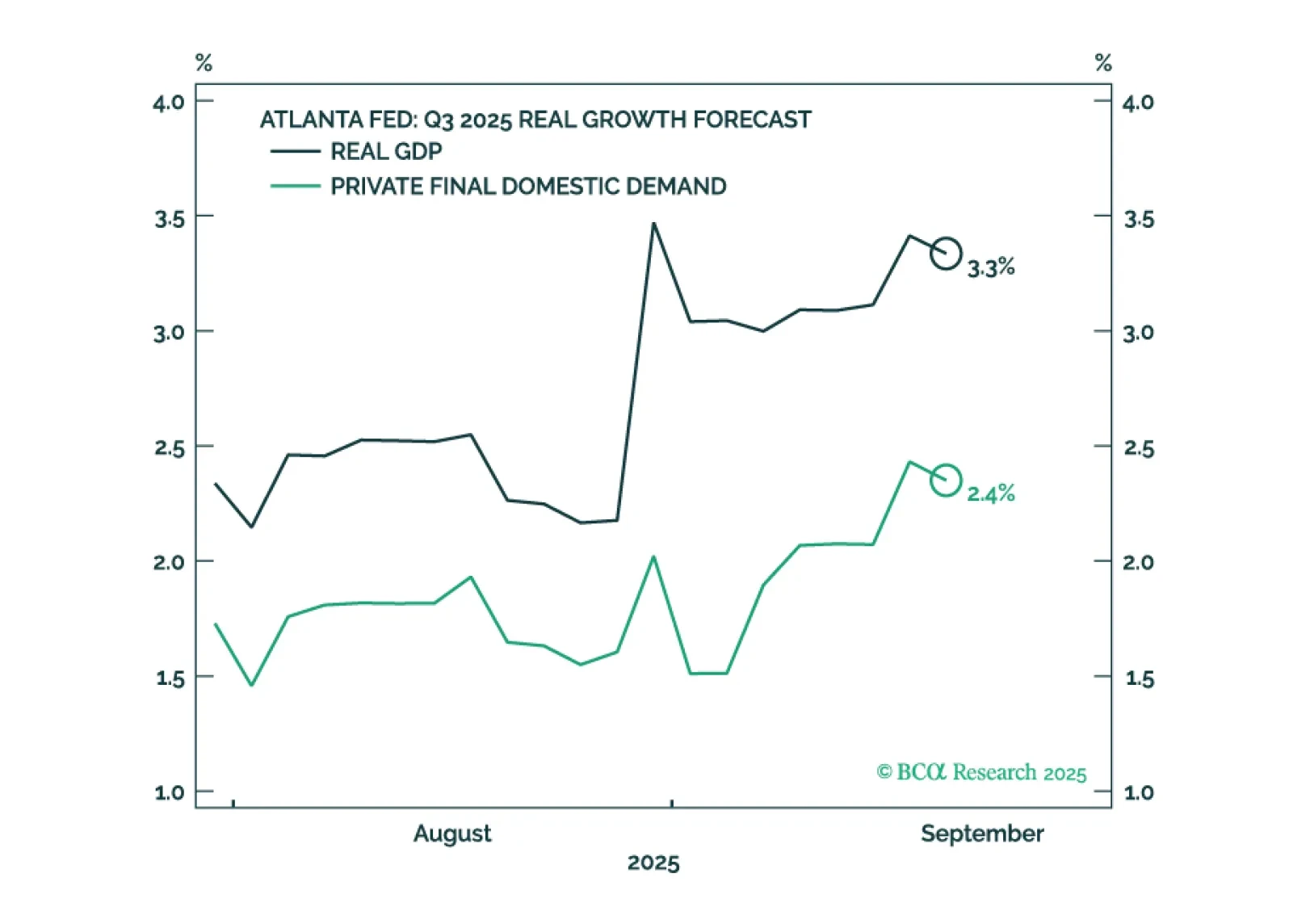

US GDP growth appears to have accelerated even as employment growth has faltered. We will make a final decision in early October when we publish our next Strategy Outlook, but most likely, we will cut our 12-month US recession probability to 40%-to-50% from 60% and turn tactically neutral on stocks, while still retaining a modest equity underweight over a 12-month horizon.

