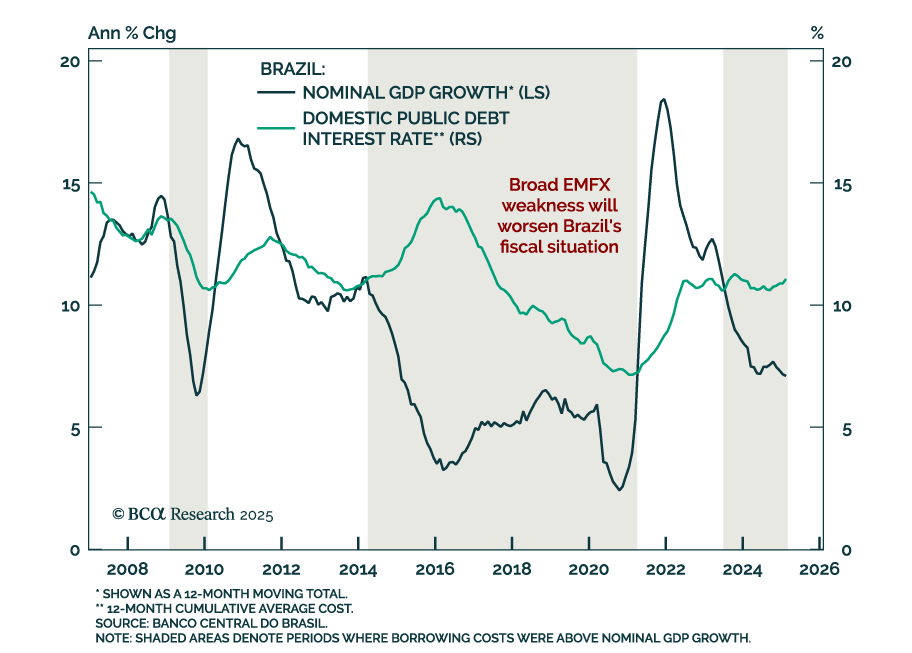

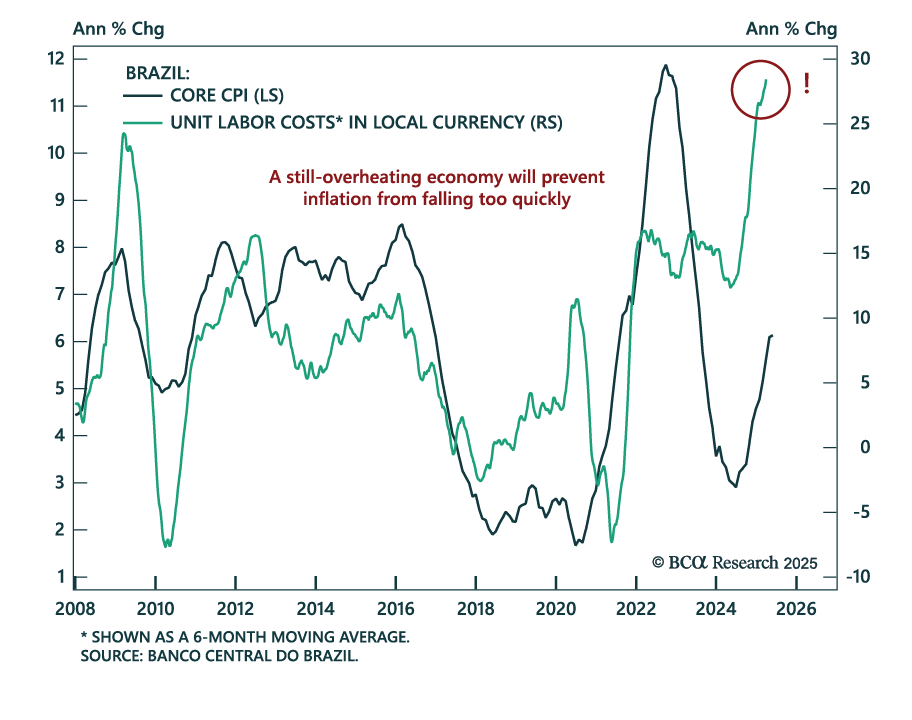

Latin America

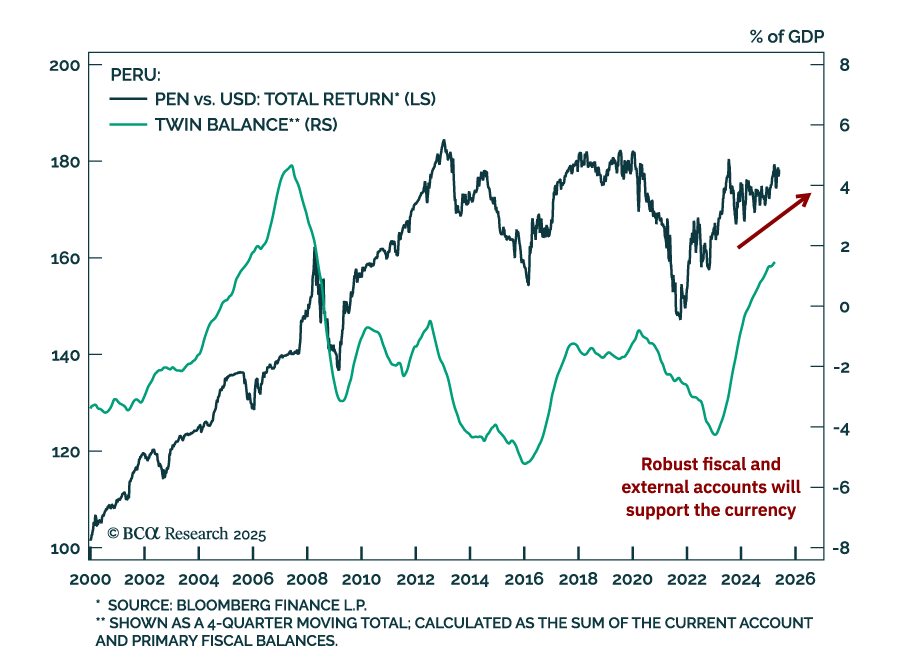

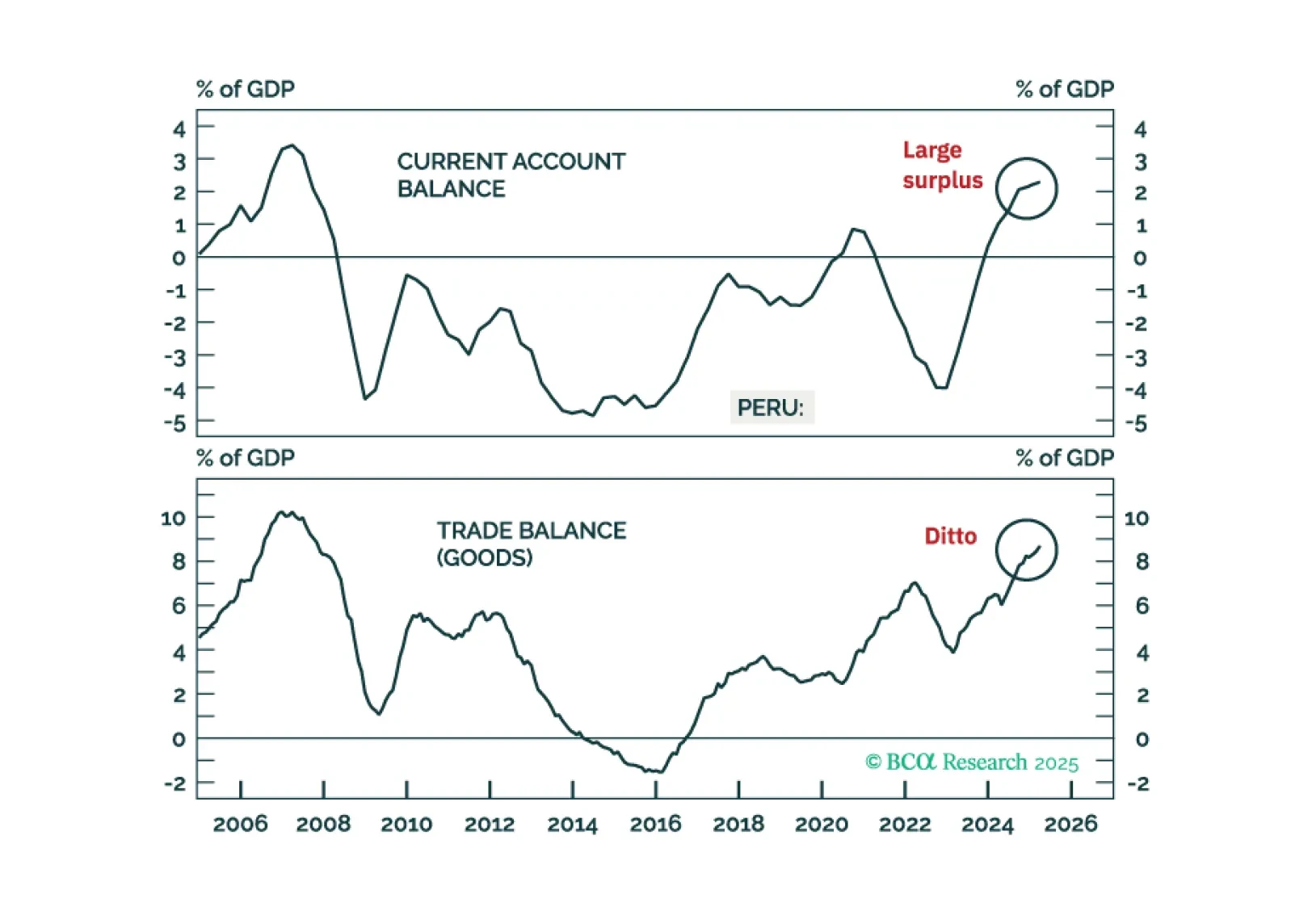

Peru’s economic resilience will help its markets outperform their EM peers. Domestic macro fundamentals are robust, and strong external accounts will lead to a stable-to-strengthening currency versus the US dollar. Overweight Peruvian equities, local bonds, and sovereign credit relative to their respective EM benchmarks, and go long 10-year domestic bonds (currency unhedged).

