Latin America

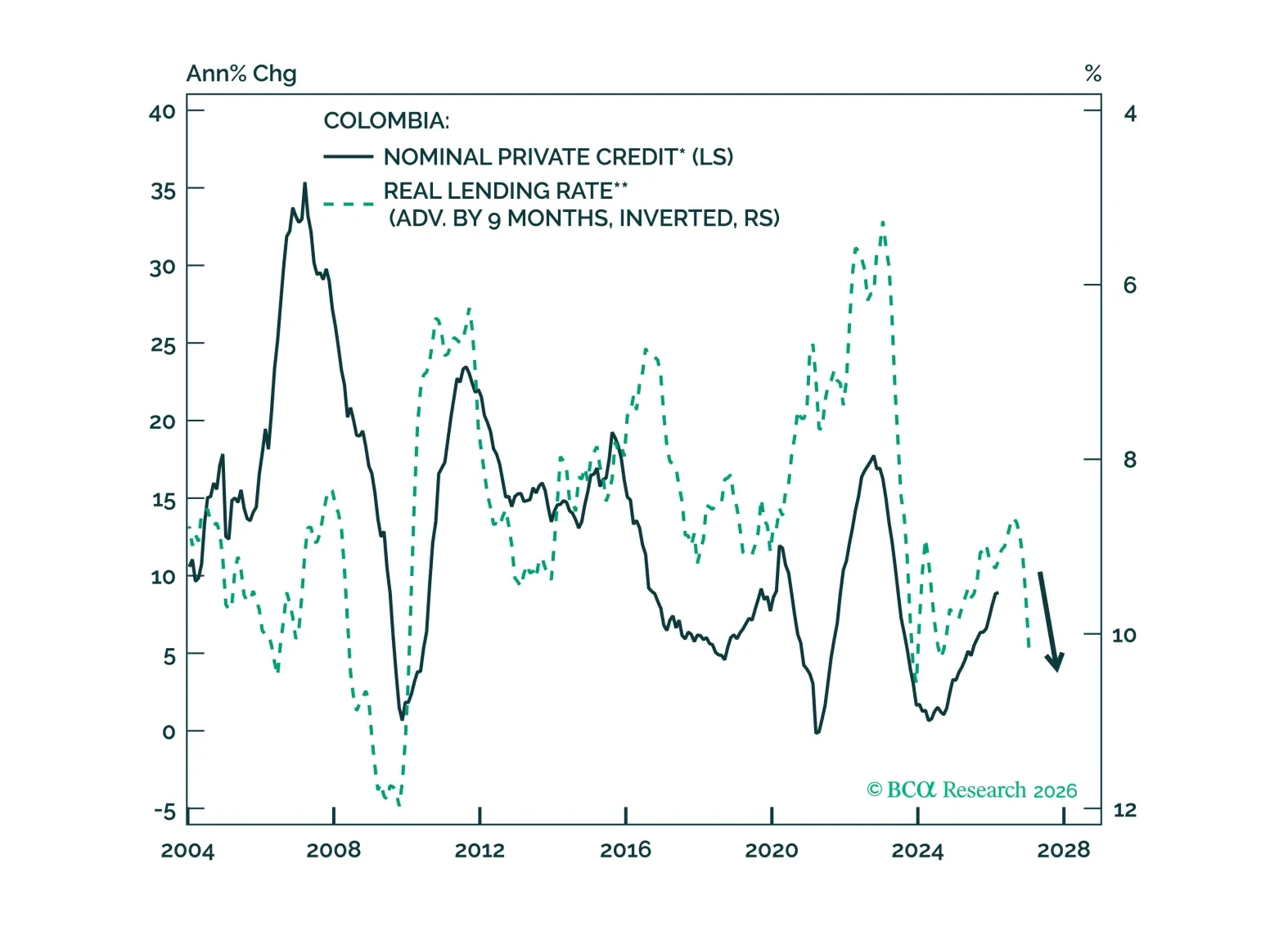

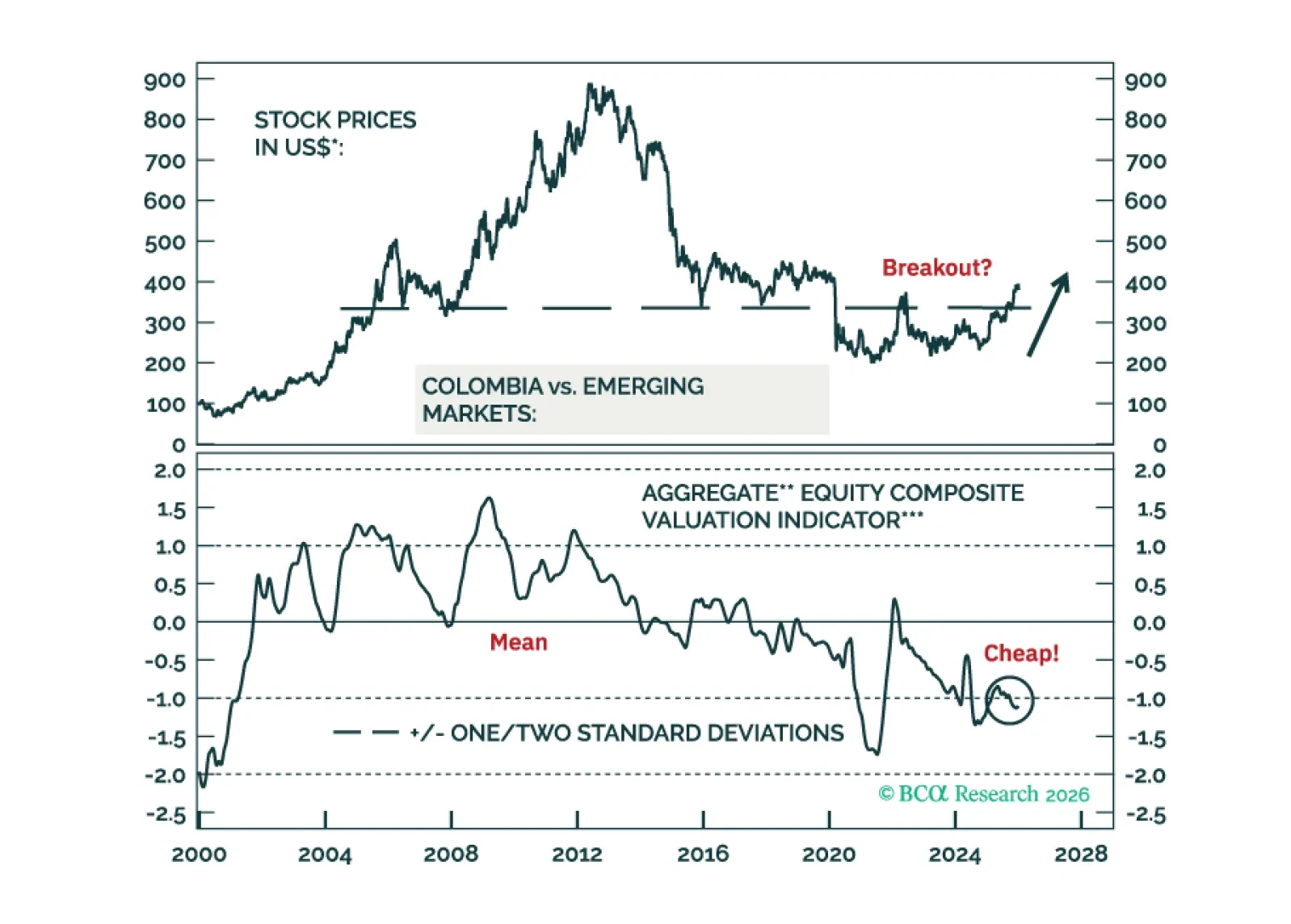

The rally in Colombia’s financial markets has a short shelf life. The election will bring a right-wing government, but it cannot fix inflation, fiscal arithmetic, or balance-of-payments vulnerabilities. Use the near-term rally to downgrade Colombian fixed income and equities.