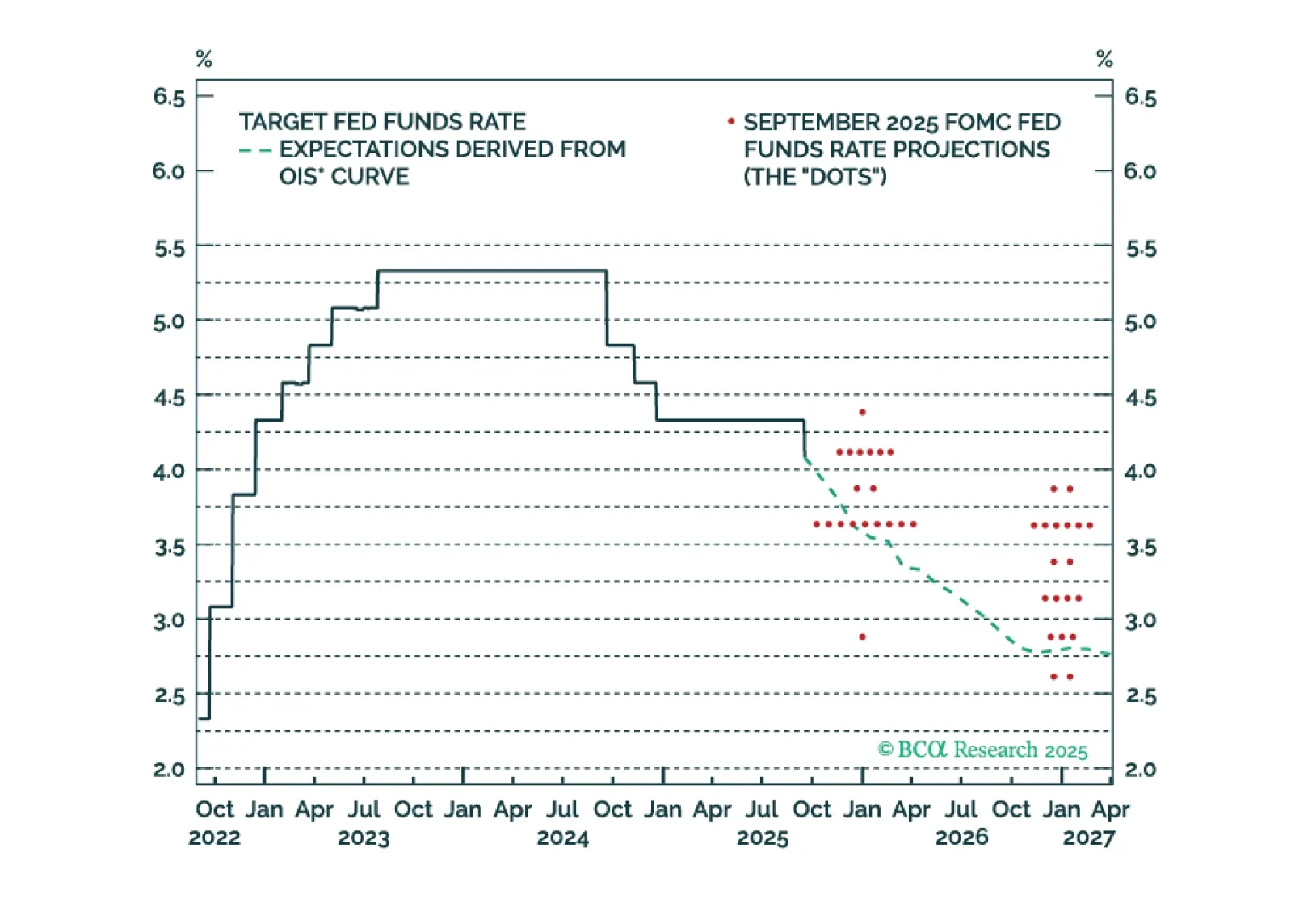

Median Fed unemployment rate projections are overly optimistic. The Fed will end up cutting more in 2026 than it currently anticipates.

While it is impossible to know exactly when global equities will peak, there are now enough vulnerabilities to justify keeping one’s finger near the eject button.