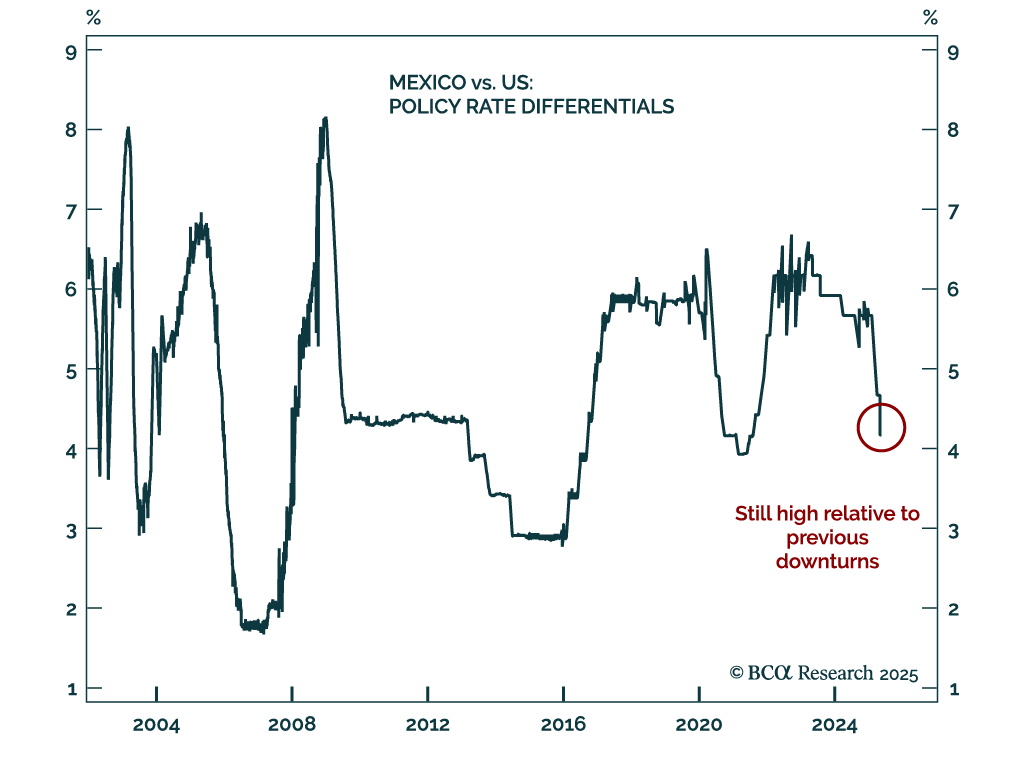

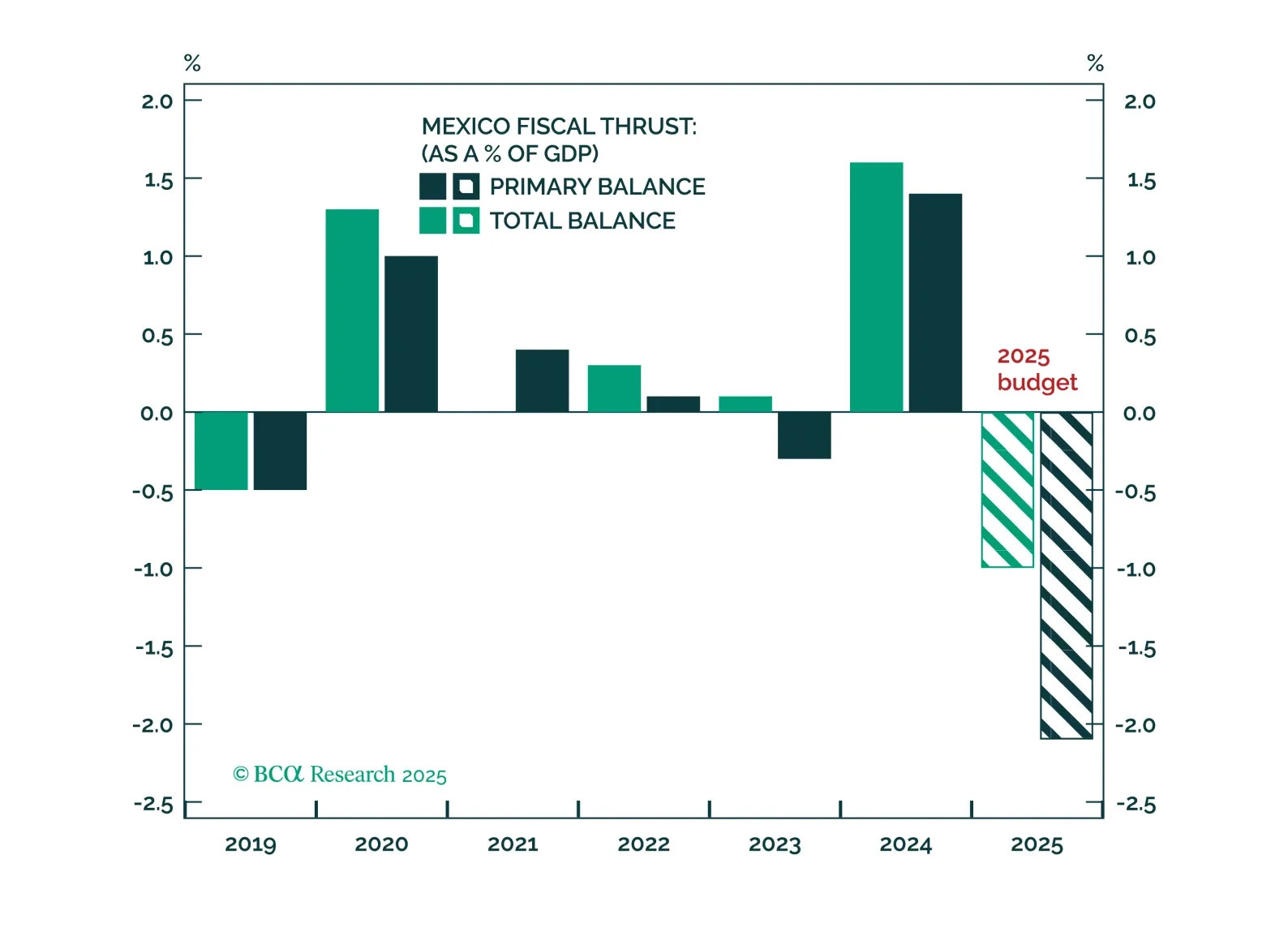

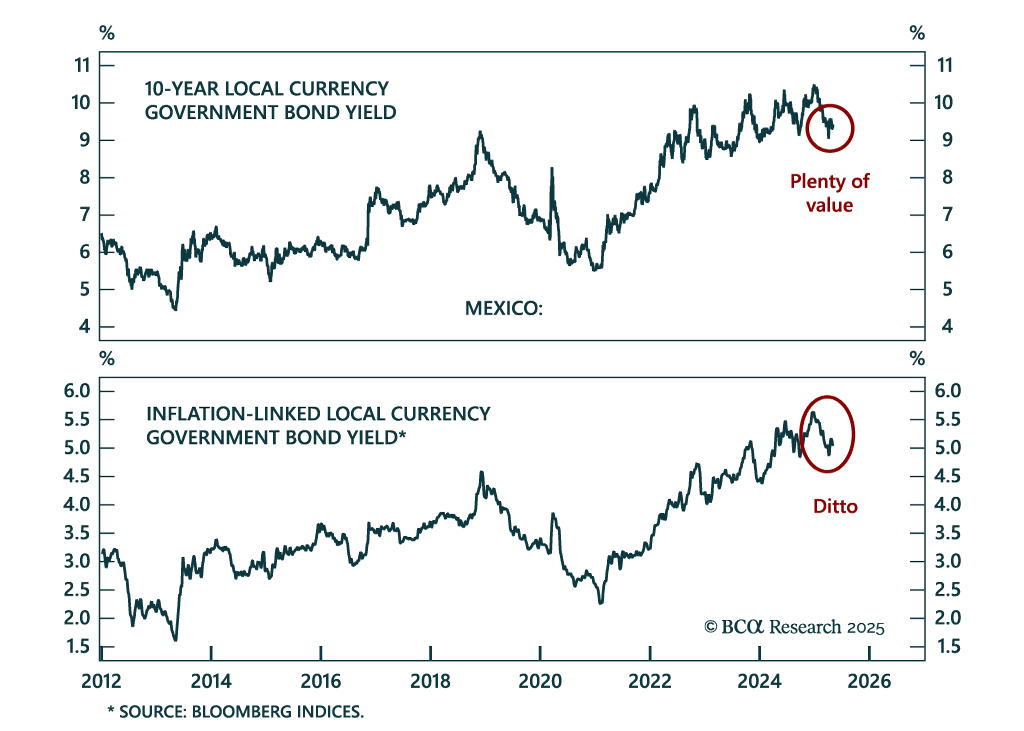

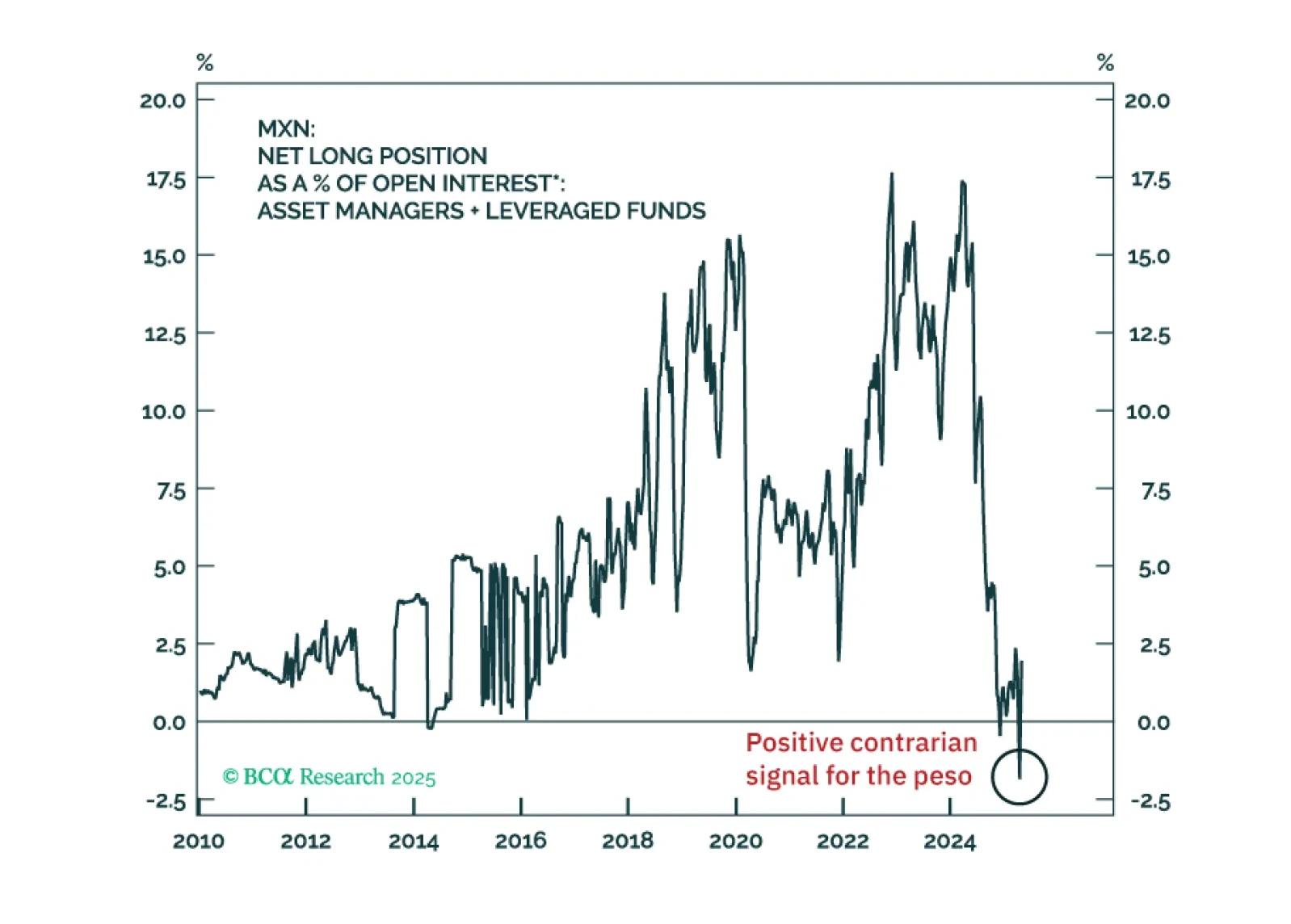

Short-term pain from Trump-related concessions, fiscal tightening amid a US and Mexican slowdown, and rising labor slack will weigh further on Mexican assets. But long-run, policy direction will capitalize on the nearshoring trend and resume the trend of Mexican asset outperformance relative to other emerging markets.

In the long run, Mexico will emerge as one of the biggest winners of US tariffs as the US diversifies supply chains away from China. In the medium term, however, a US growth slowdown and tariffs will push Mexico into recession. In EM portfolios, we remain overweight Mexican equities, domestic bonds, and sovereign credit. We are reiterating a buy on 10-year domestic bonds. Go long MXN versus CNH.