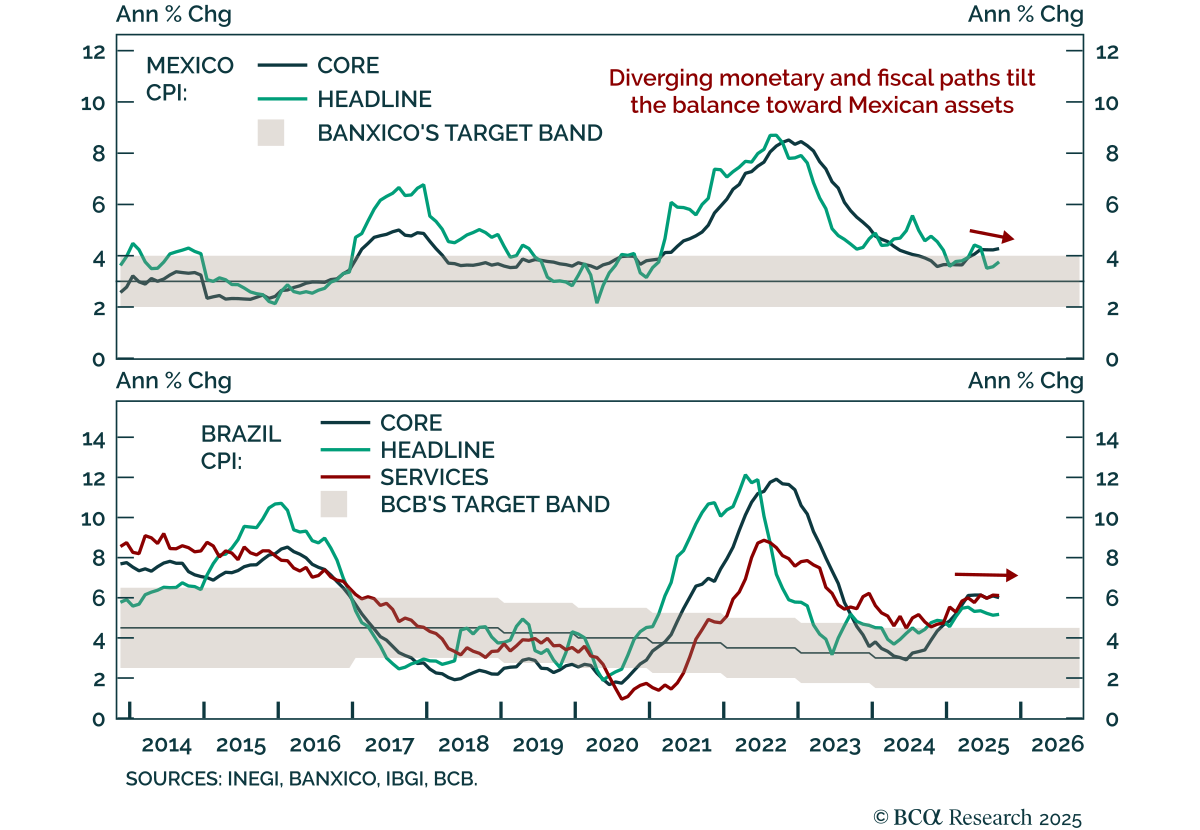

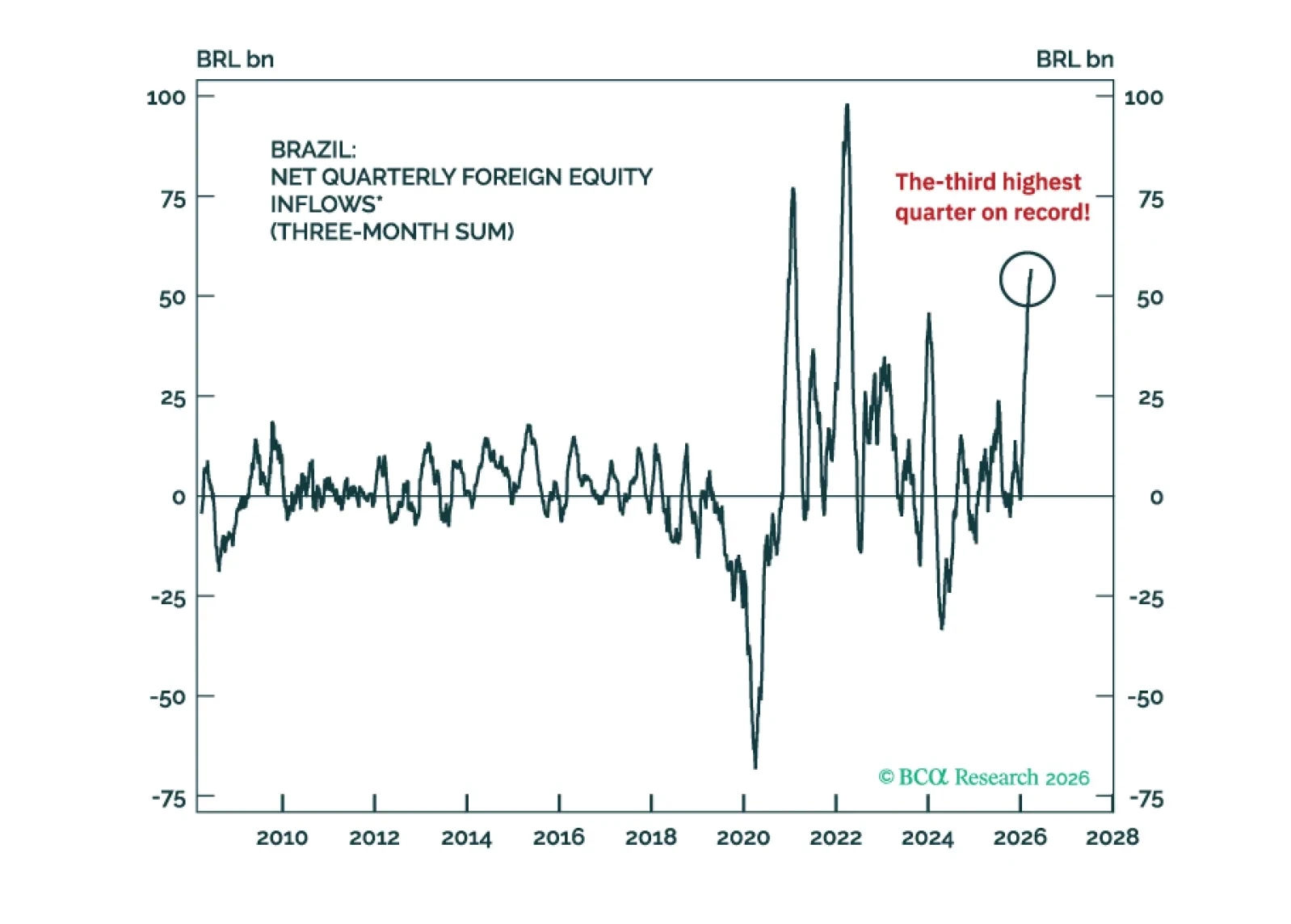

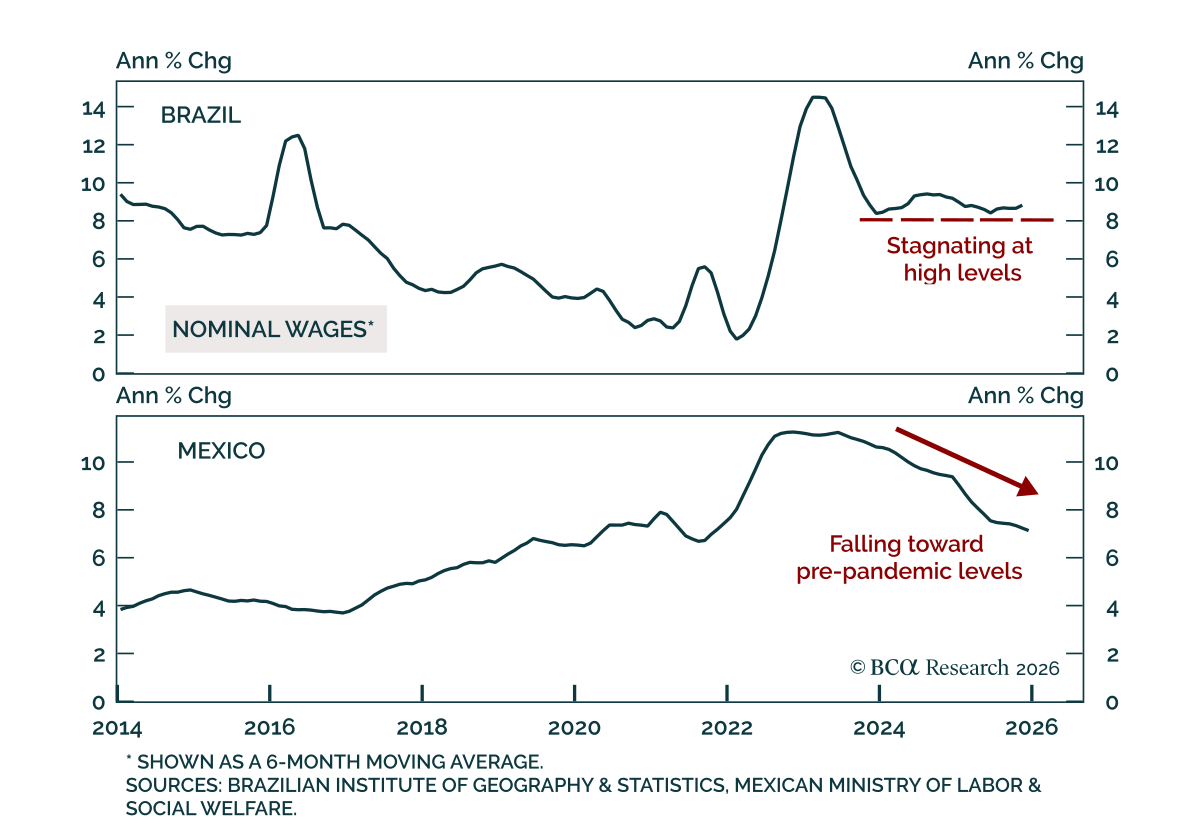

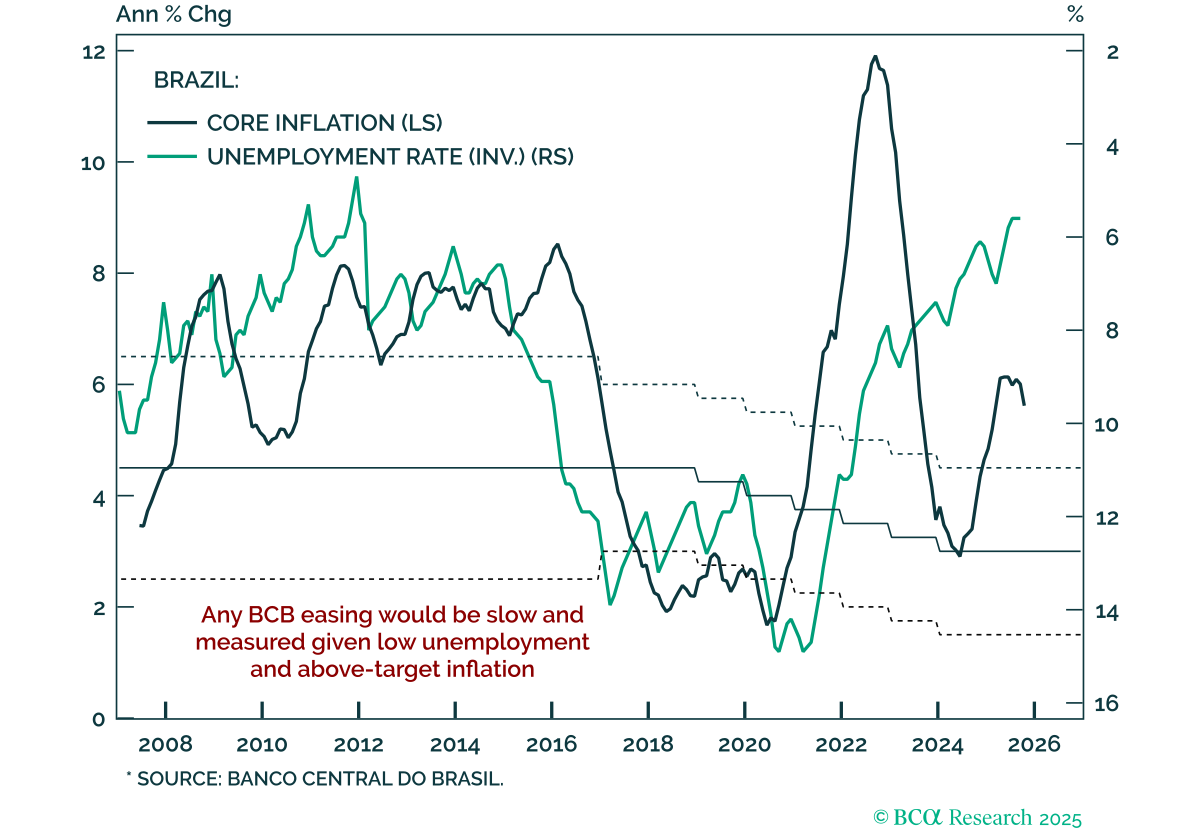

Overstretched foreign inflows into Brazilian markets will reverse, while soaring oil prices will not benefit Brazil in the near term. Avoid the country’s risk assets and the BRL, and stay underweight Brazilian equities and fixed income relative to EM. We also recommend paying 10-year Brazilian swap rates.