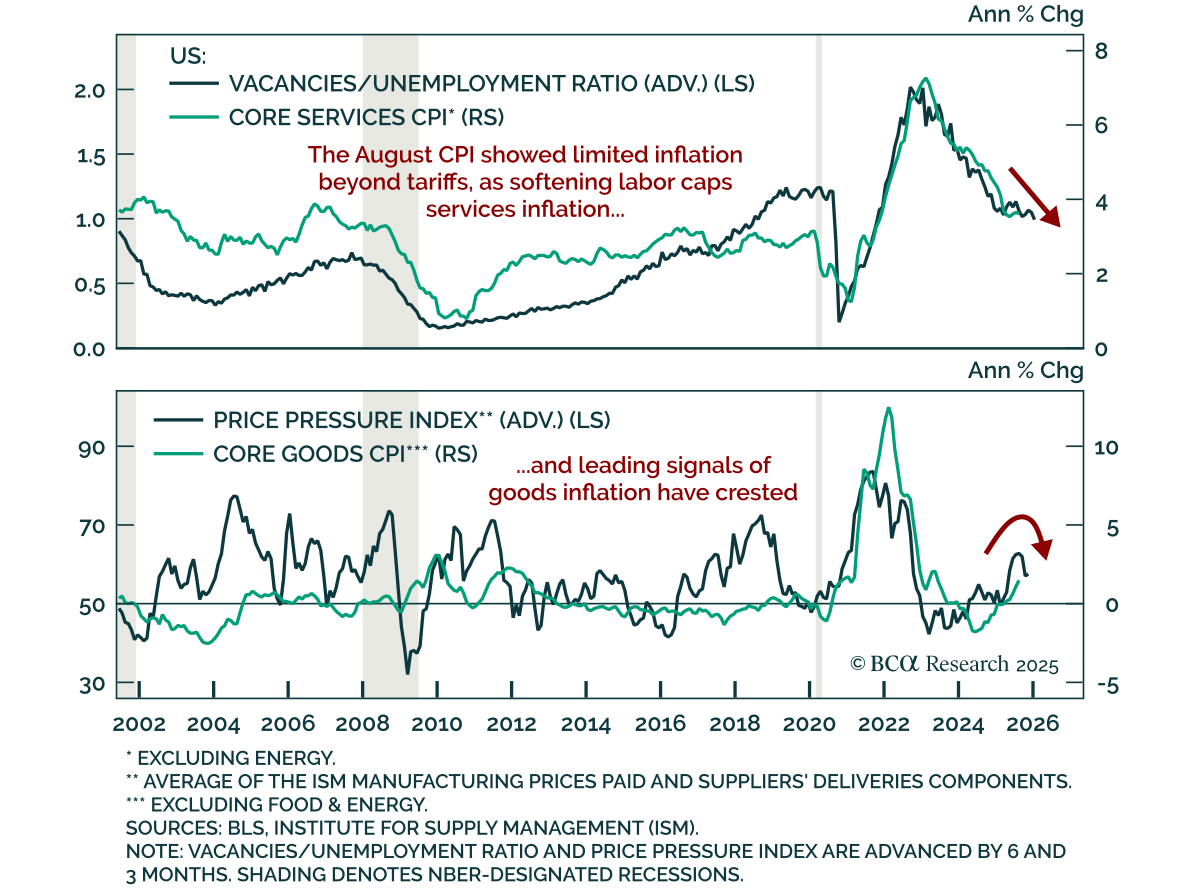

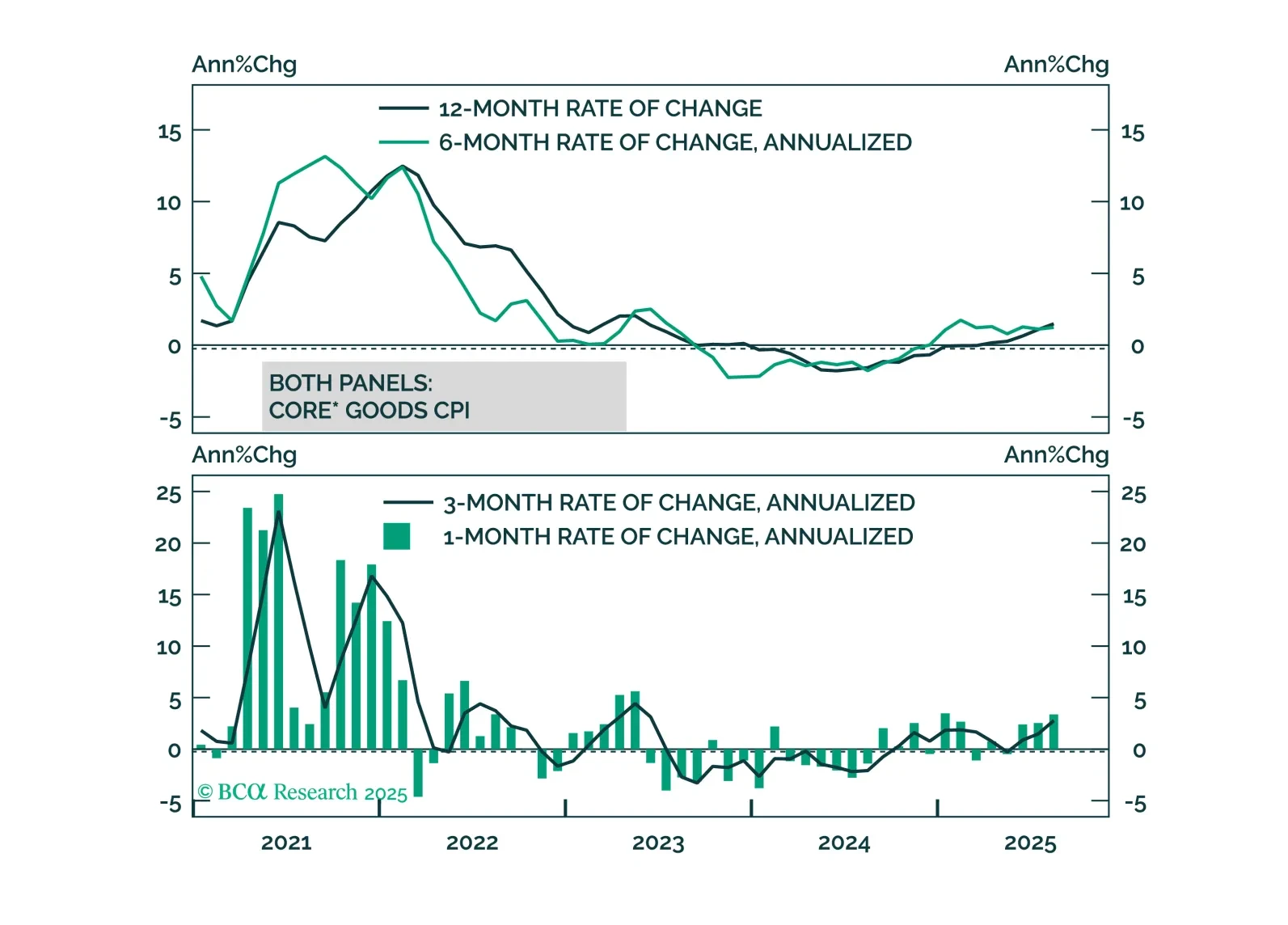

High US inflation is being driven by tariffs, not domestic inflationary pressure. This argues for Fed easing and a bull-steepening of the Treasury curve.