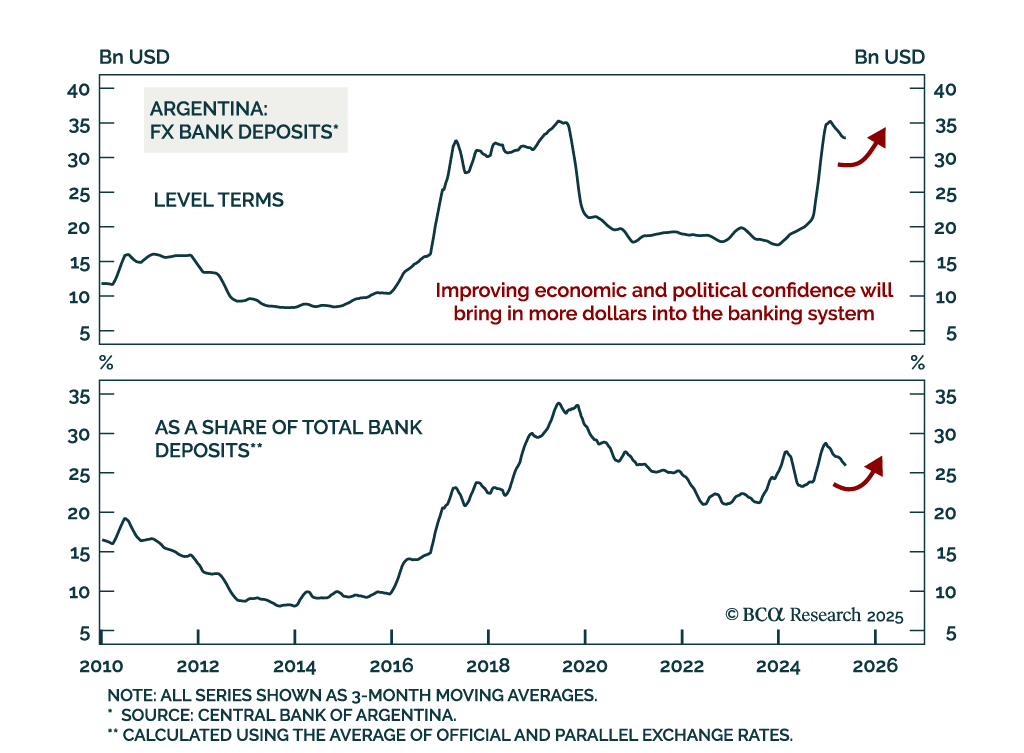

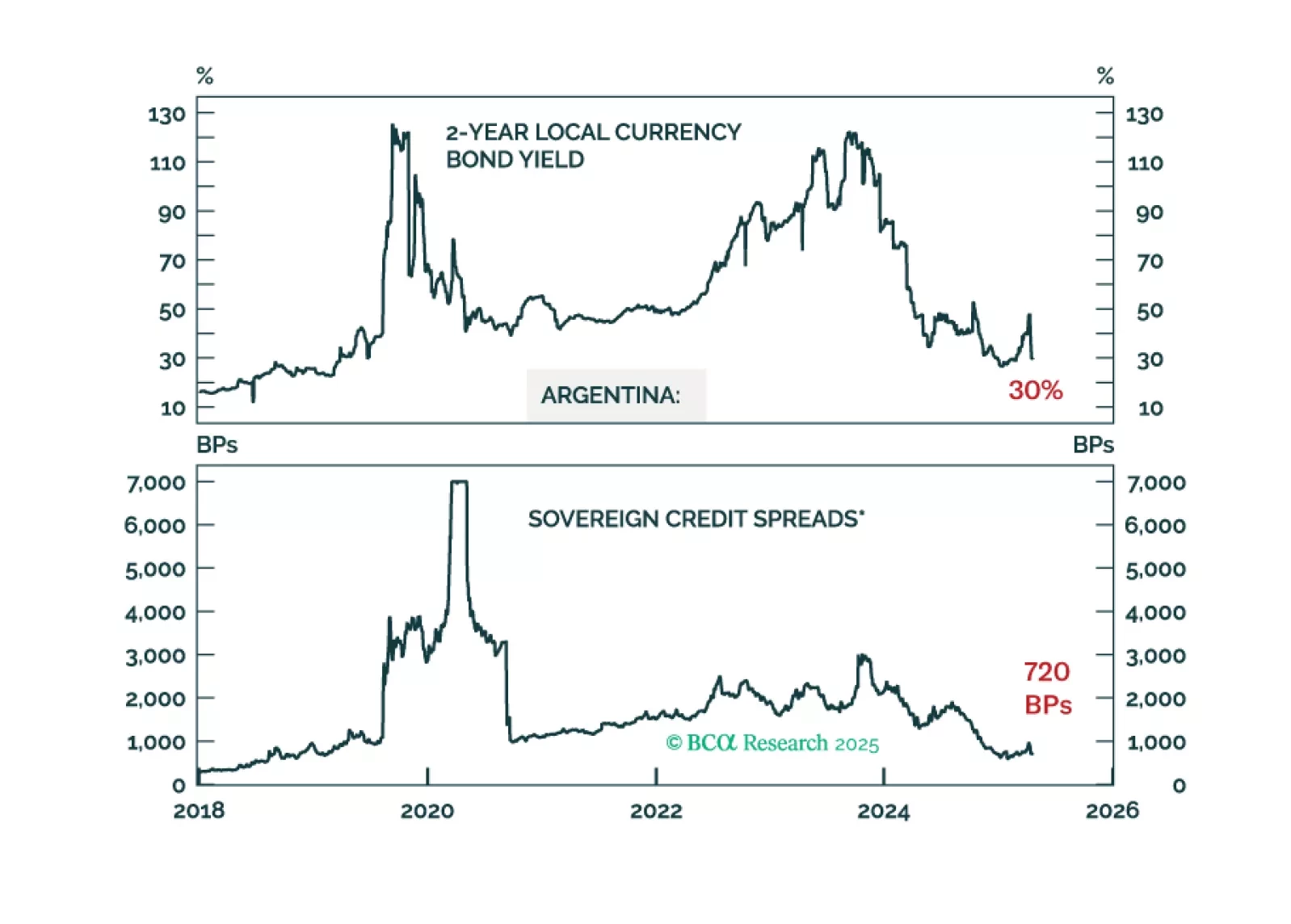

Amid the storm of global financial uncertainty, Argentina stands out as a free-market safe haven. The lifting of currency controls was the last step taken by this country to embrace market mechanisms. We recommend that investors buy Argentine equities, sovereign credit, and domestic bonds, and overweight Argentina within EM equity and fixed-income portfolios.