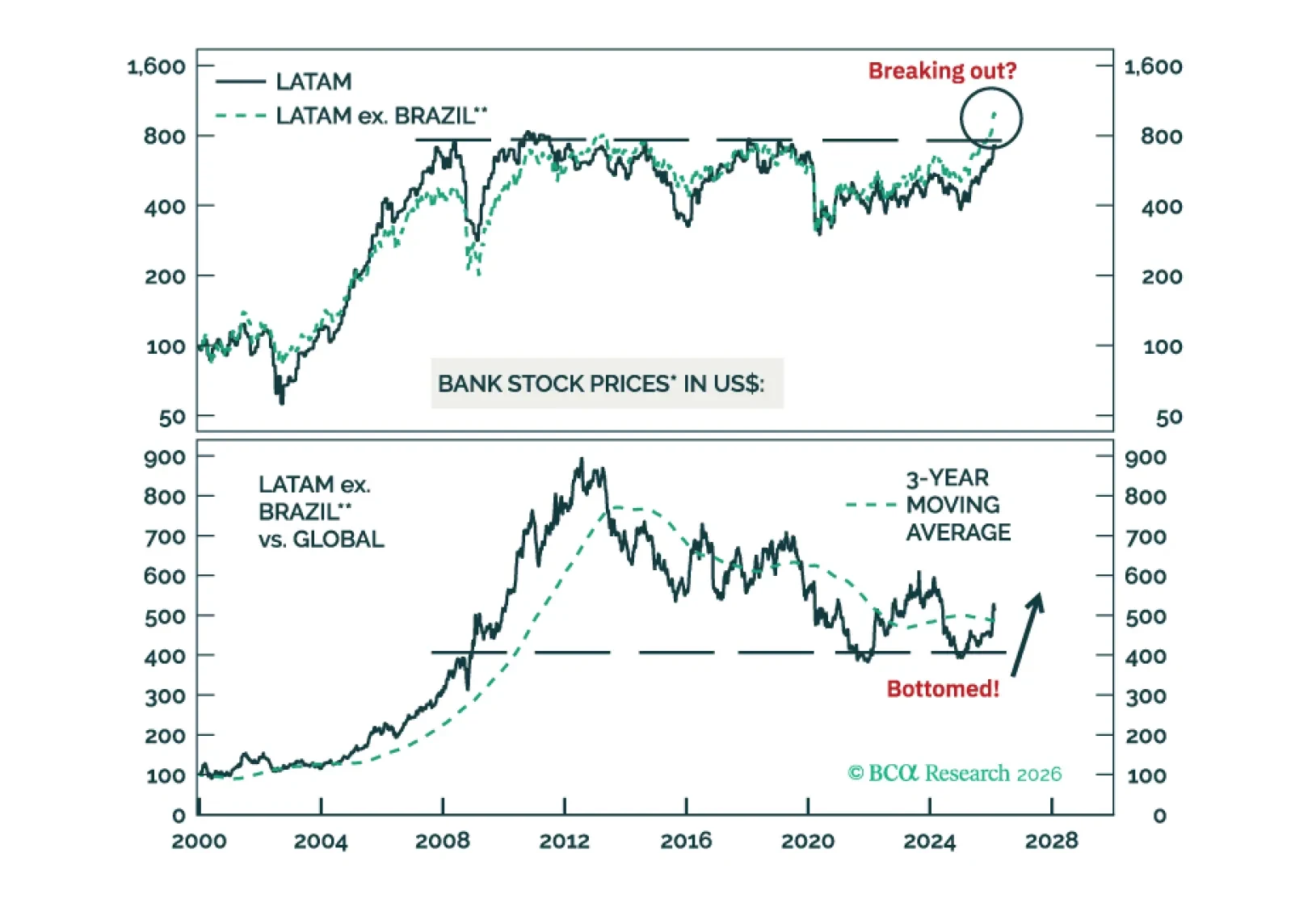

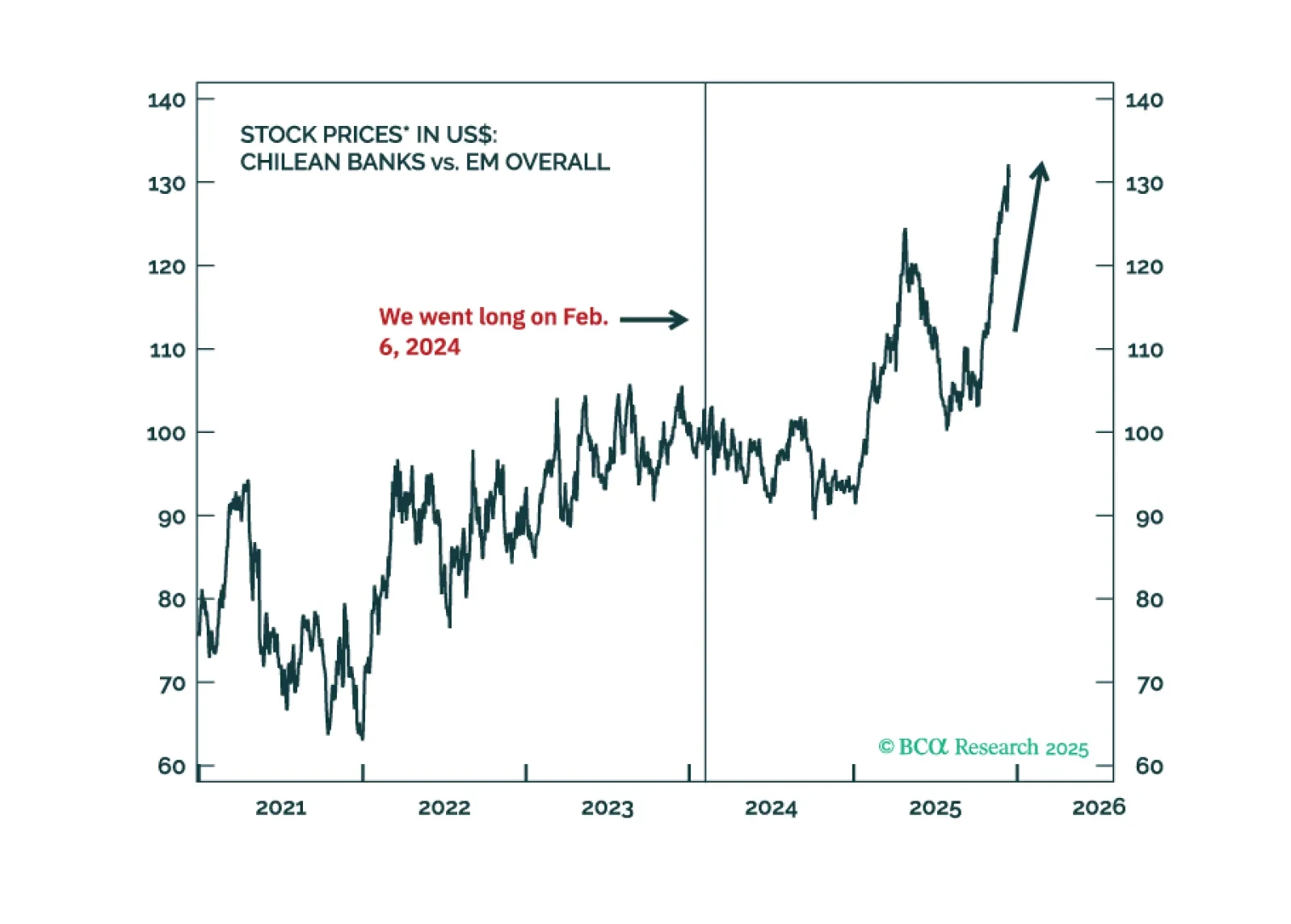

Go long LATAM ex. Brazil banks / short global bank stocks. Brazilian bank equities will underperform due to poor and worsening macro fundamentals.

There will be little market and macro implications from the US intervention in Venezuela. Fade away any near-term moves in global oil markets. However, Colombian and Peruvian assets will benefit from lower political risk premiums. We are upgrading Colombian equities and fixed income to overweight versus EM.