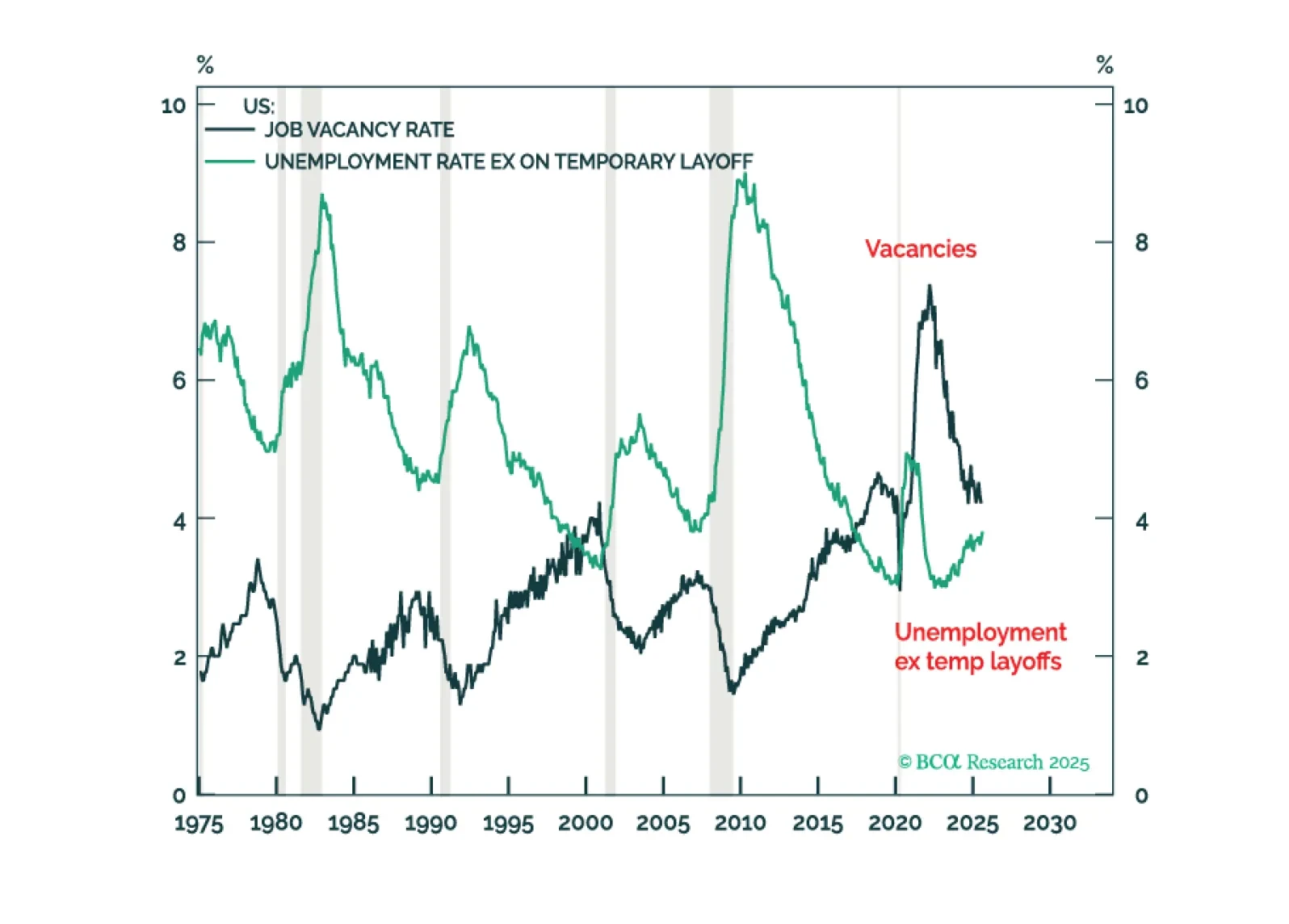

For the next few months at least, inflation risk trumps recession risk for both US markets and world markets. This because, correctly gauged, the US jobs market is still supply-constrained with ‘jobs looking for a worker’ exceeding ‘workers looking for a job’ by 0.4 percent. A still supply-constrained US jobs market cannot enter a demand-driven recession until it flips back to demand-constrained, so bond investors should underweight duration. Plus: a new tactical trade is overweight India (INDA).

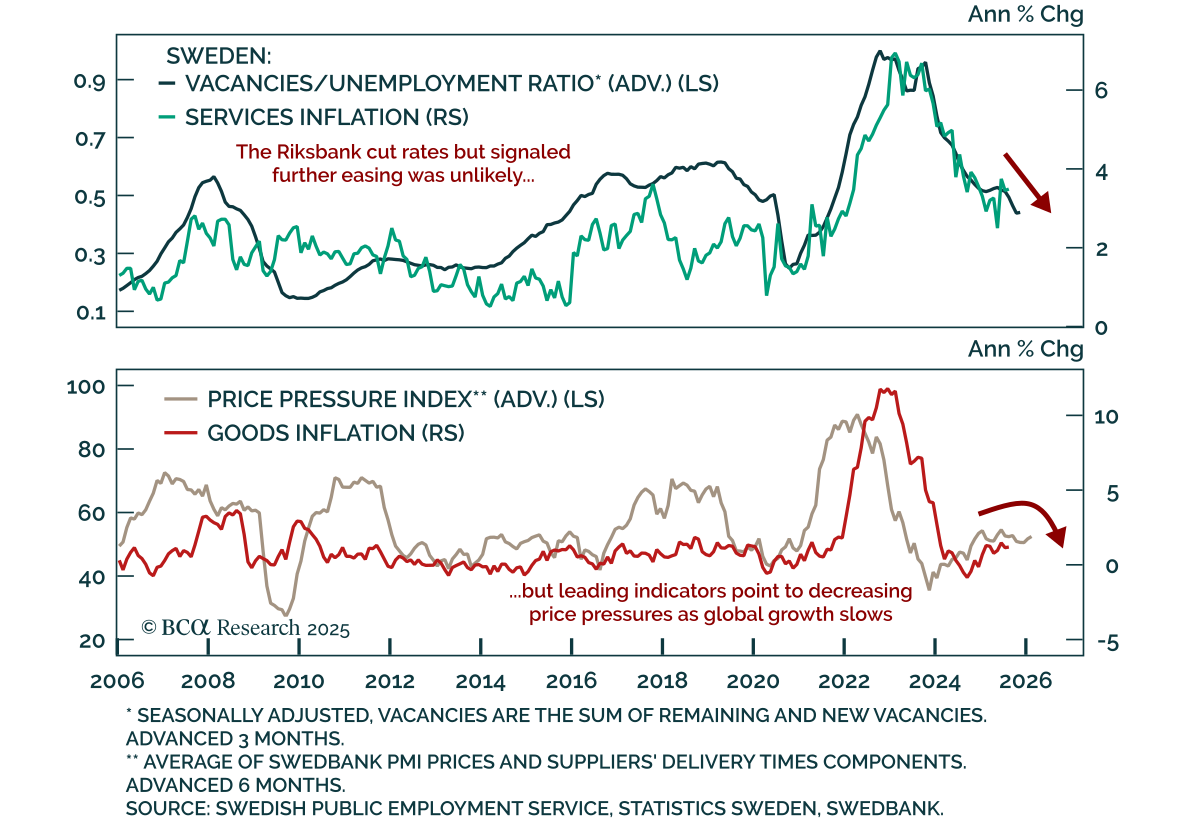

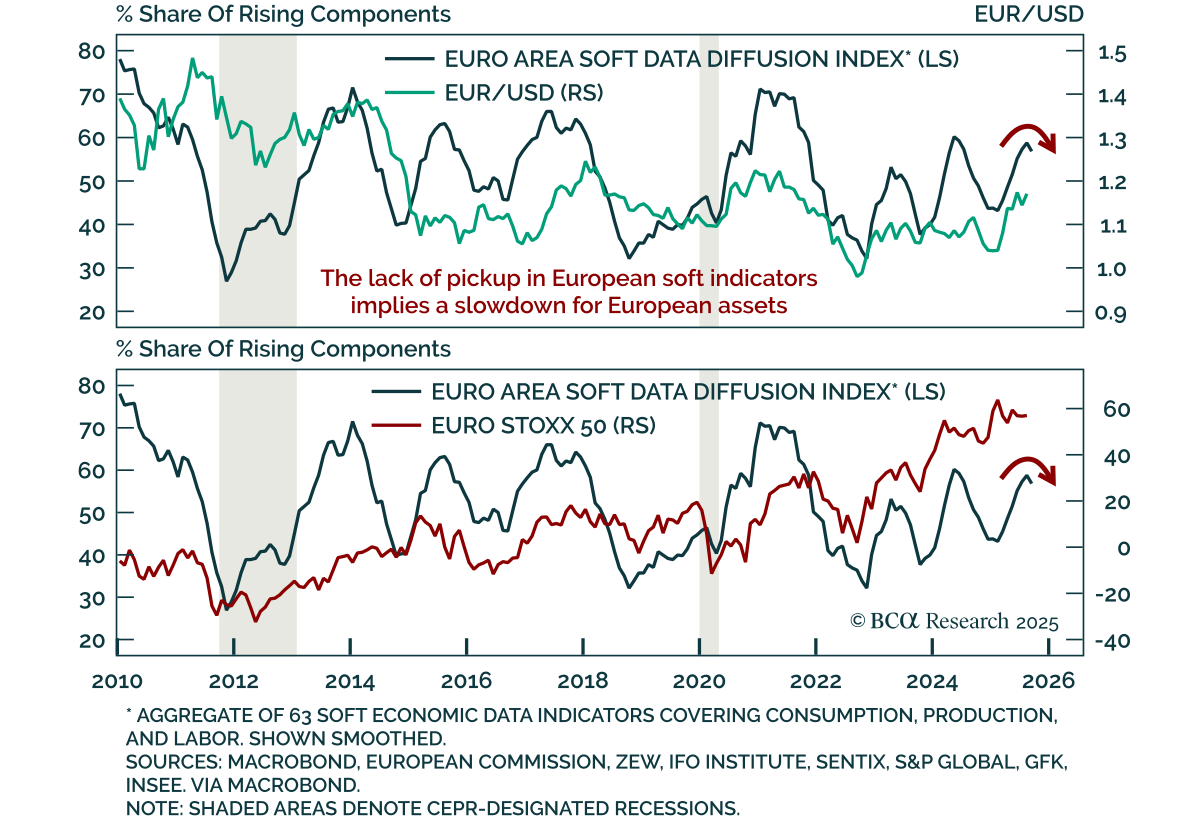

Core Europe’s industrial sector will relapse in the coming months due to US tariffs and a strong euro. Investors can play the imminent deflationary shock by being long Central European bonds. They should, however, hedge the currency risk vis-à-vis the euro.