Following this weekend's election, we reiterate an overweight stance across Chilean risk assets relative to EM benchmarks and advise buying local currency government bonds (currency unhedged).

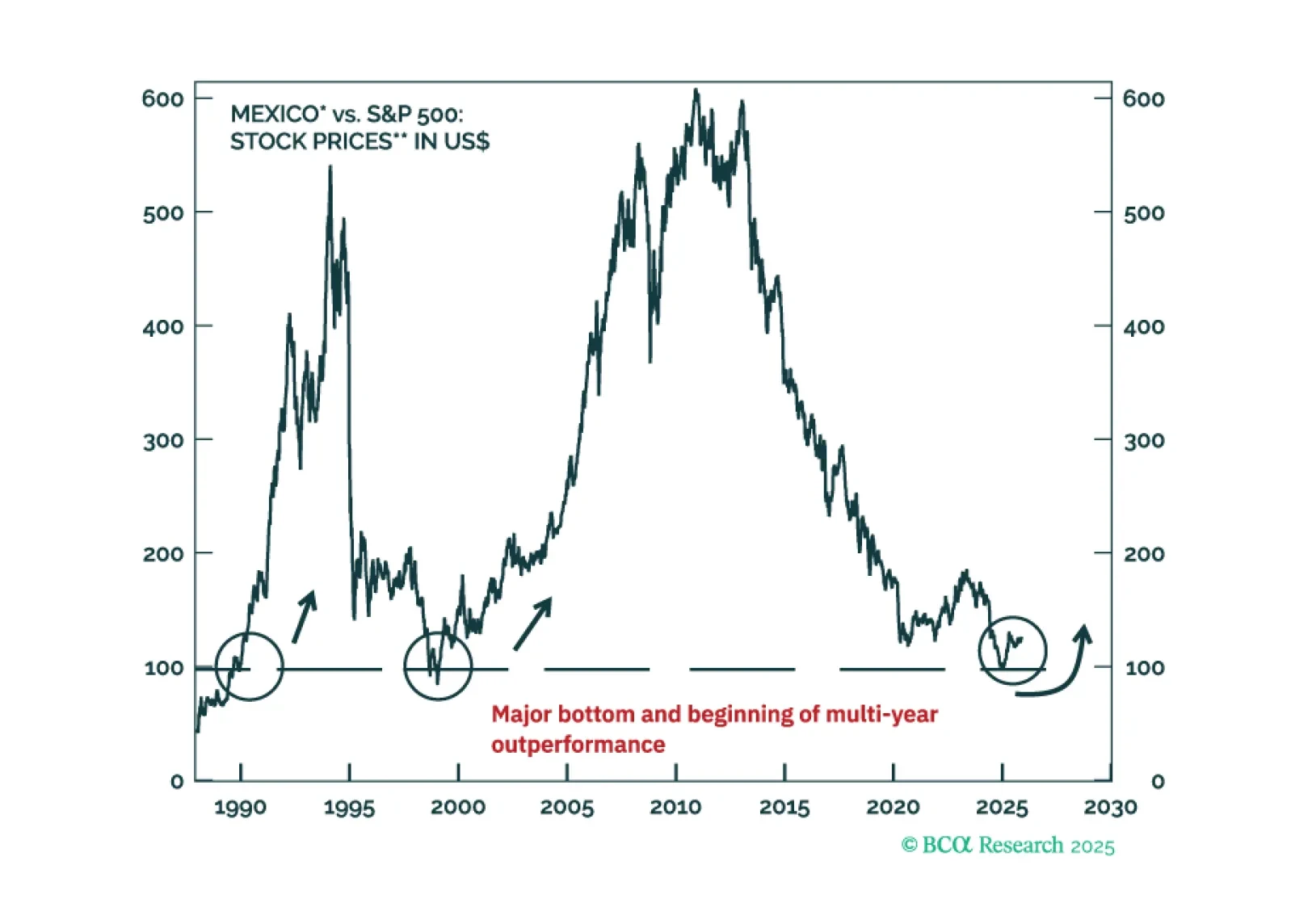

Mexican equity and fixed-income markets will continue outperforming their EM counterparts, regardless of whether global risk assets sell off or not. Also, we recommend a new trade: long Mexican stocks / short the S&P 500.

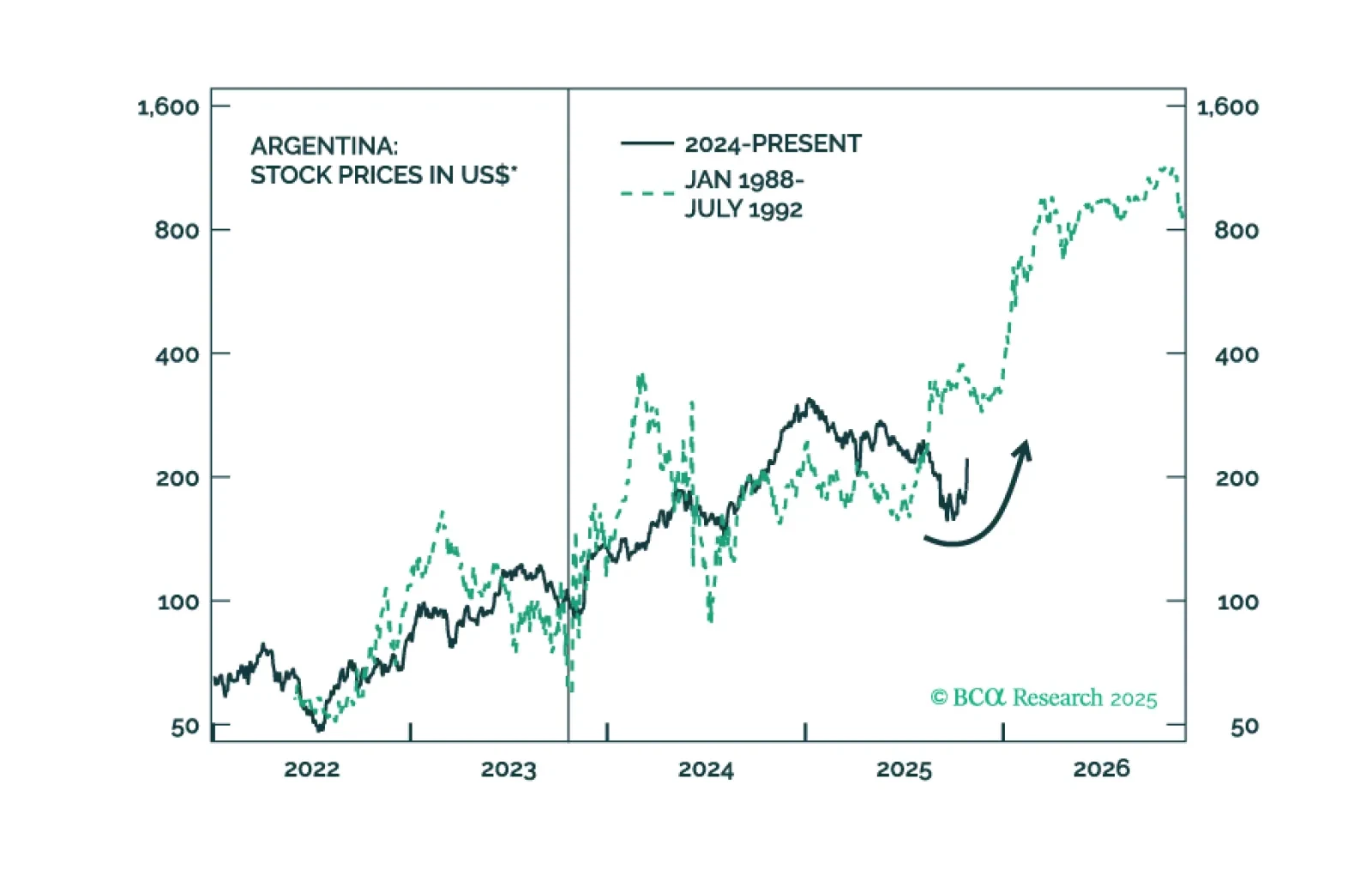

President Javier Milei’s electoral win has massively outperformed expectations. Meaningful legislative support and renewed market confidence will revitalize his liberalizing economic program. Our recommendation not to sell Argentine assets following the post-Buenos Aires election carnage has been validated.